Plant Based Packaging Market Report Size and Growth

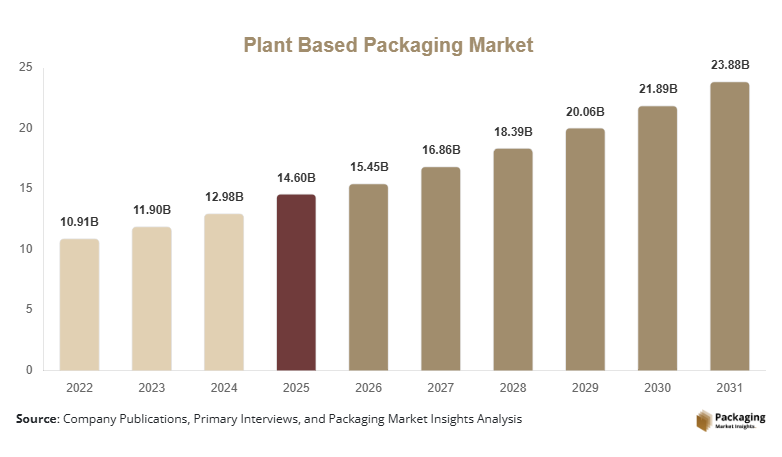

The Plant Based Packaging Market size was valued at USD 8.7 billion in 2025 and is projected to reach USD 14.6 billion by 2030, growing at a compound annual growth rate (CAGR) of 9.1% during 2025–2031. The market is expanding steadily as industries shift toward sustainable packaging materials derived from renewable resources such as corn starch, sugarcane, bamboo, bagasse, and seaweed. Plant-based packaging solutions are increasingly adopted across food and beverage, personal care, pharmaceutical, and e-commerce sectors due to rising environmental awareness and regulatory initiatives promoting biodegradable and compostable packaging materials.

One of the key global factors supporting market expansion has been the increasing implementation of sustainability policies aimed at reducing plastic waste. Governments and environmental agencies across several regions have introduced regulations and incentives encouraging businesses to replace conventional petroleum-based plastics with renewable and biodegradable alternatives. As consumer preference for environmentally responsible products continues to grow, brands are investing in plant-derived materials that help reduce carbon footprint while maintaining packaging functionality.

Advancements in bio-based polymer technologies and innovations in fiber-based packaging have also improved the performance, durability, and barrier properties of plant-based packaging materials. This technological progress has enhanced their applicability across diverse industries, further strengthening market growth prospects.

Key Highlights

- North America dominated the global market with approximately 36% share in 2025, while Asia Pacific is projected to register the fastest growth with a CAGR of 10.6% during the forecast period.

- By material, PLA (Polylactic Acid) accounted for the largest share in 2024, whereas bagasse-based packaging is expected to grow at the fastest CAGR of 11.2%.

- By packaging type, flexible packaging led the market share in 2024, while molded fiber packaging is projected to grow rapidly with a CAGR of 10.8%.

- The United States remained the dominant country, with market values estimated at USD 2.4 billion in 2025 and USD 2.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Compostable Packaging Solutions

One of the prominent trends shaping the Plant Based Packaging Market is the increasing adoption of compostable packaging materials across food service, retail, and e-commerce sectors. Companies are transitioning from traditional plastics to biodegradable materials such as PLA, starch blends, and cellulose-based films. These materials can decompose under industrial composting conditions, reducing landfill waste and environmental pollution. Major consumer brands are incorporating compostable packaging into their sustainability commitments, which is accelerating product innovation and commercial adoption. The growing availability of composting infrastructure in developed regions has further supported this trend.

Rising Use of Agricultural Waste for Packaging Materials

Another key trend in the Plant Based Packaging Market involves the use of agricultural by-products such as sugarcane bagasse, wheat straw, and rice husk to produce packaging materials. These fiber-based resources offer renewable and cost-effective alternatives to plastic packaging. Packaging manufacturers are increasingly utilizing agricultural residues to develop molded fiber trays, containers, and protective packaging. This approach not only reduces waste from agricultural activities but also creates additional value chains within the circular economy.

Market Drivers

Rising Consumer Preference for Sustainable Packaging

The increasing demand for environmentally responsible products has become a significant driver for the Plant Based Packaging Market growth. Consumers are more aware of the environmental impact of plastic waste and are actively seeking products packaged in biodegradable or renewable materials. Retailers and consumer brands are responding to this demand by integrating plant-derived packaging into their product lines. This shift toward sustainability has encouraged companies to redesign packaging formats and invest in plant-based alternatives that align with consumer expectations.

