Plastic Bag Market Size and Growth

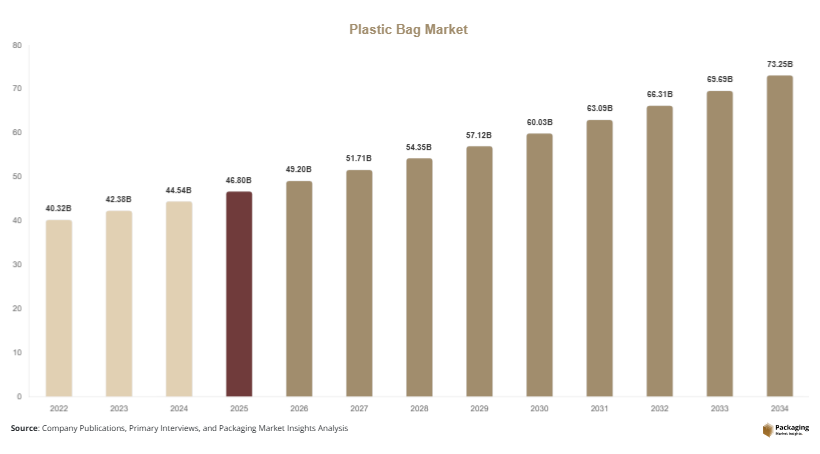

In 2025, the global market size is estimated at USD 46.8 billion, and it is projected to reach USD 49.2 billion in 2026. By 2034, the market is expected to attain approximately USD 72.5 billion, expanding at a CAGR of 5.1% during the forecast period (2025–2034). Despite increasing regulatory pressure against single-use plastics, demand remains stable due to essential applications in retail, food delivery, agriculture, and healthcare packaging. The plastic bag market is undergoing a transitional phase influenced by sustainability regulations, retail packaging demand, and evolving consumer behavior across global economies.

Growth of the plastic bag market is primarily driven by three key factors. First, expanding retail and e-commerce sectors are increasing the need for lightweight, cost-effective packaging solutions for product handling and delivery. Second, rising demand from the food and beverage industry for hygienic and flexible packaging formats continues to support consumption. Third, industrial usage in waste management, agriculture, and chemical packaging ensures consistent baseline demand even in regions with strict environmental policies.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share, while antimicrobial additives are expected to grow at a CAGR of 6.5%.

- Plastic packaging dominated with a 52.3% share, while paper-based packaging is forecasted to grow at a CAGR of 5.9%.

- Food & beverage applications led the segment with 43.1% share, while healthcare packaging is expected to grow at a CAGR of 6.3%.

- China remained the dominant country with a market size of USD 11.2 billion in 2025 and USD 11.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Biodegradable and Compostable Plastic Bags

The plastic bag market is witnessing a structural shift toward biodegradable and compostable materials driven by environmental regulations and corporate sustainability commitments. Manufacturers are increasingly developing bags made from polylactic acid (PLA), starch-based polymers, and oxo-biodegradable compounds. These alternatives are designed to reduce long-term environmental impact while maintaining flexibility and durability required for retail and industrial applications. Governments in Europe and parts of Asia are imposing restrictions on single-use plastics, accelerating adoption of eco-friendly alternatives. Retailers are also transitioning toward sustainable packaging to improve brand perception. However, cost challenges and performance limitations still restrict large-scale adoption in price-sensitive markets, particularly in developing economies.

Expansion of E-commerce and Retail Packaging Demand

The rapid growth of e-commerce platforms is significantly influencing the plastic bag market. Online retail operations require durable, lightweight, and cost-efficient packaging solutions for shipping and last-mile delivery. Plastic courier bags, zip-lock bags, and tamper-evident pouches are widely used due to their protective properties and affordability. The expansion of quick-commerce and grocery delivery services has further increased demand for food-grade plastic bags. Retailers are also adopting branded plastic bags for customer engagement and marketing purposes. This trend is particularly strong in Asia Pacific and Latin America, where digital retail penetration is increasing rapidly, supporting consistent market demand despite environmental concerns.

