Packaging 5.0 Market Size and Growth

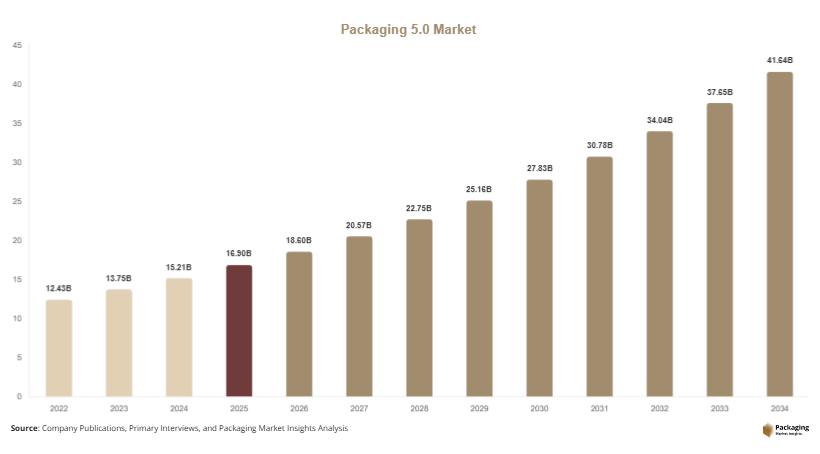

The global packaging 5.0 market size is estimated at USD 16.9 billion in 2025, and it is projected to reach USD 18.6 billion in 2026. By 2034, the market is expected to expand to approximately USD 41.5 billion, growing at a CAGR of 10.6% during 2025–2034. This growth is strongly supported by AI-driven manufacturing systems, increasing demand for hyper-personalized packaging experiences, and global sustainability transformation initiatives.

A key growth factor is the integration of AI-powered autonomous packaging systems into industrial supply chains. These systems enable real-time decision-making across packaging design, material selection, and logistics optimization. Another major driver is rising consumer demand for interactive packaging experiences, where QR codes, NFC tags, AR interfaces, and sensor-based communication transform packaging into a digital engagement platform. A third important factor is regulatory pressure for sustainable and traceable packaging systems, especially in Europe and North America, where environmental compliance frameworks are becoming stricter.

Key Highlights

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Cognitive smart packaging led with a 32.4% share.

- Hybrid intelligent materials dominated with a 51.5% share.

- Food & beverage led with 43.5% share.

- The US remained dominant with USD 4.3 billion in 2025 and USD 4.7 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Emotional AI-Driven Packaging Interfaces

Packaging 5.0 is increasingly shifting toward emotionally intelligent packaging systems capable of adapting content based on consumer behavior, interaction patterns, and environmental context. These systems use AI, behavioral analytics, and biometric signals to modify packaging experiences in real time. For example, beverage and cosmetic companies in Japan and South Korea are deploying AR-enabled packaging that changes storytelling content based on user engagement level. In retail environments, smart packaging is being used to analyze consumer attention and dynamically adjust promotional messaging. This trend is redefining packaging as a digital communication interface rather than a static physical product. Over time, emotional AI packaging is expected to become a key driver of brand differentiation and customer engagement strategies.

Autonomous Self-Optimizing Packaging Ecosystems

Another major trend is the emergence of fully autonomous packaging ecosystems where AI, robotics, and IoT systems work together without human intervention. These systems dynamically adjust packaging size, labeling, material selection, and logistics routing based on real-time demand data. In Germany and the US, logistics hubs are deploying autonomous packaging lines that integrate directly with warehouse management systems and predictive analytics engines. For example, e-commerce fulfillment centers now automatically resize packaging based on product weight and destination, reducing waste and improving efficiency. This trend is expected to reshape global supply chain architecture by enabling self-learning packaging environments.

Market Drivers

Expansion of Smart Manufacturing Ecosystems

The rise of smart manufacturing ecosystems is a key driver for Packaging 5.0 adoption. Industries are increasingly integrating AI, robotics, and IoT into unified production systems where packaging becomes an intelligent node within the supply chain. In China, South Korea, and the United States, smart factories are enabling real-time synchronization between production output and packaging systems. This allows packaging lines to automatically adjust configurations based on production speed and demand fluctuations. The result is reduced operational inefficiency, lower material waste, and improved scalability across global manufacturing networks.

