Plant Based Food Bioplastics Market Size and Growth

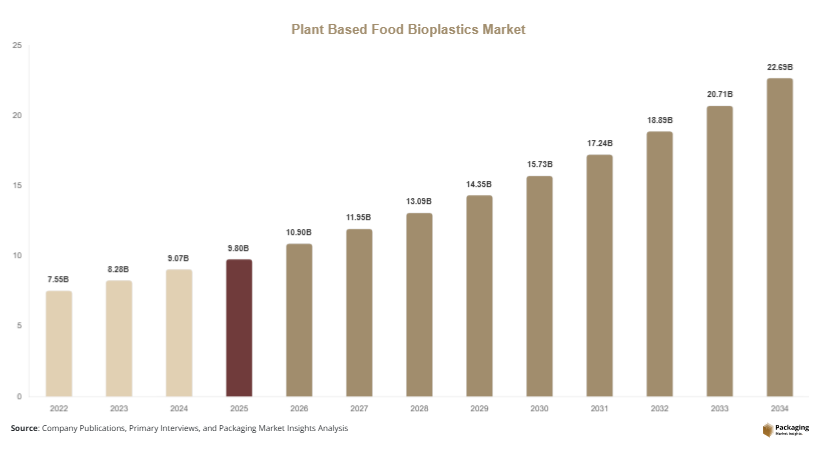

The global plant based food bioplastics market size was valued at USD 9.8 billion in 2025 and is projected to reach USD 10.9 billion in 2026. By 2034, the market is expected to grow to USD 22.7 billion, registering a CAGR of 9.6% during the forecast period from 2025 to 2034. This growth reflects the increasing adoption of biodegradable and compostable materials in food packaging applications, driven by environmental concerns and regulatory support. The plant based food bioplastics market is gaining traction as industries shift toward sustainable packaging alternatives derived from renewable resources.

One of the primary growth factors is the rising global awareness regarding plastic pollution and its environmental impact. Governments and regulatory bodies are implementing strict regulations to limit single-use plastics, encouraging manufacturers to adopt plant-based alternatives. Another key factor is the growing demand from the food and beverage industry, where companies are seeking sustainable packaging solutions to align with consumer preferences and brand commitments. Additionally, advancements in biopolymer technology are improving the performance and cost-effectiveness of plant-based bioplastics, making them more competitive with conventional plastics.

Key Highlights

- Asia Pacific dominated the market with a 36.8% share in 2025, while Latin America is projected to grow at the fastest CAGR of 9.9%.

- Polylactic acid (PLA) led the type segment with a 32.5% share, while polyhydroxyalkanoates (PHA) are expected to grow at a CAGR of 10.2%.

- Flexible packaging dominated with a 49.6% share, while rigid bioplastic packaging is forecasted to grow at a CAGR of 9.4%.

- Food & beverage applications led the segment with 44.3% share, while ready-to-eat meals packaging is expected to grow at a CAGR of 10.1%.

- China remained the dominant country with a market size of USD 2.6 billion in 2025 and USD 2.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing adoption of compostable and biodegradable packaging materials

The plant based food bioplastics market is experiencing a shift toward compostable and biodegradable materials as industries aim to reduce environmental impact. These materials break down naturally under specific conditions, reducing landfill waste and pollution. Food companies are increasingly adopting compostable packaging for products such as fresh produce, snacks, and takeaway meals. This trend is supported by regulatory frameworks that promote sustainable packaging solutions. Additionally, consumers are becoming more environmentally conscious, influencing purchasing decisions and encouraging brands to adopt eco-friendly materials. As infrastructure for composting improves, the adoption of biodegradable bioplastics is expected to expand further.

Integration of advanced biopolymer technologies

Technological advancements in biopolymer production are shaping the plant based food bioplastics market. Innovations in materials such as PLA and PHA are improving mechanical strength, thermal stability, and barrier properties. These enhancements allow bioplastics to compete with conventional plastics in various applications. Companies are also exploring new feedstocks, including agricultural waste and algae, to improve sustainability and reduce costs. The integration of nanotechnology and blending techniques is further enhancing material performance. As research continues, advanced biopolymers are expected to open new opportunities in high-performance packaging applications.

