Plastic Packaging Market Size and Growth

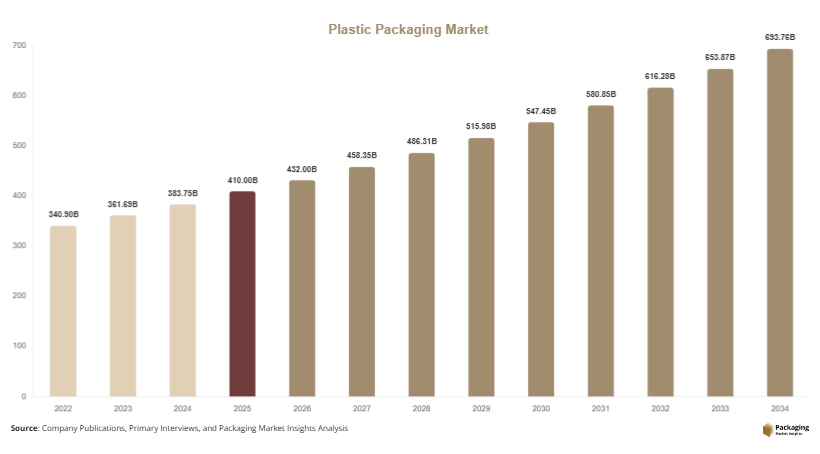

The global plastic packaging market size was estimated at USD 410 billion in 2025 and is projected to reach approximately USD 432 billion in 2026. Over the forecast period, the market is expected to expand steadily, reaching USD 690 billion by 2034, registering a compound annual growth rate (CAGR) of 6.1% from 2025 to 2034. Rising consumer demand for convenience products and improved shelf life for packaged goods continues to support the adoption of plastic packaging formats.

The plastic packaging market continues to play a central role in global packaging supply chains due to its durability, lightweight nature, cost efficiency, and design flexibility. Plastic packaging materials such as polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), and polyvinyl chloride (PVC) are widely used across industries including food and beverage, pharmaceuticals, personal care, and industrial goods. Increasing demand for packaged food products, expansion of organized retail, and the growth of e-commerce distribution channels are contributing to sustained market expansion.

Key Highlights

- Global plastic packaging market size reached USD 410 billion in 2025

- Market projected to reach USD 690 billion by 2034

- CAGR of 6.1% (2025–2034)

- Food and beverage sector represents the largest demand segment

- Increasing adoption of recyclable and lightweight plastic materials

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable and Recyclable Plastic Materials

A major trend shaping the plastic packaging market is the increasing shift toward sustainable plastic solutions. Governments, environmental organizations, and consumers are encouraging manufacturers to reduce plastic waste and increase recycling efficiency. As a result, packaging producers are investing in recyclable polymers, biodegradable plastics, and recycled plastic resins. Technologies such as chemical recycling and advanced mechanical recycling are improving the quality of recycled plastics, enabling them to be used in food-grade packaging applications.

Many consumer goods companies are also setting long-term sustainability goals that include higher recycled content in packaging. This trend is encouraging plastic packaging manufacturers to redesign products with improved recyclability while maintaining durability and barrier performance. As sustainability requirements become integrated into supply chains, demand for recyclable plastic packaging formats is expected to increase steadily.

Increasing Demand for Flexible Plastic Packaging

Flexible plastic packaging formats such as pouches, films, and sachets are gaining significant popularity across multiple industries. Compared with rigid packaging, flexible plastics offer advantages such as reduced material consumption, lower transportation costs, and extended shelf life. These benefits make flexible packaging particularly attractive for food, personal care, and pharmaceutical products.

The expansion of single-serve food products and ready-to-eat meals has further strengthened demand for flexible plastic packaging. Manufacturers are also adopting high-barrier films and multilayer structures that provide improved oxygen and moisture protection. As consumer lifestyles become more convenience-oriented, flexible plastic packaging formats are expected to remain one of the fastest evolving trends in the market.

