Paint Packaging Market Size and Growth

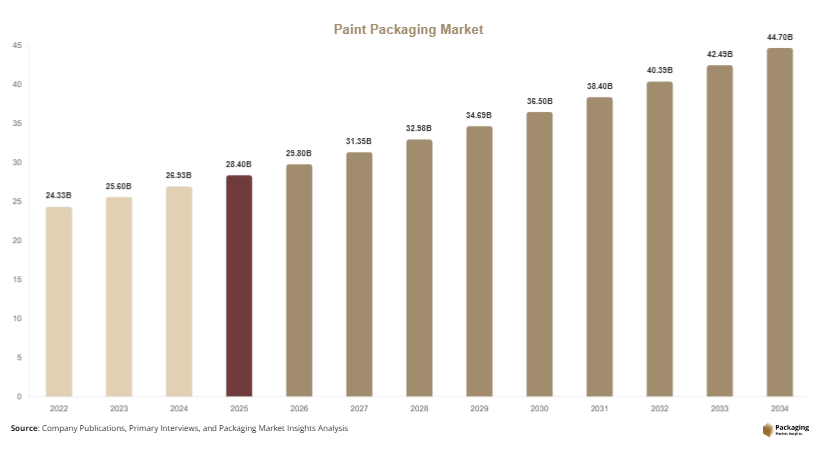

The global paint packaging market was valued at USD 28.4 billion in 2025 and is estimated to reach USD 29.8 billion in 2026. The market is further projected to reach USD 44.7 billion by 2034, expanding at a CAGR of 5.2% during the forecast period from 2025 to 2034. The market continues to experience stable growth due to increasing construction activities, expanding automotive production, and rising industrial coating consumption across developed and emerging economies. Paint packaging plays a critical role in ensuring product safety, shelf life, transportation efficiency, and brand differentiation for manufacturers operating in decorative, industrial, marine, and automotive coatings industries.

Growing urbanization across Asia Pacific, the Middle East, and Latin America has accelerated residential and commercial infrastructure development, leading to higher demand for paints and coatings. This trend has directly supported demand for metal cans, plastic containers, flexible pouches, and bulk paint packaging solutions. In addition, increasing renovation activities in mature economies such as the United States, Germany, France, and Japan have contributed to rising demand for premium and sustainable paint packaging formats.

Key Market Insights

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.1%.

- Metal packaging led the type segment with a 41.8% share.

- Plastic materials dominated with a 48.6% share.

- Decorative paints applications led the end-use segment with 46.2% share.

- The US remained the dominant country in North America with a market size of USD 4.8 billion in 2025 and USD 5.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Growing Adoption of Sustainable and Recyclable Paint Packaging

Sustainability has become a major trend shaping the paint packaging market as manufacturers focus on reducing carbon emissions and packaging waste. Regulatory pressure regarding plastic waste management and recycling targets has encouraged paint producers to adopt recyclable metal cans, reusable plastic containers, and paper-based solutions. Water-based paints are increasingly being packaged in lightweight recyclable containers to improve environmental performance and reduce transportation costs.

Several paint brands are introducing post-consumer recycled plastic packaging for decorative coatings and DIY paint products. Industrial manufacturers are also shifting toward reusable intermediate bulk containers for large-scale coating transportation. For example, construction paint suppliers in Europe have expanded the use of high-density polyethylene containers with recycled content to comply with regional sustainability standards. This transition is expected to improve circular economy practices across the packaging value chain.

Over the forecast period, sustainable packaging innovation is likely to become a competitive differentiator. Companies investing in biodegradable coatings, refill systems, and lightweight container technologies are expected to strengthen market positioning while addressing environmental compliance requirements.

Rising Demand for Smart and User-Friendly Packaging Designs

The market is witnessing increased demand for advanced packaging designs that improve convenience, safety, and consumer engagement. Paint manufacturers are incorporating ergonomic handles, resealable lids, anti-spill mechanisms, and tamper-evident seals to enhance usability and reduce product wastage. Smart labeling technologies with QR codes and digital product tracking are also becoming more common in premium packaging formats.

The rise of online paint sales and direct-to-consumer distribution has increased the importance of durable and leak-proof packaging solutions. E-commerce platforms require impact-resistant packaging capable of maintaining product integrity during transportation. As a result, flexible packaging and reinforced plastic containers are gaining popularity among decorative paint suppliers.

