PET VCI Shrink Film Market

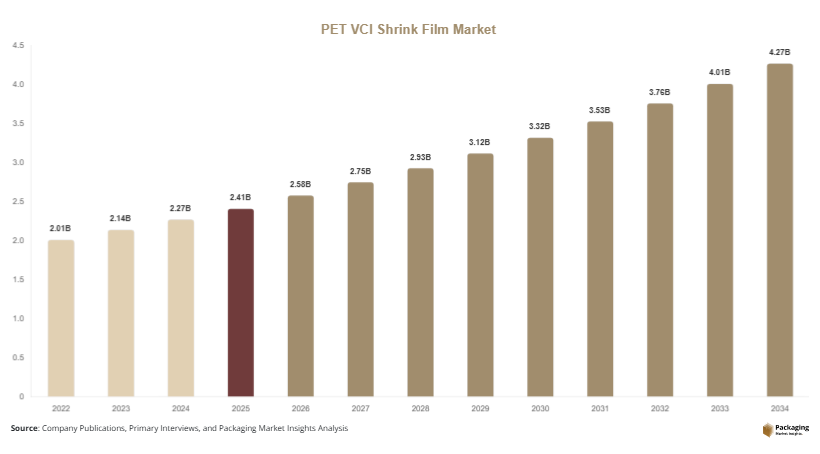

In 2025, the global PET VCI shrink film market size is estimated at approximately USD 2.41 billion, which is projected to reach USD 2.58 billion in 2026. Looking ahead, the market is expected to attain around USD 4.32 billion by 2034, registering a CAGR of 6.5% from 2025 to 2034. The growth trajectory reflects rising integration of vapor corrosion inhibitor technology within PET shrink films used across automotive, industrial machinery, aerospace, and electronics packaging applications. The PET VCI shrink film market is witnessing consistent expansion as industries increasingly prioritize corrosion protection, export durability, and advanced polymer-based packaging solutions.

A major growth factor is the expansion of global manufacturing and cross-border trade, which has increased the need for long-term corrosion-resistant packaging. Another key driver is the shift toward recyclable PET-based materials as industries move away from PVC-based shrink films due to environmental concerns. Additionally, improvements in multi-layer film extrusion and nano-additive dispersion technologies are enhancing film durability, transparency, and corrosion protection efficiency.

Key Highlights

Asia Pacific dominated the market with a 37.4% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.2%.

Antioxidants led the type segment with a 29.6% share, while antimicrobial additives are expected to grow at a CAGR of 6.5%.

Plastic packaging dominated with a 52.3% share, while paper-based packaging is forecasted to grow at a CAGR of 5.9%.

Food & beverage applications led the segment with 43.1% share, while healthcare packaging is expected to grow at a CAGR of 6.3%.

China remained the dominant country with a market size of USD 11.2 billion in 2025 and USD 11.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Integration of Multi-Functional Protective Packaging Systems

The PET VCI shrink film market is experiencing a shift toward multi-functional packaging solutions that combine corrosion protection with moisture resistance, UV shielding, and tamper-evident features. Traditional shrink films were limited to containment functions, but modern PET VCI films are engineered with advanced vapor-phase inhibitors that form a protective molecular barrier on metal surfaces. This ensures long-term protection of industrial components during storage and overseas shipping. Industries such as automotive and aerospace are increasingly adopting these solutions to reduce product degradation risks. Additionally, manufacturers are incorporating layered structures to improve mechanical strength and enhance film clarity while maintaining corrosion resistance performance.

Rising Demand for Sustainable and Recyclable PET-Based Solutions

Sustainability concerns are significantly shaping the evolution of the PET VCI shrink film market. PET-based shrink films are gaining preference due to their recyclability and reduced environmental impact compared to conventional PVC films. Regulatory frameworks in Europe and North America are encouraging manufacturers to adopt eco-friendly packaging materials that align with circular economy principles. In addition, companies are investing in bio-enhanced PET resins and solvent-free VCI formulations to minimize environmental emissions. Industrial end-users are also focusing on reducing packaging waste without compromising corrosion protection performance. This transition toward sustainable packaging is expected to accelerate innovation in green chemistry-based VCI additives and recyclable multilayer film structures.