Market Drivers

Rising environmental regulations and sustainability initiatives

The implementation of stringent environmental regulations is a key factor driving the plant based food bioplastics market. Governments worldwide are introducing policies to reduce plastic waste and promote the use of biodegradable materials. These regulations include bans on single-use plastics and incentives for sustainable packaging solutions. Companies are responding by adopting plant-based bioplastics to comply with these requirements. Additionally, corporate sustainability initiatives are encouraging the use of eco-friendly materials. Many organizations are setting targets to reduce carbon footprints and improve environmental performance. These factors are collectively driving demand for plant-based bioplastics in the food industry.

Increasing demand from food and beverage packaging sector

The food and beverage industry is a major driver of the plant based food bioplastics market. Packaging plays a critical role in preserving food quality and extending shelf life. As consumers demand sustainable products, food companies are shifting toward plant-based packaging solutions. Bioplastics offer advantages such as biodegradability and reduced environmental impact. They are widely used in packaging applications such as trays, containers, and films. The growth of ready-to-eat meals and online food delivery services is further increasing demand. As the industry continues to expand, the need for sustainable packaging solutions is expected to grow significantly.

Market Restraint

High production costs and limited infrastructure

The plant based food bioplastics market faces challenges due to high production costs and limited infrastructure for processing and disposal. Bioplastics are often more expensive than conventional plastics due to the cost of raw materials and manufacturing processes. This price difference can limit adoption, particularly in cost-sensitive markets. Additionally, the lack of adequate composting and recycling infrastructure poses challenges for effective waste management. For example, some bioplastics require specific conditions to degrade, which are not widely available. These limitations can reduce the environmental benefits of bioplastics and hinder market growth. Addressing these challenges will require investment in infrastructure and technological advancements.

Market Opportunities

Expansion of bio-based feedstock supply chains

The development of bio-based feedstock supply chains presents significant opportunities in the plant based food bioplastics market. Agricultural resources such as corn, sugarcane, and cassava are commonly used to produce bioplastics. Expanding the availability of these feedstocks can reduce production costs and improve scalability. Additionally, the use of agricultural waste and non-food biomass is gaining attention as a sustainable alternative. This approach reduces competition with food resources and enhances environmental sustainability. As supply chains become more efficient, the adoption of plant-based bioplastics is expected to increase.

Growing demand in emerging markets

Emerging economies offer substantial growth opportunities for the plant based food bioplastics market. Increasing urbanization, rising disposable incomes, and growing awareness of environmental issues are driving demand for sustainable packaging solutions. Governments in these regions are implementing policies to promote eco-friendly materials. The expansion of food processing industries is also contributing to market growth. Companies are investing in local manufacturing facilities to meet rising demand. As awareness and infrastructure improve, emerging markets are expected to play a significant role in the growth of the plant-based bioplastics industry.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.8 Billion |

| Market Size in 2026 | USD 10.9 Billion |

| Market Size in 2034 | USD 22.7 Billion |

| CAGR | 9.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Polylactic acid (PLA) held the largest share of the plant based food bioplastics market in 2024, accounting for approximately 32.5%. PLA is widely used due to its biodegradability, transparency, and ease of processing. It is commonly used in food packaging applications such as containers, films, and trays. The material offers good barrier properties and is suitable for various food products. Increasing demand for sustainable packaging solutions is supporting the growth of this segment. Manufacturers are investing in improving PLA properties to expand its application range.

Polyhydroxyalkanoates (PHA) are expected to grow at the fastest CAGR of 10.2%. PHA offers superior biodegradability and can degrade in various environments, including marine conditions. This makes it an attractive option for reducing plastic pollution. The increasing focus on environmental sustainability is driving demand for PHA. Advances in production technologies are also reducing costs and improving scalability.

By Packaging Type

Flexible packaging dominated the market in 2024, holding a share of approximately 49.6%. This segment includes films, wraps, and pouches used in food packaging. Flexible packaging offers advantages such as lightweight design and reduced material usage. It is widely used in the food industry due to its convenience and cost-effectiveness.

Rigid packaging is expected to grow at a CAGR of 9.4%. This segment includes containers, bottles, and trays made from bioplastics. The demand for rigid packaging is increasing due to its durability and ability to protect products. Advances in material technology are improving the performance of rigid bioplastics, supporting market growth.

