Plain Packaging Market Size and Growth

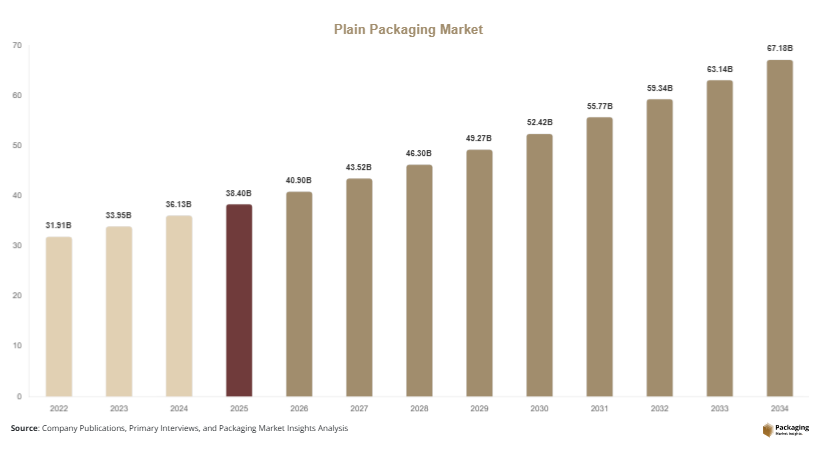

The plain packaging market size is estimated at USD 38.4 billion in 2025 and is projected to reach USD 66.9 billion by 2034, expanding at a CAGR of 6.4% during 2025–2034. The growth trajectory reflects increasing adoption across tobacco, pharmaceutical, and food packaging industries where standardized packaging is becoming a compliance requirement rather than an optional strategy. The plain packaging market is experiencing steady transformation as governments and regulatory bodies across multiple regions continue to enforce stricter packaging standardization laws aimed at reducing brand-based promotion on packaging.

In 2026, the market is expected to reach approximately USD 40.9 billion, driven by expansion of regulatory frameworks in developed economies and gradual adoption in emerging markets. The transition toward uniform packaging formats is also being influenced by rising public health awareness and government-led anti-advertising initiatives, particularly in nicotine-based and controlled consumer products.

Key Highlights:

- The market size is estimated at USD 38.4 billion in 2025, reflecting steady demand across regulated packaging industries. Growth is primarily supported by strict compliance requirements and standardized packaging norms.

- By 2034, the market is projected to reach USD 66.9 billion, driven by expanding regulatory enforcement and increased adoption across tobacco and pharmaceutical packaging sectors.

- The market is expected to expand at a CAGR of 6.4% during 2025–2034, supported by long-term shifts toward simplified and regulation-driven packaging formats.

- Strong adoption is observed in tobacco, pharmaceutical, and regulated food sectors, where packaging standardization and compliance requirements are becoming increasingly strict.

- Regulatory mandates across multiple regions are accelerating global standardization, pushing manufacturers to adopt plain packaging formats for legal compliance and brand control limitations.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Expansion of Regulatory Standardization Policies

One of the most significant trends in the plain packaging market is the rapid expansion of government-led regulatory standardization policies across multiple regions. Countries are increasingly adopting uniform packaging laws, particularly for tobacco, alcohol alternatives, and pharmaceutical products. These regulations require removal of logos, branding elements, and promotional designs, replacing them with standardized fonts, colors, and warning labels. This trend is especially strong in Europe, Australia, and parts of Asia where public health campaigns are driving policy changes. As regulatory frameworks tighten, manufacturers are compelled to redesign packaging processes to comply with legal standards, leading to increased demand for plain packaging solutions and compliance-oriented design systems.

Shift Toward Digitally Traceable Plain Packaging Systems

Another major trend is the integration of digital traceability features within plain packaging formats. While packaging aesthetics are minimized, functional elements such as QR codes, RFID tags, and serialized identifiers are being embedded to ensure product authentication and supply chain visibility. This trend is particularly important in pharmaceutical and regulated consumer goods industries, where tracking and anti-counterfeiting measures are essential. Companies are increasingly combining plain packaging requirements with smart packaging technologies to maintain compliance while ensuring operational efficiency. This hybrid approach is reshaping packaging design strategies across global manufacturers.

