Pctfe Pharmaceutical Packaging Films Market Size and Growth

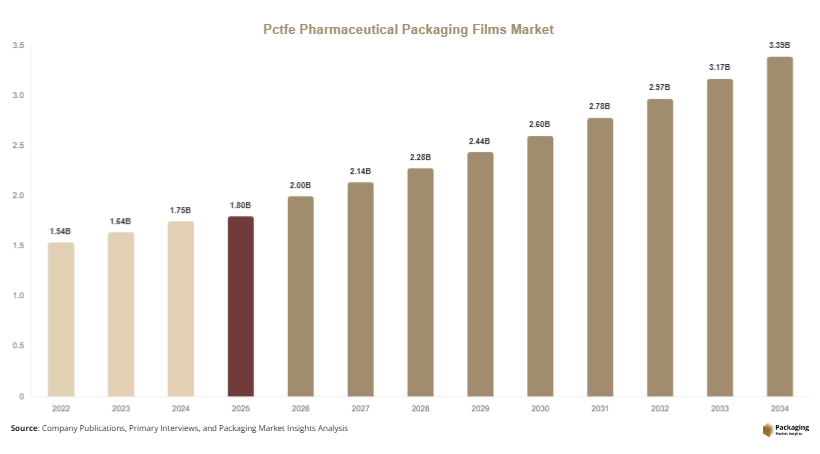

The global pctfe pharmaceutical packaging films market size was valued at USD 1.8 billion in 2025 and is projected to reach USD 2.0 billion in 2026. With increasing demand for advanced pharmaceutical packaging, the market is forecasted to reach USD 3.6 billion by 2034, expanding at a CAGR of 6.8% during the forecast period (2025–2034). The pctfe pharmaceutical packaging films market is experiencing steady growth as pharmaceutical manufacturers prioritize high-barrier packaging solutions to ensure product stability, safety, and extended shelf life. Polychlorotrifluoroethylene (PCTFE) films are widely used in blister packaging due to their exceptional moisture barrier properties, making them suitable for sensitive drugs and formulations.

Growth in the pctfe pharmaceutical packaging films market is driven by multiple factors. The rising global pharmaceutical industry, supported by increasing healthcare expenditure and drug consumption, is a primary contributor. Additionally, the growing demand for moisture-sensitive drugs, including biologics and specialty medicines, is accelerating the adoption of high-performance packaging materials. Another significant growth factor is the increasing regulatory focus on drug safety and compliance, which requires robust packaging solutions that maintain product integrity throughout the supply chain.

Key Highlights:

Asia Pacific dominated the market with a 39.1% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.2%.

High-barrier PCTFE films led the type segment with a 54.7% share, while ultra-high barrier films are expected to grow at a CAGR of 7.5%.

Blister packaging dominated with a 63.8% share, while strip packaging is forecasted to grow at a CAGR of 6.9%.

Pharmaceutical applications led the segment with 91.2% share, while nutraceutical packaging is expected to grow at a CAGR of 7.1%.

China remained the dominant country with a market size of USD 0.5 billion in 2025 and USD 0.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing adoption of high-barrier multi-layer film structures

The pctfe pharmaceutical packaging films market is witnessing a growing shift toward multi-layer film structures that combine PCTFE with other materials such as PVC and polyethylene. These structures offer enhanced barrier properties, improved mechanical strength, and cost optimization. Pharmaceutical companies are increasingly adopting these films to protect moisture-sensitive drugs and ensure product stability throughout the distribution cycle. The use of co-extrusion and lamination technologies is enabling manufacturers to develop customized film solutions tailored to specific drug requirements. This trend is expected to continue as demand for advanced packaging solutions rises.

Rising focus on sustainability and material optimization

Sustainability is becoming an important consideration in the pharmaceutical packaging industry. Manufacturers are focusing on reducing material usage and developing thinner film structures without compromising performance. Efforts are also being made to improve recyclability and reduce environmental impact. Innovations in material science are enabling the development of eco-friendly alternatives to traditional packaging materials. This trend is driven by regulatory pressures and increasing awareness among stakeholders about environmental sustainability.

Market Drivers

Growth in pharmaceutical manufacturing and drug consumption

The expansion of the global pharmaceutical industry is a key driver of the pctfe pharmaceutical packaging films market. Increasing demand for medications, driven by aging populations and rising prevalence of chronic diseases, is fueling the need for reliable packaging solutions. PCTFE films are widely used in blister packaging due to their superior moisture barrier properties, which are essential for maintaining drug efficacy. The growth of generic drug production and the expansion of pharmaceutical manufacturing facilities in emerging markets are further contributing to market growth.

Stringent regulatory requirements for drug safety

Regulatory requirements for pharmaceutical packaging are becoming increasingly stringent, emphasizing the need for high-quality materials that ensure product safety and compliance. PCTFE films meet these requirements by providing excellent protection against moisture and environmental factors. Pharmaceutical companies are investing in advanced packaging solutions to comply with regulations and maintain product integrity. This driver is expected to continue influencing market growth as regulatory standards evolve.

Market Restraint

High cost of PCTFE films compared to alternative materials

One of the major restraints in the pctfe pharmaceutical packaging films market is the high cost of PCTFE films compared to alternative packaging materials such as PVC. The production of PCTFE involves complex processes and specialized raw materials, which increase overall costs. This can limit adoption, particularly among small and medium-sized pharmaceutical manufacturers. For example, cost-sensitive markets may opt for lower-cost packaging solutions, even if they offer lower barrier performance. Additionally, fluctuations in raw material prices can impact profitability and create challenges for manufacturers. These factors can restrain market growth to some extent.