Market Drivers

Growth of the Global Food and Beverage Industry

The expanding food and beverage industry represents one of the strongest drivers of the plastic packaging market. Packaged food consumption has increased significantly due to urbanization, rising disposable income, and changing consumer lifestyles. Plastic packaging materials provide protection against contamination, moisture, and oxygen exposure, which helps maintain product freshness and shelf life.

In addition, plastic packaging is lightweight and cost efficient, making it suitable for high-volume food production and transportation. Large food manufacturers rely on plastic containers, bottles, films, and pouches to package products ranging from beverages to dairy items and snacks. With global food consumption continuing to grow, the demand for reliable and scalable plastic packaging solutions is expected to remain strong.

Expansion of E-Commerce and Retail Logistics

The rapid growth of e-commerce platforms has significantly increased demand for protective packaging materials. Plastic packaging is widely used in logistics due to its durability, flexibility, and lightweight properties. Shipping products through complex distribution networks requires packaging materials that can withstand transportation stress and environmental exposure.

Plastic packaging materials such as bubble wrap, stretch films, and protective pouches help reduce product damage during shipping. These materials also lower shipping costs due to their lightweight structure. As online retail continues expanding globally, logistics providers and retailers are increasing their use of plastic packaging to ensure product safety and efficient delivery.

Market Restraint

Environmental Concerns and Regulatory Restrictions

Environmental concerns related to plastic waste represent a significant restraint for the plastic packaging market. Governments and regulatory authorities across several countries have introduced policies aimed at reducing single-use plastics and encouraging sustainable alternatives. These regulations can create compliance challenges for plastic packaging manufacturers and may increase operational costs.

For example, several countries in Europe and Asia have implemented taxes or restrictions on specific plastic packaging formats such as single-use bags and disposable containers. These policies require manufacturers to redesign products using recyclable materials or biodegradable plastics, which can involve additional research and development investments.

Public awareness about marine pollution and plastic waste has also increased pressure on companies to adopt environmentally responsible packaging solutions. Brands are now expected to reduce plastic usage or shift toward recyclable packaging. While plastic packaging remains widely used due to its functional advantages, regulatory constraints and sustainability expectations may slow growth in certain segments of the market.

Market Opportunities

Development of Advanced Recycling Technologies

Advancements in recycling technologies present a significant opportunity for the plastic packaging market. Traditional mechanical recycling has limitations in processing mixed or contaminated plastics. However, emerging technologies such as chemical recycling can break plastics into their molecular components, enabling them to be reused in new packaging products.

These technologies can significantly improve circular economy initiatives within the packaging industry. Companies that invest in advanced recycling infrastructure can reduce raw material costs while meeting sustainability requirements. As governments and corporations increase their commitment to plastic waste reduction, the adoption of advanced recycling technologies is expected to create long-term growth opportunities.

Growth of Emerging Markets

Emerging economies present strong opportunities for plastic packaging manufacturers. Rapid urbanization, population growth, and expansion of retail infrastructure are increasing demand for packaged goods in regions such as Asia Pacific, Latin America, and the Middle East.

In these markets, rising disposable income is driving higher consumption of packaged food, beverages, and personal care products. Plastic packaging provides cost-effective and scalable solutions for mass production and distribution. As modern retail chains and e-commerce platforms expand in developing countries, plastic packaging demand is expected to grow steadily.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 410 Billion |

| Market Size in 2026 | USD 432 Billion |

| Market Size in 2034 | USD 690 Billion |

| CAGR | 6.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Rigid plastic packaging dominated the plastic packaging market in 2024, accounting for approximately 58% of the total market share. Rigid plastics include bottles, containers, trays, and jars widely used across food, beverage, pharmaceutical, and household product applications. These packaging formats offer durability, strong barrier properties, and excellent product protection during transportation and storage.

