Pharmaceutical APET Film Market Size and Growth

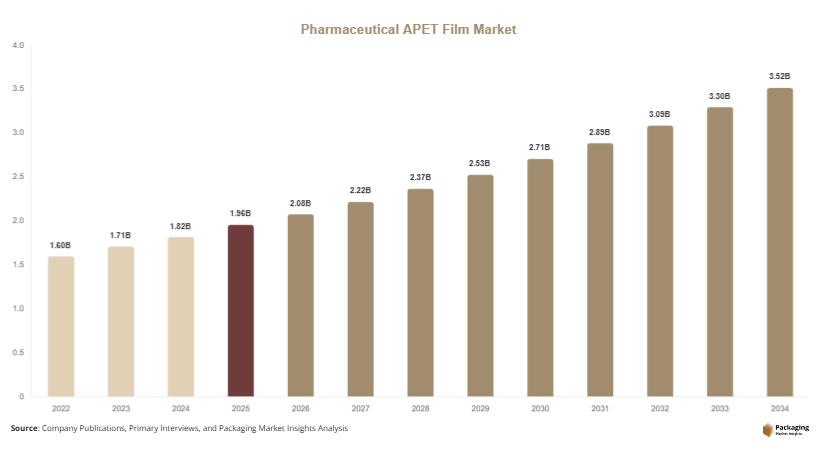

In 2025, the global pharmaceutical APET film market size is estimated at USD 1.96 billion, rising to USD 2.08 billion in 2026. The market is projected to reach approximately USD 3.52 billion by 2034, registering a CAGR of 6.8% during 2025–2034. The pharmaceutical APET film market is expanding steadily due to increasing demand for high-clarity, thermoformable, and recyclable packaging materials in the pharmaceutical sector. APET (Amorphous Polyethylene Terephthalate) films are widely used in blister packaging, medical trays, and sterile barrier systems due to their excellent transparency, chemical resistance, and moisture barrier properties.

Growth in the pharmaceutical APET film market is driven by multiple factors. The rising global demand for pharmaceutical products, particularly generics and over-the-counter drugs, is increasing the need for efficient and protective packaging solutions. In addition, strict regulatory requirements for drug safety and contamination prevention are encouraging the use of high-quality barrier materials such as APET films. Another significant growth factor is the increasing shift toward sustainable packaging, as APET films offer recyclability and lower environmental impact compared to traditional PVC-based materials.

Key Highlights

Asia Pacific dominated the market with a 38.1% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.4%.

Blister packaging films led the type segment with a 33.7% share, while high-barrier multi-layer films are expected to grow at a CAGR of 7.1%.

Plastic-based pharmaceutical packaging dominated with a 54.8% share, while sustainable packaging solutions are forecasted to grow at a CAGR of 6.6%.

Oral solid dosage applications led the segment with 46.2% share, while biologics packaging is expected to grow at a CAGR of 7.3%.

India remained the dominant country with a market size of USD 0.42 billion in 2025 and USD 0.45 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of High-Barrier Multi-Layer APET Films

The pharmaceutical APET film market is witnessing increased adoption of high-barrier multi-layer films designed to improve product protection and shelf life. Pharmaceutical manufacturers are focusing on packaging solutions that provide enhanced resistance to oxygen, moisture, and light exposure. Multi-layer APET films, often combined with materials such as PE or EVOH, are gaining traction due to their ability to maintain drug stability. These films are particularly important for sensitive formulations, including biologics and specialty drugs. The trend is also supported by advancements in extrusion technologies that allow precise layering and improved material efficiency.

Rising Focus on Sustainable and Recyclable Pharmaceutical Packaging

Sustainability is becoming a key trend influencing the pharmaceutical APET film market. Regulatory bodies and pharmaceutical companies are increasingly focusing on reducing environmental impact through recyclable packaging materials. APET films are gaining preference as they can be recycled more easily than PVC-based alternatives. Companies are investing in closed-loop recycling systems and developing mono-material structures to simplify recycling processes. Additionally, the use of post-consumer recycled PET in pharmaceutical packaging is gradually increasing, supported by advancements in purification technologies. This trend aligns with global sustainability goals and is expected to drive innovation in eco-friendly packaging solutions.

Market Drivers

Increasing Demand for Pharmaceutical Packaging Solutions

The growth of the global pharmaceutical industry is a major driver for the pharmaceutical APET film market. Rising demand for prescription drugs, generic medicines, and over-the-counter products is increasing the need for reliable packaging solutions. APET films are widely used in blister packs and medical trays, providing protection against contamination and physical damage. The expansion of healthcare infrastructure and increasing access to medicines in emerging economies are further boosting demand. Pharmaceutical companies are also focusing on packaging innovations to improve product safety and compliance, which is driving the adoption of advanced film materials.

Stringent Regulatory Requirements for Drug Safety

Regulatory frameworks governing pharmaceutical packaging are becoming increasingly stringent, emphasizing product safety and quality assurance. APET films meet many of these requirements due to their high clarity, chemical resistance, and barrier properties. Regulatory authorities require packaging materials to ensure drug stability and prevent contamination during storage and transportation. As a result, pharmaceutical companies are adopting high-quality packaging materials that comply with global standards. The growing emphasis on patient safety and traceability is also encouraging the use of advanced packaging solutions, supporting market growth.

Market Restraint

Limited Barrier Properties Compared to Advanced Alternatives

One of the challenges in the pharmaceutical APET film market is the relatively limited barrier performance of standard APET films compared to advanced materials such as PVDC or aluminum-based laminates. While APET offers good clarity and recyclability, it may require additional coatings or layers to achieve the desired level of protection for highly sensitive drugs. This increases production complexity and cost. In some cases, pharmaceutical manufacturers may opt for alternative materials that provide superior barrier properties. This limitation can restrict the use of APET films in certain high-performance packaging applications.

