Panel Level Packaging Market Size and Growth

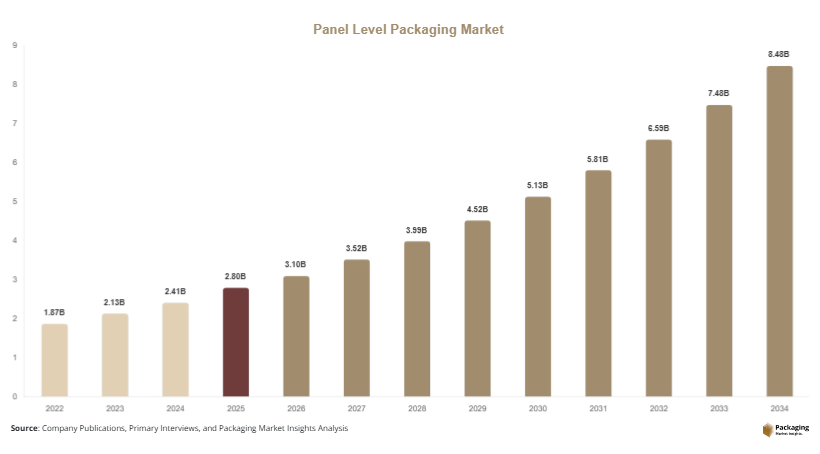

The global panel level packaging market size is estimated at USD 2.8 billion in 2025, and it is projected to reach USD 3.1 billion in 2026. By 2034, the market is expected to attain USD 8.6 billion, expanding at a CAGR of 13.4% (2025–2034). Growth is supported by increasing semiconductor complexity, rising demand for advanced packaging in AI chips, and expansion of heterogeneous integration technologies.

Key growth factors include the shift toward system-in-package (SiP) architectures, increasing adoption of fan-out packaging for mobile processors, and the rising need for energy-efficient chip designs in data centers and edge computing. Additionally, semiconductor manufacturers are investing heavily in panel-based fabrication lines to improve throughput and reduce manufacturing waste.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Antioxidants led the type segment with a 29.6% share.

- Plastic packaging dominated with a 52.3% share.

- Food & beverage applications led the segment with 43.1% share.

- The US remained the dominant country with a market size of USD 3.2 billion in 2025 and USD 3.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Transition from Wafer-Level to Panel-Level Advanced Packaging

A major trend in the panel level packaging market is the transition from traditional wafer-level packaging to panel-level fan-out technologies. Manufacturers are adopting larger rectangular substrates, which allow higher throughput and better material utilization compared to circular wafers. This shift is particularly visible in consumer electronics, where smartphones and tablets require compact and high-performance chip designs. Companies such as OSAT providers are investing in panel processing equipment to scale production efficiency. For example, fan-out panel level packaging is increasingly used in mobile application processors and RF modules. This trend is expected to reshape semiconductor backend manufacturing, reducing cost per die while enabling more complex multi-chip integration in a single package.

Integration of Heterogeneous Systems in Advanced Computing

Another key trend is the growing integration of heterogeneous systems using panel level packaging architectures. This includes combining logic chips, memory units, and power management components into a single module. The demand is driven by artificial intelligence workloads, cloud computing, and automotive electronics. For instance, AI accelerators used in data centers require high bandwidth and low latency interconnects, which PLP enables efficiently. Automotive systems such as ADAS also rely on compact and thermally efficient packaging solutions. In the future, PLP is expected to play a central role in chiplet-based architectures, enabling modular semiconductor design and accelerating innovation in high-performance computing ecosystems.

Market Drivers

Rising Demand for Miniaturized and High-Performance Electronics

The increasing demand for compact and high-performance electronic devices is a primary driver of the panel level packaging market. Consumer electronics such as smartphones, wearables, and IoT devices require smaller chip footprints without compromising performance. PLP enables higher interconnect density and reduced form factor, making it suitable for next-generation devices. For example, smartphone manufacturers are integrating multiple sensors and processors into single modules using fan-out PLP technology. This improves device efficiency while reducing production complexity. As consumer electronics continue to evolve toward thinner and more powerful devices, PLP adoption is expected to accelerate across semiconductor manufacturing ecosystems.