Market Drivers

Rising Demand from Retail, Food, and Healthcare Sectors

The plastic bag market is strongly driven by demand from retail, food, and healthcare industries. Retail stores continue to rely on plastic bags for packaging and point-of-sale distribution due to their low cost and convenience. The food industry uses plastic bags extensively for packaging frozen food, bakery items, fresh produce, and takeaway services, ensuring hygiene and shelf-life extension. In the healthcare sector, plastic bags are used for medical waste disposal, pharmaceutical packaging, and sterile storage applications. The versatility and low production cost of plastic bags make them indispensable across multiple industries. As urbanization and organized retail continue to grow globally, demand remains stable despite regulatory pressures.

Cost Efficiency and Versatility of Plastic Packaging Solutions

Cost efficiency remains a major driver in the plastic bag market, especially in price-sensitive regions. Plastic bags require relatively low production costs compared to paper or cloth alternatives, making them a preferred choice for mass distribution. Their lightweight nature reduces transportation costs, while their flexibility allows usage across diverse applications, including packaging, storage, and waste management. Plastic bags also offer high customization potential, including printing, branding, and size variation. This versatility makes them suitable for both industrial and consumer applications. In emerging economies, where affordability is a key factor, plastic bags continue to dominate everyday packaging requirements across multiple sectors.

Market Restraint

Stringent Environmental Regulations and Plastic Bans

A major restraint in the plastic bag market is the increasing implementation of environmental regulations and plastic bans across several countries. Governments in Europe, North America, and parts of Asia are introducing strict policies to reduce single-use plastic consumption. These regulations include taxes on plastic bags, mandatory recycling targets, and outright bans in certain retail segments. Such policies are significantly impacting demand in regulated markets, forcing manufacturers to shift toward alternative materials. For example, retail chains in multiple European countries have replaced traditional plastic bags with paper or reusable options. While this shift supports sustainability goals, it creates revenue pressure for conventional plastic bag manufacturers and increases production costs for compliant biodegradable alternatives.

Market Opportunities

Growth in Bioplastic and Recycled Plastic Innovation

The development of bioplastics and recycled plastic materials presents a major opportunity in the plastic bag market. Manufacturers are investing in advanced polymer technologies that allow production of recyclable and compostable bags without compromising strength or durability. Recycled polyethylene (rPE) and bio-based polyethylene are gaining traction as sustainable alternatives. These innovations are supported by government incentives and corporate sustainability targets. As demand for eco-friendly packaging increases, companies that adopt circular economy models are expected to gain competitive advantage. Additionally, improvements in recycling infrastructure are expected to increase availability of raw materials, further supporting market expansion.

Expansion in Emerging Economies and Organized Retail Growth

Emerging economies present significant growth opportunities due to expanding urban populations and increasing organized retail penetration. Countries in Asia Pacific, Latin America, and Africa are witnessing rapid growth in supermarkets, convenience stores, and online grocery platforms. These retail formats rely heavily on plastic bags for packaging and distribution. Rising disposable incomes and changing consumption patterns are further driving packaged goods demand. Additionally, lack of strong enforcement of plastic bans in several developing regions allows continued usage of conventional plastic bags. This creates a stable demand base for manufacturers targeting high-volume, low-cost packaging solutions in these fast-growing markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 46.8 Billion |

| Market Size in 2026 | USD 49.2 Billion |

| Market Size in 2034 | USD 72.5 Billion |

| CAGR | 5.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

High-density polyethylene (HDPE) bags dominated the plastic bag market with a 42.6% share in 2024, driven by their strength, flexibility, and low production cost. These bags are widely used in retail, grocery stores, and waste collection applications. Their durability and resistance to moisture make them suitable for both consumer and industrial usage. HDPE bags remain the most widely produced category due to their cost efficiency and high-volume manufacturing capabilities across global markets.

Biodegradable plastic bags are the fastest-growing subsegment, projected to expand at a CAGR of 6.8%, driven by environmental regulations and rising consumer awareness. These bags are made using bio-based polymers and compostable materials, offering reduced environmental impact. Growth is further supported by government bans on conventional plastic bags and increasing adoption by eco-conscious brands. Improvements in material performance are enhancing their competitiveness in retail and food packaging applications.

By Application

Retail and grocery applications dominated the segment with a 45.1% share in 2024, driven by widespread use in supermarkets, convenience stores, and local shops. Plastic bags are essential for carrying purchased goods due to their convenience and affordability. The segment remains highly volume-driven, especially in emerging economies where organized retail is expanding rapidly.

E-commerce and logistics applications are the fastest-growing segment, projected to grow at a CAGR of 7.1%, driven by rising online shopping and home delivery services. Plastic courier bags and tamper-proof packaging solutions are increasingly used for secure transportation. Growth is further supported by expansion of quick-commerce platforms and increasing demand for last-mile delivery packaging solutions.