Market Drivers

Rising Public Health Regulations and Anti-Advertising Laws

A major driver of the plain packaging market is the increasing implementation of public health regulations aimed at reducing the influence of branding on consumer behavior. Governments are introducing strict anti-advertising laws, particularly targeting tobacco and nicotine-based products. These regulations mandate standardized packaging designs that remove visual branding cues such as logos, colors, and promotional imagery. The objective is to reduce product attractiveness and discourage consumption. This regulatory environment is significantly increasing demand for plain packaging solutions across multiple regions, especially in developed economies where public health policies are highly structured.

Growing Demand for Standardization in Pharmaceutical Packaging

The pharmaceutical sector is another key driver of market growth. Plain packaging is increasingly used to ensure consistency, reduce counterfeit risks, and improve regulatory compliance in drug distribution. Standardized packaging formats help simplify product identification while maintaining necessary legal disclosures and safety warnings. Additionally, global pharmaceutical trade requires uniform packaging standards to streamline cross-border distribution. This is driving pharmaceutical manufacturers to adopt plain packaging systems that align with international compliance frameworks and serialization requirements.

Market Restraint

The primary restraint in the plain packaging market is the reduction in brand differentiation opportunities for manufacturers. Since plain packaging removes logos, colors, and promotional elements, companies face challenges in maintaining brand identity and customer recognition. This is particularly impactful in competitive consumer goods markets such as tobacco alternatives, packaged food, and over-the-counter healthcare products. As a result, some manufacturers experience resistance to full adoption, as branding plays a critical role in customer loyalty and market positioning. Additionally, the transition to plain packaging requires redesigning production lines and packaging workflows, which increases operational costs and slows adoption in cost-sensitive markets.

Market Opportunities

Integration of Smart Compliance Packaging Systems

A significant opportunity lies in the integration of smart compliance technologies within plain packaging systems. Companies are increasingly embedding digital elements such as QR codes, blockchain-based verification, and serialization systems into plain packaging designs. This allows manufacturers to comply with regulatory requirements while enhancing product traceability and anti-counterfeiting capabilities. The combination of regulatory compliance and digital intelligence is expected to create new growth avenues for packaging solution providers.

Expansion in Emerging Regulatory Markets

Emerging economies present a strong opportunity for market expansion as governments gradually adopt standardized packaging regulations. Countries in Asia Pacific, Latin America, and the Middle East are beginning to implement tobacco control policies and pharmaceutical packaging standards similar to those in developed markets. This regulatory shift is expected to drive long-term demand for plain packaging solutions, particularly as global health organizations continue to influence policy development.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 38.4 Billion |

| Market Size in 2026 | USD 40.9 Billion |

| Market Size in 2034 | USD 66.9 Billion |

| CAGR | 6.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Paper-based packaging dominated the market in 2024 with approximately 42% share, driven by its wide adoption in pharmaceutical and tobacco packaging applications. Its low cost, regulatory compatibility, and recyclability make it a preferred material for plain packaging compliance across developed and emerging markets. Additionally, paper-based formats are easier to standardize, which aligns with regulatory requirements for non-branded packaging formats.

Plastic-based packaging is expected to be the fastest-growing segment, expanding at a CAGR of 7.0%. Growth is driven by increasing use in pharmaceutical blister packs and controlled consumer goods requiring moisture resistance and product protection. Improved recyclable plastic formulations are also supporting adoption in regulated packaging environments.

By Application

Tobacco products dominated in 2024 with approximately 39% share, due to strict global regulations enforcing standardized cigarette and nicotine packaging. Plain packaging regulations in multiple countries have significantly reduced branding influence, making this the largest application segment.

Pharmaceutical packaging is the fastest-growing segment with a CAGR of 7.4%, driven by rising demand for counterfeit prevention, serialization compliance, and global drug distribution standardization. Increasing cross-border pharmaceutical trade is further strengthening adoption.

