Packaging For Aseptic Manufacturing Market Size and Growth

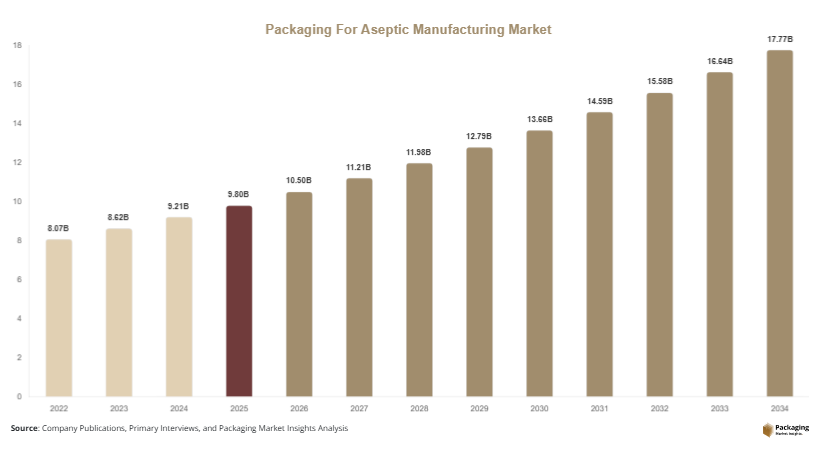

The global packaging for aseptic manufacturing market was valued at USD 9.8 billion in 2025 and is estimated to reach USD 10.5 billion in 2026. By 2034, the market is projected to achieve USD 18.9 billion, expanding at a CAGR of 6.8% during the forecast period from 2025 to 2034. Aseptic manufacturing packaging solutions are widely used across pharmaceutical, biotechnology, medical device, and food processing industries where maintaining sterility is essential for product safety and shelf stability. The global packaging for aseptic manufacturing market is experiencing steady growth due to increasing demand for sterile pharmaceutical packaging, biologics production, and contamination-free manufacturing environments.

The growing production of injectable drugs and biologics is one of the major factors accelerating market growth. Pharmaceutical manufacturers are increasingly investing in aseptic filling lines, sterile barrier systems, and contamination-resistant packaging to comply with strict regulatory standards. The expansion of vaccine manufacturing capacity across developed and emerging economies has further increased the demand for aseptic bags, sterile containers, vials, ampoules, and barrier films. The rise in chronic diseases and demand for advanced therapeutics has also strengthened the requirement for secure sterile packaging systems.

Key Highlights

- North America dominated the market with a 34.8% share in 2025.

- Asia Pacific is projected to grow at the fastest CAGR of 7.6%.

- Sterile bags and pouches led the type segment with a 31.2% share.

- Plastic-based aseptic packaging dominated the material segment with a 48.7% share.

- Pharmaceutical applications led the end-use segment with 51.9% share.

- The US remained the dominant country with a market size of USD 2.7 billion in 2025 and USD 2.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Single-Use Sterile Packaging Systems

Single-use sterile packaging systems are becoming increasingly common across aseptic manufacturing environments due to their operational flexibility and contamination control benefits. Pharmaceutical and biotechnology manufacturers are replacing reusable stainless-steel systems with disposable sterile bags, tubing assemblies, and aseptic connectors. These packaging systems help reduce cleaning validation costs, shorten production turnaround time, and improve manufacturing efficiency. The increasing production of biologics, vaccines, and personalized medicines is further accelerating adoption because sterile single-use packaging minimizes contamination risks during sensitive manufacturing processes.

For example, several contract development and manufacturing organizations are expanding their use of disposable aseptic filling systems for clinical-stage biologics production. The trend is also gaining traction in emerging economies where pharmaceutical manufacturers seek cost-efficient sterile manufacturing solutions. In the future, single-use packaging systems are expected to integrate advanced tracking sensors and smart sterilization indicators to improve quality assurance and production monitoring.