For instance, several Asian paint companies have introduced digitally printed packaging that provides application tutorials, color matching information, and recycling instructions through smartphone-enabled labels. This trend is expected to strengthen customer interaction and brand visibility while supporting digital transformation across the coatings industry.

Market Drivers

Expansion of Construction and Infrastructure Activities

Rapid growth in residential, commercial, and industrial construction projects continues to drive demand for paints and coatings, thereby supporting the paint packaging market. Governments across emerging economies are investing heavily in transportation infrastructure, smart cities, industrial parks, and affordable housing projects. These developments have increased the consumption of decorative and protective coatings requiring reliable packaging solutions.

The growth of urban populations in India, Indonesia, Vietnam, and African economies has accelerated new housing construction and renovation activities. Paint manufacturers require durable packaging formats capable of preserving product quality during transportation and storage across large distribution networks. This has increased demand for metal containers, stackable plastic buckets, and industrial drums.

For example, infrastructure modernization projects in the Middle East have significantly boosted demand for corrosion-resistant industrial coatings used in bridges, airports, and oil facilities. Such projects require bulk paint packaging systems designed for large-scale commercial operations. Continued investments in global infrastructure development are expected to sustain long-term market growth.

Increasing Automotive and Industrial Coating Consumption

The expansion of automotive manufacturing and industrial production has emerged as another major growth driver for the paint packaging market. Automotive coatings require specialized packaging with high chemical resistance and durability to maintain product stability. Industrial sectors including machinery, marine equipment, aerospace, and electronics also depend on high-performance coating solutions.

Growing vehicle production in China, Mexico, India, and Eastern Europe has increased the need for efficient packaging solutions for primers, protective coatings, and refinishing paints. Metal cans and high-barrier plastic containers are commonly used due to their resistance to solvent evaporation and contamination.

Industrial coating manufacturers are additionally adopting large-capacity packaging formats to improve logistics efficiency and reduce packaging waste. For instance, chemical manufacturing facilities increasingly use reusable bulk containers for transporting industrial coatings between suppliers and production sites. The rising demand for protective and specialty coatings across manufacturing industries is expected to strengthen packaging demand throughout the forecast period.

Market Restraint

Volatility in Raw Material Prices and Environmental Compliance Costs

Fluctuating raw material prices remain a significant restraint for the paint packaging market. Packaging manufacturers rely heavily on raw materials such as steel, aluminum, polyethylene, polypropylene, and specialty resins. Variations in crude oil prices and global metal supply chains can substantially increase production costs, affecting profit margins for packaging suppliers.

Environmental regulations regarding plastic usage, recycling obligations, and industrial emissions have also increased compliance costs across the packaging industry. Manufacturers are required to invest in sustainable materials, recycling infrastructure, and environmentally compliant production technologies. Smaller companies often face financial challenges in adapting to evolving regulatory standards.

For example, rising aluminum prices in Europe and North America have increased production costs for metal paint cans used in industrial and decorative coatings. At the same time, restrictions on single-use plastics have pressured packaging firms to redesign traditional packaging systems. These factors can slow adoption among cost-sensitive customers and create operational challenges for regional manufacturers.

In addition, transportation and energy cost fluctuations continue to impact packaging production economics. Supply chain disruptions affecting resin availability and metal sourcing may further restrain market growth during periods of global economic uncertainty.

Market Opportunities

Growth of Water-Based and Eco-Friendly Paints

The increasing adoption of water-based and low-VOC paints presents substantial opportunities for packaging manufacturers. Environmental awareness and stricter emissions regulations are encouraging consumers and industries to shift away from solvent-based coatings. This transition is creating demand for sustainable and lightweight packaging formats optimized for eco-friendly paint products.

Water-based paints typically require packaging with improved moisture resistance and contamination protection. Manufacturers are developing recyclable plastic containers and paper-composite packaging solutions tailored for environmentally friendly coatings. The decorative paints segment particularly benefits from this trend as homeowners increasingly prefer sustainable products.

Several packaging firms are investing in bio-based plastics and reusable paint containers to meet evolving market expectations. Future opportunities are expected to emerge in refillable packaging systems and closed-loop recycling programs. As sustainability initiatives expand globally, packaging suppliers capable of offering eco-friendly solutions are likely to gain long-term competitive advantages.