By End-Use Industry

Healthcare dominated the market in 2024 with approximately 37% share, supported by strict regulatory frameworks and high demand for standardized packaging in medicines and medical devices.

Food & beverage is the fastest-growing segment, expanding at a CAGR of 6.9%, driven by increasing labeling regulations, health-conscious consumer behavior, and government initiatives promoting transparent packaging practices.

Plain Packaging Market Segmentations

By Material Type

- Paper-based Packaging

- Plastic-based Packaging

- Metal Packaging

- Glass Packaging

- Composite Materials

By Application

- Tobacco Products

- Pharmaceutical Products

- Food & Beverage

- Healthcare Products

- Controlled Consumer Goods

By End-Use Industry

- Healthcare

- Food & Beverage

- Tobacco Industry

- Retail Packaging

- Industrial Goods

Regional Analysis

North America

North America accounted for approximately 27% market share in 2025, with a projected CAGR of 6.1% during 2025–2034. Growth is supported by strict regulatory frameworks in pharmaceutical labeling, tobacco control policies, and increasing standardization across healthcare packaging systems.

The United States dominates the regional market due to strong FDA compliance requirements and well-established packaging regulations. A key growth factor is the rising implementation of serialization and anti-counterfeit packaging mandates in pharmaceutical and healthcare supply chains.

Europe

Europe held approximately 33% market share in 2025, with a projected CAGR of 6.5% during 2025–2034. The region leads globally in plain packaging adoption due to strict public health policies and early enforcement of standardized tobacco packaging laws.

The United Kingdom dominates the European market due to its pioneering implementation of plain tobacco packaging regulations. A key growth factor is strong government-backed anti-smoking campaigns combined with expanding compliance requirements in pharmaceutical packaging.

Asia Pacific

Asia Pacific accounted for approximately 25% market share in 2025, with the fastest projected CAGR of 7.3% during 2025–2034. Growth is driven by expanding regulatory frameworks, rising healthcare infrastructure, and increasing adoption of standardized packaging systems.

China dominates the region due to large-scale pharmaceutical manufacturing and regulatory modernization. A key growth factor is increasing government focus on counterfeit prevention and packaging standardization in medical and controlled consumer goods.

Middle East & Africa

The region held approximately 8% market share in 2025, with a projected CAGR of 5.7% during 2025–2034. Growth is driven by gradual regulatory adoption, expanding healthcare investments, and rising pharmaceutical imports.

The United Arab Emirates leads the region due to strong pharmaceutical import standards and regulatory alignment with global packaging compliance frameworks. A key growth factor is the expansion of centralized healthcare procurement systems requiring standardized packaging formats.

Latin America

Latin America accounted for approximately 7% market share in 2025, with a projected CAGR of 6.0% during 2025–2034. Growth is supported by increasing tobacco control laws, pharmaceutical regulation upgrades, and healthcare system modernization.

Brazil dominates the region due to large-scale healthcare distribution networks and growing regulatory enforcement in packaging standards. A key growth factor is increasing adoption of plain packaging in tobacco and over-the-counter pharmaceutical products.

Competitive Landscape

The plain packaging market is moderately consolidated, with key players focusing on regulatory compliance solutions and standardized packaging production technologies. Major companies include Amcor Plc, WestRock Company, Smurfit Kappa Group, Mondi Group, Sonoco Products Company.

Among these, Amcor Plc holds a leading position due to its global packaging network and strong compliance-driven product portfolio. Recently, the company expanded its pharmaceutical packaging division with enhanced serialization-enabled plain packaging solutions designed for regulated markets.

Key Players List

- Amcor Plc

- WestRock Company

- Smurfit Kappa Group

- Mondi Group

- Sonoco Products Company

- International Paper Company

- DS Smith Plc

- Sealed Air Corporation

- Berry Global Inc.

- Stora Enso Oyj

- Huhtamaki Oyj

- Graphic Packaging Holding Company

- Coveris Holdings

- Rengo Co. Ltd.

- Mayr-Melnhof Karton AG