Rising Demand for Supply Chain Transparency

Another major driver is the increasing need for end-to-end supply chain transparency. Companies are under pressure to track goods from production to final delivery with real-time visibility. Packaging 5.0 enables this through embedded sensors, RFID, blockchain integration, and IoT connectivity. In the pharmaceutical sector, smart packaging is used to monitor temperature-sensitive drugs across international logistics routes. In food supply chains, packaging systems ensure traceability from farm to retail shelf. This transparency improves regulatory compliance, reduces fraud, and enhances consumer trust.

Market Restraint

High System Complexity and Capital Requirements

Despite strong growth, Packaging 5.0 adoption is constrained by high system complexity and significant capital requirements. The technology demands integration of AI platforms, sensor networks, robotics, and cloud-based analytics systems, which require substantial investment. Small and mid-sized manufacturers face challenges in upgrading legacy systems to support intelligent packaging infrastructure. Additionally, cybersecurity risks increase due to high connectivity across packaging ecosystems. These challenges slow down full-scale adoption, particularly in developing economies where digital infrastructure is still evolving.

Market Opportunities

AI-Based Hyper-Personalized Packaging

A major opportunity lies in AI-based hyper-personalized packaging systems that deliver customized consumer experiences at scale. These systems analyze customer data, preferences, and behavioral patterns to generate personalized packaging content in real time. For example, FMCG companies are developing packaging that changes digital content based on individual consumer profiles. This enables targeted marketing, improved engagement, and stronger brand loyalty. Over time, hyper-personalization will become a standard feature in premium consumer goods packaging.

Smart Healthcare Packaging Integration

Healthcare represents a significant growth opportunity for Packaging 5.0 technologies. Intelligent packaging systems are being integrated into digital healthcare ecosystems to monitor medication adherence, track drug authenticity, and support patient monitoring. In the United States and Europe, smart pill packaging is being used to alert patients and healthcare providers when doses are missed. This improves treatment outcomes and reduces healthcare risks. Future applications include integration with telemedicine platforms and AI-driven diagnostic systems.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 16.9 Billion |

| Market Size in 2026 | USD 18.6 Billion |

| Market Size in 2034 | USD 41.5 Billion |

| CAGR | 10.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Technology

Cognitive smart packaging held 32.4% share in 2024, driven by its ability to integrate AI, sensors, and adaptive intelligence into packaging systems across FMCG, pharmaceutical, and electronics industries. This segment enables real-time monitoring of environmental conditions, product integrity, and consumer interaction behavior. In pharmaceuticals, cognitive packaging ensures drug safety by tracking temperature and humidity during transportation. In FMCG, it enables dynamic consumer engagement through smart labeling and interactive packaging content. The segment is widely adopted in North America and Europe due to advanced digital infrastructure and regulatory compliance requirements.

Adaptive AI packaging is the fastest-growing segment with 11.8% CAGR, driven by increasing demand for autonomous decision-making systems in packaging operations. This technology enables packaging systems to self-adjust based on predictive analytics, reducing human intervention. In Asia Pacific, especially China and South Korea, adaptive AI packaging is being deployed in high-volume manufacturing environments where production speed and customization are critical. The future of this segment lies in fully autonomous packaging ecosystems where machines continuously learn and optimize packaging processes based on real-time supply chain data, significantly improving efficiency and reducing waste across industries.

By Material

Hybrid intelligent materials dominated with 51.5% share in 2024, due to their ability to combine structural durability with embedded intelligence features such as sensors, RFID tags, and digital interfaces. These materials are widely used in electronics, automotive, and healthcare packaging systems where both strength and smart functionality are required. In Europe, hybrid materials are extensively used in regulated industries requiring traceability and sustainability compliance.

Bio-digital packaging is the fastest-growing segment with 10.4% CAGR, driven by sustainability trends and demand for eco-friendly intelligent materials. These materials combine biodegradable components with digital intelligence systems, enabling environmentally sustainable packaging solutions without compromising functionality. In North America and Europe, regulatory pressure is accelerating adoption of bio-digital systems, while Asia Pacific is scaling production due to cost-efficient manufacturing capabilities. Future development will focus on mass adoption of bio-integrated intelligent materials across global FMCG and healthcare supply chains.

