Plastic Healthcare Packaging Market Size and Growth

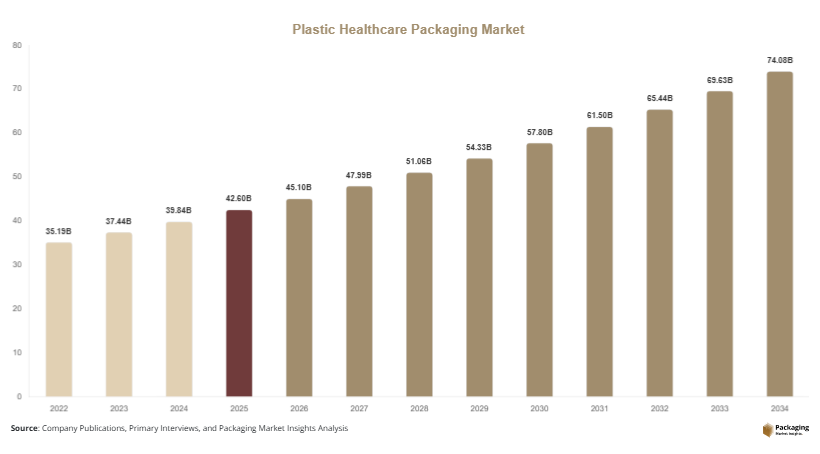

The global plastic healthcare packaging market was valued at USD 42.6 billion in 2025 and is projected to reach USD 45.1 billion in 2026. The market is forecast to grow at a CAGR of 6.4% during 2025–2034, reaching approximately USD 78.9 billion by 2034. Growing pharmaceutical production, rising healthcare expenditures, and increasing demand for sterile and lightweight packaging solutions are major factors supporting market expansion worldwide. Plastic healthcare packaging has become essential for protecting medical products, maintaining sterility, improving shelf life, and ensuring safe transportation across pharmaceutical and medical supply chains.

Plastic packaging solutions are widely used in pharmaceutical bottles, blister packs, medical pouches, syringes, IV containers, diagnostic kits, and medical device packaging. Materials such as polyethylene, polypropylene, PET, PVC, and HDPE are commonly utilized because they offer flexibility, durability, chemical resistance, and cost efficiency. Healthcare manufacturers increasingly rely on advanced plastic packaging technologies to maintain compliance with strict regulatory requirements related to hygiene, product integrity, and patient safety.

Key Highlights

- North America dominated the market with a 34.8% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.1%.

- Bottles and containers led the type segment with a 31.6% share.

- Polyethylene materials dominated with a 29.8% share.

- Pharmaceutical applications led the end-use segment with 58.4% share.

- The US remained the dominant country with a market size of USD 11.5 billion in 2025 and USD 12.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable Medical Packaging Materials

Sustainability is becoming a major trend across the plastic healthcare packaging market as healthcare companies face increasing pressure to reduce packaging waste and carbon emissions. Pharmaceutical manufacturers are investing in recyclable plastic packaging, mono-material structures, and lightweight designs to align with environmental targets while maintaining strict safety standards. Packaging suppliers are also introducing bio-based plastics and recycled resin content for secondary healthcare packaging applications.

For example, several pharmaceutical companies are replacing multilayer packaging structures with recyclable polyethylene-based alternatives for medication bottles and medical pouches. Hospitals and healthcare systems are also encouraging suppliers to adopt sustainable packaging practices to support environmental procurement goals. Future demand for eco-friendly healthcare packaging is expected to rise as regulatory agencies strengthen sustainability guidelines for pharmaceutical and medical packaging materials worldwide.

Growth of Smart and Traceable Healthcare Packaging

The increasing adoption of smart packaging technologies is another important trend shaping the plastic healthcare packaging market. Pharmaceutical manufacturers are integrating RFID labels, QR codes, and temperature-monitoring indicators into healthcare packaging to improve supply chain visibility and prevent counterfeit products.

Smart packaging solutions are increasingly used for vaccines, biologics, insulin products, and temperature-sensitive medications that require strict monitoring during transportation and storage. For instance, cold-chain pharmaceutical distributors are adopting track-and-trace packaging technologies to monitor product conditions throughout global distribution networks. Future growth of connected healthcare packaging is expected to improve patient safety, reduce medication errors, and strengthen pharmaceutical authentication systems across hospitals and pharmacies.

Market Drivers

Rising Global Pharmaceutical Production

The rapid growth of pharmaceutical manufacturing is one of the strongest drivers supporting the plastic healthcare packaging market. Increasing production of prescription drugs, vaccines, nutraceuticals, and biologic medicines is significantly increasing demand for reliable and sterile packaging solutions.