By Application

Food and beverage applications accounted for the largest share of the market in 2024, with approximately 44.3%. The demand for sustainable packaging in this sector is driven by consumer preferences and regulatory requirements. Bioplastics are used in various packaging formats to maintain food quality and safety.

Ready-to-eat meals packaging is expected to grow at a CAGR of 10.1%. The increasing popularity of convenience foods is driving demand for packaging solutions that are both sustainable and functional. Bioplastics provide an effective solution, supporting growth in this segment.

Plant Based Food Bioplastics Market Segmentations

By Type

- Polylactic Acid (PLA)

- Polyhydroxyalkanoates (PHA)

- Starch Blends

- Others

By Packaging Type

- Flexible Packaging

- Rigid Packaging

By Application

- Food & Beverage

- Ready-to-Eat Meals

- Fresh Produce PackagingDairy Packaging

Regional Analysis

North America

North America accounted for approximately 28.4% of the plant based food bioplastics market share in 2025 and is projected to grow at a CAGR of 9.1%. The region benefits from strong regulatory frameworks, high consumer awareness, and advanced manufacturing capabilities. Demand is driven by the food and beverage industry, which is increasingly adopting sustainable packaging solutions. Investments in research and development further support market growth.

The United States dominates the regional market due to its large consumer base and strong presence of packaging companies. A key growth factor is the increasing adoption of compostable packaging solutions in food service applications. This trend is supported by regulatory initiatives and growing consumer demand for environmentally friendly products.

Europe

Europe held around 26.7% of the market share in 2025 and is expected to grow at a CAGR of 9.3%. The region is known for its stringent environmental regulations and strong focus on sustainability. Demand for plant-based bioplastics is driven by the need to reduce plastic waste and meet regulatory requirements.

Germany leads the European market due to its advanced manufacturing sector and commitment to sustainability. A unique growth factor is the widespread adoption of circular economy practices. Companies are focusing on recycling and reuse, which supports the growth of bioplastics.

Asia Pacific

Asia Pacific dominated the market with a 36.8% share in 2025 and is projected to grow at a CAGR of 10.0%. Rapid industrialization, increasing population, and rising environmental awareness are driving demand. The region’s strong agricultural base also supports the production of bio-based materials.

China is the dominant country in this region due to its large manufacturing capacity. Government initiatives to promote sustainable materials are a key growth factor. These initiatives are encouraging investment in bioplastic production and innovation.

Middle East & Africa

The Middle East & Africa region held a market share of approximately 4.1% in 2025 and is expected to grow at a CAGR of 8.8%. Increasing awareness about environmental sustainability and improving infrastructure are supporting market growth. The food industry is a key driver in this region.

South Africa is a leading market due to its growing adoption of sustainable packaging. A unique growth factor is the increasing focus on reducing plastic waste through government policies and initiatives.

Latin America

Latin America accounted for around 4.0% of the market in 2025 and is projected to grow at a CAGR of 9.9%. The region is witnessing increasing demand for sustainable packaging solutions due to environmental concerns and regulatory support.

Brazil dominates the regional market due to its strong agricultural sector. A unique growth factor is the availability of bio-based feedstocks such as sugarcane, which supports bioplastic production and reduces costs.

Competitive Landscape

The plant based food bioplastics market is moderately competitive, with several global and regional players focusing on innovation and expansion. Companies are investing in research and development to improve material properties and reduce costs. Strategic partnerships and collaborations are also common as firms seek to expand their market presence.

NatureWorks LLC is a leading player in the market, known for its PLA-based bioplastics. The company recently expanded its production capacity to meet growing demand. Other major players are focusing on developing new materials and improving sustainability.

Key Players List

- NatureWorks LLC

- BASF SE

- TotalEnergies Corbion

- Novamont S.p.A.

- Braskem S.A.

- Danimer Scientific

- Mitsubishi Chemical Group

- Toray Industries, Inc.

- Arkema S.A.

- Biome Bioplastics

- FKuR Kunststoff GmbH

- Plantic Technologies Limited

- Cardia Bioplastics

- Yield10 Bioscience

- Green Dot Bioplastics