Market Opportunities

Expansion of biologics and specialty drug markets

The growing demand for biologics and specialty drugs presents significant opportunities for the pctfe pharmaceutical packaging films market. These drugs are often highly sensitive to moisture and require advanced packaging solutions to maintain stability. PCTFE films provide the necessary barrier properties, making them suitable for such applications. The increasing focus on personalized medicine and advanced therapies is expected to drive demand for high-performance packaging materials.

Development of cost-effective and recyclable film solutions

Another opportunity lies in the development of cost-effective and recyclable PCTFE film solutions. Manufacturers are investing in research and development to reduce material costs and improve sustainability. Innovations in film extrusion and coating technologies are enabling the production of thinner films with enhanced performance. These advancements can help expand market adoption and create new growth opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 1.8 Billion |

| Market Size in 2026 | USD 2.0 Billion |

| Market Size in 2034 | USD 3.6 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

High-barrier PCTFE films dominated the market with a 54.7% share in 2024. These films are widely used in pharmaceutical packaging due to their superior moisture barrier properties. They are essential for protecting sensitive drugs and ensuring product stability. Manufacturers are continuously improving film quality to meet industry requirements.

Ultra-high barrier films are expected to grow at the fastest CAGR of 7.5%. These films offer enhanced protection and are used for highly sensitive drugs. Increasing demand for advanced therapies is driving growth in this segment.

By Packaging Type

Blister packaging accounted for the largest share of 63.8% in 2024. It is widely used for pharmaceutical products due to its convenience and protection. PCTFE films are commonly used in blister packs to provide moisture resistance.

Strip packaging is projected to grow at a CAGR of 6.9%. It offers cost advantages and is suitable for certain applications. Increasing demand for cost-effective packaging solutions is supporting growth.

By Application

Pharmaceutical applications dominated the market with a share of 91.2% in 2024. PCTFE films are widely used for packaging tablets and capsules. The growth of the pharmaceutical industry is driving demand.

Nutraceutical packaging is expected to grow at a CAGR of 7.1%. Increasing consumer awareness about health and wellness is driving demand for nutraceutical products, supporting segment growth.

Pctfe Pharmaceutical Packaging Films Market Segmentations

By Type

- High-Barrier PCTFE Films

- Ultra-High Barrier PCTFE Films

- Standard PCTFE Films

By Packaging Type

- Blister Packaging

- Strip Packaging

- Sachet Packaging

By Application

- Pharmaceutical

- Nutraceutical

- Medical Devices

Regional Analysis

North America

North America accounted for approximately 24.5% of the pctfe pharmaceutical packaging films market share in 2025 and is projected to grow at a CAGR of 6.2%. The region benefits from a well-established pharmaceutical industry and strong regulatory framework. High demand for advanced packaging solutions is supporting market growth.

The United States dominates the regional market due to its large pharmaceutical manufacturing base. A key growth factor is the increasing adoption of high-barrier packaging for specialty drugs, which require enhanced protection against environmental factors.

Europe

Europe held a market share of around 22.7% in 2025 and is expected to grow at a CAGR of 6.0%. The region’s growth is driven by stringent regulatory requirements and strong focus on product safety. Pharmaceutical companies are investing in advanced packaging technologies.

Germany is the leading country in the European market. A major growth factor is the presence of a strong pharmaceutical industry and emphasis on high-quality packaging solutions.

Asia Pacific

Asia Pacific dominated the market with a 39.1% share in 2025 and is projected to grow at a CAGR of 7.1%. Rapid growth in pharmaceutical manufacturing and increasing healthcare expenditure are driving market expansion. The region is becoming a hub for generic drug production.

China is the dominant country in the region due to its large manufacturing capacity. A unique growth factor is the expansion of pharmaceutical exports, which requires high-quality packaging solutions.

Middle East & Africa

The Middle East & Africa region accounted for approximately 6.3% of the market share in 2025 and is expected to grow at a CAGR of 6.4%. The market is gradually expanding due to improving healthcare infrastructure and increasing demand for pharmaceuticals.

Saudi Arabia is a key contributor to regional growth. A significant growth factor is government investment in healthcare and pharmaceutical manufacturing.

Latin America

Latin America held a market share of around 7.4% in 2025 and is projected to grow at the fastest CAGR of 7.2%. Increasing demand for pharmaceuticals and improving distribution networks are driving market growth.

Brazil dominates the regional market due to its large population and growing healthcare sector. A unique growth factor is the increasing adoption of advanced packaging technologies.

Competitive Landscape

The pctfe pharmaceutical packaging films market is characterized by the presence of several key players focusing on innovation and product development. Companies are investing in advanced technologies to enhance film performance and reduce costs. Strategic collaborations and expansions are common strategies used to strengthen market position.

Honeywell International Inc. is a leading player in the market and has recently introduced advanced PCTFE films with improved barrier properties. Other companies are also focusing on expanding their product portfolios and improving manufacturing capabilities to remain competitive.

Key Players List

- Honeywell International Inc.

- Arkema S.A.

- Daikin Industries Ltd.

- Solvay S.A.

- Kureha Corporation

- Bilcare Limited

- Tekni-Plex, Inc.

- Liveo Research AG

- Perlen Packaging AG

- Amcor plc

- UFlex Limited

- Jiangsu Shuangxing Color Plastic New Materials Co., Ltd.

- Shanghai Haishun New Pharmaceutical Packaging Material Co., Ltd.

- Winpak Ltd.

- Constantia Flexibles Group GmbH