Expansion of Automotive Electronics and ADAS Systems

The growing integration of electronics in vehicles is another significant driver. Advanced Driver Assistance Systems (ADAS), electric vehicles, and autonomous driving technologies require highly reliable and thermally stable semiconductor packaging. Panel level packaging provides improved electrical performance and heat dissipation, making it suitable for automotive-grade applications. For instance, automotive radar and sensor modules increasingly use PLP for compact integration. As EV production expands globally, semiconductor content per vehicle is rising, driving demand for advanced packaging solutions. This trend is expected to strengthen PLP adoption in automotive supply chains over the forecast period.

Market Restraint

High Manufacturing Complexity and Equipment Costs

A key restraint in the panel level packaging market is the high complexity of manufacturing processes and the significant capital investment required for equipment. Unlike wafer-level packaging, PLP requires precise alignment on large rectangular panels, which introduces technical challenges in yield control and process stability. Equipment for lithography, molding, and inspection at panel scale is expensive and not widely standardized. For example, semiconductor foundries transitioning to PLP must upgrade entire backend production lines, increasing operational costs. Additionally, yield optimization remains challenging due to warpage and material stress issues. These factors limit adoption among smaller manufacturers and slow down large-scale commercialization in certain regions.

Market Opportunities

Growth of Chiplet-Based Architecture

The rising adoption of chiplet-based architecture presents a major opportunity for the panel level packaging market. Chiplets allow multiple smaller semiconductor dies to be integrated into a single system, improving performance and flexibility. PLP is well-suited for chiplet integration due to its high interconnect density and scalability. For example, data center processors increasingly rely on modular chiplet designs to enhance computing power while reducing cost. Semiconductor companies are investing in advanced packaging platforms that support heterogeneous integration using PLP. This trend is expected to significantly expand the application scope of panel level packaging in high-performance computing and AI-driven systems.

Expansion in 5G and Edge Computing Infrastructure

The rapid expansion of 5G networks and edge computing infrastructure creates strong growth opportunities. These technologies require compact, energy-efficient, and high-speed semiconductor modules, which PLP can deliver. For instance, 5G base stations use advanced RF modules that benefit from fan-out panel packaging for improved signal integrity. Similarly, edge computing devices require low-latency processing capabilities in compact form factors. As global 5G penetration increases, semiconductor manufacturers are expected to scale PLP adoption to meet performance and cost requirements. This will drive long-term expansion in telecom and networking applications.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 2.8 Billion |

| Market Size in 2026 | USD 3.1 Billion |

| Market Size in 2034 | USD 8.6 Billion |

| CAGR | 13.4% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Fan-out panel level packaging dominated the market with a 2024 share of 48.2%, driven by its ability to deliver high-density interconnects and cost-efficient production. It is widely used in mobile processors and RF modules, especially in smartphones and wearable devices. For example, leading semiconductor companies use fan-out PLP to integrate multiple functional chips into compact modules for consumer electronics.

Fan-in panel level packaging is the fastest-growing subsegment with a CAGR of 14.1%, driven by increasing demand for compact chip integration in IoT and automotive applications. Its adoption is rising due to improved thermal performance and reduced signal latency. Future growth will be supported by advanced 5G and edge computing deployments.

By Material

Organic substrates dominated with a 2024 share of 52.6%, due to their flexibility, cost efficiency, and compatibility with large-panel processing. They are widely used in consumer electronics and computing applications. For example, organic interposers are commonly used in mobile SoC integration.

Glass substrates are the fastest-growing segment with a CAGR of 15.3%, driven by superior dimensional stability and electrical performance. They are increasingly used in high-performance computing and AI chips. Future adoption will expand in data centers and advanced semiconductor nodes.

By End-Use

Consumer electronics led the segment with a 2024 share of 44.8%, driven by smartphones, tablets, and wearable devices. PLP enables compact integration and improved device performance.

Automotive electronics is the fastest-growing segment with a CAGR of 14.6%, driven by EV adoption and ADAS systems. Growth is supported by demand for reliable and thermally efficient semiconductor packaging.