Market Drivers

Expansion of Global Industrial Manufacturing and Export Activities

The growth of global industrial manufacturing and export activities is a key driver of the PET VCI shrink film market. Increasing international trade in machinery, automotive parts, and heavy equipment has created strong demand for corrosion-resistant packaging solutions. PET VCI shrink films are widely used to protect metal components during long-distance transportation and extended storage periods. Emerging economies in Asia Pacific are becoming major manufacturing hubs, further increasing export volumes. As global supply chains become more complex, manufacturers require reliable packaging solutions that ensure product integrity across varying climatic conditions. This has significantly boosted adoption across industrial logistics networks.

Rising Adoption in Automotive and Precision Engineering Industries

Automotive and precision engineering sectors are major contributors to market growth. Components such as engines, gears, and machined metal parts are highly susceptible to oxidation during storage and shipping. PET VCI shrink films provide effective corrosion protection without requiring additional chemical treatments, reducing operational complexity. The growth of electric vehicle production has further increased demand for protective packaging for sensitive components such as battery parts and electronic assemblies. Manufacturers are also standardizing packaging protocols across global production facilities, increasing reliance on high-performance shrink films. This trend is expected to continue as automotive supply chains expand globally.

Market Restraint

High Production Costs and Raw Material Price Volatility

A major challenge in the PET VCI shrink film market is the high production cost associated with PET resins and specialized VCI additives. Price fluctuations in raw materials linked to crude oil markets directly affect manufacturing stability and profit margins. Advanced extrusion and multilayer film production technologies also require significant capital investment, limiting scalability for smaller manufacturers. In price-sensitive regions, end-users often opt for lower-cost packaging alternatives despite lower corrosion protection performance. This cost barrier restricts widespread adoption, particularly in developing economies where budget constraints influence procurement decisions.

Market Opportunities

Expansion in Aerospace and Defense Packaging Applications

The aerospace and defense sectors present strong growth opportunities for PET VCI shrink films. High-value components such as aircraft engines, structural parts, and defense equipment require long-term corrosion protection during storage and transportation. PET VCI films offer superior barrier properties, making them suitable for mission-critical applications. Increasing aircraft production rates and rising defense modernization programs globally are boosting demand. Additionally, strict regulatory standards for equipment preservation are encouraging adoption of advanced corrosion prevention packaging systems. This segment is expected to become a major contributor to market expansion over the forecast period.

Advancements in Smart and Nano-Enhanced Packaging Technologies

Technological innovation is creating new opportunities in the PET VCI shrink film market through the development of smart and nano-enhanced packaging materials. Manufacturers are integrating nano-scale corrosion inhibitors that improve vapor diffusion and extend protection duration. Smart packaging concepts such as humidity indicators and corrosion monitoring sensors are also being explored for high-value industrial applications. These innovations enable real-time condition tracking of packaged goods, improving supply chain visibility. As Industry 4.0 adoption increases, demand for intelligent protective packaging solutions is expected to grow significantly across industrial sectors.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.41 Billion |

| Market Size in 2026 | USD 2.58 Billion |

| Market Size in 2034 | USD 4.32 Billion |

| CAGR | 6.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Antioxidant-based VCI films dominated the market with a 34.1% share in 2024 due to their cost-effectiveness and reliable corrosion protection for ferrous metals. These films are widely used across industrial packaging applications where long-term storage protection is required.

Antimicrobial and hybrid additive-based films are the fastest-growing category with a CAGR of 6.7%. Growth is driven by increasing demand for advanced packaging materials that combine corrosion resistance with microbial protection, especially in sensitive industrial environments.

By Application

Industrial equipment packaging held the largest share of 38.5% in 2024 due to strong demand from automotive and machinery sectors. These industries require durable packaging solutions to protect components during global transportation and storage cycles.

Electronics and precision component packaging is the fastest-growing application segment with a CAGR of 6.4%. Growth is driven by increasing sensitivity of electronic devices and the need for contamination-free, corrosion-resistant packaging solutions.

By End-Use Industry

The automotive industry dominated the market with a 41.2% share in 2024 due to widespread use of VCI shrink films for protecting metal parts and assemblies during logistics operations.

