Pharmaceutical Packaging Market Size and Growth

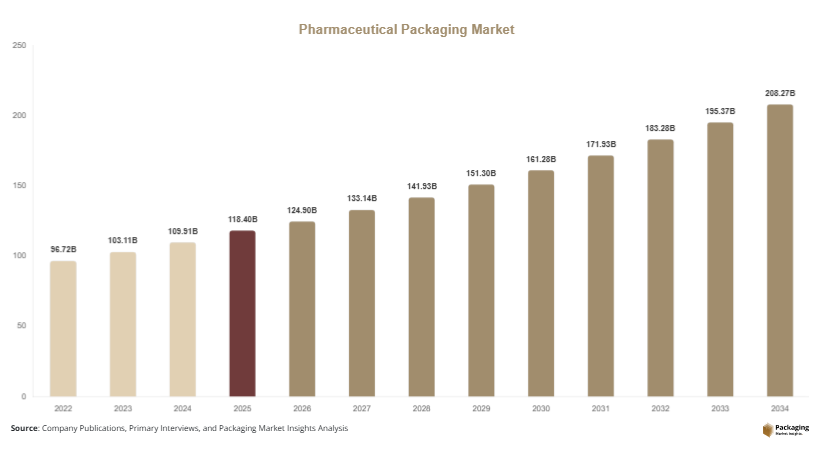

The global pharmaceutical packaging market size was valued at approximately USD 118.4 billion in 2025 and is estimated to reach USD 124.9 billion in 2026. Over the forecast period, the market is projected to grow steadily and reach nearly USD 208.7 billion by 2034, expanding at a compound annual growth rate (CAGR) of 6.6% from 2025 to 2034. This growth reflects increasing pharmaceutical production, expanding biologics manufacturing, and stricter regulatory requirements for drug safety and traceability.

The pharmaceutical packaging market plays a central role in ensuring drug safety, product stability, and regulatory compliance across the global pharmaceutical industry. Packaging solutions are designed to protect medicines from contamination, moisture, light, and mechanical damage while also enabling safe distribution and patient convenience. As pharmaceutical manufacturing expands globally, demand for reliable and innovative packaging solutions continues to grow across primary, secondary, and tertiary packaging formats.

Key Highlights

- Global pharmaceutical packaging market size reached USD 118.4 billion in 2025

- Market projected to reach USD 208.7 billion by 2034

- CAGR of 6.6% from 2025 to 2034

- Increasing biologics production driving demand for specialized packaging

- Serialization regulations accelerating smart packaging adoption

- Sustainability initiatives influencing packaging material innovation

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Smart and Track-and-Trace Packaging

One of the most notable trends in the pharmaceutical packaging market is the growing adoption of smart packaging technologies that improve traceability and supply chain visibility. Pharmaceutical manufacturers increasingly use serialization codes, RFID tags, and digital barcodes to track products from production facilities to pharmacies and hospitals. These technologies help companies comply with regulatory mandates designed to reduce counterfeit drugs and improve patient safety.

Track-and-trace packaging also enables pharmaceutical companies to monitor distribution channels more effectively. Smart labels and digital verification systems allow stakeholders to authenticate products in real time. In addition, digital packaging solutions support automated inventory management across healthcare facilities. As pharmaceutical supply chains expand globally, the integration of digital tracking features into packaging systems is becoming a standard requirement for many drug manufacturers.

Increasing Demand for Sustainable Packaging Materials

Another emerging trend in the pharmaceutical packaging market is the transition toward sustainable and recyclable packaging materials. Pharmaceutical companies are under increasing pressure from regulators, investors, and healthcare providers to reduce environmental impact without compromising drug safety or compliance standards. As a result, packaging manufacturers are introducing recyclable plastics, bio-based polymers, and lightweight materials.

Sustainable packaging initiatives are also influencing design strategies across blister packs, bottles, and cartons. Companies are reducing packaging layers and optimizing material use to decrease waste generation during manufacturing and distribution. In addition, pharmaceutical companies are exploring closed-loop recycling programs for certain packaging components. These sustainability efforts are expected to reshape packaging material selection and innovation across the pharmaceutical supply chain.

