Pallet Boxes Market Size and Growth

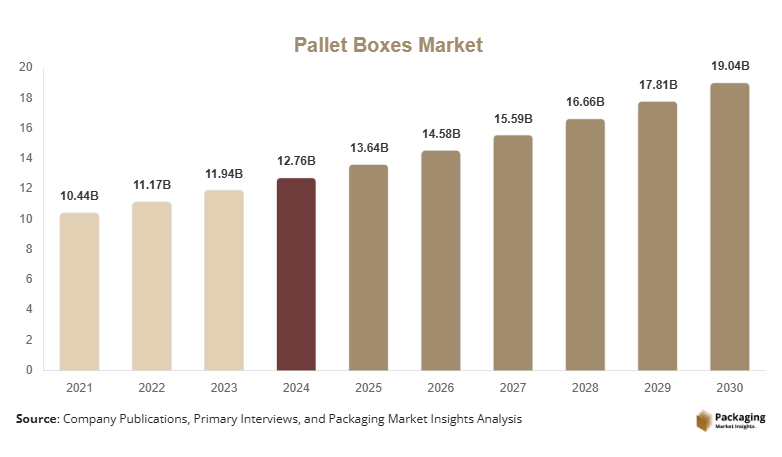

The global pallet boxes market size was valued at USD 12.76 billion in 2024 and is projected to grow from USD 13.64 billion in 2025 to reach USD 19.04 billion by 2030, expanding at a CAGR of 6.9% during the forecast period (2025–2030).

The pallet boxes market growth is primarily driven by rising demand for reusable and sustainable bulk packaging solutions, increasing global trade volumes, and rapid expansion of industrial manufacturing, food processing, and export-oriented logistics worldwide.

Key Highlights

- Plastic pallet boxes dominate the global market, supported by superior durability, hygiene compliance, recyclability, and long service life across food, pharmaceutical, and industrial applications.

- Collapsible and foldable pallet boxes are gaining strong traction, as manufacturers and logistics operators seek to reduce return transportation costs and improve warehouse space efficiency.

- Asia-Pacific leads global demand, driven by export-focused manufacturing hubs in China, India, Japan, and Southeast Asia.

- Food and beverage remains the largest end-use segment, supported by growth in cold-chain infrastructure, processed food exports, and stringent food safety regulations.

- Automation-friendly pallet boxes, compatible with robotic handling and warehouse management systems, are increasingly preferred by large manufacturing and distribution facilities.

- Sustainability initiatives and circular economy regulations are accelerating the shift from single-use packaging toward reusable pallet box systems.

Explore more data points, trends and opportunities Download Free Sample Report

Latest Market Trends

Shift Toward Reusable and Sustainable Transport Packaging

The pallet boxes market is witnessing a strong shift toward reusable transport packaging as companies focus on lowering long-term logistics costs and meeting sustainability targets. Plastic and composite pallet boxes are increasingly replacing corrugated bulk containers due to their longer lifecycle and reduced environmental footprint. Many manufacturers are introducing pallet boxes made from recycled polymers and offering closed-loop recycling programs to support circular economy goals. Regulatory pressure in Europe and North America is further reinforcing this trend, encouraging adoption across food, pharmaceutical, and chemical supply chains.

The pallet boxes market is also benefiting from rising automation in warehousing and logistics. Pallet boxes designed for compatibility with automated storage and retrieval systems (ASRS), robotic forklifts, and conveyor systems are seeing higher adoption, particularly in large-scale manufacturing plants and e-commerce fulfillment centers. Integration of RFID tags and tracking features is emerging as a value-added differentiator, improving inventory visibility and loss prevention.

Market Drivers

Growth in Global Manufacturing and Industrial Output

The expansion of automotive, electronics, and industrial manufacturing has significantly increased the need for heavy-duty bulk packaging. Pallet boxes offer high load-bearing capacity and protection, making them essential in modern production and distribution systems.

Shift Toward Reusable Transport Packaging

Rising logistics costs and sustainability goals are pushing companies to replace single-use packaging with reusable pallet boxes. Over their lifecycle, pallet boxes reduce per-trip costs by up to 40%, making them economically attractive.

Market Restraint

High Initial Capital Cost

Compared to corrugated packaging, pallet boxes require a higher upfront investment, which can deter small-scale users or price-sensitive markets.

