Pharmaceutical Stand Up Pouches Market Size and Growth

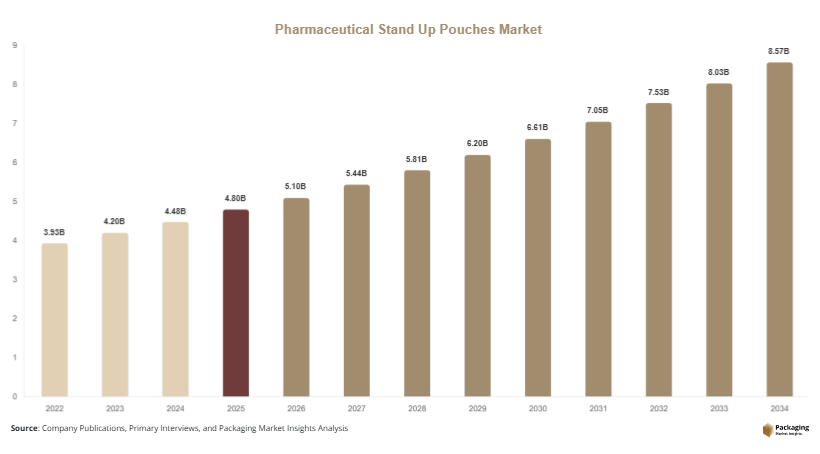

In 2025, the global pharmaceutical stand up pouches market size is estimated at USD 4.8 billion, increasing to USD 5.1 billion in 2026, driven by rising demand for advanced drug packaging solutions. By 2034, the market is projected to reach approximately USD 8.7 billion, registering a CAGR of 6.7% (2025–2034). Growth is primarily supported by increasing pharmaceutical production, stringent packaging regulations, and the rapid expansion of e-commerce-based drug distribution channels. The pharmaceutical stand up pouches market is witnessing steady expansion as pharmaceutical packaging shifts toward lightweight, flexible, and contamination-resistant formats.

Key growth factors include the rising adoption of child-resistant and tamper-evident packaging, increasing demand for moisture-resistant and barrier-enhanced materials, and growing pharmaceutical exports from emerging economies. Additionally, sustainability initiatives are encouraging the use of recyclable and mono-material stand-up pouches, further accelerating market penetration across global healthcare systems.

Key Highlights

Asia Pacific dominated the market with a 37.4% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.2%.

Antioxidants led the type segment with a 29.6% share, while antimicrobial additives are expected to grow at a CAGR of 6.5%.

Plastic packaging dominated with a 52.3% share, while paper-based packaging is forecasted to grow at a CAGR of 5.9%.

Food & beverage applications led the segment with 43.1% share, while healthcare packaging is expected to grow at a CAGR of 6.3%.

China remained the dominant country with a market size of USD 11.2 billion in 2025 and USD 11.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Shift Toward Sustainable Pharmaceutical Packaging

One of the most significant trends in the pharmaceutical stand up pouches market is the transition toward sustainable and eco-friendly packaging materials. Pharmaceutical companies are increasingly adopting recyclable polyethylene, bio-based polymers, and compostable laminates to reduce environmental impact. Regulatory bodies across Europe and North America are encouraging reduced plastic waste, pushing manufacturers to innovate in mono-material pouch structures. These sustainable pouches maintain barrier protection while reducing carbon footprint, making them suitable for sensitive pharmaceutical formulations. Additionally, pharmaceutical brands are using sustainability as a differentiating factor to enhance corporate responsibility and brand value. This shift is expected to reshape procurement strategies and accelerate demand for green packaging solutions over the forecast period.

Adoption of High-Barrier Multi-Layer Pouch Technology

Another major trend is the rising adoption of high-barrier multi-layer stand-up pouch technology. These advanced pouches are engineered with aluminum foil, EVOH, and specialized polymer blends that provide superior protection against oxygen, moisture, and UV exposure. This is particularly important for biologics, powders, and moisture-sensitive tablets. Pharmaceutical companies are increasingly focusing on extending shelf life and ensuring drug stability in varying climatic conditions. The integration of smart packaging features such as QR codes and track-and-trace systems is further enhancing product safety and supply chain transparency. This technological evolution is significantly improving product reliability and boosting adoption across global pharmaceutical distribution networks.