Growing Demand for Sustainable Aseptic Packaging Materials

Sustainability initiatives are reshaping the packaging for aseptic manufacturing market as manufacturers focus on recyclable and lightweight sterile packaging materials. Pharmaceutical companies are under increasing pressure to reduce packaging waste while maintaining sterility standards. This has encouraged suppliers to develop recyclable barrier films, lightweight polymer packaging, and bio-based sterile materials for aseptic manufacturing environments.

Several global packaging companies are investing in low-carbon manufacturing technologies and sustainable resin materials for pharmaceutical applications. For instance, sterile packaging manufacturers are introducing mono-material barrier structures that improve recyclability without compromising product protection. Demand is particularly strong in Europe and North America where environmental regulations are becoming stricter. Over the forecast period, sustainable aseptic packaging is expected to become a major competitive differentiator, especially among pharmaceutical companies pursuing carbon reduction goals and circular economy initiatives.

Market Drivers

Expansion of Biologics and Injectable Drug Manufacturing

The rapid growth of biologics and injectable pharmaceuticals is a major driver for the packaging for aseptic manufacturing market. Injectable drugs require highly sterile production and packaging conditions to ensure patient safety and regulatory compliance. The increasing prevalence of chronic diseases, autoimmune disorders, and cancer has accelerated the demand for injectable therapies and biosimilars globally.

Biotechnology companies and pharmaceutical manufacturers are expanding aseptic production facilities to meet rising therapeutic demand. For example, several vaccine and biologics manufacturing plants in the U.S., India, and Germany have increased investments in sterile packaging systems for vials, cartridges, and prefilled syringes. This expansion directly supports demand for contamination-resistant packaging products. As advanced therapeutics continue to grow, the requirement for high-performance aseptic packaging solutions is expected to increase significantly.

Stringent Regulatory Standards for Sterile Manufacturing

Global healthcare authorities are enforcing strict regulations regarding sterile manufacturing and contamination prevention. Regulatory agencies require pharmaceutical manufacturers to maintain high levels of sterility assurance throughout production, storage, and transportation processes. As a result, companies are investing heavily in advanced aseptic packaging technologies.

For instance, pharmaceutical manufacturers are implementing high-barrier sterile packaging systems and tamper-evident packaging to comply with updated manufacturing standards. Increased inspections and compliance requirements across North America and Europe are encouraging companies to modernize packaging infrastructure. The growing importance of product traceability and patient safety is also contributing to demand for secure aseptic packaging systems. Regulatory-driven investments are expected to remain a major growth contributor throughout the forecast period.

Market Restraint

High Production and Validation Costs

High production and validation costs remain a key restraint for the packaging for aseptic manufacturing market. Aseptic packaging systems require specialized materials, sterilization processes, cleanroom environments, and strict quality control procedures. These requirements significantly increase operational expenses for manufacturers. Small and medium-sized pharmaceutical companies often face challenges in adopting advanced aseptic packaging solutions due to high capital investments and ongoing compliance costs.

Validation procedures for sterile packaging systems are also complex and time-consuming. Companies must conduct extensive microbial testing, packaging integrity analysis, and sterilization verification before commercial deployment. For example, biologics manufacturers using high-barrier multilayer packaging must comply with rigorous regulatory documentation and testing standards, increasing product development timelines. In developing economies, limited access to advanced sterile manufacturing infrastructure further restricts adoption. Rising raw material costs and supply chain disruptions for medical-grade polymers also create pricing pressure across the industry, potentially limiting profit margins for packaging manufacturers.

Market Opportunities

Growth of Contract Manufacturing Organizations

The rapid expansion of pharmaceutical contract manufacturing organizations is creating substantial opportunities for aseptic packaging providers. Many pharmaceutical and biotechnology companies are outsourcing sterile manufacturing operations to specialized contract manufacturers to reduce infrastructure investments and accelerate production timelines. This shift has increased demand for flexible sterile packaging solutions compatible with multiple drug formulations and production scales.