Market Opportunities

Expansion of Sustainable & Reusable Packaging Mandates

Governments and regulatory bodies across Europe, North America, and parts of Asia are increasingly promoting reusable transport packaging (RTP) to reduce waste generation. Pallet boxes, particularly plastic and composite variants, align strongly with circular economy objectives. Manufacturers that invest in closed-loop recycling systems, bio-based polymers, and extended-life pallet boxes can capitalize on regulatory incentives and growing customer preference for sustainable packaging solutions.

Rising Demand from Export-Oriented Industries

Export-driven sectors such as automotive components, pharmaceuticals, processed food, and chemicals require robust, standardized, and hygienic bulk packaging solutions. Pallet boxes offer superior protection during long-distance transport and multi-modal logistics. Rapid export growth from countries such as China, India, Vietnam, Mexico, and Poland presents a strong opportunity for localized production and regional customization of pallet box designs.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2024 | USD 12.76 Billion |

| Market Size in 2025 | USD 13.64 Billion |

| Market Size in 2030 | USD 19.04 Billion |

| CAGR | 6.9% (2025-2030) |

| Base Year for Estimation | 2024 |

| Historical Data | 2021-2023 |

| Forecast Period | 2025-2030 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

The plastic pallet boxes subsegment, including HDPE and PP variants, accounted for a dominant 52% share of the global pallet boxes market in 2024. This leadership is primarily attributed to their superior durability, hygiene compliance, resistance to moisture and chemicals, and long operational lifespan. Plastic pallet boxes are extensively used across food & beverage, pharmaceutical, and chemical industries, where cleanliness, reusability, and regulatory compliance are critical. Their compatibility with automated handling systems and recyclability further strengthens their market position.

The composite pallet boxes subsegment is projected to witness the fastest growth, registering a CAGR of approximately 9.2% during 2025–2030. This growth is driven by rising demand for lightweight yet high-strength bulk packaging solutions that combine multiple materials to enhance load-bearing capacity, sustainability, and cost efficiency, particularly in export-oriented industrial applications.

By Product Design

The collapsible and foldable pallet boxes subsegment held the largest share, accounting for 38% of the global market in 2024. This dominance is largely due to their ability to significantly reduce reverse logistics costs and warehouse space requirements when empty. Collapsible pallet boxes are widely adopted by automotive, retail, and export-focused manufacturers seeking to optimize supply chain efficiency and minimize transportation expenses.

The custom-engineered pallet boxes subsegment is expected to grow at the fastest pace, with a projected CAGR of 9.5% from 2025 to 2030. This growth is fueled by increasing demand for application-specific designs tailored to unique product dimensions, weight requirements, and industry regulations, particularly in pharmaceuticals, electronics, and high-value industrial components.

By Load Capacity

The 500–1,000 kg load capacity subsegment dominated the market by load capacity, capturing approximately 41% of the global pallet boxes market in 2024. This segment’s leadership stems from its versatility, as it caters to a broad range of industries including food processing, chemicals, automotive parts, and agriculture. Pallet boxes in this range offer an optimal balance between load-bearing strength, handling efficiency, and cost-effectiveness.

The above 1,500 kg load capacity subsegment is anticipated to record the fastest growth, expanding at a CAGR of 8.8% during the forecast period. Rising demand from heavy industrial manufacturing, metal components, and large-scale automotive parts transportation is driving adoption of high-capacity pallet boxes globally.

By End-Use Industry

The food and beverage subsegment accounted for the largest share, representing approximately 29% of the global pallet boxes market in 2024. This strong position is supported by expanding cold-chain infrastructure, rising processed food exports, and stringent food safety regulations that necessitate hygienic and reusable bulk packaging solutions. Plastic pallet boxes, in particular, are widely used for fresh produce, meat, dairy, and frozen foods.

The pharmaceuticals and healthcare subsegment is projected to be the fastest-growing, registering a CAGR of 9.6% from 2025 to 2030. Growth is driven by increasing pharmaceutical production, rising global healthcare demand, and strict regulatory standards requiring contamination-free, durable, and traceable packaging solutions for medical products.

By Distribution Channel

The direct sales (OEM and industrial contracts) subsegment dominated the market, accounting for nearly 57% of total revenue in 2024. This dominance is attributed to large-volume procurement by manufacturers, logistics companies, and food processors that prefer long-term supply agreements, customized pallet box designs, and cost efficiencies associated with bulk purchasing.

The online and B2B e-commerce platforms subsegment is expected to experience the fastest growth, with a projected CAGR of 10.1% during 2025–2030. Increasing digitalization of industrial procurement, ease of product comparison, and expanding access to standardized pallet box solutions are driving rapid adoption of online purchasing channels, particularly among small and mid-sized enterprises.