Expanding Applications in Food and Beverage Packaging

The growing use of plant-based materials in food and beverage packaging is another major driver supporting market expansion. Food manufacturers are adopting biodegradable containers, films, and pouches made from plant-derived polymers to comply with environmental guidelines and improve brand perception. Plant-based packaging provides sufficient barrier properties and structural integrity required for various food products. As the food delivery and takeaway culture continues to grow globally, demand for sustainable packaging materials in this sector is expected to increase steadily.

Market Restraint

Higher Production Costs Compared to Conventional Plastics

Despite strong growth prospects, the Plant Based Packaging Market faces challenges associated with higher production costs. Plant-based materials often require specialized processing technologies and raw material sourcing that can increase manufacturing expenses. Compared to petroleum-based plastics, the production scale of bio-based packaging remains relatively limited, resulting in higher unit costs. Additionally, infrastructure for composting and recycling plant-based materials is still developing in several regions. These cost and infrastructure challenges can limit widespread adoption, particularly among price-sensitive industries.

Market Opportunities

Expansion in E-commerce Packaging Applications

The rapid expansion of the e-commerce sector presents a significant opportunity for the Plant Based Packaging Market. Online retailers are increasingly seeking eco-friendly packaging solutions to reduce environmental impact and enhance brand reputation. Plant-based protective packaging, including molded fiber cushioning and biodegradable mailers, offers sustainable alternatives to traditional plastic-based packaging materials. As e-commerce shipments continue to increase globally, demand for renewable packaging solutions is expected to grow.

Development of High-Performance Bio-Based Polymers

Technological advancements in bio-based polymer development present another emerging opportunity for the Plant Based Packaging Market growth. Researchers and packaging manufacturers are developing advanced plant-derived polymers with improved durability, flexibility, and barrier properties. These innovations are enabling plant-based packaging to compete more effectively with traditional plastics in demanding applications such as pharmaceutical and beverage packaging. Continuous investment in research and development is expected to expand the range of applications for plant-derived packaging materials.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14.6 Billion |

| Market Size in 2026 | USD 15.45 Billion |

| Market Size in 2031 | USD 20.47 Billion |

| CAGR | 9.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material

The PLA (Polylactic Acid) segment dominated the Plant Based Packaging Market in 2024, accounting for approximately 34% of the market share. PLA is widely used in packaging applications due to its biodegradability, transparency, and compatibility with conventional plastic processing equipment. It is commonly utilized in food containers, bottles, films, and disposable packaging products. The availability of corn-based raw materials and growing production capacity of bio-based polymers contributed to the segment’s dominant market position.

The bagasse-based packaging segment is expected to grow at the fastest CAGR of 11.2% during the forecast period. Bagasse is derived from sugarcane processing waste and offers a renewable and compostable alternative to plastic packaging. Its high strength and thermal resistance make it suitable for food containers and trays. Increasing utilization of agricultural residues for packaging production will further support the rapid growth of this segment.

By Packaging Type

The flexible packaging segment accounted for the largest share of the Plant Based Packaging Market in 2024, representing around 41% of the market. Flexible packaging materials such as films, pouches, and wraps made from plant-derived polymers are widely used in food and personal care packaging. Their lightweight nature, cost efficiency, and convenience in transportation contributed to the segment’s dominant market share.

The molded fiber packaging segment will grow at the fastest CAGR of 10.8% during the forecast period. Molded fiber packaging is produced from renewable materials such as bamboo, bagasse, and recycled paper pulp. It is widely used for protective packaging applications and food service containers. Increasing demand for sustainable protective packaging solutions will drive the growth of this segment.

By Application

The food and beverage segment dominated the Plant Based Packaging Market in 2024, accounting for approximately 46% of the total market share. Plant-based packaging materials are widely used for food containers, trays, cups, and beverage bottles due to their compostable properties. Growing consumer demand for eco-friendly food packaging has contributed to the segment’s leading position.

The e-commerce packaging segment will grow at the fastest CAGR of 10.4% during the forecast period. The rapid expansion of online retail has increased demand for sustainable packaging materials used for shipping and protective packaging. Plant-based cushioning materials and biodegradable mailers are gaining traction among e-commerce companies seeking to reduce environmental impact.

