Packaging Coatings Market Size and Growth

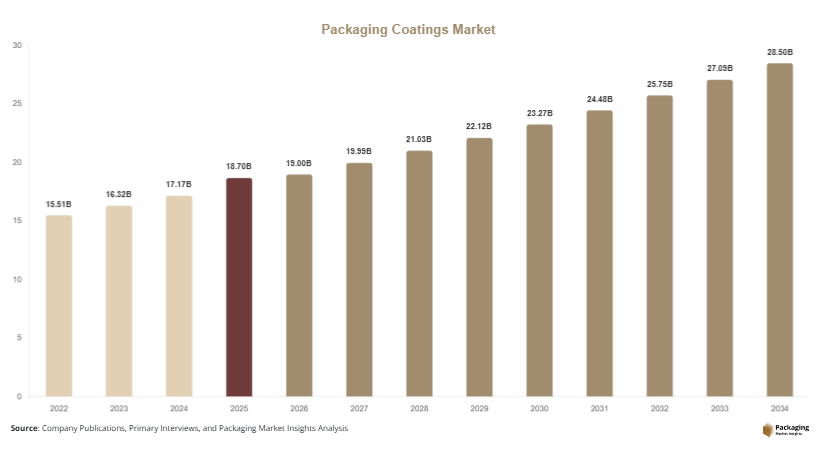

The global packaging coatings market was valued at USD 18.7 billion in 2025 and is estimated to reach USD 19.6 billion in 2026. The market is projected to reach USD 30.9 billion by 2034, expanding at a CAGR of 5.2% during the forecast period from 2025 to 2034. The market is witnessing consistent growth due to rising demand for packaged food and beverages, increasing pharmaceutical packaging production, and expanding use of sustainable coating technologies across flexible and rigid packaging industries. Packaging coatings are widely used to enhance durability, corrosion resistance, moisture protection, printability, and chemical stability in metal cans, plastic containers, cartons, and flexible packaging materials.

The rapid expansion of the food processing and beverage industries continues to support demand for advanced packaging coatings. Manufacturers are increasingly using barrier coatings to preserve product freshness and extend shelf life. Growing urbanization and changing consumer lifestyles have accelerated demand for ready-to-eat meals, canned foods, and packaged beverages, directly increasing coating consumption in metal and plastic packaging applications. In addition, rising healthcare spending and pharmaceutical manufacturing activities are creating demand for specialty coatings used in medical and drug packaging.

Key Market Insights

- Asia Pacific dominated the market with a 38.7% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.3%.

- Epoxy coatings led the type segment with a 34.8% share.

- Metal packaging substrates dominated with a 49.2% share.

- Food & beverage applications led the end-use segment with 51.4% share.

- The US remained the dominant country in North America with a market size of USD 3.9 billion in 2025 and USD 4.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of BPA-Free and Sustainable Coatings

The packaging coatings market is experiencing a strong shift toward BPA-free and environmentally sustainable coating technologies. Regulatory authorities and consumer advocacy groups have raised concerns regarding the use of traditional epoxy coatings containing bisphenol-A in food and beverage packaging. As a result, packaging manufacturers are increasingly adopting water-based acrylic coatings, polyester coatings, and bio-based alternatives that comply with food safety and environmental regulations.

Several beverage can manufacturers in Europe and North America have introduced BPA-free internal coatings to improve consumer confidence and meet evolving compliance requirements. Food packaging companies are also investing in low-VOC and recyclable coating systems to support sustainability goals. This transition is expected to encourage innovation in coating chemistry and expand commercial adoption of renewable raw materials.

Over the forecast period, sustainable coatings are likely to become a major competitive factor for packaging suppliers and consumer brands. Manufacturers investing in eco-friendly product portfolios may strengthen long-term market positioning while reducing regulatory risks and environmental impact.

Rising Demand for High-Performance Barrier Coatings

The market is witnessing growing demand for high-performance barrier coatings that improve packaging protection and shelf-life stability. Barrier coatings are increasingly used to protect packaged food, pharmaceuticals, and beverages from moisture, oxygen, UV radiation, and chemical contamination. The growth of e-commerce and global supply chains has further increased the need for durable coating technologies capable of maintaining packaging integrity during transportation.

For example, flexible food packaging manufacturers are introducing multilayer barrier coatings that enhance product freshness while reducing material thickness. Beverage packaging companies are also using corrosion-resistant internal coatings to maintain product quality in metal cans and containers. Pharmaceutical packaging producers increasingly require specialty coatings with antimicrobial and chemical-resistant properties.