Panel Level Packaging Market Segmentations

By Type

- Fan-Out Panel Level Packaging

- Fan-In Panel Level Packaging

- 2.5D Panel Level Integration

- 3D Panel Level Packaging

By Material

- Organic Substrates

- Glass Substrates

- Silicon Interposers

- Polyimide Materials

- Advanced Composite Materials

By End-Use

- Consumer Electronics

- Automotive Electronics

- Data Centers & Cloud Computing

- Telecommunications

- Industrial & IoT Devices

By Distribution Channel

- Direct Semiconductor Manufacturers

- OSAT Providers

- Contract Manufacturing Partners

- Technology Licensing Partnerships

- Foundry Ecosystem Sales

Regional Analysis

North America

North America accounted for 27.5% of the panel level packaging market in 2025, with a projected CAGR of 12.8% through 2034. The region benefits from strong semiconductor R&D infrastructure and high adoption of advanced computing technologies. Demand is primarily driven by AI, cloud computing, and data center expansion. Companies in the United States are investing heavily in next-generation packaging technologies to support high-performance processors and GPUs.

The United States dominates the region due to its leadership in semiconductor design and hyperscale data centers. A key growth driver is the increasing deployment of AI accelerators requiring advanced heterogeneous integration. For example, leading cloud service providers are adopting PLP-based solutions for improved processing efficiency and thermal management in server farms.

Europe

Europe held a 21.3% share in 2025, with a forecast CAGR of 12.1% through 2034. The region is driven by automotive electronics, industrial automation, and semiconductor innovation programs supported by government funding. Countries such as Germany and France are investing in advanced packaging research to strengthen semiconductor independence.

Germany leads the regional market due to its strong automotive sector. A unique driver is the integration of PLP in electric vehicle control systems and ADAS modules. For example, German automotive suppliers are using advanced packaging to improve sensor accuracy and reduce system size in EV platforms.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025, growing at a CAGR of 14.2% through 2034. The region is supported by strong semiconductor manufacturing bases in China, Taiwan, South Korea, and Japan. High-volume electronics production and government-backed semiconductor initiatives are key growth drivers.

China is the dominant country due to its massive electronics manufacturing ecosystem. A major driver is the expansion of domestic semiconductor packaging capacity to reduce import dependency. For example, Chinese OSAT companies are scaling panel level packaging lines to support smartphone and AI chip production.

Middle East & Africa

The Middle East & Africa accounted for 6.2% of the market in 2025, with a CAGR of 11.5% through 2034. Growth is driven by digital transformation initiatives, telecom expansion, and emerging data center investments. Countries like the UAE and Israel are investing in semiconductor-related technologies.

Israel leads the region due to its strong semiconductor R&D ecosystem. A key driver is the development of advanced chip design and packaging solutions for defense and communication systems. For example, Israeli tech firms are integrating PLP in compact radar and surveillance systems.

Latin America

Latin America held a 7.6% share in 2025, with the fastest CAGR of 14.5% through 2034. Growth is supported by expanding electronics assembly operations and increasing telecom infrastructure investments in Brazil and Mexico.

Brazil dominates the region due to its growing electronics manufacturing sector. A key driver is the rising demand for consumer electronics assembly and import substitution strategies. For example, Brazilian electronics firms are gradually adopting advanced packaging technologies to improve local semiconductor value chains.

Competitive Landscape

The panel level packaging market is moderately consolidated with major players focusing on capacity expansion and technology innovation. Key companies include TSMC, Samsung Electronics, Intel Corporation, ASE Group, and Amkor Technology. Among these, TSMC leads due to its strong investment in advanced packaging platforms and high-volume manufacturing capabilities.

Companies are focusing on scaling panel-level production lines, improving yield efficiency, and integrating heterogeneous packaging solutions. Recent developments include expansion of OSAT facilities in Asia and increased R&D investment in glass-based packaging technologies.

Key Players List

- TSMC

- Samsung Electronics

- Intel Corporation

- ASE Group

- Amkor Technology

- JCET Group

- Powertech Technology Inc.

- Tongfu Microelectronics

- Nepes Corporation

- Deca Technologies

- Nepes

- SPIL (Siliconware Precision Industries)

- Unimicron Technology

- Infineon Technologies

- STMicroelectronics