Packaging In Supply Chain Management Market Size and Growth

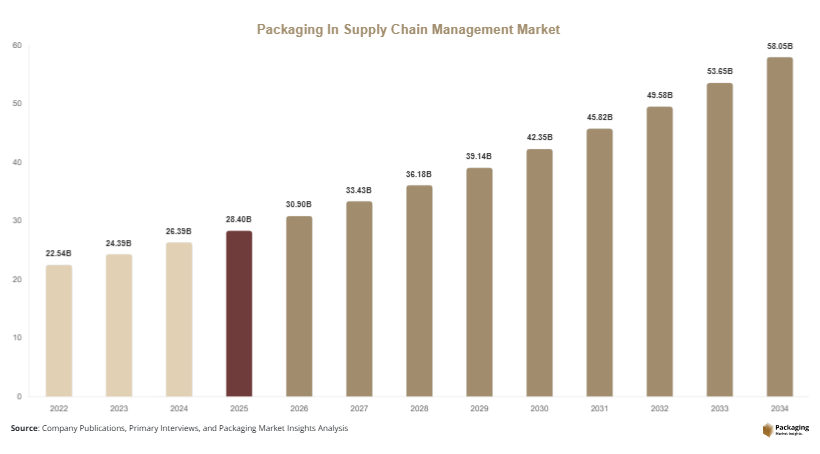

The global packaging in supply chain management market is estimated at USD 28.4 billion in 2025, and it is projected to reach USD 30.9 billion in 2026. By 2034, the market is forecasted to expand to USD 58.7 billion, registering a CAGR of 8.2% (2025–2034). This strong growth reflects increasing global trade complexity, rising demand for temperature-controlled logistics, and rapid adoption of smart packaging technologies integrated with digital supply chain systems.

The packaging in supply chain management market is evolving into a core enabler of global logistics efficiency, driven by increasing demand for end-to-end visibility, product protection, and automation across distribution networks. Packaging is no longer viewed as a static material layer; it has become an integrated component of supply chain intelligence, supporting tracking, sustainability compliance, and operational optimization across industries such as e-commerce, food and beverage, pharmaceuticals, automotive, and industrial manufacturing.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Smart tracking packaging solutions led the type segment with a 33.9% share.

- Plastic packaging dominated with a 51.6% share.

- Food & beverage applications led the segment with 42.7% share.

- The US remained the dominant country with a market size of USD 12.4 billion in 2025 and USD 13.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rise of Smart and Connected Packaging Systems in Supply Chains

A major trend shaping the packaging in supply chain management market is the rapid adoption of smart packaging systems integrated with IoT, RFID, and cloud-based tracking platforms. These technologies allow packaging units to transmit real-time data on product location, temperature, humidity, and handling conditions. For example, pharmaceutical companies in Europe are increasingly using RFID-enabled packaging to track vaccine distribution across cold chain networks. Similarly, logistics companies in the United States are deploying sensor-based packaging for high-value electronics to reduce theft and damage risks. This trend is expected to expand further as AI-driven supply chain platforms integrate packaging data for predictive logistics optimization and automated decision-making.

Growth of Sustainable and Circular Packaging Models

Sustainability is another key trend reshaping supply chain packaging strategies. Companies are shifting toward recyclable, reusable, and compostable packaging materials to comply with environmental regulations and reduce carbon footprints. For instance, FMCG companies in Germany and the Netherlands are adopting closed-loop packaging systems where containers are returned, cleaned, and reused in distribution cycles. In Asia, e-commerce platforms are introducing biodegradable packaging for last-mile deliveries to reduce plastic waste. Over time, circular packaging models are expected to become a standard practice in global supply chains, supported by regulatory frameworks and consumer demand for environmentally responsible logistics operations.

Market Drivers

Expansion of Global E-commerce and Omnichannel Distribution

The rapid growth of e-commerce platforms is a key driver of the packaging in supply chain management market. With increasing online purchases, companies require advanced packaging systems that ensure product protection, efficient warehousing, and optimized delivery processes. For example, large fulfillment centers in China and the United States are investing in automated packaging lines that integrate directly with inventory management systems. These systems reduce packaging time, improve accuracy, and enhance shipment tracking. The rise of same-day and next-day delivery models has further intensified demand for high-performance packaging solutions that can withstand complex logistics environments.

