Plastic Tray And Container Market Size and Growth

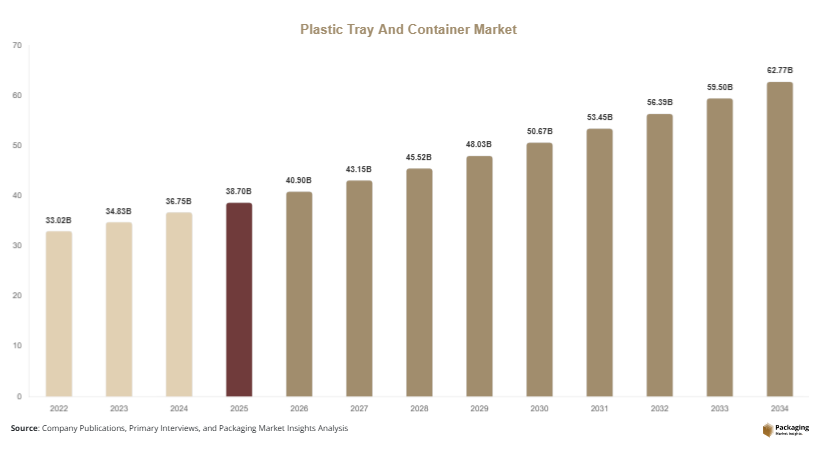

The global plastic tray and container market size is estimated at USD 38.7 billion in 2025 and is projected to reach approximately USD 40.9 billion in 2026. Over the forecast period, the market is expected to grow to USD 62.8 billion by 2034, registering a CAGR of 5.5% from 2025 to 2034. This growth reflects rising consumption of packaged goods and the ongoing need for efficient packaging formats that enhance product protection and shelf appeal. The plastic tray and container market continues to expand steadily, supported by increasing demand for durable, lightweight, and cost-effective packaging solutions across multiple industries.

A major growth factor is the expansion of the food and beverage industry, where plastic trays and containers are widely used for fresh produce, ready meals, and takeaway packaging. Their ability to preserve freshness, extend shelf life, and provide convenience makes them highly suitable for modern consumption patterns. Another key driver is the rapid growth of e-commerce and organized retail, which requires robust packaging solutions capable of withstanding transportation and handling. Plastic trays and containers offer structural integrity and cost efficiency, making them a preferred choice.

Key Highlights

- Asia Pacific dominated the market with a 39.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.1%.

- Polypropylene materials led the type segment with a 31.8% share, while recycled plastics are expected to grow at a CAGR of 6.4%.

- Thermoformed trays dominated the product segment with a 44.5% share, while injection-molded containers are forecasted to grow at a CAGR of 5.9%.

- Food & beverage applications led the segment with 47.3% share, while healthcare packaging is expected to grow at a CAGR of 6.2%.

- China remained the dominant country with a market size of USD 10.6 billion in 2025 and USD 11.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing adoption of recyclable and sustainable plastic materials

The plastic tray and container market is undergoing a gradual shift toward sustainable materials, driven by environmental concerns and regulatory pressure. Manufacturers are focusing on developing recyclable and reusable plastic packaging solutions to reduce environmental impact. The use of recycled polyethylene terephthalate and polypropylene is increasing, enabling companies to meet sustainability targets while maintaining product performance. Innovations in mono-material packaging are also gaining traction, as they simplify recycling processes and improve material recovery rates. Additionally, brands are adopting circular economy principles by integrating recycled content into packaging. This trend is expected to continue as companies strive to balance functionality with environmental responsibility.

Rising demand for convenience-driven and ready-to-eat packaging formats

Consumer preferences are shifting toward convenience-oriented packaging solutions, significantly influencing the plastic tray and container market. The growing demand for ready-to-eat meals, fresh-cut produce, and takeaway food is driving the adoption of plastic trays and containers. These packaging formats offer ease of handling, portion control, and extended shelf life, making them suitable for modern lifestyles. Innovations such as microwave-safe containers, tamper-evident lids, and compartmentalized trays are enhancing user experience. The expansion of food delivery services and online grocery platforms is further supporting this trend, as these applications require durable and lightweight packaging solutions.