By End-Use Industry

Food and beverage industry dominated with a 39.4% share in 2024, driven by demand for hygienic and flexible packaging solutions. Plastic bags are widely used for fresh produce, frozen food, and takeaway packaging. Their ability to maintain product freshness and reduce contamination makes them essential in this sector.

Healthcare is the fastest-growing end-use segment, projected to grow at a CAGR of 6.5%, driven by increasing use in medical waste disposal and pharmaceutical packaging. Strict hygiene requirements and safety standards are boosting adoption of specialized plastic bags in hospitals and laboratories.

Plastic Bag Market Segmentations

By Material Type

- HDPE Bags

- LDPE Bags

- Biodegradable Plastic Bags

- Recycled Plastic Bags

By Application

- Retail & Grocery

- Food Packaging

- E-commerce & Logistics

- Industrial Use

By End-Use Industry

- Food & Beverage

- Healthcare

- Retail Industry

- Industrial & Waste Management

Regional Analysis

North America

North America accounted for approximately 22.8% of the plastic bag market in 2025, with a projected CAGR of 4.6% through 2034. The region’s growth is moderate due to increasing environmental regulations and shifting consumer preferences toward sustainable packaging solutions. However, demand remains stable in essential sectors such as food retail and healthcare packaging, which continue to rely on plastic bags for hygiene and cost efficiency.

The United States dominates the regional market due to its large retail industry and well-established food delivery ecosystem. Growth is supported by demand for recyclable and reusable plastic bag alternatives, particularly in states with strict environmental policies. Innovation in biodegradable plastic technologies is also shaping market evolution.

Europe

Europe held around 20.4% market share in 2025, with a CAGR of 4.3% during the forecast period. Strict environmental regulations and strong sustainability initiatives are significantly influencing market dynamics. Many countries have implemented bans or taxes on single-use plastic bags, leading to reduced consumption.

Germany leads the European market due to its strong recycling infrastructure and advanced manufacturing base. The country’s focus on circular economy models and high adoption of eco-friendly packaging solutions is driving innovation in biodegradable plastic bags.

Asia Pacific

Asia Pacific dominated the market with 37.4% share in 2025, expanding at a CAGR of 6.0% through 2034. Rapid urbanization, population growth, and expansion of retail sectors are key drivers. The region continues to rely heavily on plastic bags due to affordability and high consumption volumes.

China remains the dominant country due to its large manufacturing base and extensive retail and food service industries. Rising demand for packaged goods and online delivery services further strengthens plastic bag consumption.

Middle East & Africa

Middle East & Africa accounted for 10.2% market share in 2025, with a CAGR of 5.4% through 2034. Growth is driven by expanding retail infrastructure and increasing food delivery services in urban centers.

Saudi Arabia leads the region due to strong retail expansion and rising consumer demand for packaged goods. Infrastructure development and growing supermarket penetration are key growth factors.

Latin America

Latin America held around 9.2% market share in 2025, with the fastest CAGR of 6.2% through 2034. Rising urbanization and expansion of organized retail are driving demand for plastic bags.

Brazil dominates the region due to its large retail sector and growing food delivery ecosystem. Increasing consumer spending on packaged goods supports steady market growth.

Competitive Landscape

The plastic bag market is highly fragmented with the presence of global, regional, and local manufacturers competing on cost efficiency and material innovation. Key players include Berry Global Inc., Novolex Holdings, Sealed Air Corporation, Amcor plc, and Advance Polybag Inc. These companies focus on expanding sustainable product portfolios and investing in recyclable plastic technologies. Berry Global Inc. is a leading player, known for its strong manufacturing capabilities and wide product range across retail and industrial applications. Recent developments include expansion of recycled plastic production facilities and introduction of advanced biodegradable bag solutions for retail and food service sectors.

Key Players List

- Berry Global Inc.

- Novolex Holdings

- Amcor plc

- Sealed Air Corporation

- Advance Polybag Inc.

- RKW Group

- Cosmoplast Industrial Company

- Keter Plastic Ltd.

- Sah Polymers Limited

- Shenzhen Zhengwang Packaging

- Thantawan Industry

- Armando Alvarez Group

- ProAmpac LLC

- Superbag Co. Ltd.

- Sahil Plastic Industries