Plastic packaging materials provide lightweight transportation, chemical resistance, and tamper protection, making them highly suitable for pharmaceutical applications. Drug manufacturers increasingly prefer HDPE bottles, PET containers, and blister packaging because these formats improve product safety and extend shelf life. For example, global vaccine manufacturing expansion has accelerated demand for sterile plastic vials, closures, and medical trays. As pharmaceutical companies continue to expand production capacity across emerging economies, demand for healthcare plastic packaging is expected to increase steadily.

Expansion of Home Healthcare and E-Pharmacy Services

The expansion of home healthcare services and online pharmacy distribution is strongly driving demand for durable and secure healthcare packaging products. Patients increasingly prefer home-based treatment and medication delivery services due to convenience, aging populations, and digital healthcare adoption.

Plastic healthcare packaging offers lightweight transportation, impact resistance, and improved handling for direct-to-patient pharmaceutical distribution. E-pharmacy providers are increasingly adopting tamper-evident packaging and child-resistant medication containers to ensure product safety during delivery. For example, demand for unit-dose packaging and portable medication packs has increased significantly in home healthcare applications involving diabetes management and chronic disease treatment. The continued growth of digital healthcare ecosystems is expected to support long-term packaging demand.

Market Restraint

Environmental Concerns Regarding Medical Plastic Waste

One of the major restraints affecting the plastic healthcare packaging market is the growing concern regarding medical plastic waste and disposal challenges. Healthcare packaging products often involve single-use plastics designed to maintain hygiene and prevent contamination, resulting in large volumes of medical waste generated by hospitals, clinics, and pharmaceutical companies.

Many healthcare plastic materials are difficult to recycle because of contamination risks, mixed polymer structures, and strict regulatory requirements. Incineration and landfill disposal of medical plastic waste can contribute to environmental pollution and carbon emissions. For example, disposable medical packaging used for syringes, IV bags, and sterile pouches generates significant waste volumes globally.\n\nRegulatory agencies and environmental organizations are increasingly pressuring healthcare companies to adopt sustainable packaging alternatives and improve recycling infrastructure. However, replacing conventional medical plastics remains challenging because healthcare packaging requires strict barrier protection, sterility, and chemical resistance. These factors may increase compliance costs and limit rapid adoption of alternative packaging materials in certain applications.

Market Opportunities

Expansion of Biologic and Specialty Drug Packaging

The rapid growth of biologic drugs and specialty pharmaceuticals presents major opportunities for the plastic healthcare packaging market. Biologic medicines often require advanced packaging systems capable of maintaining product stability, temperature control, and contamination prevention throughout distribution and storage.

Packaging manufacturers are developing specialized plastic containers, sterile trays, and multilayer barrier packaging solutions designed for sensitive pharmaceutical products. The expansion of injectable therapies, biosimilars, and personalized medicine applications is expected to increase demand for high-performance healthcare packaging materials. Future opportunities are likely to emerge from temperature-sensitive biologic products requiring advanced smart packaging and cold-chain monitoring systems.

Growth of Recyclable and Bio-Based Healthcare Packaging

The increasing demand for environmentally sustainable healthcare packaging is creating strong growth opportunities across the plastic healthcare packaging market. Packaging manufacturers are investing in recyclable polyethylene packaging, biodegradable polymers, and renewable resin technologies to reduce environmental impact without compromising medical safety requirements.

Several pharmaceutical companies are introducing recyclable medicine bottles and sustainable secondary packaging solutions to support environmental goals. Healthcare packaging suppliers are also developing mono-material blister packs and lightweight medical pouches designed for improved recyclability. Future demand for sustainable medical packaging is expected to accelerate as governments introduce stricter plastic waste regulations and healthcare providers prioritize low-carbon procurement practices.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 42.6 Billion |

| Market Size in 2026 | USD 45.1 Billion |

| Market Size in 2034 | USD 78.9 Billion |

| CAGR | 6.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Bottles and containers dominated the plastic healthcare packaging market with approximately 31.6% of the global market share in 2024. These packaging formats are widely used for tablets, capsules, liquid medicines, syrups, disinfectants, and nutritional supplements because they provide durability, chemical resistance, and cost efficiency. Pharmaceutical manufacturers increasingly prefer HDPE and PET bottles due to their lightweight structure, tamper protection, and moisture resistance. Bottles and containers also support large-scale pharmaceutical distribution through retail pharmacies, hospitals, and e-commerce channels. Several healthcare companies are introducing child-resistant closures and recyclable bottle designs to improve patient safety and sustainability performance. The continued growth of over-the-counter medication consumption and dietary supplements is expected to maintain strong demand for healthcare bottles and containers across global markets.

Blister packs are projected to witness the fastest CAGR of 7.4% during the forecast period because of increasing demand for unit-dose medication packaging and improved patient compliance. Blister packaging provides strong protection against moisture, oxygen, and contamination while improving medication tracking and dosage management. Pharmaceutical companies are increasingly adopting recyclable blister materials and smart labeling technologies designed to improve traceability and anti-counterfeit protection. Future demand is expected to be driven by aging populations, rising chronic disease treatments, and expansion of prescription medication distribution across emerging healthcare markets.

