Pet Rigid Plastic Packaging Market Size and Growth

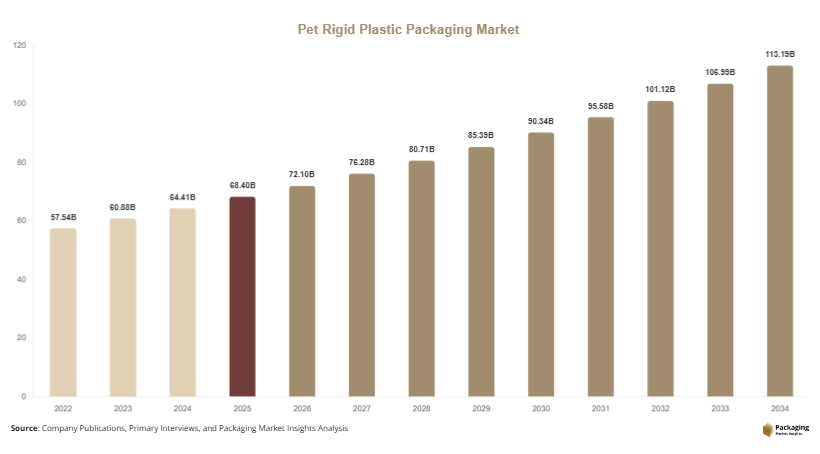

The global pet rigid plastic packaging market size was valued at approximately USD 68.4 billion in 2025 and is estimated to reach USD 72.1 billion in 2026. With rising consumption across food & beverages, personal care, and pharmaceuticals, the market is projected to grow at a compound annual growth rate (CAGR) of 5.8% from 2025 to 2034, reaching nearly USD 118.7 billion by 2034. The pet rigid plastic packaging market is experiencing steady expansion driven by increasing demand for lightweight, durable, and cost-effective packaging solutions across multiple end-use industries.

Growth in the market is supported by several factors. First, the increasing adoption of polyethylene terephthalate (PET) due to its recyclability and lightweight properties is significantly boosting demand. PET packaging offers superior barrier protection against moisture and gases, making it suitable for food and beverage storage. Second, the rising consumption of bottled beverages, particularly in emerging economies, is fueling the need for rigid plastic packaging solutions. Third, advancements in manufacturing technologies such as injection molding and blow molding are improving product quality while reducing production costs, further enhancing market penetration.

Key Market Insights:

- Asia Pacific dominated the market with a 38.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.4%.

- Bottles led the product segment with a 46.7% share, while containers are expected to grow at a CAGR of 6.1%.

- Food & beverage applications dominated with a 49.3% share, while pharmaceutical packaging is projected to grow at a CAGR of 6.6%.

- Polyethylene terephthalate (PET) material held a 61.5% share, while recycled PET is forecasted to grow at a CAGR of 7.2%.

- China remained the dominant country with a market size of USD 13.4 billion in 2025 and USD 14.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Recycled PET (rPET) Materials

The increasing shift toward sustainability is significantly influencing the pet rigid plastic packaging market. Manufacturers are actively incorporating recycled PET into their production processes to reduce environmental impact and comply with regulatory requirements. rPET offers similar performance characteristics as virgin PET while reducing carbon footprint and dependence on fossil fuels. Many companies are setting targets to increase the percentage of recycled content in their packaging portfolios, particularly in beverage bottles and food containers. Additionally, governments are introducing mandates encouraging the use of recycled materials, which is accelerating adoption. Consumer awareness regarding sustainable packaging is also driving brands to prioritize eco-friendly solutions, further supporting the growth of rPET-based packaging products across global markets.

Lightweight Packaging and Design Optimization

Another notable trend shaping the market is the increasing focus on lightweight packaging solutions. Manufacturers are optimizing product designs to reduce material usage without compromising strength or functionality. This trend is particularly prominent in the beverage industry, where lightweight PET bottles are widely used to minimize transportation costs and improve supply chain efficiency. Advanced engineering techniques and material innovations are enabling companies to produce thinner yet durable packaging structures. In addition, lightweight packaging contributes to lower greenhouse gas emissions, aligning with sustainability goals. As companies aim to balance cost efficiency and environmental responsibility, lightweight PET rigid packaging is expected to witness continued adoption across multiple industries.

Market Drivers

Growth of the Beverage Industry

The expansion of the global beverage industry is a major driver of the pet rigid plastic packaging market. PET bottles are widely used for packaging water, carbonated drinks, juices, and energy beverages due to their durability, transparency, and cost-effectiveness. The increasing demand for packaged drinking water, particularly in urban areas and developing regions, is fueling the need for PET packaging solutions. Additionally, changing lifestyles and rising disposable incomes are contributing to higher consumption of ready-to-drink beverages. Manufacturers prefer PET packaging because it offers ease of transportation and longer shelf life for liquid products. The ongoing innovation in bottle design and closure systems is further enhancing product appeal, supporting sustained market growth.