Market Drivers

Growth in Global Pharmaceutical Production

A major driver of the pharmaceutical packaging market growth is the continuous expansion of global pharmaceutical manufacturing. Pharmaceutical companies are increasing production capacity to meet growing demand for prescription drugs, vaccines, and over-the-counter medications. This growth is particularly evident in emerging economies where healthcare access is improving and government healthcare spending is rising.

Each pharmaceutical product requires specialized packaging to maintain stability, protect drug efficacy, and meet regulatory requirements. As drug production volumes increase, demand for packaging solutions such as blister packs, bottles, vials, and syringes also grows. Contract manufacturing organizations and pharmaceutical companies are investing heavily in packaging automation and high-speed filling lines, further supporting market expansion across primary and secondary packaging segments.

Expansion of Biologics and Injectable Drug Markets

The rapid expansion of biologics, vaccines, and injectable drugs is another important driver of the pharmaceutical packaging market. Biologic therapies require advanced packaging formats that ensure sterility, temperature stability, and protection from contamination. Products such as monoclonal antibodies, cell therapies, and mRNA vaccines rely on packaging solutions including sterile vials, ampoules, and prefilled syringes.

These packaging formats often require high-quality materials such as borosilicate glass and specialized polymers. Additionally, biologics packaging must comply with strict quality standards due to the sensitivity of these products. As pharmaceutical companies continue to expand biologics pipelines, the demand for specialized packaging solutions is expected to grow significantly over the next decade.

Market Restraint

High Regulatory Compliance and Packaging Validation Costs

One of the key restraints affecting the pharmaceutical packaging market is the high cost associated with regulatory compliance and packaging validation processes. Pharmaceutical packaging must meet strict regulatory standards established by health authorities such as the FDA, EMA, and other national regulatory bodies. These regulations govern aspects such as material safety, contamination control, labeling accuracy, and tamper evidence.

Before a packaging system can be used for commercial drug distribution, it must undergo extensive validation and testing procedures. These processes include stability testing, compatibility analysis, sterility validation, and transportation simulations. The testing process can be time-consuming and expensive, particularly for new packaging materials or technologies.

Smaller packaging companies often face challenges in meeting these regulatory requirements due to limited financial resources and technical capabilities. In addition, regulatory changes or updates can require companies to redesign packaging systems or revalidate production processes. This creates additional operational costs and delays in product launches. As pharmaceutical packaging technologies become more advanced, regulatory oversight is expected to increase, which may continue to present challenges for market participants.

Market Opportunities

Growth of Pharmaceutical Manufacturing in Emerging Markets

Emerging economies present strong growth opportunities for the pharmaceutical packaging market as pharmaceutical manufacturing expands in regions such as Asia Pacific, Latin America, and the Middle East. Governments in these regions are investing in domestic pharmaceutical production to improve healthcare access and reduce reliance on imported drugs.

As local pharmaceutical companies increase manufacturing output, demand for high-quality packaging solutions is also rising. Packaging manufacturers have opportunities to establish regional production facilities and supply packaging components directly to pharmaceutical plants. In addition, contract packaging organizations are expanding their operations in emerging markets, creating further demand for advanced packaging technologies.

Expansion of Personalized and Specialty Medicines

The rise of personalized medicine and specialty pharmaceuticals is creating new opportunities within the pharmaceutical packaging market. Personalized therapies often require smaller production batches and specialized packaging formats designed for precise dosing and patient-specific treatment regimens.

Packaging solutions for personalized medicines must support traceability, patient identification, and flexible production runs. As healthcare providers increasingly adopt targeted therapies, packaging companies are developing modular and customizable packaging systems. These innovations allow pharmaceutical manufacturers to package smaller batches efficiently while maintaining compliance with regulatory requirements.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 118.4 Billion |

| Market Size in 2026 | USD 124.9 Billion |

| Market Size in 2034 | USD 208.7 Billion |

| CAGR | 6.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Based on material type, the plastic packaging segment dominated the Pharmaceutical Packaging Market and accounted for approximately 39% of the market share in 2024. Plastic materials are widely used in pharmaceutical packaging due to their lightweight properties, cost efficiency, and design flexibility. Packaging formats such as bottles, blister packs, and containers commonly use materials like polyethylene, polypropylene, and PET. These materials provide adequate protection against moisture and contamination while allowing manufacturers to produce packaging at high volumes.