Future demand is expected to rise as packaging companies focus on lightweight packaging systems that require advanced coating performance. Technological developments in nano-coatings and smart coatings may further improve product safety, traceability, and packaging efficiency across multiple industries.

Market Drivers

Expansion of Packaged Food and Beverage Consumption

The increasing consumption of packaged food and beverages is a major driver supporting the packaging coatings market. Rapid urbanization, rising disposable incomes, and changing consumer lifestyles have increased demand for ready-to-eat meals, bottled beverages, canned products, and convenience foods. Packaging coatings play a critical role in maintaining food quality, preventing contamination, and extending shelf life across these applications.

Food and beverage manufacturers require coatings that provide moisture resistance, flavor protection, and corrosion prevention for metal and plastic packaging materials. Beverage cans, food containers, and flexible pouches increasingly depend on advanced coatings to preserve product integrity during storage and transportation. Rising demand for premium packaged foods has also encouraged adoption of decorative and printable coating technologies.

For instance, canned beverage production in Asia Pacific and North America has increased significantly due to growing consumption of energy drinks, carbonated beverages, and ready-to-drink coffee products. This trend continues to strengthen demand for internal can coatings and external protective finishes across global packaging operations.

Growth in Pharmaceutical and Healthcare Packaging

The expansion of pharmaceutical manufacturing and healthcare packaging industries is another key driver for the packaging coatings market. Pharmaceutical packaging requires highly specialized coatings that ensure chemical resistance, contamination prevention, and product stability. Increasing healthcare spending and rising production of medicines, vaccines, and medical devices are contributing to higher coating demand globally.

Coatings used in pharmaceutical packaging applications must comply with strict safety and regulatory standards. Blister packs, medical containers, aluminum foils, and drug storage systems increasingly rely on high-performance coatings to protect sensitive products from moisture, oxygen, and light exposure. The rise of biologics and specialty medicines has further increased the importance of advanced barrier coating technologies.

Countries such as the United States, Germany, India, and China are witnessing substantial growth in pharmaceutical packaging investments. Several healthcare packaging companies are expanding production facilities and adopting antimicrobial coatings to improve product safety and packaging performance across medical applications.

Market Restraint

Stringent Environmental Regulations and Raw Material Volatility

Stringent environmental regulations regarding chemical usage and emissions remain a significant restraint for the packaging coatings market. Governments across North America and Europe have introduced strict compliance requirements related to VOC emissions, hazardous substances, and food-contact materials. Packaging coating manufacturers are under pressure to reformulate products using safer and environmentally compliant ingredients, which can increase production costs and research expenditures.

Raw material price volatility further impacts market profitability. Key coating ingredients such as resins, solvents, pigments, and specialty additives are heavily influenced by fluctuations in crude oil prices and global chemical supply chains. Rising energy costs and transportation expenses have also increased operational challenges for coating manufacturers.

For example, restrictions on BPA-containing epoxy coatings in food packaging have forced several companies to invest heavily in alternative coating technologies. Smaller manufacturers often face difficulties adapting to evolving regulatory standards due to limited financial resources. In addition, disruptions in global chemical supply chains may lead to shortages of specialty raw materials, affecting production efficiency and pricing stability across the market.

Environmental concerns regarding recycling compatibility and disposal of coated packaging materials may also slow adoption in certain applications. These factors continue to create operational and financial challenges for coating suppliers worldwide.

Market Opportunities

Rising Demand for Water-Based and Bio-Based Coatings

The increasing adoption of water-based and bio-based coating technologies presents significant growth opportunities for the packaging coatings market. Sustainability goals and environmental regulations are encouraging packaging manufacturers to reduce dependence on solvent-based coatings with high VOC emissions. Water-based coatings offer improved environmental performance while maintaining strong adhesion, printability, and barrier properties.

Food and beverage packaging companies are increasingly using bio-based coatings derived from renewable raw materials to improve recyclability and reduce carbon footprints. Paper-based packaging applications are particularly benefiting from these technologies as retailers and consumer brands focus on eco-friendly packaging alternatives.

Several coating manufacturers are investing in research and development to improve the durability and chemical resistance of sustainable coating systems. Future opportunities are expected in compostable food packaging, recyclable flexible packaging, and renewable barrier coatings for e-commerce packaging solutions.