By End-Use

Food & beverage led the market with 43.5% share in 2024, driven by demand for freshness monitoring, traceability, and consumer personalization. This segment heavily relies on intelligent packaging systems for supply chain optimization and brand engagement. In Asia Pacific, food packaging is increasingly integrated with digital tracking systems for export logistics.

Healthcare is the fastest-growing segment with 11.0% CAGR, driven by digital healthcare transformation, medication adherence systems, and anti-counterfeiting requirements. In North America and Europe, smart pharmaceutical packaging is becoming essential for regulatory compliance and patient safety. Future applications include integration with telemedicine platforms and AI-driven health monitoring systems.

Packaging 5.0 Market Segmentations

By Technology Type

- Cognitive Smart Packaging

- Adaptive AI Packaging Systems

- IoT-Enabled Connected Packaging

- AR/VR Interactive Packaging Interfaces

- Autonomous Self-Optimizing Packaging Lines

By Material Type

- Hybrid Intelligent Materials

- Bio-Digital Packaging Materials

- Smart Plastic Polymers

- Sensor-Embedded Paper & Paperboard

- Recyclable Electronic Packaging Substrates

By End-Use Industry

- Food & Beverage

- Pharmaceuticals & Healthcare

- Electronics & Semiconductors

- Logistics & E-commerce

- Industrial Manufacturing

Regional Analysis

North America

North America accounted for 31.9% share of the packaging 5.0 market in 2025, expanding at a CAGR of 9.9% through 2034. The region represents one of the most advanced ecosystems for intelligent packaging adoption due to strong digital infrastructure, AI integration maturity, and high penetration of automated manufacturing systems. The United States, Canada, and Mexico collectively form a diversified demand structure where each economy contributes differently to Packaging 5.0 expansion. The US dominates high-value cognitive packaging deployment in pharmaceuticals, FMCG, and e-commerce logistics, while Canada emphasizes sustainable smart packaging systems, and Mexico is emerging as a cost-efficient manufacturing-linked packaging hub for export-oriented industries.

In the United States, Packaging 5.0 adoption is driven by AI-powered fulfillment automation systems in large-scale logistics centers. These systems dynamically adjust packaging size, labeling, and material selection based on real-time demand forecasting models. For example, major US e-commerce players operate fully automated packaging hubs where machine learning algorithms determine optimal packaging configurations per shipment in milliseconds. Canada’s growth is influenced by regulatory pressure on sustainable packaging materials and strong adoption of bio-based smart packaging in food retail supply chains. Mexico, on the other hand, is increasingly integrated into North American manufacturing supply chains, where automotive and electronics exports require standardized intelligent packaging systems for cross-border logistics optimization. The region’s growth is further strengthened by integration of digital twin systems, IoT-enabled warehouse ecosystems, and predictive supply chain analytics that collectively transform packaging from a static function into a real-time decision-making layer within industrial operations.

Europe

Europe held 28.6% share in 2025, growing at a CAGR of 10.7%, driven by regulatory enforcement, sustainability mandates, and advanced industrial automation ecosystems. The region demonstrates a structurally balanced demand landscape across Germany, France, Italy, and the United Kingdom, each contributing uniquely to Packaging 5.0 development. Germany leads in industrial cyber-physical packaging systems, France drives luxury and cosmetic packaging innovation, Italy contributes high-end design-centric packaging manufacturing, and the UK focuses on digital retail and e-commerce packaging transformation.

Germany remains the core innovation hub where Packaging 5.0 is integrated into Industry 4.0/5.0 hybrid production systems. Smart factories deploy AI-controlled packaging lines that continuously self-optimize based on supply chain data inputs. France’s luxury goods sector utilizes emotionally intelligent packaging systems that enhance consumer experience through interactive digital storytelling embedded into packaging surfaces. Italy plays a critical role in high-end export packaging for fashion and automotive industries, where precision packaging design and sustainability compliance intersect. The UK is increasingly adopting Packaging 5.0 in retail logistics, particularly in omnichannel distribution systems where packaging is dynamically adjusted based on multi-channel demand signals. Additionally, Europe benefits from strong circular economy regulations, which are accelerating adoption of recyclable intelligent materials and digital traceability systems embedded into packaging ecosystems.

