Pharmaceutical Contract Packaging Market Report Size and Growth

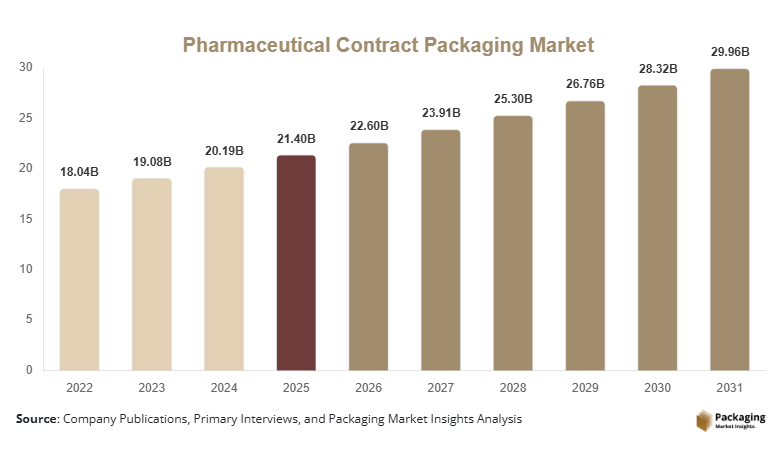

The Pharmaceutical Contract Packaging Market was valued at USD 21.4 billion in 2025 and is projected to reach USD 28.9 billion by 2030, expanding at a compound annual growth rate (CAGR) of 5.8% during the forecast period from 2025 to 2031. Contract packaging services play a vital role in the pharmaceutical supply chain by enabling drug manufacturers to outsource packaging operations such as blister packing, bottling, labeling, and secondary packaging. These services help pharmaceutical companies improve operational efficiency, meet regulatory requirements, and manage fluctuating product demand.

A key factor supporting the growth of the pharmaceutical contract packaging market is the increasing outsourcing of packaging operations by pharmaceutical companies. Pharmaceutical manufacturers are focusing on core activities such as drug discovery, clinical research, and commercialization, while delegating packaging and logistics tasks to specialized service providers. Contract packaging organizations provide advanced automation, serialization technologies, and regulatory compliance expertise, which helps pharmaceutical firms reduce operational complexity and cost.

In addition, the growing demand for pharmaceutical products, expansion of biologics manufacturing, and rising regulatory requirements for product traceability are contributing to increased demand for contract packaging services worldwide. The need for specialized packaging formats for temperature-sensitive drugs and personalized medicines is also encouraging pharmaceutical companies to collaborate with contract packaging providers.

Key Highlights

- North America accounted for approximately 39.2% of the global pharmaceutical contract packaging market share in 2025, while Asia Pacific is projected to record the fastest CAGR of 7.1% during the forecast period.

- Blister packaging dominated the packaging type segment with nearly 34.5% share in 2024, whereas pre-filled syringe packaging is expected to grow at the fastest CAGR of 7.6%.

- Primary packaging led the service segment with about 46.8% share in 2024, while secondary packaging services are projected to expand at a CAGR of 6.9%.

- The United States dominated the market with a value of USD 7.3 billion in 2025, which increased to USD 7.7 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Adoption of Serialization and Track-and-Trace Technologies

Serialization technologies are increasingly being integrated into pharmaceutical packaging processes. Regulatory authorities across major markets have introduced serialization mandates to ensure product traceability and reduce counterfeit drugs. Contract packaging providers are investing in digital labeling, barcoding, and track-and-trace systems that help pharmaceutical companies comply with global regulatory standards.

The adoption of serialization solutions is transforming packaging operations by improving supply chain visibility and enabling real-time monitoring of pharmaceutical products. Advanced packaging facilities equipped with automated serialization lines allow pharmaceutical companies to meet regulatory requirements without investing heavily in in-house infrastructure.

Expansion of Biologics and Specialty Drug Packaging

The increasing production of biologics and specialty pharmaceuticals is shaping packaging requirements in the pharmaceutical industry. Biologic drugs often require specialized packaging formats such as vials, pre-filled syringes, and temperature-controlled containers. Contract packaging providers are expanding capabilities to support cold-chain packaging and sterile filling services.

As the pipeline of biologic therapies continues to grow, pharmaceutical companies are relying on contract packaging organizations that offer advanced handling systems and specialized packaging materials. This trend is expected to support the long-term expansion of the pharmaceutical contract packaging market.

Market Drivers

Rising Pharmaceutical Production Worldwide

The expansion of pharmaceutical manufacturing globally has created significant demand for specialized packaging services. Pharmaceutical companies are launching new therapies and expanding drug production capacity to meet increasing healthcare needs. As production volumes grow, manufacturers are seeking external partners that can manage packaging operations efficiently.

Contract packaging providers offer scalable packaging solutions that help pharmaceutical firms manage seasonal demand fluctuations and rapid product launches. By outsourcing packaging services, pharmaceutical companies can reduce capital investment and streamline supply chain operations.