Market Drivers

Growth of the global food processing and retail sectors

The expansion of the food processing and retail industries is a major factor driving the plastic tray and container market. Increasing urbanization and changing dietary habits are leading to higher consumption of packaged and processed foods. Plastic trays and containers are widely used for packaging fruits, vegetables, meat, and ready meals due to their durability and cost efficiency. Their ability to maintain product quality and extend shelf life is essential for food manufacturers and retailers. In addition, the growth of supermarkets and hypermarkets is increasing demand for standardized packaging formats that improve product visibility and storage efficiency.

Expansion of e-commerce and logistics infrastructure

The rapid growth of e-commerce and logistics networks is significantly contributing to the demand for plastic packaging solutions. Plastic trays and containers provide excellent protection during transportation, reducing the risk of product damage. Their lightweight nature helps lower shipping costs, making them suitable for online retail applications. The increasing popularity of home delivery services for groceries, pharmaceuticals, and consumer goods is further driving demand. Additionally, advancements in packaging design are improving stackability and space utilization, enhancing supply chain efficiency and supporting market growth.

Market Restraint

Environmental concerns and regulatory restrictions on plastic usage

The plastic tray and container market faces challenges due to growing environmental concerns and regulatory restrictions on plastic usage. The accumulation of plastic waste and its impact on ecosystems have led to increased scrutiny from governments and environmental organizations. Many countries are implementing policies to reduce single-use plastics and promote sustainable alternatives. These regulations can limit the use of conventional plastic materials and increase compliance costs for manufacturers. For instance, bans on certain types of plastic packaging in Europe and North America have prompted companies to invest in alternative materials and recycling technologies. While these initiatives support sustainability, they also create challenges for market growth by increasing operational complexity and costs.

Market Opportunities

Development of advanced recyclable and bio-based plastics

The development of advanced recyclable and bio-based plastics presents significant opportunities for the plastic tray and container market. Manufacturers are investing in research and development to create materials that offer the same performance as traditional plastics while being environmentally friendly. Bio-based plastics derived from renewable resources are gaining attention as sustainable alternatives. These materials can reduce carbon emissions and dependence on fossil fuels. As technology advances, the cost of producing bio-based plastics is expected to decrease, making them more accessible to a wider range of industries. This shift toward sustainable materials is likely to drive market growth.

Increasing demand from healthcare and pharmaceutical packaging

The healthcare and pharmaceutical sectors offer substantial growth opportunities for the plastic tray and container market. The need for safe, hygienic, and tamper-proof packaging is driving the adoption of plastic containers in medical applications. These containers are used for packaging medical devices, diagnostic kits, and pharmaceutical products. Their durability and ability to maintain sterility make them suitable for healthcare use. The expansion of healthcare infrastructure and rising demand for medical products are further supporting market growth. Additionally, innovations in packaging design are improving product safety and usability, creating new opportunities for manufacturers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 38.7 Billion |

| Market Size in 2026 | USD 40.9 Billion |

| Market Size in 2034 | USD 62.8 Billion |

| CAGR | 5.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material

Polypropylene dominated the plastic tray and container market in 2024, accounting for approximately 31.8% of the total share. This material is widely used due to its strength, flexibility, and resistance to heat and chemicals. Polypropylene trays and containers are commonly used in food packaging applications, as they can withstand high temperatures and are suitable for microwave use. Additionally, the material’s cost-effectiveness and availability make it a preferred choice for manufacturers. The growing demand for durable and lightweight packaging solutions further supports the dominance of polypropylene in the market.

Recycled plastics are expected to grow at the fastest CAGR of 6.4% during the forecast period. The increasing focus on sustainability and circular economy practices is driving demand for recycled materials. These plastics help reduce environmental impact by minimizing waste and conserving resources. Advances in recycling technologies are improving the quality and performance of recycled plastics, making them suitable for various applications. As regulatory pressure increases, the adoption of recycled materials is expected to rise significantly.

By Product Type

Thermoformed trays accounted for the largest market share in 2024, representing 44.5% of the total market. These trays are widely used due to their cost efficiency and versatility. Thermoforming allows for the production of lightweight and customizable packaging solutions, making it suitable for various applications, including food and consumer goods. The ability to produce trays in different shapes and sizes enhances their appeal among manufacturers.

Injection-molded containers are expected to grow at the fastest CAGR of 5.9%. These containers offer superior strength and durability, making them suitable for applications requiring high structural integrity. The increasing demand for rigid packaging solutions in industries such as healthcare and electronics is driving the growth of this segment.

