Packaging Testing Services Market Size and Growth

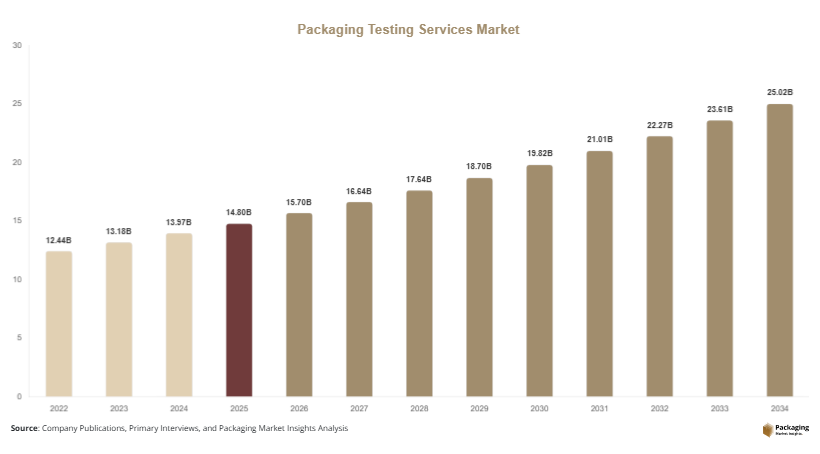

The global packaging testing services market was valued at USD 14.8 billion in 2025 and is projected to reach USD 24.9 billion by 2034, expanding at a CAGR of 6.0% during the forecast period from 2025 to 2034. The market is estimated to reach USD 15.7 billion in 2026 as regulatory compliance requirements, product safety standards, and international trade activities continue to strengthen across major industries. Packaging testing services are increasingly used to evaluate the durability, barrier protection, contamination resistance, labeling accuracy, and transportation safety of packaging materials used in food, beverages, pharmaceuticals, cosmetics, chemicals, and consumer goods.

The growing complexity of global supply chains has accelerated demand for advanced testing procedures. Manufacturers are adopting packaging validation services to reduce product recalls, prevent leakage or contamination, and ensure compliance with transportation regulations. E-commerce growth is also contributing significantly to the market as online retailers require packaging that can withstand long-distance handling, compression, and temperature fluctuations. In addition, pharmaceutical and healthcare industries are increasing investments in sterile and tamper-evident packaging testing to comply with safety regulations and serialization standards.

Key Market Highlights

- Asia Pacific dominated the market with a 38.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.8%.

- Physical testing services led the type segment with a 31.4% share.

- Plastic packaging materials dominated with a 47.6% share.

- Food & beverage applications led the end-use segment with 41.8% share.

- The US remained the dominant country with a market size of USD 3.6 billion in 2025 and USD 3.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable Packaging Validation

Sustainability initiatives are becoming a major trend in the packaging testing services market as manufacturers shift toward recyclable, compostable, and bio-based packaging solutions. Companies are increasingly testing paper-based flexible packaging, molded fiber containers, and mono-material plastics to verify durability and shelf-life performance. Sustainable materials often behave differently under moisture, temperature, and transportation pressure, creating a greater need for laboratory testing and certification services.

For example, food packaging producers are conducting migration testing and barrier analysis for biodegradable films used in ready-to-eat meal packaging. Retail brands are also requesting compression and drop testing for recycled corrugated boxes used in e-commerce deliveries. Testing laboratories are investing in climate chambers and advanced simulation systems to support sustainable packaging innovation. Over the forecast period, stricter environmental regulations and extended producer responsibility programs are expected to further increase demand for eco-friendly packaging validation services.

Growth of Smart and Connected Packaging Testing

The use of smart packaging technologies is transforming testing requirements across pharmaceuticals, food, and logistics industries. Smart labels, QR-enabled authentication systems, RFID packaging, and temperature-sensitive indicators are becoming more common in global supply chains. These packaging formats require specialized testing services to evaluate sensor functionality, data accuracy, adhesion quality, and environmental performance.

Pharmaceutical manufacturers are increasingly adopting intelligent packaging solutions for cold-chain monitoring and counterfeit prevention. Testing companies are developing advanced protocols to assess electronic component durability under varying humidity and vibration conditions. In the food sector, freshness-monitoring labels and oxygen sensors are creating new service opportunities for packaging laboratories. As connected packaging adoption rises, demand for integrated mechanical and electronic testing solutions is expected to expand steadily across both developed and emerging markets.

Market Drivers

Increasing Regulatory Compliance Requirements

One of the primary drivers of the packaging testing services market is the growing implementation of strict packaging safety regulations across industries. Governments and international organizations are enforcing standards related to contamination prevention, chemical migration, child-resistant packaging, and transport safety. Industries such as pharmaceuticals, food processing, and chemicals require certified packaging performance to ensure compliance with regional and international trade laws.