Expansion of E-Commerce Distribution Channels

The rapid growth of online retail channels for paints and coatings is creating new opportunities in protective and logistics-oriented packaging. E-commerce platforms require packaging solutions capable of preventing leakage, damage, and contamination during transportation. This has increased demand for impact-resistant containers, flexible pouches, and tamper-proof closures.

DIY home improvement trends and digital paint retailing have accelerated online paint sales in North America, Europe, and Asia Pacific. Consumers increasingly purchase decorative paints through e-commerce platforms due to convenience and product variety. Packaging manufacturers are responding by designing lightweight containers with improved stacking efficiency and shipping durability.

Future growth opportunities are expected in smart packaging systems integrated with tracking technologies and digital authentication features. Companies investing in advanced e-commerce packaging formats may benefit from rising online paint consumption across residential and commercial sectors.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28.4 Billion |

| Market Size in 2026 | USD 29.8 Billion |

| Market Size in 2034 | USD 44.7 Billion |

| CAGR | 5.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Metal packaging dominated the paint packaging market in 2024 with a market share of 41.8%. Metal cans and containers remain widely used for solvent-based paints, industrial coatings, and automotive applications due to their durability, chemical resistance, and long shelf life. Steel and aluminum packaging solutions provide superior protection against moisture, contamination, and leakage, making them suitable for hazardous and high-performance coatings. Industrial manufacturers prefer metal packaging for transporting protective coatings used in marine, aerospace, and heavy machinery applications. Decorative paint manufacturers also continue using metal cans for premium product lines because of their strong stacking capability and branding advantages. The widespread availability of recycling infrastructure for steel and aluminum further supports the dominance of metal packaging in developed economies such as the United States, Germany, and Japan.

Flexible packaging is projected to register the fastest CAGR of 6.4% during the forecast period. Flexible pouches and lightweight paint sachets are gaining popularity due to lower transportation costs, reduced material usage, and convenience in small-volume applications. Growth is particularly strong in emerging economies where affordable packaging solutions are increasingly demanded by low-income and middle-income consumers. Flexible packaging also supports e-commerce distribution by reducing shipping weight and improving storage efficiency. Several paint companies in Asia Pacific are introducing refill pouches for water-based decorative paints to minimize packaging waste and improve sustainability performance. Future demand is expected to rise further as manufacturers develop advanced multilayer films with enhanced leak resistance and product protection capabilities.

By Material

Plastic materials accounted for the largest share of 48.6% in 2024 due to their lightweight properties, cost efficiency, and versatility across multiple paint applications. High-density polyethylene and polypropylene containers are widely used for decorative paints, primers, emulsions, and water-based coatings because they offer durability and ease of handling. Plastic packaging also enables manufacturers to produce containers in various sizes and shapes suitable for residential, commercial, and industrial consumers. The growth of retail paint sales and home improvement activities has further strengthened demand for stackable plastic buckets and resealable containers. Packaging producers continue investing in advanced molding technologies to improve strength, reduce material consumption, and enhance transportation efficiency. In emerging markets, plastic packaging remains highly preferred because of its affordability and compatibility with large-scale manufacturing operations.

Paper-based materials are expected to witness the fastest CAGR of 6.0% through 2034. Increasing environmental awareness and sustainability regulations are encouraging paint manufacturers to explore renewable and recyclable packaging alternatives. Paper-composite containers and fiber-based packaging systems are increasingly used for eco-friendly paints and specialty coatings. The segment is benefiting from rising demand for biodegradable packaging solutions among environmentally conscious consumers and commercial buyers. Several European and North American packaging companies are introducing hybrid paper containers with moisture-resistant linings designed specifically for water-based paints. Future opportunities are likely to emerge in fully recyclable paper packaging systems integrated with bio-based barrier coatings. As governments continue implementing stricter plastic waste regulations, paper-based materials are expected to gain wider commercial acceptance across decorative paint applications.

By End-Use

Decorative paints represented the dominant end-use segment with a 46.2% market share in 2024. Strong demand from residential construction, commercial renovation, and home improvement activities continues to support packaging consumption within this segment. Decorative paints require packaging solutions that provide convenience, aesthetic appeal, and efficient storage for retail consumers. Plastic buckets, metal cans, and smaller-volume containers are commonly used for interior and exterior paints sold through retail distribution channels. Growth in urban housing projects and rising consumer spending on home decoration have increased demand for premium packaging designs with ergonomic handles and spill-resistant closures. Manufacturers are also investing in attractive labeling and digital printing technologies to improve product differentiation and brand visibility in competitive retail markets.