Market Drivers

Expansion of Global Pharmaceutical Production

The continuous expansion of global pharmaceutical manufacturing is a major driver for the pharmaceutical stand up pouches market. Increasing prevalence of chronic diseases such as diabetes, cancer, and cardiovascular disorders has resulted in higher demand for medications worldwide. As pharmaceutical production scales up, manufacturers require efficient, cost-effective, and durable packaging solutions that ensure product integrity. Stand-up pouches offer advantages such as lightweight structure, reduced transportation costs, and improved storage efficiency. Emerging economies such as India and China are becoming major pharmaceutical production hubs, further boosting demand for flexible packaging solutions. Additionally, contract manufacturing organizations are increasingly adopting stand-up pouch formats to optimize operational efficiency and reduce packaging waste.

Rising Demand for Patient-Centric and Convenient Packaging

Another key driver is the growing focus on patient-centric packaging solutions. Modern healthcare systems emphasize ease of use, portability, and safety, particularly for elderly and home-care patients. Stand-up pouches provide resealable, easy-to-handle, and lightweight packaging, making them ideal for over-the-counter medicines, supplements, and unit-dose drugs. Pharmaceutical companies are also incorporating features such as child-resistant closures and dosage accuracy markings to improve patient compliance. The rise of online pharmacy distribution channels has further strengthened demand for durable packaging that can withstand logistics handling. This growing emphasis on convenience and safety is significantly driving adoption of stand-up pouch packaging formats across the pharmaceutical industry.

Market Restraint

High Material and Compliance Costs

A key restraint in the pharmaceutical stand up pouches market is the high cost associated with advanced packaging materials and regulatory compliance. High-barrier films, multi-layer laminates, and specialized coatings significantly increase production costs compared to traditional rigid packaging. Additionally, pharmaceutical packaging must comply with strict regulatory requirements such as FDA, EMA, and ISO standards, which further raises development and validation costs. Small and mid-sized pharmaceutical companies often face budget constraints when adopting premium stand-up pouch solutions. Moreover, frequent changes in compliance standards require continuous upgrades in packaging technology, adding to operational complexity. These cost-related challenges limit widespread adoption, particularly in price-sensitive markets across developing regions.

Market Opportunities

Growth in Biopharmaceutical and Specialty Drug Packaging

The rapid expansion of biopharmaceuticals and specialty drugs presents a significant opportunity for the pharmaceutical stand up pouches market. These drugs require advanced packaging solutions that provide high barrier protection against moisture, oxygen, and contamination. Stand-up pouches with multi-layer structures and controlled environment features are increasingly being adopted for packaging biologics, injectables, and temperature-sensitive formulations. The rising prevalence of personalized medicine is also driving demand for small-batch, customized packaging solutions. Pharmaceutical companies are investing in flexible packaging technologies that ensure product stability throughout complex supply chains. This trend is expected to create long-term growth opportunities for pouch manufacturers specializing in high-performance pharmaceutical packaging solutions.

Expansion of E-Pharmacy and Direct-to-Consumer Distribution

Another major opportunity lies in the rapid growth of e-pharmacy and direct-to-consumer pharmaceutical distribution channels. Online pharmacies require durable, tamper-evident, and lightweight packaging solutions capable of withstanding extended logistics chains. Stand-up pouches offer significant advantages in terms of cost efficiency, portability, and protection against environmental exposure. As digital healthcare platforms expand globally, pharmaceutical companies are increasingly redesigning packaging formats to align with direct-to-patient delivery models. This shift is particularly strong in urban regions where online medicine ordering is becoming mainstream. The increasing integration of logistics automation and last-mile delivery systems is expected to further boost demand for flexible pouch packaging solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.8 Billion |

| Market Size in 2026 | USD 5.1 Billion |

| Market Size in 2034 | USD 8.7 Billion |

| CAGR | 6.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

Type Segment

Plastic-based stand-up pouches dominated the pharmaceutical stand up pouches market in 2024 with a 52.3% share due to their cost efficiency, flexibility, and strong barrier properties. These materials are widely used for tablets, capsules, and powdered drug formulations. Their ability to support multi-layer structures makes them highly suitable for moisture-sensitive pharmaceutical products.

The fastest-growing subsegment is antimicrobial and advanced additive-based pouches, projected to grow at a CAGR of 6.8%. Growth is driven by increasing demand for contamination-resistant packaging in sterile pharmaceutical environments. These pouches incorporate specialized coatings that inhibit microbial growth, making them ideal for high-risk drug categories and biologics.

Application Segment

The food-grade pharmaceutical packaging application, including nutraceuticals and OTC medicines, held a 43.1% share in 2024. This dominance is supported by increasing consumer preference for self-medication and wellness products. Stand-up pouches are widely used for vitamins, supplements, and herbal formulations due to their convenience and resealability.

The fastest-growing application segment is healthcare and clinical drug packaging, expanding at a CAGR of 6.6%. Growth is driven by rising demand for hospital-based medication distribution and home-care drug delivery systems. Pharmaceutical companies are increasingly adopting flexible pouches for unit-dose packaging.