Expansion of Smart and Functional Packaging Technologies

The growth of smart and functional packaging technologies is creating new opportunities for coating manufacturers. Advanced coatings capable of providing antimicrobial protection, temperature resistance, anti-counterfeit features, and digital printing compatibility are gaining importance across food, pharmaceutical, and consumer goods packaging applications.

Smart coatings integrated with freshness indicators and QR-enabled traceability systems are increasingly used in premium packaging products. E-commerce expansion has also increased demand for scratch-resistant and impact-resistant coatings designed for transportation durability.

For example, pharmaceutical packaging companies are developing antimicrobial coatings that help reduce contamination risks during product handling and storage. Beverage manufacturers are also investing in heat-resistant coatings for metal cans used in energy drinks and alcoholic beverages. As smart packaging adoption expands globally, coating suppliers with advanced functional technologies are expected to benefit from strong long-term demand.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.7 Billion |

| Market Size in 2026 | USD 19. Billion |

| Market Size in 2034 | USD 30.9 Billion |

| CAGR | 5.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Epoxy coatings dominated the packaging coatings market in 2024 with a market share of 34.8%. These coatings are widely used in metal food cans, beverage containers, industrial packaging, and pharmaceutical packaging applications due to their strong adhesion, corrosion resistance, and chemical protection properties. Epoxy coatings help prevent contamination and maintain product stability in food and beverage packaging exposed to acidic or moisture-rich contents. Beverage manufacturers continue using epoxy-based internal can coatings because of their durability and compatibility with high-speed production systems. Industrial packaging applications also rely on epoxy coatings for protecting chemical containers and metal drums against corrosion. The widespread availability of epoxy resin technologies and established manufacturing infrastructure across North America, Europe, and Asia Pacific further supports segment dominance. Several packaging companies continue investing in BPA-free epoxy variants to maintain regulatory compliance while preserving packaging performance standards.

Acrylic coatings are projected to register the fastest CAGR of 6.5% during the forecast period due to increasing demand for environmentally friendly and water-based coating solutions. Acrylic coatings offer strong printability, UV resistance, and flexibility, making them suitable for paper packaging, flexible packaging, and decorative consumer goods applications. Growth is particularly strong in food packaging and retail packaging segments where sustainability and visual appeal are becoming more important purchasing factors. Several packaging manufacturers are adopting acrylic coatings because they contain lower VOC emissions compared to solvent-based alternatives. The rise of recyclable paper packaging and eco-friendly beverage cartons is also contributing to higher acrylic coating demand. Future growth opportunities are expected in bio-based acrylic formulations and digital printing-compatible coatings designed for premium branded packaging applications across global retail industries.

By Material

Metal packaging substrates accounted for the largest market share of 49.2% in 2024 due to extensive use of coatings in aluminum cans, steel food containers, aerosol cans, and industrial drums. Metal packaging requires advanced coatings to prevent corrosion, maintain food safety, and improve product durability during transportation and storage. Beverage companies remain major consumers of coated aluminum cans because of increasing demand for carbonated drinks, beer, and ready-to-drink beverages. Food processing companies also depend on coated steel containers for canned vegetables, soups, sauces, and pet food products. The expansion of recyclable metal packaging initiatives in Europe and North America has further strengthened demand for sustainable coating technologies compatible with aluminum and steel recycling systems. Manufacturers continue developing lightweight metal packaging solutions integrated with advanced barrier coatings to improve performance and reduce production costs.

Paper-based substrates are expected to witness the fastest CAGR of 6.1% through 2034 due to increasing demand for sustainable and recyclable packaging materials. Retailers, foodservice providers, and consumer goods companies are increasingly replacing plastic packaging with coated paper packaging solutions to reduce environmental impact. Water-based coatings and bio-based barrier coatings are becoming essential for paper cups, cartons, takeaway food containers, and e-commerce packaging applications. Several global brands are introducing coated paper packaging capable of providing grease resistance, moisture protection, and improved printability without affecting recyclability. The rapid expansion of online retailing and environmentally conscious consumer behavior is expected to support long-term growth in this segment. Future innovation is likely to focus on compostable barrier coatings and renewable fiber-based packaging technologies.