Rising Demand for Pharmaceutical and Cold Chain Logistics

Another major driver is the growing need for temperature-controlled and secure packaging in pharmaceutical supply chains. Vaccines, biologics, and specialty drugs require strict temperature management throughout transportation and storage. For instance, global vaccine distribution during large-scale immunization programs has significantly increased demand for insulated packaging solutions with integrated temperature monitoring systems. Pharmaceutical companies are adopting advanced packaging technologies such as phase-change materials and digital sensors to maintain product integrity. As healthcare logistics continue to expand globally, this segment will remain a critical driver of market growth.

Market Restraint

High Cost of Smart and Sustainable Packaging Integration

One of the primary restraints in the packaging in supply chain management market is the high cost associated with advanced packaging systems. Smart packaging technologies, including RFID-enabled systems, IoT sensors, and biodegradable materials, require significant investment in both infrastructure and integration with supply chain software. Small and medium-sized enterprises often struggle to adopt these solutions due to budget limitations. For example, logistics providers in developing regions still rely on conventional packaging methods because smart packaging costs increase operational expenses. Additionally, maintenance, data management, and technology upgrades further add to the total cost burden. This financial challenge slows down adoption rates, particularly in cost-sensitive markets.

Market Opportunities

Expansion of AI-Driven Supply Chain Packaging Optimization

The integration of artificial intelligence into supply chain packaging systems presents a major opportunity for market growth. AI-powered platforms can analyze packaging performance, predict damage risks, and optimize material usage based on shipping conditions. For instance, logistics companies in the United States are using AI-based systems to determine optimal packaging sizes, reducing material waste and transportation costs. In the future, AI-driven packaging optimization will become a standard feature in warehouse automation systems, improving efficiency and reducing environmental impact across global supply chains.

Growth of Cross-Border Trade and Global Logistics Networks

Increasing international trade is creating strong opportunities for advanced packaging solutions in supply chain management. As companies expand their global footprint, they require packaging systems that comply with diverse regulatory standards and withstand long-distance transportation. For example, export-driven manufacturing hubs in Southeast Asia are adopting reinforced packaging systems to ensure product safety during long-haul shipments to Europe and North America. This trend is expected to accelerate as global trade agreements and digital logistics platforms streamline cross-border commerce, increasing demand for standardized and intelligent packaging solutions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 28.4 Billion |

| Market Size in 2026 | USD 30.9 Billion |

| Market Size in 2034 | USD 58.7 Billion |

| CAGR | 8.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Smart tracking packaging solutions dominated with a 33.9% share in 2024, driven by widespread adoption of RFID, QR codes, and sensor-based packaging in logistics operations. These solutions are widely used in pharmaceuticals and high-value goods transportation to ensure visibility and reduce losses. For example, global logistics firms use smart packaging to monitor shipment conditions in real time.

Sustainable intelligent packaging is the fastest-growing segment with a CAGR of 7.1%, driven by environmental regulations and corporate sustainability goals. Companies are increasingly adopting recyclable and biodegradable packaging integrated with digital tracking features. Future growth will be supported by advancements in eco-friendly materials and smart labeling technologies.

By Material

Plastic-based packaging dominated with a 51.6% share in 2024, due to its durability, cost efficiency, and widespread use in FMCG and industrial logistics. It remains the preferred material for high-volume shipping applications.

Paper-based and biodegradable packaging is the fastest-growing segment with a CAGR of 6.3%, driven by sustainability initiatives and regulatory pressure to reduce plastic waste. Companies in Europe and North America are increasingly transitioning toward recyclable packaging materials, particularly in food and retail logistics.

By End-Use

Food & beverage logistics dominated with a 42.7% share in 2024, driven by global demand for packaged and perishable goods. Packaging plays a critical role in ensuring product safety and shelf life.

Healthcare logistics is the fastest-growing segment with a CAGR of 6.8%, driven by rising pharmaceutical shipments and cold chain requirements. Hospitals and pharmaceutical companies are increasingly adopting temperature-controlled and secure packaging systems.