Expansion of the Food and Personal Care Industries

The growing demand for packaged food products and personal care items is another key factor driving the market. PET rigid packaging is widely used for storing edible oils, sauces, cosmetics, and hygiene products due to its excellent barrier properties and chemical resistance. The increasing preference for convenience foods and ready-to-use products is boosting demand for reliable packaging solutions. Additionally, the personal care industry relies heavily on PET containers for products such as shampoos, lotions, and skincare items. As consumers seek high-quality and visually appealing packaging, manufacturers are investing in innovative designs and enhanced functionality. This trend is expected to continue driving demand for PET rigid plastic packaging across various applications.

Market Restraint

Environmental Concerns and Regulatory Pressure

Environmental concerns related to plastic waste remain a significant restraint for the pet rigid plastic packaging market. Despite PET being recyclable, improper waste management and low recycling rates in certain regions contribute to environmental pollution. Governments worldwide are implementing strict regulations to reduce plastic usage and promote sustainable alternatives. Policies such as plastic bans, extended producer responsibility (EPR), and recycling mandates are increasing compliance costs for manufacturers. These regulations can impact production processes and limit the use of virgin plastic materials. For instance, several countries have introduced restrictions on single-use plastics, which directly affect packaging demand. As a result, companies must invest in recycling infrastructure and alternative materials, which may increase operational expenses and affect profit margins.

Market Opportunities

Advancements in Bio-Based PET Materials

The development of bio-based PET materials presents a significant growth opportunity for the market. Bio-based PET is derived from renewable resources, reducing dependence on fossil fuels and lowering environmental impact. As sustainability becomes a key priority for consumers and regulatory bodies, companies are exploring innovative materials to enhance their product offerings. Bio-based PET retains the desirable properties of conventional PET, including strength, clarity, and recyclability, making it a viable alternative. The increasing investment in research and development is expected to accelerate the commercialization of these materials. This trend offers manufacturers an opportunity to differentiate their products and meet evolving consumer demands.

Expansion in Emerging Markets

Emerging economies present substantial growth opportunities for the pet rigid plastic packaging market. Rapid urbanization, population growth, and rising disposable incomes are driving demand for packaged goods in regions such as Asia Pacific, Latin America, and Africa. The expansion of retail infrastructure and e-commerce platforms is further increasing the need for durable and efficient packaging solutions. Additionally, the growing awareness of hygiene and food safety is encouraging consumers to opt for packaged products. Companies are focusing on expanding their presence in these regions by establishing production facilities and distribution networks. This strategic expansion is expected to contribute significantly to market growth over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 68.4 Billion |

| Market Size in 2026 | USD 72.1 Billion |

| Market Size in 2034 | USD 118.7 Billion |

| CAGR | 5.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Product Type

The bottles segment dominated the pet rigid plastic packaging market in 2024, accounting for approximately 46.7% of the total market share. PET bottles are widely used in the beverage industry due to their lightweight nature, durability, and transparency. They are suitable for packaging water, soft drinks, juices, and other liquid products. The high demand for bottled beverages, particularly in urban areas, is driving the growth of this segment. Additionally, advancements in bottle design and manufacturing technologies are enhancing product performance and reducing material usage. The increasing adoption of recycled PET in bottle production is also contributing to the segment’s growth.

The containers segment is expected to be the fastest-growing category, with a projected CAGR of 6.1% during the forecast period. Containers are widely used for packaging food, personal care products, and household items. The growth of this segment is driven by the increasing demand for convenience foods and ready-to-use products. Additionally, the rising popularity of e-commerce is boosting demand for durable and protective packaging solutions. Manufacturers are focusing on developing innovative container designs to enhance functionality and improve consumer experience.

By Application

The food & beverage segment held the largest share of the market in 2024, accounting for approximately 49.3%. PET rigid packaging is widely used in this sector due to its excellent barrier properties and ability to preserve product freshness. The increasing demand for packaged food and beverages is driving the growth of this segment. Additionally, the rising consumption of ready-to-eat meals and convenience foods is further supporting market expansion. Manufacturers are investing in advanced packaging solutions to improve product shelf life and enhance consumer appeal.

The pharmaceutical segment is expected to grow at the fastest CAGR of 6.6% during the forecast period. The increasing demand for safe and reliable packaging solutions for medicines and healthcare products is driving this growth. PET packaging offers excellent protection against contamination and ensures product integrity. Additionally, the rising prevalence of chronic diseases and the growing healthcare industry are contributing to the demand for pharmaceutical packaging solutions.

By Material

The polyethylene terephthalate (PET) segment dominated the market in 2024, accounting for approximately 61.5% of the total share. PET is widely used due to its strength, clarity, and recyclability. It is suitable for a wide range of applications, including food, beverages, and personal care products. The increasing demand for lightweight and cost-effective packaging solutions is driving the growth of this segment. Additionally, advancements in PET manufacturing technologies are improving product performance and reducing environmental impact.