By Application

The food and beverage segment dominated the market in 2024, accounting for 47.3% of the total share. The increasing demand for packaged and ready-to-eat food products is a key factor driving this segment. Plastic trays and containers are widely used for packaging fresh produce, meat, and prepared meals due to their ability to maintain product quality and extend shelf life.

Healthcare packaging is expected to grow at the fastest CAGR of 6.2%. The increasing demand for safe and hygienic packaging solutions in the healthcare sector is driving growth. Plastic containers are used for packaging medical devices and pharmaceutical products, ensuring product safety and preventing contamination.

Plastic Tray And Container Market Segmentations

By Material

- Polypropylene

- Polyethylene Terephthalate

- Polystyrene

- Recycled Plastics

By Product Type

- Thermoformed Trays

- Injection-Molded Containers

- Blow-Molded Containers

By Application

- Food & Beverage

- Healthcare

- Personal Care

- Industrial

Regional Analysis

North America

North America accounted for approximately 23.7% of the plastic tray and container market in 2025 and is expected to grow at a CAGR of 5.2% during the forecast period. The region’s well-established food processing industry and high demand for packaged goods are key factors driving market growth. Additionally, advancements in packaging technologies and increasing focus on sustainability are influencing market dynamics.

The United States dominates the regional market due to its large consumer base and strong retail sector. A key growth factor is the increasing adoption of recycled plastic materials in packaging. Companies are investing in sustainable solutions to meet regulatory requirements and consumer expectations, supporting market expansion.

Europe

Europe held a market share of around 21.9% in 2025 and is projected to grow at a CAGR of 5.3%. The region’s strict environmental regulations are shaping the plastic tray and container market by encouraging the use of recyclable materials. The demand for packaging solutions is driven by the food, pharmaceutical, and personal care industries.

Germany leads the European market due to its strong manufacturing capabilities and focus on innovation. A unique growth factor is the increasing implementation of circular economy practices, which promote recycling and reuse of plastic materials. This trend is expected to support market growth.

Asia Pacific

Asia Pacific dominated the plastic tray and container market in 2025 with a 39.2% share and is expected to grow at a CAGR of 5.9%. Rapid urbanization, population growth, and rising disposable incomes are driving demand for packaged goods in the region. The expansion of the food and beverage industry further supports market growth.

China is the dominant country in the region, benefiting from a large manufacturing base and strong consumer demand. A unique growth factor is the increasing demand for affordable packaging solutions, which drives the adoption of plastic trays and containers across various industries.

Middle East & Africa

The Middle East & Africa region accounted for 7.8% of the market share in 2025 and is expected to grow at a CAGR of 5.4%. The growing population and increasing demand for packaged food products are driving market growth. Improvements in retail infrastructure are also supporting adoption.

Saudi Arabia is a key market in the region, driven by the expansion of the food and beverage sector. A unique growth factor is the increasing investment in modern retail formats, which boosts demand for efficient packaging solutions.

Latin America

Latin America held a market share of 7.4% in 2025 and is projected to grow at the fastest CAGR of 6.1%. The region’s growing middle class and rising consumption of packaged goods are key drivers of market growth. The expansion of the retail sector further supports demand.

Brazil dominates the regional market due to its large population and strong food industry. A unique growth factor is the increasing demand for cost-effective packaging solutions, encouraging manufacturers to adopt plastic trays and containers.

Competitive Landscape

The plastic tray and container market is characterized by intense competition among global and regional players focusing on product innovation, cost efficiency, and sustainability. Leading companies include Amcor plc, Berry Global Inc., Sonoco Products Company, Sealed Air Corporation, and Pactiv Evergreen Inc. Among these, Amcor plc is recognized as a leading player due to its extensive product portfolio and strong global presence.

Companies are investing in research and development to create recyclable and bio-based plastic packaging solutions. Strategic partnerships and acquisitions are common strategies used to expand market reach. Recent developments include the launch of sustainable packaging solutions and expansion of production capacities to meet increasing demand.

Key Players List

- Amcor plc

- Berry Global Inc.

- Sonoco Products Company

- Sealed Air Corporation

- Pactiv Evergreen Inc.

- Huhtamaki Oyj

- Winpak Ltd.

- Dart Container Corporation

- Genpak LLC

- Sabert Corporation

- Anchor Packaging LLC

- Placon Corporation

- Silgan Holdings Inc.

- Greiner Packaging International

- Coveris Holdings S.A.