Contract manufacturers increasingly rely on ready-to-use sterile packaging systems, pre-sterilized containers, and disposable aseptic assemblies to improve operational efficiency. The trend is particularly strong in Asia Pacific where pharmaceutical outsourcing continues to expand. Future growth opportunities are expected in customized aseptic packaging designed for cell therapies, biosimilars, and personalized medicines. Packaging suppliers capable of offering scalable and regulatory-compliant solutions are likely to benefit significantly from this trend.

Expansion of Aseptic Packaging in Nutritional Beverages

Aseptic packaging adoption is increasing in nutritional beverages, dairy alternatives, and shelf-stable liquid foods. Consumers are demanding preservative-free beverages with longer shelf life, encouraging food manufacturers to invest in advanced aseptic manufacturing technologies. This creates new growth opportunities for packaging companies supplying sterile cartons, multilayer barrier films, and aseptic filling systems.

Several beverage manufacturers are expanding aseptic processing capacity for plant-based drinks, protein beverages, and infant nutrition products. Emerging economies in Latin America and Asia Pacific are witnessing strong demand for shelf-stable packaged beverages due to changing retail distribution networks and rising urbanization. In the future, innovative lightweight aseptic packaging solutions with enhanced barrier performance are expected to gain strong commercial adoption across food and beverage applications.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.8 Billion |

| Market Size in 2026 | USD 10.5 Billion |

| Market Size in 2034 | USD 18.9 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Sterile bags and pouches dominated the type segment with a 31.2% market share in 2024. These packaging solutions are widely used across pharmaceutical and biotechnology manufacturing because they provide strong contamination resistance, lightweight handling, and compatibility with single-use systems. Sterile bags are commonly utilized in biologics processing, media storage, and fluid transfer applications. Pharmaceutical manufacturers increasingly prefer flexible sterile packaging because it reduces cleaning requirements and supports operational efficiency. Growth in vaccine manufacturing and injectable drug production has significantly increased demand for sterile flexible packaging systems. Companies are also introducing multilayer barrier films with enhanced puncture resistance and sterilization compatibility to improve product protection.

Prefilled syringes are projected to witness the fastest CAGR of 7.4% during the forecast period. Rising demand for self-administered injectable therapies and biologics is accelerating adoption of prefilled delivery systems. Pharmaceutical companies prefer prefilled syringes because they improve dosage accuracy, reduce contamination risks, and support patient convenience. Demand is especially strong for chronic disease treatments, insulin therapies, and specialty biologics. Manufacturers are investing in polymer-based syringe technologies with improved break resistance and enhanced sterility protection. Future growth is expected to be driven by expansion of home healthcare and rising demand for ready-to-use injectable drug delivery systems.

By Material

Plastic-based aseptic packaging dominated the material segment with a 48.7% share in 2024. Plastic materials such as polyethylene, polypropylene, and cyclic olefin polymers are widely used due to their flexibility, lightweight properties, and compatibility with sterilization processes. Pharmaceutical companies prefer plastic packaging because it offers strong barrier performance while reducing transportation costs. Plastic materials are extensively utilized in sterile bags, pouches, vials, and tubing systems for aseptic manufacturing. Increasing use of disposable packaging systems in biologics production has further strengthened segment growth. Manufacturers are also developing medical-grade polymers with improved chemical resistance and lower extractables to meet regulatory standards.

High-barrier composite materials are expected to grow at the fastest CAGR of 7.1% during the forecast period. These materials combine multiple protective layers to improve moisture resistance, oxygen barrier performance, and contamination protection. Composite aseptic packaging is increasingly used in sensitive biologics, vaccines, and nutritional products requiring extended shelf life. Packaging manufacturers are investing in recyclable multilayer structures to balance sterility performance with sustainability goals. Demand is expected to increase significantly as pharmaceutical companies seek advanced packaging capable of supporting complex biologic formulations and global distribution requirements.