The recycled PET (rPET) segment is expected to grow at the fastest CAGR of 7.2% during the forecast period. The growth of this segment is driven by increasing environmental awareness and regulatory requirements promoting the use of recycled materials. Companies are investing in recycling infrastructure and technologies to enhance the quality and availability of rPET. This trend is expected to support the growth of sustainable packaging solutions in the market.

Pet Rigid Plastic Packaging Market Segmentations

By Product Type

- Bottles

- Containers

- Jars

- Others

By Application

- Food & Beverage

- Pharmaceutical

- Personal Care

- Household Products

By Material

- Polyethylene Terephthalate (PET)

- Recycled PET (rPET)

- Bio-based PET

Regional Analysis

North America

North America accounted for a significant share of the pet rigid plastic packaging market in 2025, contributing approximately 24.6% of the global revenue. The region is expected to grow at a CAGR of 5.1% during the forecast period. The presence of well-established food & beverage and healthcare industries is driving demand for PET packaging. Additionally, the increasing adoption of sustainable packaging solutions is influencing market dynamics. Companies in the region are focusing on incorporating recycled materials and improving packaging efficiency.

The United States dominates the North American market due to its advanced manufacturing capabilities and high consumption of packaged goods. A key growth factor in the country is the increasing demand for bottled beverages and convenience foods. The strong presence of leading packaging companies and ongoing technological advancements further support market growth.

Europe

Europe held a market share of around 22.3% in 2025 and is projected to grow at a CAGR of 5.3%. The region is characterized by stringent environmental regulations and a strong focus on sustainability. The adoption of recycled PET and circular economy practices is driving innovation in packaging solutions. Additionally, the growing demand for eco-friendly products is encouraging companies to invest in sustainable packaging technologies.

Germany leads the European market, supported by its robust manufacturing sector and advanced recycling infrastructure. A unique growth factor in the country is the widespread implementation of deposit return schemes, which promote recycling and increase the availability of recycled materials for packaging production.

Asia Pacific

Asia Pacific dominated the global market with a share of 38.2% in 2025 and is expected to grow at a CAGR of 6.2%. Rapid urbanization, population growth, and increasing disposable incomes are driving demand for packaged products in the region. The expansion of the food & beverage industry and the growing popularity of bottled drinks are key factors supporting market growth.

China is the leading country in the region, driven by its large population and strong manufacturing base. A major growth factor is the increasing demand for packaged food and beverages, supported by rising consumer awareness of hygiene and convenience. Government initiatives promoting recycling and sustainable practices are also contributing to market expansion.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7.8% of the market share in 2025 and is expected to grow at a CAGR of 5.6%. The increasing demand for packaged food and beverages, coupled with the expansion of retail sectors, is driving market growth. Additionally, the rising awareness of food safety and hygiene is encouraging the adoption of PET packaging solutions.

Saudi Arabia is a key market in the region, supported by its growing food and beverage industry. A unique growth factor is the increasing investment in infrastructure and retail development, which is boosting demand for packaged products and associated packaging solutions.

Latin America

Latin America held a market share of around 7.1% in 2025 and is projected to grow at the fastest CAGR of 6.4%. The region is witnessing increasing demand for packaged goods due to urbanization and changing consumer lifestyles. The expansion of the beverage industry is a major driver of market growth.

Brazil dominates the Latin American market, driven by its large consumer base and growing retail sector. A key growth factor is the rising consumption of bottled beverages, which is increasing the demand for PET rigid plastic packaging solutions across the country.

Competitive Landscape

The pet rigid plastic packaging market is moderately competitive, with several global and regional players operating in the industry. Key companies are focusing on product innovation, sustainability, and strategic partnerships to strengthen their market position. The market leader, Amcor plc, has a strong global presence and offers a wide range of packaging solutions across various industries. The company is actively investing in sustainable packaging technologies, including the use of recycled and bio-based materials.

Other major players such as Berry Global Inc., ALPLA Group, Plastipak Holdings, and Silgan Holdings are also contributing to market growth through continuous innovation and expansion strategies. Recent developments include investments in recycling facilities and the introduction of lightweight packaging solutions. Companies are also focusing on mergers and acquisitions to expand their product portfolios and geographic reach. The competitive landscape is expected to remain dynamic as companies strive to meet evolving consumer demands and regulatory requirements.

Key Players List

- Amcor plc

- Berry Global Inc.

- ALPLA Group

- Plastipak Holdings Inc.

- Silgan Holdings Inc.

- Gerresheimer AG

- Graham Packaging Company

- Retal Industries Ltd.

- Resilux NV

- Logoplaste Group

- CCL Industries Inc.

- Esterform Packaging Ltd.

- Indorama Ventures Public Company Limited

- Alpha Packaging

- Altium Packaging