Plant Based Packaging Market Segmentations

By Material

- PLA (Polylactic Acid)

- Starch-Based Plastics

- Cellulose-Based Plastics

- Bagasse Fiber

- Bamboo Fiber

- Others

By Packaging Type

- Flexible Packaging

- Rigid Packaging

- Molded Fiber Packaging

By Application

- Food & Beverage

- Personal Care & Cosmetics

- Healthcare & Pharmaceuticals

- E-commerce

- Consumer Goods

Regional Analysis

North America

North America accounted for approximately 36% of the global Plant Based Packaging Market share in 2025. The region demonstrated strong adoption of sustainable packaging solutions due to increasing regulatory initiatives targeting single-use plastics. The market in this region is expected to expand steadily and will grow at a CAGR of 8.7% during 2025–2033. Packaging manufacturers across the United States and Canada are investing in biodegradable and renewable packaging materials to meet corporate sustainability commitments and regulatory standards.

The United States dominated the North American market, supported by the strong presence of packaging technology providers and food processing companies adopting eco-friendly materials. Major consumer goods brands in the country are increasingly shifting toward plant-derived packaging formats to meet environmental targets and consumer expectations. The growing availability of compostable packaging products across retail and food service industries has further strengthened market expansion.

Europe

Europe represented approximately 29% of the global Plant Based Packaging Market share in 2025. The region’s market growth was influenced by strong environmental policies and widespread adoption of circular economy practices. The European market will expand at a CAGR of 8.9% during 2025–2033, supported by strict regulations limiting the use of conventional plastic packaging and encouraging biodegradable alternatives.

Germany emerged as the dominant country in Europe, supported by its well-established packaging manufacturing industry and strong emphasis on sustainable materials. German companies have been actively investing in bio-based polymers and fiber-based packaging technologies. The country’s focus on recycling efficiency and waste reduction initiatives has encouraged packaging manufacturers to develop plant-derived alternatives that align with regional sustainability goals.

Asia Pacific

Asia Pacific accounted for approximately 24% of the global Plant Based Packaging Market share in 2025. The region has been experiencing rapid industrial growth and increasing environmental awareness, which supported the adoption of plant-based packaging solutions. The regional market will register the fastest growth with a CAGR of 10.6% during 2025–2033 due to expanding manufacturing industries and growing demand for sustainable consumer goods packaging.

China dominated the Asia Pacific market, driven by its extensive manufacturing infrastructure and rising investments in biodegradable materials. Packaging companies in China are increasingly adopting plant-derived polymers and agricultural fiber materials to reduce dependence on petroleum-based plastics. Government policies promoting eco-friendly packaging have further strengthened the adoption of plant-based materials across multiple industries.

Middle East & Africa

The Middle East & Africa region accounted for approximately 6% of the global Plant Based Packaging Market share in 2025. The region has gradually increased its adoption of sustainable packaging materials, particularly in the food and beverage sector. The market in this region will grow at a CAGR of 7.9% during 2025–2033, supported by increasing investments in packaging innovation and waste management initiatives.

The United Arab Emirates emerged as a leading country in the region, supported by sustainability initiatives aimed at reducing plastic waste. Several food service and hospitality businesses in the country are adopting biodegradable packaging materials to align with environmental goals and tourism sustainability strategies.

Latin America

Latin America accounted for approximately 5% of the global Plant Based Packaging Market share in 2025. The region has gradually increased its adoption of sustainable packaging solutions as industries seek environmentally responsible alternatives to conventional plastic packaging. The regional market will expand at a CAGR of 8.1% during 2025–2033.

Brazil dominated the Latin American market, supported by its strong agricultural sector that provides abundant raw materials for plant-based packaging production. Sugarcane bagasse and other agricultural residues are widely used in the development of biodegradable packaging materials, which has supported the regional market growth.

Competitive Landscape

The Plant Based Packaging Market is moderately competitive with the presence of several global packaging manufacturers and bio-material technology providers. Companies are focusing on developing innovative plant-derived polymers and fiber-based packaging solutions to strengthen their market position.

Tetra Pak International S.A. is considered a leading company in the market due to its extensive portfolio of renewable packaging solutions. The company has recently expanded its plant-based packaging materials that incorporate renewable polymers derived from sugarcane.

Other major players are investing in research and development activities to enhance the performance of biodegradable materials and improve production scalability. Strategic partnerships, product launches, and sustainability initiatives are common strategies adopted by market participants.

Key Players in the Plant Based Packaging Market

- Tetra Pak International S.A.

- Amcor Plc

- Mondi Group

- Smurfit Kappa Group

- Stora Enso Oyj

- International Paper Company

- Huhtamaki Oyj

- UPM-Kymmene Corporation

- WestRock Company

- DS Smith Plc

- Vegware Ltd.

- Biopak Pty Ltd

- Genpak LLC

- Ecologic Brands Inc.

- NatureWorks LL