By End-Use

Pharmaceutical applications dominated the end-use segment with a 51.9% market share in 2024. The segment benefits from growing injectable drug production, increasing biologics manufacturing, and rising demand for sterile medical products. Aseptic packaging solutions are critical for maintaining product integrity throughout pharmaceutical manufacturing and distribution processes. Pharmaceutical companies are heavily investing in sterile fill-finish systems, contamination-resistant packaging, and automated aseptic production lines. Increasing global demand for vaccines, insulin products, and oncology therapies has significantly expanded the use of aseptic packaging technologies across the pharmaceutical industry.

Biotechnology manufacturing is anticipated to register the fastest CAGR of 7.8% during the forecast period. Rapid growth in cell therapies, monoclonal antibodies, and personalized medicine production is increasing demand for advanced sterile packaging systems. Biotechnology companies require highly specialized packaging solutions capable of protecting temperature-sensitive biologics from contamination and environmental exposure. Single-use sterile packaging products are gaining popularity because they improve manufacturing flexibility and reduce downtime. Future demand is expected to rise as global investment in biotechnology research and commercial biologics manufacturing continues to expand.

Packaging For Aseptic Manufacturing Market Segmentations

By Type

- Vials & Ampoules

- Pre-Filled Syringes

- Bags & Pouches

- Bottles & Containers

- Cartons & Composite Packaging

By Material

- Plastic

- Glass

- Metal

- Paperboard & Laminates

By End-User

- Pharmaceutical Manufacturing

- Biotechnology Companies

- Food & Beverage Processing

- Medical Device Packaging

- Contract Manufacturing Organizations

Regional Analysis

North America

North America accounted for 34.8% of the global packaging for aseptic manufacturing market share in 2025 and is expected to maintain steady growth at a CAGR of 6.4% during the forecast period. The region benefits from a highly developed pharmaceutical industry, advanced biologics manufacturing infrastructure, and strict regulatory oversight. Demand for sterile packaging systems continues to rise due to increasing injectable drug production and expansion of biotechnology research facilities. The U.S. remains the largest contributor to regional growth due to strong investments in aseptic drug manufacturing technologies. Growing adoption of automation and robotic filling systems further supports market expansion across pharmaceutical and medical device applications.

The U.S. dominates the regional market due to large-scale vaccine manufacturing, biologics production, and pharmaceutical exports. A major growth driver is the expansion of contract manufacturing organizations supporting global pharmaceutical supply chains. Several pharmaceutical companies are investing in new sterile fill-finish facilities equipped with advanced aseptic packaging systems. Demand for prefilled syringes and sterile flexible packaging has also increased significantly due to rising chronic disease treatment volumes. Canada is witnessing steady growth in biotech manufacturing and sterile packaging innovation, contributing to regional market development.

Europe

Europe represented 27.6% of the global market in 2025 and is projected to expand at a CAGR of 6.2% through 2034. The region benefits from stringent pharmaceutical safety regulations, strong healthcare infrastructure, and rising demand for biologics manufacturing. Countries such as Germany, France, Switzerland, and the UK are major centers for pharmaceutical production and sterile packaging innovation. Increasing investments in sustainable aseptic packaging materials are further supporting market growth. European pharmaceutical companies are adopting recyclable sterile packaging solutions to align with regional environmental regulations and circular economy initiatives.

Germany is the dominant country in the European market due to its advanced pharmaceutical manufacturing ecosystem and strong exports of sterile healthcare products. A key regional growth driver is the increasing adoption of sustainable sterile packaging technologies. Several packaging companies are introducing lightweight aseptic barrier materials to reduce environmental impact while maintaining sterility performance. Growth in biologics production facilities and expansion of vaccine manufacturing infrastructure continue to support aseptic packaging demand across the region.