Industrial coatings are anticipated to register the fastest CAGR of 5.9% during the forecast period due to rising demand from automotive, marine, aerospace, electronics, and heavy machinery industries. Industrial coatings require specialized packaging capable of preserving chemical stability and ensuring safe transportation of hazardous materials. Large-capacity drums, intermediate bulk containers, and corrosion-resistant metal packaging systems are increasingly used across manufacturing sectors. Rapid industrialization in Asia Pacific and the Middle East has accelerated demand for protective coatings used in factories, infrastructure projects, and oil facilities. Future growth is expected to be supported by increasing adoption of smart industrial packaging with digital tracking systems and reusable container technologies designed to improve supply chain efficiency and sustainability performance.

Paint Packaging Market Segmentations

By Type

- Metal Packaging

- Plastic Containers

- Flexible Packaging

- Intermediate Bulk Containers

- Composite Containers

By Material

- Plastic

- Metal

- Paper & Paperboard

- Glass

- Composite Materials

By End-User

- Decorative Paints

- Industrial Coatings

- Automotive Paints

- Marine Coatings

- Protective Coatings

Regional Analysis

North America

North America accounted for 24.3% of the global paint packaging market share in 2025 and is projected to expand at a CAGR of 4.7% through 2034. The region benefits from stable demand across residential renovation, industrial coatings, and automotive refinishing sectors. Rising investments in infrastructure rehabilitation projects across the United States and Canada continue to support consumption of decorative and protective paints. The market is also influenced by increasing demand for sustainable packaging materials, particularly recyclable plastic containers and metal cans with reduced material usage. Growth in e-commerce distribution channels for DIY paints has further accelerated demand for durable and leak-resistant packaging solutions suitable for long-distance transportation.

The United States remained the dominant country in the regional market due to strong construction activity and high paint consumption across residential remodeling applications. One major growth driver is the increasing adoption of eco-friendly paints and coatings supported by environmental regulations. Several U.S. paint manufacturers are transitioning toward recycled plastic packaging and lightweight steel containers to reduce emissions and logistics costs. The expansion of smart home renovation projects and premium interior paints has also increased demand for innovative packaging designs with resealable lids and ergonomic features. Canada is additionally witnessing growth in industrial coatings used in mining and energy sectors, contributing to rising demand for industrial drums and bulk packaging systems.

Europe

Europe represented 21.7% of the global paint packaging market in 2025 and is anticipated to grow at a CAGR of 4.9% during the forecast period. The region maintains strong demand for sustainable and recyclable packaging solutions due to stringent environmental policies and circular economy initiatives. Countries across Western Europe are increasingly reducing dependence on virgin plastics and promoting reusable packaging systems for industrial coatings and decorative paints. Demand for water-based paints in residential and commercial applications has supported the use of lightweight packaging formats with improved recyclability. In addition, renovation of aging infrastructure across several European countries continues to stimulate coatings demand.

Germany emerged as the leading country within the European market due to its advanced automotive and industrial manufacturing sectors. A major growth driver in the country is the increasing production of industrial coatings used in automotive refinishing and machinery protection applications. German packaging manufacturers are investing in digitally printed packaging and smart labeling technologies to improve supply chain visibility and consumer engagement. France and Italy are also experiencing rising demand for decorative paints linked to urban renovation activities and hospitality construction projects. Northern European countries are further promoting bio-based packaging materials and reusable industrial containers to meet sustainability targets across the coatings industry.

Asia Pacific

Asia Pacific dominated the paint packaging market with a 39.1% share in 2025 and is expected to register a CAGR of 5.8% through 2034. Rapid urbanization, industrialization, and infrastructure expansion remain the primary growth drivers in the region. Strong growth in residential housing projects across China, India, Indonesia, and Vietnam has increased paint consumption and packaging demand. Rising automotive production and industrial manufacturing activities are also strengthening demand for industrial coating containers and bulk packaging solutions. The region benefits from cost-effective manufacturing capabilities and expanding domestic packaging industries capable of serving large-scale paint producers.