By End-Use

Food & beverage applications dominated the packaging coatings market in 2024 with a market share of 51.4%. Rising consumption of packaged foods, canned beverages, dairy products, sauces, snacks, and ready-to-eat meals continues to support strong coating demand across this segment. Packaging coatings help maintain food quality, extend shelf life, and improve resistance against moisture, oxygen, and contamination. Beverage manufacturers heavily depend on internal can coatings and external decorative coatings to ensure packaging durability and branding performance. Flexible food packaging applications also increasingly use high-barrier coatings to preserve freshness and reduce food waste. The growth of organized retail chains, convenience food consumption, and online grocery delivery services has further accelerated demand for advanced packaging coating technologies globally. Emerging economies in Asia Pacific and Latin America continue to experience strong growth in packaged food production, strengthening the segment’s dominant market position.

Pharmaceutical packaging is expected to register the fastest CAGR of 6.4% during the forecast period due to rising healthcare spending, increasing medicine production, and growing demand for specialty drug packaging. Pharmaceutical products require highly protective coatings capable of preventing contamination, moisture penetration, and chemical interaction. Blister packs, aluminum foils, medicine bottles, and sterile packaging systems increasingly depend on advanced barrier coatings to maintain product safety and stability. The expansion of biologics, vaccines, and temperature-sensitive medicines is further supporting demand for antimicrobial and chemical-resistant coatings. Pharmaceutical packaging manufacturers are also investing in smart coatings compatible with anti-counterfeit technologies and digital traceability systems. Future growth opportunities are expected in sustainable medical packaging coatings and recyclable pharmaceutical packaging materials designed to meet stricter environmental regulations.

Packaging Coatings Market Segmentations

By Type

- Epoxy Coatings

- Acrylic Coatings

- Polyester Coatings

- Polyurethane Coatings

- Fluoropolymer Coatings

By Material

- Metal Packaging

- Plastic Packaging

- Paper & Paperboard Packaging

- Glass Packaging

- Flexible Packaging

By End-User

- Food & Beverage

- Pharmaceutical Packaging

- Personal Care & Cosmetics

- Household Products

- Industrial Packaging

Regional Analysis

North America

North America accounted for 24.8% of the global packaging coatings market share in 2025 and is projected to expand at a CAGR of 4.8% through 2034. The region benefits from strong packaged food consumption, advanced pharmaceutical manufacturing, and increasing adoption of sustainable packaging technologies. Rising demand for canned beverages, frozen foods, and ready-to-eat meals has accelerated the use of protective and barrier coatings across metal and flexible packaging applications. In addition, the expansion of e-commerce retailing has strengthened demand for scratch-resistant and moisture-resistant coatings used in transportation packaging. Regulatory support for BPA-free and low-VOC coatings is also encouraging innovation among regional coating manufacturers.

The United States remained the dominant country in the regional market due to high production volumes in beverage cans, pharmaceutical packaging, and consumer goods industries. A key growth driver is the increasing investment in recyclable aluminum packaging and sustainable food containers. Several U.S. packaging companies are expanding water-based coating production facilities to meet evolving environmental compliance standards. The rise of premium beverage brands and specialty packaged foods has also increased demand for decorative and printable coatings. Canada is additionally witnessing growth in healthcare packaging and sustainable paper-based food packaging applications supported by rising environmental awareness and retail modernization trends.

Europe

Europe represented 22.1% of the global packaging coatings market in 2025 and is expected to register a CAGR of 5.0% during the forecast period. The region continues to experience strong demand for eco-friendly packaging solutions driven by circular economy initiatives and strict environmental regulations. Packaging manufacturers across Germany, France, Italy, and the Nordic countries are increasingly adopting water-based and recyclable coating technologies. Rising consumption of packaged organic foods and premium beverages has supported demand for specialty barrier coatings with food-safe properties. In addition, pharmaceutical packaging production remains an important contributor to market expansion across Western Europe.

Germany emerged as the leading market within Europe due to its large food processing, automotive lubricant packaging, and pharmaceutical industries. One important growth driver is the increasing use of recyclable metal cans and coated paper packaging in beverage applications. German coating manufacturers are investing in BPA-free internal can coatings and UV-curable technologies designed for high-speed packaging operations. France is also witnessing rising demand for sustainable cosmetic packaging coatings, while Italy continues expanding decorative coatings used in luxury food packaging. The United Kingdom is increasingly focusing on digital printing-compatible coatings for premium retail packaging and branded consumer products.

Asia Pacific

Asia Pacific dominated the packaging coatings market with a 38.7% share in 2025 and is forecast to grow at a CAGR of 5.9% through 2034. Rapid urbanization, industrialization, and retail sector expansion continue to drive demand for coated packaging materials across the region. The growth of packaged food, beverages, pharmaceuticals, and personal care products has accelerated consumption of metal cans, flexible packaging, cartons, and plastic containers requiring protective coatings. Increasing investments in local packaging manufacturing facilities and rising exports of processed food products are also supporting regional market expansion.