By Material

Polyethylene accounted for nearly 29.8% of the plastic healthcare packaging market in 2024, making it the dominant material segment. Polyethylene materials are widely used for medicine bottles, pouches, IV containers, and flexible healthcare packaging because they provide flexibility, impact resistance, and chemical stability. Pharmaceutical companies increasingly rely on polyethylene packaging because it offers low production costs and compatibility with sterilization processes. Healthcare packaging manufacturers are also introducing lightweight polyethylene structures designed to reduce transportation costs and environmental impact. The expansion of flexible healthcare packaging applications and pharmaceutical exports continues to support strong market demand for polyethylene materials globally.

Bio-based plastics are expected to register the fastest CAGR of 8.2% during the forecast period due to rising environmental concerns and increasing demand for sustainable healthcare packaging solutions. Packaging manufacturers are developing renewable resin technologies and biodegradable healthcare materials designed to reduce plastic waste and carbon emissions. Several pharmaceutical companies are investing in bio-based secondary packaging solutions and recyclable medical containers to strengthen sustainability initiatives. Future growth is expected to be supported by regulatory pressure, environmental awareness, and technological advancements in medical-grade bio-based polymers.

By End-Use

Pharmaceutical applications dominated the plastic healthcare packaging market with approximately 58.4% of the global market share in 2024. Rising production of prescription drugs, vaccines, biologics, and over-the-counter medicines continues to increase demand for sterile and durable healthcare packaging solutions. Pharmaceutical packaging requires strong barrier protection, tamper resistance, and compliance with strict regulatory standards. Plastic healthcare packaging provides lightweight transportation, efficient storage, and extended product shelf life, making it highly suitable for pharmaceutical applications. Several global pharmaceutical manufacturers are investing in smart packaging systems and high-barrier medical containers to improve product safety and supply chain visibility. The rapid expansion of biologic drug manufacturing and global pharmaceutical distribution networks is expected to strengthen future segment growth.

Home healthcare is projected to witness the fastest CAGR of 7.5% during the forecast period due to increasing adoption of remote patient care and home-delivered medical treatments. Patients increasingly prefer home-based healthcare solutions for chronic disease management, diabetes treatment, and elderly care applications. Plastic healthcare packaging supports safe transportation and easy handling of medications, diagnostic products, and portable medical devices. Packaging manufacturers are developing user-friendly medication packs and tamper-evident containers specifically designed for home healthcare environments. Future demand is expected to rise as digital healthcare platforms and e-pharmacy services continue expanding globally.

Plastic Healthcare Packaging Market Segmentations

By Type

- Bottles & Containers

- Blister Packs

- Medical Pouches

- Syringes & Vials

- Trays & Clamshells

By Material

- Polyethylene

- Polypropylene

- PET

- PVC

- Bio-Based Plastics

By End-User

- Pharmaceuticals

- Medical Devices

- Diagnostic Products

- Home Healthcare

- Nutraceuticals

Regional Analysis

North America

North America accounted for approximately 34.8% of the global plastic healthcare packaging market in 2025 and is expected to register a CAGR of 6.1% through 2034. The region benefits from strong pharmaceutical manufacturing infrastructure, advanced healthcare systems, and high healthcare spending levels. Rising demand for sterile pharmaceutical packaging, biologic drug distribution, and home healthcare services continues to support market expansion across the United States and Canada. Healthcare companies are also investing heavily in smart packaging technologies and recyclable medical plastics to comply with evolving environmental standards.

The United States remains the dominant country within the regional market due to its large pharmaceutical industry and extensive medical device manufacturing activities. One unique growth driver is the increasing adoption of specialty drug packaging for biologics and injectable therapies. Pharmaceutical companies are expanding investments in temperature-controlled packaging and tamper-evident healthcare containers to support global distribution of high-value medicines. In addition, the rapid growth of online pharmacies and home-based healthcare delivery systems is strengthening demand for lightweight and secure healthcare packaging products across the country.

Europe

Europe represented nearly 27.4% of the global plastic healthcare packaging market in 2025 and is projected to grow at a CAGR of 6.2% during the forecast period. Strict pharmaceutical safety regulations, strong sustainability initiatives, and rising demand for recyclable healthcare packaging are supporting regional market growth. European pharmaceutical companies are increasingly adopting lightweight packaging formats and recyclable polymers to align with circular economy policies and packaging waste reduction goals.