Increasing Regulatory Compliance Requirements

Pharmaceutical packaging must comply with strict regulatory guidelines related to labeling accuracy, tamper evidence, and product traceability. Compliance with these regulations requires specialized infrastructure and quality assurance systems. Contract packaging providers maintain dedicated compliance teams and quality management frameworks that support pharmaceutical companies in meeting global regulatory requirements.

Packaging service providers also implement validation protocols, serialization systems, and inspection technologies that ensure product safety and regulatory adherence. These capabilities make contract packaging an essential component of pharmaceutical supply chain management.

Market Restraint

Stringent Regulatory Approval and Validation Processes

Regulatory complexity remains a key challenge for the pharmaceutical contract packaging market. Pharmaceutical packaging operations must comply with strict regulatory guidelines issued by global health authorities. Packaging facilities must undergo extensive validation procedures and regular inspections to maintain compliance with Good Manufacturing Practices (GMP).

These regulatory requirements increase operational costs for contract packaging providers. Companies must invest in quality control systems, validation equipment, and regulatory documentation to maintain certification standards. Smaller contract packaging firms may face difficulties in meeting these requirements due to limited financial resources.

Furthermore, pharmaceutical companies often conduct extensive audits before selecting contract packaging partners. This process can delay project approvals and slow the adoption of outsourcing models in some regions. As regulatory standards continue to evolve, contract packaging providers must continuously update packaging processes and compliance frameworks, which may limit market growth in certain areas.

Market Opportunities

Growth of Personalized Medicine Packaging

The rise of personalized medicine is creating new opportunities for contract packaging providers. Personalized therapies require smaller batch sizes and specialized packaging formats designed for individual patient treatments. Contract packaging organizations are developing flexible packaging systems that support small-scale production and customized labeling.

These capabilities allow pharmaceutical companies to launch personalized therapies without investing in dedicated packaging facilities. The growth of targeted therapies and gene-based medicines is expected to generate demand for flexible contract packaging services.

Expansion of Emerging Pharmaceutical Markets

Emerging markets are becoming important manufacturing hubs for pharmaceutical products. Countries across Asia Pacific, Latin America, and the Middle East are expanding pharmaceutical production capacity to support domestic healthcare systems and export markets. This expansion is creating demand for specialized packaging services.

Contract packaging providers are establishing facilities in emerging regions to support local pharmaceutical manufacturers. These partnerships enable pharmaceutical companies to access cost-efficient packaging solutions while meeting regional regulatory requirements.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 21.4 Billion |

| Market Size in 2026 | USD 22.6 Billion |

| Market Size in 2031 | USD 29.9 Billion |

| CAGR | 5.8% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Packaging Type

Blister packaging held the dominant share of approximately 34.5% in 2024. Blister packs are widely used for pharmaceutical tablets and capsules because they provide product protection, dosage accuracy, and tamper evidence. Pharmaceutical manufacturers adopted blister packaging due to its ability to extend product shelf life and maintain drug stability. Contract packaging providers have developed high-speed blister packaging lines that support large-scale pharmaceutical production.

Pre-filled syringe packaging will record the fastest CAGR of 7.6% during the forecast period. The growing use of injectable drugs and biologics will drive demand for pre-filled syringes. These packaging formats improve dosing accuracy and simplify drug administration. Contract packaging providers will invest in sterile filling technologies and automated syringe packaging systems to support increasing demand.

By Service Type

Primary packaging services accounted for nearly 46.8% of the pharmaceutical contract packaging market share in 2024. These services involve direct packaging of pharmaceutical products into containers such as bottles, vials, and blister packs. Pharmaceutical companies relied on contract packaging providers for primary packaging operations to ensure product safety and regulatory compliance.

Secondary packaging services will expand at a CAGR of 6.9% during the forecast period. Secondary packaging includes labeling, cartoning, and bundling of pharmaceutical products. Pharmaceutical companies will increasingly outsource these operations to improve packaging efficiency and reduce operational costs. Automation technologies and digital labeling systems will support the expansion of secondary packaging services.

By Packaging Material

Plastic materials dominated the segment with around 41.3% share in 2024. Plastic packaging materials offer durability, flexibility, and cost efficiency. Pharmaceutical manufacturers used plastic containers for bottles, blister packs, and syringe components. Contract packaging providers adopted plastic materials due to their compatibility with automated packaging systems.

Glass packaging materials will grow at a CAGR of 6.5% during the forecast period. Glass containers are widely used for injectable drugs and biologic formulations. Glass packaging provides chemical stability and protects pharmaceutical products from contamination. Increasing demand for injectable drugs will support the growth of glass packaging in pharmaceutical contract packaging operations.

By End Use

Pharmaceutical companies held the largest share of 52.6% in 2024. These companies relied on contract packaging providers to manage packaging operations and maintain regulatory compliance. Outsourcing packaging activities allowed pharmaceutical manufacturers to focus on research and drug development activities.