For instance, pharmaceutical companies must conduct stability testing, seal integrity testing, and sterile barrier validation before launching medical products. Food exporters are increasingly required to comply with packaging migration and contamination standards in North America and Europe. This regulatory environment is encouraging companies to outsource testing activities to accredited laboratories with specialized expertise. As global trade continues to expand, demand for packaging testing services is expected to remain strong throughout the forecast period.

Expansion of E-Commerce and Logistics Activities

Rapid growth in e-commerce and international logistics networks is significantly driving demand for packaging testing services. Products shipped through online channels face higher risks of compression damage, vibration, moisture exposure, and mishandling during transportation. Retailers and logistics providers are therefore increasing investments in package durability and transit testing to reduce return rates and customer complaints.

Large e-commerce platforms are implementing stricter packaging performance guidelines for suppliers. Corrugated packaging manufacturers are using drop testing, vibration testing, and compression testing services to improve package resilience during last-mile delivery. Consumer electronics and personal care companies are also adopting advanced transit simulation testing to reduce product damage. The continued rise of direct-to-consumer shipping models is expected to create sustained demand for transportation packaging validation services.

Market Restraint

High Cost of Advanced Testing Infrastructure

The high cost associated with advanced laboratory infrastructure remains a key restraint for the packaging testing services market. Modern testing facilities require significant investments in environmental simulation chambers, tensile testing equipment, spectroscopy systems, leak detection technologies, and automated inspection tools. Small and medium-sized testing companies often face financial challenges when upgrading laboratory capabilities to meet evolving industry standards.

In addition, maintaining international accreditation and regulatory compliance increases operational costs for testing service providers. Skilled technicians, laboratory calibration, and quality assurance programs further add to overall expenses. Smaller packaging manufacturers in developing countries may avoid comprehensive testing services due to budget limitations, relying instead on limited in-house quality checks. For example, regional food packaging suppliers in emerging markets frequently delay adoption of advanced barrier testing because of cost pressures. These financial constraints may slow market penetration in price-sensitive industries despite rising awareness regarding packaging safety and compliance.

Market Opportunities

Increasing Demand for Pharmaceutical Packaging Validation

The pharmaceutical industry presents strong growth opportunities for packaging testing service providers. Rising global healthcare spending, vaccine distribution, and biologics production are increasing the need for sterile and high-performance packaging systems. Pharmaceutical packaging requires rigorous validation to ensure product stability, contamination resistance, and regulatory compliance throughout the supply chain.

Testing laboratories are expanding capabilities for blister packaging analysis, container closure integrity testing, and accelerated aging studies. Injectable drug manufacturers are increasingly using high-barrier flexible packaging and temperature-sensitive materials that require advanced environmental testing. Cold-chain pharmaceutical logistics is also creating opportunities for thermal performance testing and transit simulation services. As pharmaceutical exports continue to grow globally, packaging validation services are expected to become an essential part of regulatory approval processes.

Expansion of Sustainable E-Commerce Packaging Solutions

The transition toward sustainable e-commerce packaging is creating significant opportunities for packaging testing companies. Retailers and logistics providers are adopting lightweight recyclable packaging to reduce shipping costs and carbon emissions. However, sustainable packaging materials require extensive performance testing to ensure they maintain strength during transportation and storage.

Testing service providers are introducing customized protocols for recycled corrugated boxes, paper mailers, and compostable protective packaging. Companies are also offering lifecycle analysis and environmental stress testing for reusable transport packaging systems. Fashion, electronics, and grocery delivery companies are increasingly partnering with laboratories to validate eco-friendly packaging durability. As sustainability targets become more aggressive across the retail industry, demand for specialized testing services for recyclable packaging formats is expected to rise substantially.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 14.8 Billion |

| Market Size in 2026 | USD 15.7 Billion |

| Market Size in 2034 | USD 24.9 Billion |

| CAGR | 6.0% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Physical testing services dominated the market in 2024 with a 31.4% share due to widespread demand for compression testing, drop testing, seal strength analysis, and vibration testing across industrial packaging applications. These services are critical for ensuring packaging durability during transportation and storage. Food, electronics, and consumer goods manufacturers extensively use physical testing to minimize product damage and reduce return rates. Corrugated box manufacturers and flexible packaging suppliers are investing heavily in transportation simulation testing to improve package reliability. E-commerce companies are also requiring physical validation standards for third-party suppliers. The segment continues to maintain strong demand because physical testing forms the foundation of packaging performance evaluation across nearly all industries.