Pallet Boxes Market Segmentations

By Material Type

- Plastic Pallet Boxes (HDPE, PP)

- Wooden Pallet Boxes

- Metal Pallet Boxes

- Corrugated/Fiberboard Pallet Boxes

- Composite Pallet Boxes

By Product Design

- Solid Wall Pallet Boxes

- Vented Pallet Boxes

- Collapsible/Foldable Pallet Boxes

- Stackable Pallet Boxes

- Custom-Engineered Pallet Boxes

By Load Capacity

- Below 500 kg

- 500–1,000 kg

- 1,000–1,500 kg

- Above 1,500 kg

By End-Use Industry

- Food & Beverage

- Pharmaceuticals & Healthcare

- Automotive & Industrial Manufacturing

- Chemicals

- Agriculture & Horticulture

- Retail & E-commerce

- Electronics & Electricals

By Distribution Channel

- Direct Sales (OEM & Industrial Contracts)

- Distributors & Packaging Suppliers

- Online/B2B E-commerce Platforms

Regional Analysis

North America

North America remains a key demand region for pallet boxes, driven primarily by the United States and Canada. Strong industrial output, advanced warehouse automation, and widespread adoption of reusable packaging systems support market growth. The region shows high demand from food processing, pharmaceuticals, and automotive manufacturing. Export-oriented logistics and stringent hygiene standards further strengthen the use of plastic pallet boxes. North America accounts for approximately 22% of the global pallet boxes market in 2024, with steady growth supported by continued investment in smart logistics infrastructure.

Europe

Europe represents one of the most mature and sustainability-driven markets for pallet boxes, led by Germany, France, the U.K., Italy, and Poland. Strong regulatory frameworks promoting reusable packaging and waste reduction are accelerating pallet box adoption. European manufacturers emphasize collapsible and lightweight designs to optimize cross-border logistics. The region holds an estimated 27% share of the global market in 2024, with demand particularly strong in automotive components, chemicals, and food exports. Eastern Europe, especially Poland and the Czech Republic, is emerging as a fast-growing sub-region due to manufacturing expansion.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing regional market, accounting for approximately 38% of global pallet box demand in 2024. China dominates regional consumption due to its massive manufacturing base and export volumes. India is the fastest-growing country, supported by government-led manufacturing initiatives, expanding cold-chain infrastructure, and rising food and pharmaceutical exports. Japan and South Korea contribute steady demand driven by advanced automation and quality standards. Rapid industrialization and export growth across Southeast Asia are further accelerating pallet box adoption.

Latin America

The pallet boxes market in Latin America is expanding gradually, led by Brazil, Mexico, and Argentina. Growth is supported by increasing agricultural exports, automotive manufacturing, and food processing industries. While adoption remains lower than in developed regions, rising investment in export logistics and cold-chain facilities is creating new opportunities. Latin America represents roughly 8% of global market demand, with growing interest in durable and reusable bulk packaging solutions.

Middle East & Africa

The Middle East & Africa region holds approximately 5% of the global pallet boxes market, with demand concentrated in the UAE, Saudi Arabia, South Africa, and Egypt. Growth is driven by expanding food imports, chemical processing, and logistics hubs serving international trade routes. Africa’s agricultural exports and intra-regional trade are supporting increased use of pallet boxes, particularly in horticulture and fresh produce logistics. Government-backed infrastructure investments and port expansions are expected to drive steady growth across the region.

Competitive Landscape

The pallet boxes market is moderately consolidated, with leading manufacturers benefiting from global manufacturing footprints, standardized product portfolios, and long-term industrial contracts. The top five players collectively account for approximately 42% of global market share, reflecting strong competitive positioning in plastic and reusable pallet box solutions. Competition remains intense, with pricing influenced by raw material costs, customization requirements, and lifecycle service offerings. Companies investing in automation compatibility, sustainability, and value-added logistics services have shown stronger performance over recent years.

Key Players in the Pallet Boxes Market

- Schoeller Allibert

- CABKA Group

- Orbis Corporation

- Craemer Group

- Tosca Services

- SSI Schaefer

- Buckhorn (Myers Industries)

- DS Smith

- Brambles (CHEP – RTP segment)

- IPL Plastics

- Mauser Packaging Solutions

- TranPak

- Nilkamal Limited

- Georg Utz Holding

- Rehrig Pacific Company