End-Use Segment

Pharmaceutical manufacturers dominated the end-use segment with a 48.7% share in 2024 due to large-scale production requirements and regulatory compliance needs. These companies rely heavily on stand-up pouches for bulk packaging and export-oriented distribution.

The fastest-growing end-use segment is contract packaging organizations, projected to grow at a CAGR of 7.1%. Growth is driven by outsourcing trends in pharmaceutical packaging, allowing companies to reduce operational costs and improve production efficiency.

Pharmaceutical Stand Up Pouches Market Segmentations

By Type

- Plastic-Based Stand Up Pouches

- Paper-Based Stand Up Pouches

- Aluminum Laminated Pouches

- Biodegradable & Eco-Friendly Pouches

- Antimicrobial & Additive-Enhanced Pouches

By Application

- Pharmaceutical Tablets & Capsules

- Powdered Drug Packaging

- Over-the-Counter (OTC) Medicines

- Nutraceuticals & Supplements

- Biologics & Specialty Drugs

By End-Use

- Pharmaceutical Manufacturers

- Contract Packaging Organizations

- Hospitals & Clinics

- Retail & Online Pharmacies

Regional Analysis

North America

North America accounted for approximately 28.6% of the pharmaceutical stand up pouches market in 2025 and is projected to grow at a CAGR of 6.1% through 2034. The region benefits from a highly developed pharmaceutical industry, strong regulatory frameworks, and early adoption of advanced packaging technologies. Demand is particularly strong in the United States, where pharmaceutical companies are focusing on sustainability and patient-centric packaging innovations.

The United States dominates the regional market due to the presence of major pharmaceutical manufacturers and packaging innovators. A key growth factor is the rising adoption of tamper-evident and child-resistant packaging solutions driven by strict FDA regulations and increasing consumer safety awareness.

Europe

Europe held around 24.3% market share in 2025 and is expected to grow at a CAGR of 6.0% through 2034. The region is driven by stringent environmental regulations and strong emphasis on recyclable pharmaceutical packaging. Countries such as Germany, France, and the United Kingdom lead demand.

Germany remains the dominant country in Europe due to its advanced pharmaceutical manufacturing base. A major growth factor is the increasing shift toward sustainable and mono-material packaging formats aligned with EU circular economy goals.

Asia Pacific

Asia Pacific dominated the global market with a 37.4% share in 2025 and is expected to grow at a CAGR of 7.2%. Rapid pharmaceutical production expansion and rising healthcare expenditure are key drivers. India and China are major contributors.

China leads the regional market due to large-scale pharmaceutical manufacturing and export capacity. A key growth factor is the expansion of contract manufacturing and generic drug production.

Middle East & Africa

Middle East & Africa accounted for 6.8% market share in 2025 and is projected to grow at a CAGR of 6.4%. Growth is driven by improving healthcare infrastructure and rising pharmaceutical imports.

Saudi Arabia leads the region due to government investments in healthcare modernization. A key factor is increasing demand for imported packaged pharmaceuticals.

Latin America

Latin America held 2.9% market share in 2025 and is projected to grow at a CAGR of 6.2%. Growth is driven by expanding healthcare access and pharmaceutical distribution networks.

Brazil dominates the region due to its strong pharmaceutical consumption base. A key growth factor is the rise of local pharmaceutical packaging manufacturing capabilities.

Competitive Landscape

The pharmaceutical stand up pouches market is moderately fragmented, with key players focusing on innovation, sustainability, and barrier technology improvements. Leading companies include Amcor plc, Sealed Air Corporation, Mondi Group, Sonoco Products Company, and Berry Global Inc. Among these, Amcor plc holds a leading position due to its extensive global manufacturing network and strong focus on recyclable pharmaceutical packaging solutions.

Recent developments include Amcor’s expansion of recyclable mono-material pouch lines tailored for pharmaceutical applications. Sealed Air Corporation has introduced high-barrier medical-grade pouch systems designed for improved drug stability. Companies are increasingly investing in R&D to enhance material performance and comply with evolving regulatory standards, strengthening competitive intensity across global markets.

Key Players List

- Amcor plc

- Berry Global Inc.

- Mondi Group

- Sealed Air Corporation

- Sonoco Products Company

- Huhtamaki Oyj

- Winpak Ltd.

- Constantia Flexibles

- Uflex Ltd.

- Glenroy Inc.

- ProAmpac LLC

- Coveris Holdings

- PPC Flexible Packaging

- Glenroy Inc.

- Plastopil Hazorea Company