Packaging In Supply Chain Management Market Segmentations

By Type

- Smart Tracking Packaging Systems

- Sustainable Packaging Solutions

- Protective Packaging Solutions

- Temperature-Controlled Packaging

- Returnable & Reusable Packaging Systems

By Material

- Plastic Packaging

- Paper & Paperboard Packaging

- Metal Packaging

- Biodegradable & Compostable Materials

- Hybrid Composite Materials

By End-User

- Food & Beverage

- Pharmaceuticals & Healthcare

- E-commerce & Retail

- Industrial Manufacturing

- Logistics & Transportation

- Automotive Supply Chain

Regional Analysis

North America

North America accounted for 28.9% market share in 2025, with a projected CAGR of 7.8%. The region benefits from advanced logistics infrastructure, strong e-commerce penetration, and high adoption of automation technologies in supply chain operations. Packaging systems integrated with digital tracking and warehouse management platforms are widely used across retail and pharmaceutical sectors.

The United States dominates the region due to its highly developed distribution networks. A key growth driver is the expansion of automated fulfillment centers operated by major e-commerce companies. For example, large logistics hubs in Texas and California use AI-enabled packaging lines that synchronize with real-time inventory systems, improving delivery efficiency and reducing packaging waste.

Europe

Europe held 24.1% market share in 2025, with a CAGR of 7.4%. The region is strongly influenced by sustainability regulations, circular economy initiatives, and advanced manufacturing practices. Demand for eco-friendly and traceable packaging solutions is high across industries.

Germany leads the European market due to its strong industrial base. A key driver is the adoption of closed-loop packaging systems in automotive and industrial supply chains. For example, German manufacturers use reusable packaging containers for cross-border component transportation, reducing packaging waste and improving supply chain efficiency.

Asia Pacific

Asia Pacific dominated with 37.4% market share in 2025, and is projected to grow at a CAGR of 9.1%. Rapid industrialization, expanding e-commerce ecosystems, and rising manufacturing output are major growth factors. The region is also witnessing strong investment in smart logistics infrastructure.

China remains the dominant country due to its large-scale manufacturing and export-oriented economy. A key growth driver is the integration of smart packaging systems in e-commerce logistics. For instance, Chinese fulfillment centers use RFID-enabled packaging to manage millions of daily shipments efficiently across domestic and international markets.

Middle East & Africa

The region accounted for 5.9% market share in 2025, with a CAGR of 6.6%. Growth is driven by expanding retail infrastructure, increasing pharmaceutical imports, and development of logistics hubs in Gulf countries. The adoption of modern supply chain systems is gradually increasing.

The UAE dominates the region due to its strategic position as a global trade hub. A key driver is the expansion of smart free zones in Dubai, where automated packaging systems are used for high-volume re-export operations across Africa and Europe.

Latin America

Latin America held 3.7% market share in 2025, with the fastest CAGR of 6.2%. Growth is supported by expanding food exports, rising e-commerce adoption, and improvements in logistics infrastructure. Packaging modernization is becoming essential for competitiveness.

Brazil leads the region due to its strong agricultural export sector. A key driver is the increasing use of durable packaging solutions for long-distance food exports, particularly in meat and processed food industries, ensuring product safety during international shipments.

Competitive Landscape

The packaging in supply chain management market is moderately fragmented, with major players focusing on smart packaging technologies, sustainability solutions, and digital integration. Key companies include Amcor plc, Sealed Air Corporation, DS Smith Plc, Smurfit Kappa Group, and Mondi Group. Among these, Amcor plc leads the market due to its extensive global presence and strong focus on sustainable packaging innovation.

Companies are investing heavily in recyclable materials, IoT-enabled packaging, and AI-driven supply chain integration. Recent strategies include partnerships with logistics firms, expansion into emerging markets, and development of smart packaging platforms that enhance supply chain visibility and efficiency.

Key Players List

- Amcor plc

- Sealed Air Corporation

- DS Smith Plc

- Smurfit Kappa Group

- Mondi Group

- WestRock Company

- Sonoco Products Company

- International Paper Company

- Ball Corporation

- Berry Global Inc.

- Huhtamaki Oyj

- Uflex Ltd.

- Stora Enso Oyj

- Nippon Paper Industries

- Coveris Holdings S.A.