Plastic packaging is also favored for over-the-counter drugs and solid dosage forms due to its durability and lower production costs compared to glass and metal alternatives. In addition, advancements in barrier coatings and multilayer plastic films have improved the protective capabilities of plastic packaging. Pharmaceutical companies continue to adopt plastic packaging solutions to reduce transportation costs and improve manufacturing efficiency.

The glass packaging segment is expected to register the fastest growth with a CAGR of around 7.3% during the forecast period. Glass packaging is widely used for injectable drugs, biologics, and vaccines due to its high chemical resistance and ability to maintain drug purity. Materials such as borosilicate glass are particularly suitable for sensitive pharmaceutical products that require stable storage conditions.

Growth in biologics and injectable medications is significantly increasing the demand for glass vials, ampoules, and cartridges. Pharmaceutical companies prefer glass packaging because it offers strong barrier properties and does not interact with drug formulations. As biologics manufacturing continues to expand, glass packaging demand is expected to grow steadily.

By Packaging Type

In terms of packaging type, primary packaging held the dominant position in the Pharmaceutical Packaging Market and accounted for nearly 52% of the market share in 2024. Primary packaging directly contains pharmaceutical products and therefore plays a critical role in maintaining drug stability and preventing contamination. Examples include blister packs, bottles, vials, and syringes.

Primary packaging must comply with strict regulatory standards because it directly interacts with the drug formulation. Pharmaceutical manufacturers invest heavily in high-quality materials and packaging technologies to ensure product integrity throughout the supply chain. Innovations in barrier materials and sterile packaging solutions are also contributing to the expansion of this segment.

The secondary packaging segment is expected to witness the fastest growth with a CAGR of approximately 6.9% over the forecast period. Secondary packaging includes cartons, labels, and protective outer packaging used to group and transport pharmaceutical products. This packaging layer plays a critical role in branding, labeling compliance, and product information communication.

Growth in e-commerce pharmaceutical distribution and expanding global supply chains is increasing demand for durable secondary packaging solutions. Pharmaceutical companies are also integrating serialization codes and tamper-evident features into secondary packaging to improve product authentication and traceability.

By Drug Delivery Mode

Based on drug delivery mode, the oral drug delivery segment dominated the Pharmaceutical Packaging Market and accounted for approximately 44% of the market share in 2024. Oral medications such as tablets and capsules represent the most widely used form of drug administration worldwide. Packaging solutions such as blister packs and plastic bottles are commonly used for oral drugs because they provide convenient dosing and long shelf life.

Blister packaging in particular has become widely adopted due to its ability to protect individual tablets from moisture and contamination. Pharmaceutical companies also favor blister packaging because it allows accurate unit dosing and supports patient adherence. As the demand for generic drugs and over-the-counter medications grows, the oral drug delivery segment continues to dominate pharmaceutical packaging demand.

The injectable drug delivery segment is projected to grow at the fastest rate with a CAGR of around 7.5% during the forecast period. Injectable drugs require specialized packaging such as vials, ampoules, cartridges, and prefilled syringes. These packaging systems must maintain sterility and protect sensitive drug formulations from contamination and degradation.

The growth of biologics, vaccines, and advanced therapies is driving strong demand for injectable drug packaging solutions. Pharmaceutical companies are also adopting ready-to-use packaging systems such as prefilled syringes to improve patient convenience and reduce preparation time in clinical settings.