Biotechnology companies will register a CAGR of 7.2% during the forecast period. The increasing development of biologic therapies will generate demand for specialized packaging solutions. Contract packaging providers will expand capabilities to handle temperature-sensitive products and sterile packaging processes required for biotechnology products.

Pharmaceutical Contract Packaging Market Segmentations

By Packaging Type

- Blister Packaging

- Bottles

- Vials

- Pre-filled Syringes

- Sachets & Pouches

By Service Type

- Primary Packaging

- Secondary Packaging

- Labeling & Serialization

By Material

- Plastic

- Glass

- Aluminum

- Paper & Paperboard

By End Use

- Pharmaceutical Companies

- Biotechnology Companies

- Medical Device Manufacturers

Regional Analysis

North America

North America held 39.2% of the global pharmaceutical contract packaging market share in 2025. The region benefited from an established pharmaceutical industry, advanced packaging infrastructure, and strong regulatory frameworks. The market in North America will expand at a CAGR of 5.2% from 2025 to 2033 as pharmaceutical companies continue to outsource packaging operations to specialized service providers.

The United States dominated the regional market due to the presence of large pharmaceutical manufacturers and contract packaging companies. The country has developed advanced packaging facilities capable of supporting high-volume pharmaceutical production. Growth in biologics manufacturing and increasing adoption of serialization technologies have strengthened demand for contract packaging services. Pharmaceutical companies in the United States rely on contract packaging providers to meet regulatory compliance requirements and maintain efficient supply chain operations.

Europe

Europe accounted for 27.6% of the pharmaceutical contract packaging market share in 2025. The region’s pharmaceutical sector has historically emphasized quality standards and regulatory compliance. The European market will grow at a CAGR of 5.4% during the forecast period due to increasing outsourcing of packaging operations by pharmaceutical manufacturers.

Germany represented the dominant country in the region. The country has a strong pharmaceutical manufacturing base and advanced packaging technology providers. German contract packaging companies specialize in automated packaging lines and high-precision labeling systems. The presence of several pharmaceutical research centers and biotechnology companies has also supported demand for contract packaging services.

Asia Pacific

Asia Pacific held 22.1% share of the pharmaceutical contract packaging market in 2025. The region has experienced rapid expansion of pharmaceutical manufacturing capacity. The market in Asia Pacific will record the fastest CAGR of 7.1% through 2033 due to increasing pharmaceutical exports and growing contract manufacturing activity.

China emerged as the leading country in the region. The country has expanded pharmaceutical production capacity to support global supply chains. Chinese contract packaging providers are investing in automated packaging lines and modern facilities that meet international regulatory standards. Pharmaceutical manufacturers are partnering with local packaging providers to reduce operational costs and improve production efficiency.

Middle East & Africa

The Middle East & Africa represented about 6.2% of the global pharmaceutical contract packaging market in 2025. The regional market will grow at a CAGR of 5.7% during the forecast period as pharmaceutical manufacturing infrastructure continues to develop.

Saudi Arabia led the regional market due to government initiatives supporting pharmaceutical production. The country has invested in pharmaceutical industrial zones and manufacturing facilities to strengthen healthcare supply chains. Contract packaging providers are expanding operations to support domestic pharmaceutical companies and improve packaging capabilities.

Latin America

Latin America accounted for 4.9% of the pharmaceutical contract packaging market share in 2025. The region’s pharmaceutical industry has been expanding steadily due to increasing healthcare demand and improving manufacturing capabilities. The market will grow at a CAGR of 5.9% through 2033.

Brazil dominated the regional market. The country has a large pharmaceutical manufacturing sector that supports domestic and export markets. Contract packaging providers in Brazil offer packaging services such as blister packing, bottling, and labeling for pharmaceutical products. The presence of several pharmaceutical manufacturing facilities has supported steady demand for contract packaging services.

Competitive Landscape

The pharmaceutical contract packaging market features a mix of global packaging service providers and specialized pharmaceutical packaging companies. Leading companies focus on expanding packaging capabilities, investing in automation technologies, and strengthening compliance with regulatory standards.

Sharp Packaging Services remains a prominent market participant with extensive pharmaceutical packaging operations across North America and Europe. The company has expanded serialization capabilities to support regulatory compliance requirements.

Other companies such as PCI Pharma Services, Catalent Inc., AndersonBrecon, and WestRock Company have established strong positions in the pharmaceutical contract packaging market. These companies offer services including blister packaging, labeling, cold-chain packaging, and logistics support.

Recent strategic initiatives include facility expansions and adoption of automated packaging technologies. Companies are also investing in specialized packaging formats designed for biologics and injectable drugs.

Key Players in the Pharmaceutical Contract Packaging Market

- Sharp Packaging Services

- PCI Pharma Services

- Catalent Inc.

- AndersonBrecon

- WestRock Company

- Jones Packaging

- Reed-Lane Inc.

- Unicep Packaging

- Tjoapack

- Pharma Packaging Solutions

- Wasdell Group

- Multipack Solutions

- Vetter Pharma International

- CordenPharma

- Lonza Group

- Almac Group