Aerospace and defense is the fastest-growing end-use segment with a CAGR of 6.6%, driven by increasing aircraft production and stringent requirements for corrosion prevention in high-value components.

PET VCI Shrink Film Market Segmentations

By Type

- Antioxidant VCI Films

- Antimicrobial VCI Films

- Hybrid Additive Films

By Application

- Industrial Equipment Packaging

- Automotive Components Packaging

- Electronics Packaging

- Aerospace Components Packaging

By End-Use Industry

- Automotive

- Aerospace & Defense

- Industrial Manufacturing

- Electronics & Electrical

- Heavy Engineering

Regional Analysis

North America

North America accounted for approximately 24.6% of the global market share in 2025, with a projected CAGR of 6.1% through 2034. Growth is supported by strong demand from automotive, aerospace, and defense industries, which require high-performance corrosion protection packaging. The region also benefits from advanced logistics infrastructure and high adoption of industrial packaging standards across manufacturing sectors.

The United States remains the dominant country in North America due to its large-scale automotive production base and defense manufacturing industry. A key growth factor is the increasing shift toward sustainable PET-based packaging materials driven by environmental regulations and corporate sustainability initiatives.

Europe

Europe held around 21.3% market share in 2025 and is projected to grow at a CAGR of 5.8% during the forecast period. The region is characterized by strict environmental regulations and strong demand for recyclable industrial packaging materials. Advanced manufacturing industries in Europe require high-performance corrosion protection solutions for export-oriented production.

Germany dominates the European market due to its strong automotive and machinery manufacturing sectors. A key growth factor is the increasing adoption of precision engineering technologies, which require reliable and contamination-free packaging solutions for sensitive components.

Asia Pacific

Asia Pacific dominated the global market with a 37.4% share in 2025 and is expected to grow at a CAGR of 7.2%. Rapid industrialization, expanding export activities, and strong manufacturing infrastructure contribute to regional dominance. The region also benefits from cost-effective production capabilities and rising global trade participation.

China is the leading country in the region due to its large-scale industrial output and export-oriented manufacturing base. A key growth factor is the expansion of integrated industrial clusters focused on machinery, electronics, and automotive production for global supply chains.

Middle East & Africa

The Middle East & Africa region accounted for 8.5% of the global market share in 2025, with a projected CAGR of 5.9%. Growth is driven by infrastructure development, industrial diversification programs, and increasing export of oil and gas equipment requiring corrosion protection packaging.

Saudi Arabia leads the regional market due to its expanding industrial base and logistics infrastructure development initiatives. A key growth factor is the country’s economic diversification strategy, which is encouraging manufacturing and non-oil industrial exports.

Latin America

Latin America held 8.2% market share in 2025 and is projected to grow at the fastest regional CAGR of 6.2%. Growth is supported by increasing automotive assembly operations, industrial exports, and improving logistics infrastructure across the region.

Brazil dominates the Latin American market due to its strong automotive manufacturing sector and expanding participation in global supply chains. A key growth factor is the increasing investment in industrial modernization and export-oriented production capabilities.

Competitive Landscape

The PET VCI shrink film market is moderately consolidated with leading companies focusing on innovation, sustainability, and global expansion strategies. Key players include Sealed Air Corporation, Berry Global Inc., Intertape Polymer Group, Cortec Corporation, and AEP Industries. Among these, Cortec Corporation maintains a strong position due to its advanced VCI technology portfolio.

Recent developments include expansion of PET-based production facilities in Asia, introduction of nano-enhanced corrosion protection films, and strategic collaborations between packaging manufacturers and automotive OEMs. Companies are also investing in recyclable film technologies and smart packaging integration to strengthen their market position.

Key Players List

- Sealed Air Corporation

- Berry Global Inc.

- Intertape Polymer Group

- Cortec Corporation

- AEP Industries

- Bollore Group

- Polyplex Corporation

- Uflex Ltd.

- Clariant AG

- Daubert Cromwell

- Metpro Group

- Armor Protective Packaging

- SKC Co. Ltd.

- Mitsubishi Chemical Group

- Trioplast Industrier