Rigid packaging remains popular among beverage manufacturers because plastic bottles are lightweight, cost efficient, and easily moldable into different shapes. In addition, rigid plastic packaging offers improved product visibility and convenience for consumers. Industries such as dairy, carbonated drinks, and personal care products continue to rely heavily on rigid packaging formats to maintain product safety and extend shelf life.

Flexible plastic packaging represents the fastest-growing type segment, expected to expand at a CAGR of approximately 7.2% during the forecast period. Flexible packaging includes films, pouches, wraps, and sachets used widely in snack foods, frozen foods, and ready-to-eat meals. These packaging formats require less raw material compared to rigid plastics, making them cost effective and environmentally efficient.

Another factor supporting flexible packaging growth is its ability to incorporate advanced barrier technologies. Multilayer films provide protection against oxygen, moisture, and contamination while maintaining product freshness. As consumers increasingly demand lightweight and convenient packaging solutions, flexible plastic packaging is expected to gain wider adoption across industries.

By Material

Polyethylene (PE) emerged as the dominant material segment in 2024, holding nearly 34% of the plastic packaging market share. PE is widely used due to its flexibility, moisture resistance, and affordability. It is commonly applied in packaging products such as plastic bags, films, and squeeze bottles. Industries prefer PE packaging materials because they can be easily processed and molded into various shapes.

Additionally, PE offers good chemical resistance and durability, which makes it suitable for packaging food products, household chemicals, and industrial goods. High-density polyethylene (HDPE) and low-density polyethylene (LDPE) are particularly common in packaging applications. These materials provide reliable barrier properties while maintaining cost efficiency for large-scale production.

Polyethylene terephthalate (PET) is expected to be the fastest-growing material segment, projected to grow at a CAGR of around 6.9% during the forecast period. PET is widely used for beverage bottles, food containers, and pharmaceutical packaging due to its transparency and strong barrier properties. The material is also highly recyclable, which supports sustainability initiatives in the packaging industry.

Demand for PET packaging continues to grow as beverage manufacturers adopt lightweight bottle designs that reduce material usage while maintaining durability. Additionally, improvements in PET recycling technologies allow manufacturers to produce high-quality recycled PET suitable for food-grade packaging applications. These factors contribute to the rapid growth of the PET segment.

By End-Use Industry

The food and beverage industry dominated the plastic packaging market in 2024, accounting for approximately 48% of total market share. Plastic packaging materials are widely used in this industry because they provide excellent barrier protection against moisture, oxygen, and contamination. Products such as beverages, dairy items, snacks, and frozen foods rely heavily on plastic bottles, containers, and flexible packaging films.

Food manufacturers prefer plastic packaging due to its lightweight properties, which reduce transportation costs across long distribution networks. Additionally, plastic packaging offers extended shelf life and improved product safety, which are essential for large-scale food distribution systems. With rising global demand for packaged food products, this segment is expected to maintain its dominant position.

The pharmaceutical industry is projected to be the fastest-growing end-use segment, expanding at a CAGR of around 7.0% during the forecast period. Plastic packaging solutions such as blister packs, bottles, and medical pouches are widely used for drug packaging and healthcare products. These materials provide sterility, durability, and protection against contamination.

Growth in the pharmaceutical packaging segment is supported by increasing global healthcare expenditure and rising demand for medicines and medical devices. Plastic packaging ensures safe transportation and storage of pharmaceutical products while maintaining compliance with regulatory standards. As pharmaceutical manufacturing continues to expand globally, demand for specialized plastic packaging solutions is expected to increase.

Plastic Packaging Market Segmentations

Type

- Rigid Plastic Packaging

- Flexible Plastic Packaging

Material

- Polyethylene (PE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Polyvinyl Chloride (PVC)

- Others

End-Use Industry

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Industrial Packaging

- Household Products

Regional Analysis

North America

North America accounted for approximately 24% of the global plastic packaging market share in 2025, supported by strong demand from the food, pharmaceutical, and consumer goods industries. The region benefits from advanced packaging technologies and well-established supply chains. The market in North America is projected to grow at a CAGR of around 5.3% during the forecast period, driven by innovations in recyclable packaging materials and increasing demand for sustainable packaging solutions.