Market Opportunities

Expansion of Biologics and Specialty Drug Packaging

The growing market for biologics and specialty pharmaceuticals presents significant opportunities for APET film manufacturers. These drugs require advanced packaging solutions that ensure stability and prevent degradation. High-barrier APET films are being developed to meet these requirements, offering improved protection while maintaining transparency and recyclability. As the biologics segment continues to expand, demand for specialized packaging materials is expected to increase.

Growth in Emerging Pharmaceutical Markets

Emerging economies such as India, China, and Brazil are witnessing rapid growth in pharmaceutical manufacturing. Increasing healthcare access and government initiatives to boost domestic drug production are driving demand for packaging materials. APET films are widely used due to their cost-effectiveness and performance advantages. The expansion of contract manufacturing organizations in these regions is also contributing to market growth, creating new opportunities for film producers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.96 Billion |

| Market Size in 2026 | USD 2.08 Billion |

| Market Size in 2034 | USD 3.52 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Blister packaging films dominated the market with a 33.7% share in 2024 due to their widespread use in oral solid dosage packaging. These films provide excellent clarity and protection, making them suitable for tablets and capsules.

High-barrier multi-layer films are the fastest-growing segment with a CAGR of 7.1%. Growth is driven by increasing demand for advanced packaging solutions for sensitive pharmaceutical products.

By Application

Oral solid dosage packaging accounted for the largest share of 46.2% in 2024 due to high consumption of tablets and capsules globally. APET films are widely used in blister packs for these products.

Biologics packaging is the fastest-growing application segment with a CAGR of 7.3%. Growth is driven by increasing demand for specialized packaging solutions for complex drug formulations.

By End-Use Industry

Pharmaceutical manufacturing dominated the market with a 48.9% share in 2024 due to extensive use of APET films in drug packaging processes.

Contract manufacturing organizations are the fastest-growing segment with a CAGR of 6.9%. Growth is driven by outsourcing trends in pharmaceutical production.

Pharmaceutical APET Film Market Segmentations

By Type

- Blister Packaging Films

- High-Barrier Multi-Layer Films

- Medical Tray Films

By Application

- Oral Solid Dosage Packaging

- Liquid Drug Packaging

- Biologics Packaging

By End-Use Industry

- Pharmaceutical Manufacturing

- Contract Manufacturing Organizations

- Healthcare Institutions

Regional Analysis

North America

North America accounted for approximately 25.8% of the pharmaceutical APET film market share in 2025 and is expected to grow at a CAGR of 6.2% during the forecast period. The region benefits from a well-established pharmaceutical industry and advanced packaging technologies. Demand for high-quality blister packaging and sterile medical trays is driving market growth.

The United States is the dominant country in the region, supported by a large pharmaceutical manufacturing base and strong regulatory framework. A key growth factor is the increasing demand for sustainable packaging solutions that comply with environmental regulations.

Europe

Europe held around 22.4% market share in 2025 and is projected to grow at a CAGR of 5.9%. The region is characterized by strict regulatory standards and strong focus on sustainability. Pharmaceutical companies in Europe are adopting recyclable packaging materials to meet environmental targets.

Germany leads the market in Europe due to its advanced pharmaceutical and chemical industries. A key growth factor is the increasing investment in research and development of innovative packaging materials.

Asia Pacific

Asia Pacific dominated the pharmaceutical APET film market with a 38.1% share in 2025 and is expected to grow at a CAGR of 7.3%. Rapid industrialization, expanding pharmaceutical manufacturing, and increasing healthcare demand are driving growth.

India is the leading country in the region due to its large generic drug manufacturing industry. A key growth factor is government support for domestic pharmaceutical production and export activities.

Middle East & Africa

The Middle East & Africa region accounted for 7.6% of the market share in 2025 and is projected to grow at a CAGR of 5.8%. Growth is supported by increasing healthcare investments and rising demand for pharmaceutical products.

Saudi Arabia dominates the region due to its expanding healthcare infrastructure. A key growth factor is government initiatives aimed at improving local pharmaceutical production capabilities.

Latin America

Latin America held 6.1% market share in 2025 and is expected to grow at a CAGR of 6.4%. The region is witnessing increasing pharmaceutical production and improving healthcare access.

Brazil is the dominant country in Latin America due to its strong pharmaceutical industry. A key growth factor is the expansion of domestic drug manufacturing and export activities.

Competitive Landscape

The pharmaceutical APET film market is moderately competitive, with key players focusing on innovation and sustainability. Major companies include Amcor plc, Klöckner Pentaplast, Berry Global Inc., Uflex Ltd., and Polyplex Corporation. Among these, Klöckner Pentaplast is a leading player due to its extensive product portfolio and global presence.

Companies are investing in recyclable film technologies and expanding production capacities to meet growing demand. Recent developments include the introduction of high-barrier APET films and partnerships with pharmaceutical companies for customized packaging solutions.

Key Players List

- Amcor plc

- Klöckner Pentaplast

- Berry Global Inc.

- Uflex Ltd.

- Polyplex Corporation

- Toray Industries

- DuPont Teijin Films

- Mitsubishi Chemical Group

- Cosmo Films Ltd.

- Jindal Poly Films

- SRF Limited

- Tekni-Plex Inc.

- Constantia Flexibles

- Sealed Air Corporation

- Schur Flexibles