Pet Food Packaging Market Size and Growth

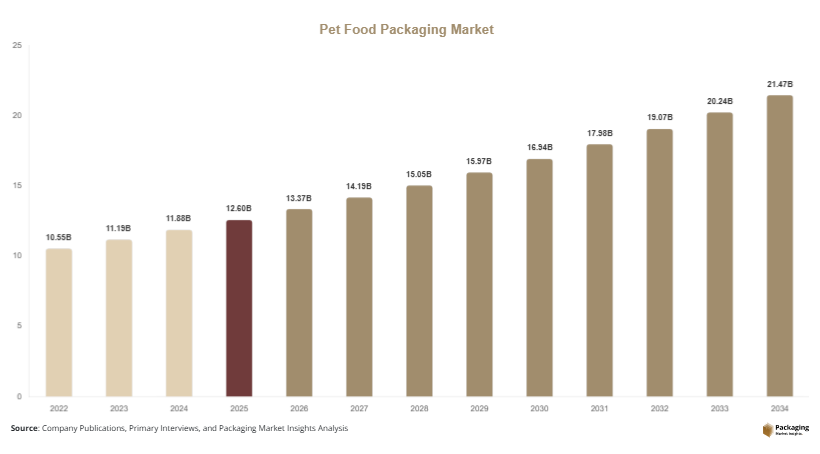

The pet food packaging market size was valued at USD 12.6 billion in 2025 and is projected to reach USD 21.4 billion by 2034, registering a CAGR of 6.1% from 2025 to 2034. The market growth reflects the expanding global pet population and rising demand for packaged pet nutrition products that require safe, durable, and convenient packaging formats. Pet food manufacturers increasingly rely on advanced packaging solutions to preserve freshness, enhance shelf life, and provide consumer convenience, which continues to support market expansion across developed and emerging economies.

A major global factor supporting the growth of the pet food packaging market is the rising trend of pet humanization. Pet owners are increasingly purchasing premium pet food products, including organic, grain-free, and specialized nutrition formulas. These products require packaging that maintains product integrity, supports brand differentiation, and communicates product information effectively. As a result, manufacturers are adopting flexible packaging materials, resealable formats, and recyclable solutions that align with both functionality and sustainability expectations.

Key Highlights

- North America accounted for the dominant regional share of 38.2% in 2025, while Asia Pacific is expected to record the fastest CAGR of 7.4% during the forecast period.

- By packaging type, bags & pouches held the leading share of 46.7% in 2025, while flexible stand-up pouches are expected to grow at a CAGR of 7.2%.

- By material type, plastic packaging dominated with 52.9% share in 2025, while paper & paperboard packaging is projected to grow at 6.8% CAGR.

- The United States, the dominant country, recorded a market size of USD 3.9 billion in 2025, expected to reach USD 4.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable Packaging Materials

Sustainability has emerged as a defining trend shaping the pet food packaging market. Consumers are increasingly aware of environmental concerns and are demanding packaging formats that reduce plastic waste and carbon footprints. Pet food brands are responding by introducing recyclable, compostable, and biodegradable packaging materials. Paper-based bags, mono-material films, and recyclable flexible pouches are gaining attention as companies seek to meet regulatory guidelines and sustainability targets. Packaging manufacturers are also investing in lightweight designs and reduced material usage to improve environmental performance while maintaining product protection. This trend is expected to continue influencing packaging innovation and supplier strategies across the industry.

Growing Adoption of Flexible and Resealable Packaging

Flexible packaging formats such as stand-up pouches and resealable bags are gaining widespread adoption within the pet food packaging market. These formats offer multiple advantages, including reduced transportation costs, improved storage efficiency, and enhanced consumer convenience. Features such as zip locks, tear notches, and easy-pour openings improve usability for pet owners while maintaining product freshness. Pet food brands are increasingly using flexible packaging to differentiate products on retail shelves and enhance visual appeal through high-quality printing and branding elements. As pet food consumption shifts toward premium and specialty diets, flexible packaging is expected to remain a preferred solution due to its versatility and cost efficiency.

Market Drivers

Rising Global Pet Ownership

The increasing adoption of companion animals is a key driver of the pet food packaging market. Urbanization, changing lifestyles, and rising disposable incomes have contributed to higher pet ownership levels worldwide. Households are increasingly adopting dogs, cats, and other companion animals, which has boosted demand for commercial pet food products. Packaged pet food products require specialized packaging solutions to ensure product safety, hygiene, and shelf life stability. As pet populations expand, manufacturers continue to increase production volumes, thereby driving demand for innovative packaging formats across dry, wet, and specialty pet food categories.

Expansion of Premium Pet Food Products

The rapid expansion of premium and specialized pet food offerings is also driving growth in the pet food packaging market. Pet owners are increasingly selecting high-quality pet food formulations that include organic ingredients, functional additives, and breed-specific nutrition. These premium products require packaging that protects sensitive ingredients from moisture, oxygen, and contamination. Additionally, premium brands emphasize attractive packaging designs to communicate product quality and brand identity. Packaging technologies such as multi-layer barrier films, resealable closures, and high-definition printing enable manufacturers to meet these requirements while maintaining product freshness and consumer convenience.