The United States represents the dominant country in the regional market due to its large consumer goods sector and strong e-commerce infrastructure. A unique growth factor in the country is the rapid adoption of lightweight packaging designs aimed at reducing transportation costs and environmental impact. Packaging manufacturers are also investing in recycled plastic materials to meet sustainability commitments from major retail and food companies.

Europe

Europe represented approximately 21% of the global plastic packaging market in 2025. The region has a well-developed packaging industry and strong demand from food processing, cosmetics, and pharmaceutical sectors. The market is expected to grow at a CAGR of around 5.0% through 2034, supported by advancements in recycling technologies and regulatory initiatives promoting circular economy practices.

Germany remains the leading country in the European plastic packaging industry due to its strong manufacturing base and advanced recycling infrastructure. A key growth factor in the country is the expansion of high-quality recycled plastics used in packaging production. German manufacturers are increasingly integrating recycled materials into packaging products while maintaining durability and safety standards.

Asia Pacific

Asia Pacific held the largest share of approximately 38% of the plastic packaging market in 2025. The region benefits from strong manufacturing activity, rapid urbanization, and expanding food and beverage industries. The market is expected to grow at the fastest CAGR of around 7.4% during the forecast period, driven by increasing consumption of packaged goods and expanding retail distribution networks.

China dominates the Asia Pacific plastic packaging market due to its large manufacturing sector and strong export industry. One unique growth factor in the country is the rapid expansion of domestic e-commerce platforms, which require large volumes of lightweight and protective packaging materials. This trend has significantly increased demand for plastic films, pouches, and protective packaging products.

Middle East & Africa

The Middle East & Africa accounted for approximately 9% of the global plastic packaging market share in 2025. Growth in the region is supported by expanding retail sectors, increasing urbanization, and rising consumption of packaged food products. The market is expected to grow at a CAGR of approximately 6.2% through 2034, reflecting steady development in the packaging industry.

Saudi Arabia represents one of the dominant countries in the regional market due to its strong petrochemical industry. A unique growth factor is the availability of raw materials used for polymer production. This provides a cost advantage for plastic packaging manufacturers operating in the region and supports local packaging production capacity.

Latin America

Latin America captured around 8% of the plastic packaging market in 2025. The market is gradually expanding as consumer demand for packaged products increases across the region. The industry is expected to grow at a CAGR of approximately 5.8% between 2025 and 2034, supported by rising food processing activities and improving distribution infrastructure.

Brazil leads the Latin American plastic packaging market due to its large population and expanding food and beverage industry. A unique growth factor in the country is the growing adoption of flexible packaging formats for packaged food products. This shift is driven by cost efficiency and extended shelf life benefits compared to traditional packaging materials.

Competitive Landscape

The plastic packaging market is moderately fragmented with several multinational companies competing across different packaging segments. Major industry participants focus on product innovation, sustainable packaging development, and strategic acquisitions to strengthen their market presence.

One of the leading companies in the market is Amcor plc, which maintains a strong global presence in both flexible and rigid plastic packaging solutions. The company continues to invest in recyclable packaging technologies and lightweight material innovations. Recent developments include the introduction of high-performance recyclable packaging designed for food and beverage applications.

Other key players include Berry Global, Sealed Air, Sonoco Products Company, and Mondi Group. These companies focus on expanding production capacity and developing sustainable plastic materials. Strategic collaborations with consumer goods manufacturers also play an important role in strengthening competitive positioning within the market.

Key Players List

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Mondi Group

- Huhtamaki Oyj

- Constantia Flexibles

- Coveris Holdings

- Plastipak Holdings Inc.

- Silgan Holdings Inc.

- Alpla Group

- Winpak Ltd.

- Uflex Ltd.

- ProAmpac LLC

- Greif Inc.