Asia Pacific

Asia Pacific held 24.9% of the global packaging for aseptic manufacturing market share in 2025 and is expected to register the fastest CAGR of 7.6% during the forecast period. Rapid pharmaceutical manufacturing expansion, increasing healthcare investments, and growing biologics production are major growth contributors. Countries such as China, India, Japan, and South Korea are investing heavily in sterile manufacturing capabilities to support domestic healthcare demand and pharmaceutical exports. Rising contract manufacturing activities and lower production costs are attracting multinational pharmaceutical companies to the region.

China dominates the regional market due to large-scale pharmaceutical production and rapid healthcare infrastructure expansion. A major growth driver is government support for domestic biologics manufacturing and vaccine development. Chinese pharmaceutical manufacturers are increasing investments in advanced sterile packaging systems to meet international regulatory standards. India is also emerging as a significant market due to rapid expansion of injectable drug production and growing pharmaceutical exports to North America and Europe.

Middle East & Africa

The Middle East & Africa market accounted for 6.1% of the global share in 2025 and is projected to grow at a CAGR of 5.8% during the forecast period. The region is witnessing gradual expansion in pharmaceutical manufacturing infrastructure and healthcare investments. Governments are increasing investments in domestic drug production to reduce dependency on imports, supporting demand for sterile packaging technologies. Rising demand for packaged nutritional products and sterile healthcare supplies is also contributing to market growth.

Saudi Arabia remains the dominant market within the region due to increasing pharmaceutical manufacturing investments and healthcare modernization initiatives. A unique growth driver is the expansion of regional vaccine production facilities aimed at improving healthcare security. The UAE is also investing in advanced healthcare manufacturing infrastructure, encouraging adoption of contamination-resistant packaging systems. Growing urbanization and rising healthcare expenditure are expected to support long-term regional growth.

Latin America

Latin America accounted for 6.6% of the global market share in 2025 and is anticipated to expand at a CAGR of 6.9% through 2034. Growth is supported by increasing pharmaceutical production, rising healthcare awareness, and expanding food processing industries. Countries including Brazil, Mexico, and Argentina are witnessing greater demand for sterile packaging systems used in injectable drugs and aseptic beverages. Improvements in healthcare infrastructure and retail distribution are also supporting market expansion.

Brazil dominates the regional market due to strong pharmaceutical manufacturing activity and increasing domestic healthcare investments. A key growth driver is the rising production of shelf-stable dairy and nutritional beverages using aseptic packaging systems. Regional food manufacturers are investing in advanced aseptic filling technologies to improve product shelf life and distribution efficiency. Mexico is also emerging as a growing pharmaceutical export hub, creating additional opportunities for sterile packaging suppliers.

Competitive Landscape

The packaging for aseptic manufacturing market is moderately consolidated, with leading companies focusing on sterile packaging innovation, strategic acquisitions, and expansion of pharmaceutical packaging capacity. Major players are investing in advanced barrier materials, recyclable sterile packaging systems, and automated aseptic filling technologies to strengthen market positioning.

Amcor plc remains one of the leading companies in the market due to its broad portfolio of pharmaceutical sterile packaging products and strong global manufacturing presence. The company continues to expand its healthcare packaging business through sustainable material innovation and strategic collaborations with pharmaceutical manufacturers. Berry Global Group is focusing on medical-grade polymer packaging and single-use sterile systems to support biologics manufacturing growth. Schott AG and Gerresheimer AG are investing in high-performance glass packaging solutions for injectable drugs and vaccines.

Companies are also increasing investments in Asia Pacific to capitalize on pharmaceutical manufacturing expansion. Strategic partnerships between packaging suppliers and biotechnology firms are becoming increasingly common as demand for customized aseptic packaging solutions rises globally.

Key Players List

- Amcor plc

- Berry Global Group, Inc.

- Schott AG

- Gerresheimer AG

- West Pharmaceutical Services, Inc.

- AptarGroup, Inc.

- Sealed Air Corporation

- DuPont de Nemours, Inc.

- Becton, Dickinson and Company

- Catalent, Inc.

- SGD Pharma

- Stevanato Group

- Nipro Corporation

- DWK Life Sciences

- Nelipak Healthcare Packaging