China remained the dominant country in Asia Pacific due to large-scale food processing operations and strong manufacturing output. One major growth driver is the rapid expansion of beverage can production linked to rising consumption of ready-to-drink products and energy beverages. Chinese coating manufacturers are increasingly introducing low-VOC and water-based packaging coatings to comply with environmental standards and export regulations. India is also experiencing significant growth supported by pharmaceutical packaging expansion and rising packaged food demand in urban areas. Southeast Asian economies such as Vietnam, Thailand, and Indonesia are witnessing growing investments in flexible packaging and coated paper packaging technologies.

Middle East & Africa

The Middle East & Africa accounted for 7.3% of the global packaging coatings market share in 2025 and is projected to expand at a CAGR of 5.1% during the study period. Growth in the region is supported by increasing packaged food imports, retail sector modernization, and rising beverage consumption. Gulf countries are witnessing strong demand for coated metal cans and flexible packaging used in food and beverage applications. Industrial development and pharmaceutical sector investments are also contributing to coating demand across healthcare and chemical packaging industries.

Saudi Arabia remained the dominant market in the region due to expanding food processing industries and growing investments in domestic manufacturing capabilities. A unique growth driver is the increasing demand for temperature-resistant packaging coatings used in harsh climatic conditions. Beverage manufacturers in the country are increasingly using high-performance coatings to improve product stability during transportation and storage. The United Arab Emirates is also witnessing rising demand for premium packaging coatings in cosmetics and luxury consumer goods applications. South Africa continues to support regional growth through expanding pharmaceutical packaging production and retail packaging demand.

Latin America

Latin America held 7.1% of the global packaging coatings market share in 2025 and is anticipated to register the fastest CAGR of 6.3% during the forecast period. The market is benefiting from increasing packaged food consumption, expanding beverage production, and rising urban populations across Brazil, Mexico, Argentina, and Colombia. Demand for coated flexible packaging and metal cans has increased significantly due to the growth of retail supermarkets and convenience food products. Packaging manufacturers are also investing in cost-efficient coating systems to improve durability and shelf-life performance across export-oriented food industries.

Brazil emerged as the dominant market in Latin America due to strong beverage can production and packaged food manufacturing activities. One important growth driver is the rapid expansion of aluminum can recycling programs supporting sustainable beverage packaging growth. Brazilian coating suppliers are increasingly adopting water-based and BPA-free technologies to align with environmental standards and consumer preferences. Mexico is also witnessing rising demand for coated pharmaceutical packaging linked to healthcare industry expansion and export growth. Regional manufacturers continue investing in decorative coatings and high-barrier technologies designed for food preservation and transportation efficiency.

Competitive Landscape

The packaging coatings market is moderately consolidated with global chemical manufacturers and specialty coating suppliers competing across food packaging, beverage packaging, pharmaceutical packaging, and industrial packaging applications. Companies are focusing on sustainable product development, acquisitions, capacity expansion, and advanced coating technologies to strengthen market presence.

PPG Industries is considered one of the leading players due to its broad packaging coatings portfolio and strong global manufacturing network. The company continues investing in BPA-free coatings, water-based technologies, and food-safe packaging solutions designed for beverage cans and food containers.

Akzo Nobel N.V. has expanded its sustainable coatings business through investments in low-VOC and recyclable coating systems. Sherwin-Williams Company focuses on advanced metal packaging coatings and industrial protective solutions for food and beverage packaging manufacturers. Axalta Coating Systems is strengthening its specialty coatings segment through innovation in flexible packaging and pharmaceutical packaging applications. BASF SE continues investing in bio-based coating materials and high-performance barrier technologies.

Manufacturers are increasingly collaborating with packaging companies and food producers to develop recyclable, lightweight, and digitally printable coating systems. Investments in automation, smart coatings, and renewable raw materials are expected to remain major competitive strategies through the forecast period.

Key Players List

- PPG Industries

- Akzo Nobel N.V.

- Sherwin-Williams Company

- Axalta Coating Systems

- BASF SE

- Nippon Paint Holdings

- RPM International

- Valspar Corporation

- Kansai Paint Co., Ltd.

- ALTANA AG

- Jotun Group

- Henkel AG & Co. KGaA

- TIGER Coatings GmbH & Co. KG

- Siegwerk Druckfarben AG & Co. KGaA

- Dow Inc.