Environmental testing services are projected to witness the fastest CAGR of 6.9% through 2034 due to rising demand for temperature, humidity, and climatic resistance analysis. Pharmaceutical and food packaging manufacturers are increasingly adopting environmental simulation testing to ensure shelf-life stability and contamination resistance. Sustainable packaging materials are also creating demand for moisture barrier and thermal performance testing. Companies are introducing advanced environmental chambers to simulate real-world transportation and storage conditions. Growth in cold-chain logistics and biologics transportation is expected to further support the adoption of environmental testing services in the coming years.

By Material

Plastic packaging materials accounted for the largest market share of 47.6% in 2024 because of their extensive use across food, beverages, pharmaceuticals, and industrial goods packaging. Plastic materials require comprehensive testing for migration analysis, tensile strength, leak detection, and chemical compatibility. Flexible plastic packaging used in snacks, frozen foods, and medical supplies must undergo strict barrier and durability evaluation to ensure regulatory compliance. The growing popularity of multilayer films and lightweight plastic packaging is increasing the complexity of testing requirements. Manufacturers are also investing in recycling validation and contamination testing for post-consumer recycled plastics to comply with sustainability standards.

Biodegradable materials are expected to grow at the fastest CAGR of 7.1% during the forecast period. Rising environmental regulations and consumer preference for sustainable packaging are driving adoption of compostable films, molded fiber materials, and paper-based alternatives. However, these materials require extensive testing for durability, shelf life, and moisture resistance before commercial deployment. Testing providers are developing specialized protocols to evaluate compostability and biodegradation performance. The expansion of sustainable retail packaging and eco-friendly food containers is expected to create strong long-term demand for biodegradable packaging testing services.

By End-Use

Food & beverage applications dominated the packaging testing services market with a 41.8% share in 2024 due to strict food safety regulations and increasing global trade of packaged food products. Packaging used for beverages, dairy products, frozen foods, and ready-to-eat meals requires extensive testing for contamination prevention, migration control, and shelf-life stability. Food exporters are heavily dependent on packaging validation to meet import regulations in developed markets. Flexible packaging and vacuum-sealed food containers are also increasing demand for seal integrity and oxygen barrier testing. The continued expansion of processed food consumption and online grocery delivery is expected to sustain strong testing demand in this segment.

Pharmaceutical packaging is projected to register the fastest CAGR of 7.3% through 2034 due to growing healthcare spending and rising biologics production. Pharmaceutical products require sterile barrier systems, tamper-evident packaging, and temperature-sensitive transport solutions. Testing laboratories are witnessing rising demand for container closure integrity testing, stability analysis, and accelerated aging studies. Growth in injectable drugs, vaccine logistics, and personalized medicine packaging is expected to further accelerate testing requirements. Increasing regulatory scrutiny related to medical packaging safety will continue supporting strong segment growth during the forecast period.

Packaging Testing Services Market Segmentations

By Type

- Physical Testing

- Chemical Testing

- Microbiological Testing

- Environmental Testing

- Shelf-Life Testing

By Material

- Plastic

- Paper & Paperboard

- Glass

- Metal

- Biodegradable Materials

By End-User

- Food & Beverage

- Pharmaceuticals

- Consumer Goods

- Chemicals

- Industrial Packaging

Regional Analysis

North America

North America accounted for 27.8% of the global packaging testing services market in 2025 and is projected to expand at a CAGR of 5.7% through 2034. The region benefits from strict packaging safety regulations across pharmaceuticals, food processing, and consumer goods industries. Strong adoption of advanced packaging technologies and growing demand for sustainable materials are supporting testing service expansion. E-commerce growth in the United States and Canada is also increasing demand for transportation testing and package integrity validation. Major testing laboratories are investing in automated testing systems and AI-enabled inspection technologies to improve efficiency and reduce turnaround time for industrial clients.

The United States remained the dominant country in North America due to its large pharmaceutical manufacturing base and well-established retail logistics infrastructure. A major growth driver in the country is the increasing adoption of cold-chain pharmaceutical packaging. Vaccine transportation, biologics distribution, and specialty drug exports are creating strong demand for temperature validation and sterile barrier testing services. Several packaging laboratories are expanding ISO-certified facilities to support medical packaging compliance. The growing use of sustainable e-commerce packaging by major retailers is also contributing to increased testing demand across the country.

Europe

Europe held 24.6% of the global packaging testing services market in 2025 and is forecast to grow at a CAGR of 5.5% during the forecast period. The region’s strong regulatory framework for food safety, sustainability, and chemical packaging standards continues to support market growth. European manufacturers are increasingly focusing on recyclable and reusable packaging materials, driving demand for environmental simulation and material performance testing. Countries such as Germany, France, and the United Kingdom are investing heavily in circular packaging systems. Rising exports of processed foods and healthcare products are also contributing to packaging validation requirements across regional supply chains.