Germany remains the leading country within the European market due to its advanced pharmaceutical manufacturing base and strong medical technology sector. One important growth driver is the rapid development of sustainable healthcare packaging materials designed to reduce carbon emissions and plastic waste. Pharmaceutical packaging suppliers are introducing recyclable blister packaging and renewable polymer-based medicine containers across the region. Increasing investments in pharmaceutical exports and biologic medicine production are also strengthening demand for high-barrier healthcare plastic packaging solutions in Europe.

Asia Pacific

Asia Pacific dominated the plastic healthcare packaging market with a 30.6% share in 2025 and is forecast to register a CAGR of 6.9% through 2034. Rapid pharmaceutical manufacturing expansion, increasing healthcare expenditures, and rising population growth are supporting strong regional market demand. Countries including China, India, Japan, and South Korea are witnessing substantial growth in pharmaceutical production, vaccine manufacturing, and healthcare infrastructure investments.\n\nThe increasing prevalence of chronic diseases and rising access to healthcare services are also driving demand for medical packaging products across urban and rural markets.

China remains the dominant country within the regional market because of its large pharmaceutical manufacturing industry and expanding medical exports. One unique growth driver is the rapid expansion of generic drug production and vaccine manufacturing capacity. Healthcare packaging companies are investing in advanced sterile packaging technologies and large-scale plastic container manufacturing facilities to meet rising pharmaceutical demand. India is also emerging as a major market due to increasing contract pharmaceutical manufacturing and growing exports of affordable medicines to international markets.

Middle East & Africa

The Middle East & Africa accounted for approximately 4.9% of the global plastic healthcare packaging market in 2025 and is expected to witness a CAGR of 6.5% during the forecast period. Growing investments in healthcare infrastructure, increasing pharmaceutical imports, and rising healthcare awareness are supporting market growth across the region. Plastic healthcare packaging is widely used for medicines, diagnostic products, and hospital consumables because of its cost efficiency and lightweight transportation benefits.

Saudi Arabia remains the dominant country in the regional market due to its expanding pharmaceutical production sector and government healthcare investments. One major growth driver is the increasing focus on local pharmaceutical manufacturing to reduce dependency on imported medicines. Healthcare packaging suppliers are establishing regional production partnerships to improve supply chain efficiency and meet rising demand for sterile packaging products. South Africa and the United Arab Emirates are also witnessing increasing adoption of advanced medical packaging technologies within hospital and pharmaceutical sectors.

Latin America

Latin America held nearly 2.3% of the global plastic healthcare packaging market in 2025 and is projected to grow at the fastest CAGR of 7.1% through 2034. Expanding pharmaceutical production, rising healthcare access, and increasing demand for affordable medicines are major factors supporting regional market expansion. Healthcare providers are increasingly adopting lightweight and cost-effective plastic packaging solutions for pharmaceutical distribution across urban and remote areas.

Brazil remains the leading country in the regional market because of its strong pharmaceutical manufacturing base and growing healthcare spending. One unique growth driver is the expansion of domestic generic medicine production supported by government healthcare programs. Pharmaceutical companies are increasingly investing in blister packaging and tamper-evident medicine containers to improve medication safety and supply chain efficiency. Mexico is also witnessing growing demand for plastic healthcare packaging due to increasing pharmaceutical exports and expanding hospital infrastructure projects.

Competitive Landscape

The plastic healthcare packaging market is highly competitive, with major companies focusing on advanced barrier technologies, sustainable materials, and smart healthcare packaging innovations to strengthen market position. Packaging manufacturers are increasing investments in recyclable plastics, lightweight structures, and pharmaceutical-grade packaging systems designed to meet strict regulatory standards and improve product safety.

Amcor plc remains one of the leading companies in the market due to its broad healthcare packaging portfolio, global manufacturing presence, and advanced flexible packaging technologies. The company continues investing in recyclable medical packaging materials and high-barrier pharmaceutical packaging solutions to support sustainability goals and pharmaceutical safety requirements.

Berry Global Inc., Gerresheimer AG, West Pharmaceutical Services Inc., and AptarGroup Inc. are also major participants in the market. These companies are focusing on product innovation, strategic partnerships, and expansion of sterile packaging production capabilities to improve competitiveness.\n\nHealthcare packaging suppliers are increasingly collaborating with pharmaceutical manufacturers to develop customized packaging systems for biologics, injectable medicines, and specialty drugs. Regional companies across Asia Pacific are also investing in cost-effective healthcare packaging production to support growing pharmaceutical exports and domestic medicine consumption.

Key Players List

- Amcor plc

- Berry Global Inc.

- Gerresheimer AG

- AptarGroup Inc.

- West Pharmaceutical Services Inc.

- SGD Pharma

- Schott AG

- Constantia Flexibles

- Sonoco Products Company

- Sealed Air Corporation

- WestRock Company

- Nelipak Healthcare Packaging

- Tekni-Plex Inc.

- DuPont de Nemours Inc.

- Nolato AB

- UFlex Ltd.

- Klöckner Pentaplast Group