Pharmaceutical Packaging Market Segmentations

Material

- Plastic

- Glass

- Metal

- Paper & Paperboard

Packaging Type

- Primary Packaging

- Secondary Packaging

- Tertiary Packaging

Drug Delivery Mode

- Oral

- Injectable

- Topical

- Pulmonary

- Transdermal

Regional Analysis

North America

North America accounted for approximately 34% of the pharmaceutical packaging market share in 2025 and is expected to maintain steady growth with a CAGR of around 5.8% during the forecast period. The region benefits from a well-established pharmaceutical industry, advanced manufacturing infrastructure, and strict regulatory frameworks that ensure high-quality packaging standards.

The United States dominates the regional market due to its large pharmaceutical manufacturing sector and strong presence of global drug manufacturers. A key growth factor in the country is the increasing development of biologics and specialty drugs, which require advanced packaging systems such as sterile vials and prefilled syringes.

Europe

Europe held nearly 27% of the global pharmaceutical packaging market share in 2025 and is projected to grow at a CAGR of about 5.6% through 2034. The region benefits from a strong pharmaceutical manufacturing base and robust regulatory oversight that ensures product safety and packaging integrity.

Germany leads the European market due to its advanced pharmaceutical manufacturing capabilities and strong packaging technology industry. The country also supports growth through innovation in sustainable packaging materials and recyclable pharmaceutical containers.

Asia Pacific

Asia Pacific represented approximately 24% of the pharmaceutical packaging market in 2025 and is expected to record the fastest CAGR of around 8.1% during the forecast period. The region is experiencing rapid growth in pharmaceutical production, supported by increasing healthcare investment and favorable manufacturing costs.

China dominates the regional market due to its expanding pharmaceutical manufacturing capacity and government support for domestic drug production. The country is also investing in advanced packaging technologies to improve drug safety and export competitiveness.

Middle East & Africa

The Middle East & Africa accounted for around 7% of the pharmaceutical packaging market share in 2025 and is forecast to grow at a CAGR of approximately 6.4%. Growth in the region is driven by increasing healthcare infrastructure development and pharmaceutical manufacturing investments.

Saudi Arabia represents a key market within the region due to its national healthcare development initiatives and investment in pharmaceutical production facilities. Government programs aimed at strengthening domestic pharmaceutical supply chains are also increasing demand for packaging solutions.

Latin America

Latin America held roughly 8% of the pharmaceutical packaging market in 2025 and is expected to expand at a CAGR of about 6.2% during the forecast period. The region is witnessing steady growth as pharmaceutical production and healthcare spending increase across several countries.

Brazil dominates the Latin American market due to its large pharmaceutical manufacturing sector and expanding healthcare system. Growth in the country is also supported by increasing demand for generic medicines, which require cost-effective packaging solutions.

Competitive Landscape

The pharmaceutical packaging market is moderately consolidated, with several global packaging companies competing alongside regional manufacturers. Leading companies focus on expanding production capacity, developing advanced materials, and forming partnerships with pharmaceutical manufacturers.

Major players in the market include Amcor plc, Gerresheimer AG, West Pharmaceutical Services, Berry Global Inc., and Schott AG. These companies maintain strong global distribution networks and invest in advanced packaging technologies designed for biologics and injectable drugs.

Among these players, Amcor plc is widely recognized as a leading participant in the pharmaceutical packaging market due to its broad portfolio of flexible and rigid packaging solutions. The company has expanded its pharmaceutical packaging offerings through investments in sustainable materials and high-barrier packaging technologies.

In recent years, companies have also focused on sustainability and digital packaging solutions. Manufacturers are introducing recyclable materials, lightweight packaging designs, and smart packaging technologies to improve product traceability and environmental performance.

Strategic acquisitions, research investments, and partnerships with pharmaceutical companies remain key competitive strategies within the market.

Key Players List

- Amcor plc

- Gerresheimer AG

- West Pharmaceutical Services Inc.

- Berry Global Inc.

- Schott AG

- AptarGroup Inc.

- Becton Dickinson and Company

- SGD Pharma

- Nipro Corporation

- WestRock Company

- Catalent Inc.

- Constantia Flexibles

- CCL Industries Inc.

- Uflex Limited

- Sealed Air Corporation