China maintained its position as the largest country-level market due to massive construction investments and strong industrial output. One unique growth driver is the rapid expansion of local decorative paint brands targeting middle-income consumers with affordable packaging formats. Chinese packaging companies are increasingly introducing lightweight plastic buckets and digitally printed metal cans designed for high-volume retail distribution. India is also experiencing substantial growth driven by smart city projects, residential development, and rising demand for water-based paints. Southeast Asian economies are witnessing increased investment in manufacturing facilities for plastic packaging and flexible paint pouches to support regional coating demand.

Middle East & Africa

The Middle East & Africa accounted for 7.8% of the global paint packaging market share in 2025 and is forecast to expand at a CAGR of 5.1% during the study period. Growth in the region is primarily supported by infrastructure development, industrial construction, and energy sector investments. Countries across the Gulf Cooperation Council are investing heavily in airports, tourism facilities, commercial buildings, and transportation projects, increasing demand for architectural and industrial coatings. This trend has accelerated the use of large-capacity paint containers, industrial drums, and corrosion-resistant metal packaging systems.

Saudi Arabia remained the dominant market in the region due to extensive construction activities linked to economic diversification programs and mega infrastructure projects. A key regional growth driver is the increasing use of protective coatings in oil and gas facilities, requiring specialized industrial packaging solutions capable of withstanding harsh environmental conditions. The United Arab Emirates is additionally witnessing increased demand for premium decorative paints used in hospitality and luxury residential projects. African economies such as South Africa and Egypt are also experiencing gradual growth in housing construction and industrial production, supporting demand for affordable plastic paint packaging formats.

Latin America

Latin America held 7.1% of the global paint packaging market in 2025 and is projected to record the fastest CAGR of 6.1% through 2034. The market is benefiting from expanding residential construction, urban population growth, and increasing industrial activity across Brazil, Mexico, Chile, and Colombia. Decorative paint demand continues to rise as governments invest in affordable housing programs and urban infrastructure modernization. Packaging manufacturers in the region are increasingly adopting lightweight plastic containers and flexible packaging systems to reduce logistics expenses and improve transportation efficiency across geographically dispersed markets.

Brazil emerged as the largest market within the region due to strong demand from construction and automotive refinishing industries. One important growth driver is the rapid expansion of retail paint distribution networks and home improvement stores across urban centers. Brazilian paint companies are increasingly introducing smaller packaging formats designed for DIY consumers and middle-income households. Mexico is also experiencing growth due to rising automotive manufacturing activities and industrial coating demand. Regional packaging suppliers are investing in recyclable plastic production technologies and cost-efficient container manufacturing to strengthen competitiveness in domestic and export markets.

Competitive Landscape

The paint packaging market remains moderately fragmented with the presence of global packaging manufacturers and regional suppliers competing across metal, plastic, and flexible packaging categories. Companies are focusing on sustainability initiatives, lightweight packaging development, digital printing technologies, and strategic acquisitions to strengthen market presence.

Ball Corporation is considered one of the leading players due to its extensive metal packaging portfolio and strong presence across industrial and decorative paint applications. The company continues investing in recyclable aluminum packaging solutions and advanced manufacturing technologies to improve operational efficiency.

Greif Inc. has expanded its industrial drum and bulk packaging business through acquisitions and capacity expansion projects targeting coatings and chemical industries. Berry Global Group focuses heavily on sustainable plastic packaging and recycled resin integration for paint containers. Mauser Packaging Solutions has strengthened its reusable industrial packaging operations for coatings transportation and storage. RPC Group continues developing lightweight plastic paint buckets and customized packaging solutions for decorative paint manufacturers.

Companies are increasingly collaborating with paint producers to design application-specific packaging formats that improve logistics efficiency and user convenience. Investments in automation, smart packaging technologies, and recyclable materials are expected to remain key competitive strategies throughout the forecast period.

Key Players List

- Ball Corporation

- Greif Inc.

- Berry Global Group

- Mauser Packaging Solutions

- RPC Group

- Amcor plc

- Crown Holdings

- Silgan Holdings

- SCHÜTZ GmbH & Co. KGaA

- Time Technoplast Ltd.

- IPL Plastics

- Nampak Ltd.

- Mondi Group

- Sonoco Products Company

- DS Smith