Asia Pacific

Asia Pacific dominated the market with 37.4% share in 2025, growing at a CAGR of 11.9%, making it the most dynamic global region for Packaging 5.0 expansion. The region’s dominance is driven by large-scale manufacturing ecosystems, rapid digital transformation, and government-backed smart factory initiatives. China, Japan, South Korea, and India collectively form the core innovation and production base, each with distinct industrial strengths. China leads in AI-driven industrial packaging automation, Japan specializes in robotics-integrated precision packaging, South Korea focuses on smart consumer packaging innovation, and India is rapidly scaling logistics automation for digital commerce ecosystems.

China’s Packaging 5.0 ecosystem is built around AI-enabled smart manufacturing clusters where packaging systems operate autonomously within fully digitized production environments. These systems are directly connected to national supply chain networks, enabling real-time synchronization between production output and packaging requirements. Japan’s advanced robotics industry supports ultra-precision packaging systems used in electronics and semiconductor exports, where micro-level accuracy is essential. South Korea is developing emotionally interactive packaging systems for consumer electronics and cosmetics, integrating AR and NFC technologies. India’s growth is primarily driven by the explosive expansion of e-commerce platforms, where AI-enabled packaging hubs manage high-volume, high-speed order fulfillment operations. The region also benefits from strong government support for industrial automation, export manufacturing competitiveness, and integration of IoT-based logistics systems across supply chains.

Middle East & Africa

MEA accounted for 3.7% share in 2025, growing at a CAGR of 9.5%, driven by infrastructure modernization, logistics expansion, and industrial diversification programs. The region is primarily led by the UAE, Saudi Arabia, and South Africa, each contributing through different structural drivers. The UAE focuses on AI-driven logistics automation and smart port infrastructure, Saudi Arabia is investing heavily in industrial transformation under Vision 2030, and South Africa is advancing retail and export packaging modernization.

The UAE has emerged as a regional logistics hub where Packaging 5.0 systems are integrated into airport and seaport operations, enabling real-time cargo tracking and automated packaging validation. Saudi Arabia is expanding smart manufacturing zones where packaging systems are integrated into industrial diversification strategies beyond oil dependency. South Africa is strengthening its agricultural export supply chains by adopting intelligent packaging systems that ensure product traceability and quality compliance for global markets. Additionally, the region is witnessing growing adoption of IoT-based logistics systems, especially in free trade zones and industrial clusters, enabling better coordination of packaging, storage, and distribution operations.

Latin America

Latin America held 5.4% share in 2025, growing at a CAGR of 11.1%, driven by e-commerce expansion, agricultural exports, and manufacturing integration with global supply chains. Brazil and Mexico dominate regional demand, while Argentina and Chile contribute selectively through food export and retail modernization.

Brazil leads due to its strong agricultural export ecosystem, where Packaging 5.0 systems are used to ensure freshness, traceability, and compliance with international standards. Mexico benefits from its integration with North American manufacturing supply chains, particularly in automotive and electronics exports requiring standardized intelligent packaging systems. Argentina and Chile are increasingly adopting smart packaging in food and beverage exports, where quality monitoring and logistics optimization are critical. The region is also witnessing rising adoption of AI-based logistics coordination systems that integrate packaging operations with port and customs management platforms.

Competitive Landscape

The packaging 5.0 market is highly competitive, with companies investing heavily in AI integration, autonomous systems, and sustainable packaging innovation. The competition is shifting from traditional packaging design to intelligent ecosystem development. Leading companies are focusing on digital twin integration, IoT-enabled packaging, and cognitive automation platforms.

Key Players List

- Sealed Air Corporation

- Amcor plc

- Tetra Pak

- Smurfit Kappa Group

- WestRock Company

- DS Smith Plc

- Mondi Group

- Avery Dennison Corporation

- Siemens AG

- Rockwell Automation

- Schneider Electric SE

- Honeywell International Inc.

- BASF SE

- SAP SE

- 3M Company