Germany dominated the European market due to its advanced manufacturing sector and strong packaging engineering capabilities. A unique growth driver in Germany is the expansion of sustainable industrial packaging for automotive and machinery exports. Companies are adopting lightweight corrugated and reusable transport packaging to reduce logistics costs and carbon emissions. Testing laboratories are offering advanced vibration, compression, and climatic testing services for export-oriented packaging solutions. In addition, increasing research into biodegradable packaging materials is supporting innovation within the regional testing industry.

Asia Pacific

Asia Pacific dominated the global packaging testing services market with a 38.2% share in 2025 and is expected to register a CAGR of 6.5% through 2034. Rapid industrialization, strong manufacturing growth, and expanding export activities are driving regional demand for packaging validation services. Countries across the region are strengthening packaging safety standards for food exports, pharmaceuticals, and consumer electronics. The growing use of flexible packaging and lightweight materials is increasing demand for seal integrity and durability testing. Rising investments in logistics infrastructure and warehouse automation are also supporting transportation packaging evaluation across the region.

China remained the leading country in Asia Pacific due to its large-scale manufacturing and export operations. One key growth driver in the country is the rapid expansion of cross-border e-commerce packaging. Chinese exporters are increasingly using testing services to comply with packaging regulations in North America and Europe. Electronics manufacturers are also investing in shock-resistant and anti-static packaging validation. Furthermore, the growth of food delivery platforms and processed food exports is creating rising demand for migration testing and shelf-life analysis services throughout the country.

Middle East & Africa

The Middle East & Africa region represented 5.8% of the global packaging testing services market in 2025 and is projected to expand at a CAGR of 5.9% through 2034. Growth in the region is supported by rising investments in food processing, pharmaceutical manufacturing, and industrial packaging sectors. Governments across the Gulf countries are implementing stricter packaging regulations to improve product safety and export competitiveness. Increasing demand for imported packaged foods and healthcare products is also contributing to testing service adoption. Logistics hubs in the UAE and Saudi Arabia are driving the need for transportation and environmental testing solutions.

Saudi Arabia emerged as the dominant country in the region due to rapid industrial diversification and healthcare sector expansion. A unique growth driver in the country is the development of pharmaceutical and medical packaging production under national industrial initiatives. Companies are increasingly investing in sterile packaging validation and shelf-life testing to support domestic healthcare manufacturing. The growth of temperature-sensitive food imports and cold-chain logistics is also increasing demand for packaging performance evaluation services across the kingdom.

Latin America

Latin America accounted for 3.6% of the global packaging testing services market in 2025 and is expected to grow at the fastest CAGR of 6.8% during the forecast period. Expanding food exports, retail modernization, and rising pharmaceutical production are supporting regional market growth. Countries across the region are improving packaging quality standards to strengthen international trade competitiveness. Demand for flexible packaging and corrugated transport packaging is increasing significantly in agriculture and processed food sectors. Testing laboratories are also witnessing higher demand for contamination analysis and transportation simulation services from export-oriented manufacturers.

Brazil dominated the Latin American market due to its strong agricultural exports and expanding food processing industry. A major growth driver in the country is the increasing export of packaged meat, coffee, and processed food products. Manufacturers are investing in packaging durability testing and migration analysis to meet international import standards. The expansion of retail e-commerce and pharmaceutical distribution is also encouraging the adoption of advanced package integrity testing services throughout Brazil.

Competitive Landscape

The packaging testing services market remains moderately consolidated, with global testing and certification companies competing through laboratory expansion, accreditation upgrades, and digital quality solutions. Leading companies are investing in automation, AI-enabled inspection systems, and sustainable packaging validation capabilities to strengthen market positioning. Strategic collaborations with food manufacturers, pharmaceutical companies, and e-commerce retailers are becoming increasingly common.

SGS SA remains one of the leading players in the market due to its extensive global laboratory network and diversified testing portfolio. The company continues expanding sustainable packaging testing capabilities and pharmaceutical validation services. Intertek Group plc and Bureau Veritas are strengthening digital packaging inspection and transportation testing services to support global trade requirements. Eurofins Scientific is focusing on food-contact material testing and contamination analysis, while TÜV SÜD is expanding medical packaging validation and cold-chain testing solutions.

Companies are also investing in regional laboratory expansion to support emerging markets in Asia Pacific and Latin America. Sustainability-focused testing services and smart packaging validation are expected to remain major competitive strategies across the industry.