Market Restraint

Volatility in Raw Material Prices

Fluctuations in raw material prices remain a significant restraint for the pet food packaging market. Packaging materials such as plastics, aluminum, and specialty films are heavily influenced by changes in global commodity prices. Petrochemical feedstock price volatility directly affects the cost of plastic-based packaging materials, which are widely used in flexible pet food packaging formats.

These cost fluctuations can create uncertainty for packaging manufacturers and pet food producers. Rising material costs often reduce profit margins or force manufacturers to adjust product pricing, which may influence purchasing decisions across price-sensitive markets. Additionally, the development of alternative packaging materials often requires significant investments in research and development, manufacturing adjustments, and supply chain restructuring.

Another challenge arises from regulatory pressures related to plastic usage and recycling requirements. Packaging producers must invest in sustainable materials and compliance initiatives, which can increase production costs. These factors collectively contribute to operational challenges for manufacturers operating within the pet food packaging market, potentially slowing adoption of new packaging technologies and limiting short-term market growth in certain regions.

Market Opportunities

Growth of Smart and Intelligent Packaging

Smart packaging technologies represent a promising opportunity in the pet food packaging market. Intelligent packaging solutions such as freshness indicators, QR codes, and digital traceability features allow manufacturers to enhance transparency and product safety. These technologies enable consumers to access product information related to ingredient sourcing, expiration dates, and storage conditions.

Pet food brands are exploring digital packaging tools to strengthen consumer trust and improve product monitoring across supply chains. Smart labels and interactive packaging also support brand engagement and marketing strategies by enabling consumers to access product details through smartphones. As technology integration becomes more accessible, smart packaging is expected to gain traction within premium and specialized pet food categories.

Rising Demand in Emerging Markets

Emerging economies present substantial growth potential for the pet food packaging market. Countries across Asia Pacific and Latin America are witnessing rising pet ownership rates due to increasing urbanization and growing middle-class populations. As consumer awareness of commercial pet nutrition increases, demand for packaged pet food products is expected to expand significantly.

This shift creates opportunities for packaging manufacturers to introduce cost-effective and durable packaging solutions tailored to regional consumption patterns. Flexible packaging formats and lightweight materials are particularly attractive for emerging markets due to their affordability and logistical advantages. These factors position developing economies as important growth areas for the pet food packaging market over the coming decade.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12.6 Billion |

| Market Size in 2026 | USD 13.37 Billion |

| Market Size in 2034 | USD 21.4 Billion |

| CAGR | 6.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Packaging Type

Bags & pouches represented the dominant subsegment in the pet food packaging market and accounted for 46.7% of the market share in 2025. These packaging formats were widely used due to their lightweight design, durability, and cost efficiency. Pet food manufacturers preferred bags and pouches for dry pet food products because they offer strong barrier protection against moisture and oxygen. In addition, flexible bags enable efficient transportation and storage while providing ample surface area for branding and product information.

The stand-up pouch segment is expected to record the fastest growth with a CAGR of 7.2% during the forecast period. This growth will be driven by increasing demand for convenient packaging solutions among pet owners. Stand-up pouches allow easy storage, resealability, and improved shelf visibility in retail environments. These features will continue to support the adoption of stand-up pouches across premium pet food brands.

By Material

Plastic packaging dominated the pet food packaging market in 2025 with a share of 52.9%. Plastic materials such as polyethylene and polypropylene were widely used due to their flexibility, lightweight characteristics, and strong barrier performance. These materials were particularly suitable for flexible packaging formats, which remain the preferred choice for dry pet food products.

The paper and paperboard segment is projected to grow at the fastest rate with a CAGR of 6.8% during the forecast period. This growth will be driven by increasing demand for sustainable packaging alternatives. Paper-based packaging solutions offer recyclability and reduced environmental impact compared with conventional plastic materials. Packaging manufacturers will continue investing in improved paper-based barrier technologies to enhance durability and moisture resistance.

By Food Type

The dry pet food segment held the largest share of the pet food packaging market in 2025, accounting for 61.3% of total demand. Dry pet food products are widely consumed due to their convenience, long shelf life, and affordability. These products typically require large-format packaging such as multi-layer bags or pouches that can preserve freshness over extended periods.

The wet pet food segment is expected to grow at a CAGR of 6.5% during the forecast period. Wet pet food products require specialized packaging solutions such as cans, trays, and retort pouches that can maintain product sterility and prevent contamination. Increasing consumer interest in premium wet food formulations will contribute to higher demand for advanced packaging solutions.

Pet Food Packaging Market Segmentations

Packaging Type

- Bags & Pouches

- Folding Cartons

- Metal Cans

- Plastic Containers

- Others

Material

- Plastic

- Paper & Paperboard

- Metal

- Others

Food Type

- Dry Pet Food

- Wet Pet Food

- Semi-Moist Pet Food

Regional Analysis

North America

North America held 38.2% of the pet food packaging market share in 2025, reflecting strong demand for packaged pet food products and advanced packaging technologies. The region will likely register a CAGR of 5.4% from 2025 to 2034 as pet food manufacturers continue to adopt flexible packaging solutions and sustainable materials. The presence of major pet food brands and packaging suppliers has created a well-developed industry ecosystem. Retail expansion and the growing popularity of specialty pet food products are expected to sustain regional demand for packaging innovations.

The United States dominated the regional market due to its large pet population and strong consumer spending on pet care products. Pet food brands in the country increasingly focus on packaging formats that emphasize convenience, portion control, and sustainability. Resealable pouches, recyclable packaging materials, and premium packaging designs are gaining adoption among manufacturers. These factors are expected to maintain the country’s leading position within the North American pet food packaging market.

Europe

Europe represented 27.4% of the pet food packaging market share in 2025. The region is expected to grow at a CAGR of 5.7% during the forecast period due to increasing emphasis on sustainable packaging solutions and regulatory initiatives aimed at reducing packaging waste. European packaging manufacturers are actively developing recyclable and biodegradable packaging materials to meet environmental targets. This transition toward eco-friendly solutions continues to shape market developments across the region.

Germany remained the dominant country in the European market due to its strong packaging manufacturing industry and high demand for premium pet food products. Pet food producers in Germany emphasize packaging innovations that combine product protection with environmentally responsible materials. The country's focus on sustainable packaging technologies is expected to support the continued development of the pet food packaging market in Europe.

Asia Pacific

Asia Pacific accounted for 21.6% of the pet food packaging market share in 2025 and is expected to record the fastest CAGR of 7.4% through 2034. Rapid urbanization, rising disposable incomes, and changing consumer lifestyles are contributing to increasing pet ownership across the region. As demand for commercial pet food grows, manufacturers are expanding packaging production capacities to support the evolving market landscape.

China dominated the regional market due to its rapidly expanding pet care industry and increasing demand for packaged pet food products. Consumers in the country are increasingly adopting companion animals, which has boosted the availability of commercial pet food brands. Packaging manufacturers are focusing on lightweight flexible packaging solutions to improve distribution efficiency and reduce transportation costs. These factors are expected to strengthen China’s position within the Asia Pacific pet food packaging market.

Middle East & Africa

The Middle East & Africa accounted for 6.1% of the pet food packaging market share in 2025 and is projected to grow at a CAGR of 6.0% between 2025 and 2034. Growth in this region is driven by expanding retail infrastructure and rising awareness of commercial pet food products. Packaging suppliers are introducing affordable and durable packaging formats suited to regional supply chain conditions.

The United Arab Emirates emerged as the leading country within the regional market due to its rapidly growing pet care sector and increasing availability of premium pet food brands. Retail expansion and rising consumer spending on pet products are encouraging manufacturers to introduce advanced packaging solutions. This trend is expected to support continued growth within the regional pet food packaging market.

Latin America

Latin America held 6.7% of the pet food packaging market share in 2025 and will likely expand at a CAGR of 6.3% through 2034. The region’s pet care industry has experienced steady growth as pet ownership becomes more common across urban households. The demand for packaged pet food products is increasing, prompting packaging manufacturers to expand production capabilities.

Brazil dominated the regional market due to its large pet population and growing pet food industry. Pet food producers in the country are adopting flexible packaging formats to improve logistics and reduce packaging costs. The increasing availability of commercial pet food brands is expected to drive demand for packaging solutions across Brazil and the broader Latin American pet food packaging market.

Competitive Landscape

The pet food packaging market features a moderately consolidated competitive landscape with global packaging companies competing through product innovation, material advancements, and strategic partnerships with pet food manufacturers.

Amcor plc is considered a leading company in the market due to its extensive portfolio of flexible and sustainable packaging solutions. The company continues to develop recyclable and high-barrier packaging formats designed specifically for pet food products. Recently, Amcor introduced recyclable flexible packaging solutions that support circular economy goals for consumer packaged goods.

Other notable companies focus on expanding manufacturing capacity and improving packaging technologies to meet evolving consumer preferences and regulatory requirements. Industry participants also emphasize sustainability initiatives, lightweight packaging structures, and improved barrier performance to maintain competitiveness.

Strategic collaborations between packaging suppliers and pet food brands are expected to remain an important strategy as companies seek to enhance packaging functionality and reduce environmental impact.

Key Players List

- Amcor plc

- Mondi Group

- Sonoco Products Company

- Berry Global Inc.

- Sealed Air Corporation

- Huhtamaki Oyj

- Coveris Holdings S.A.

- ProAmpac LLC

- Winpak Ltd.

- Smurfit Kappa Group

- Crown Holdings Inc.

- Constantia Flexibles

- Clondalkin Group

- AptarGroup Inc.

- Silgan Holdings Inc.