Packaging 4.0 Market Size and Growth

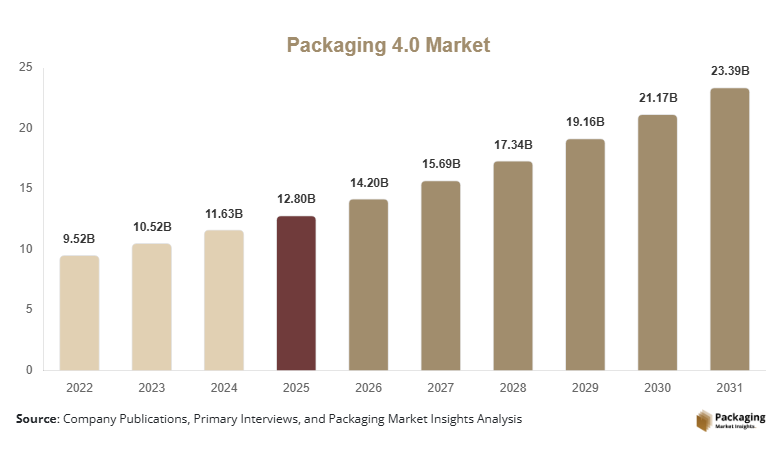

The global packaging 4.0 market size is estimated at USD 12.8 billion in 2025, and it is projected to reach USD 14.2 billion in 2026. By 2034, the market is expected to reach approximately USD 31.5 billion, expanding at a CAGR of 10.5% during 2025–2034. The shift toward smart manufacturing and Industry 4.0 adoption is transforming traditional packaging systems into data-driven, connected, and highly efficient ecosystems. The packaging 4.0 market is evolving rapidly as the packaging industry integrates digital technologies such as IoT, artificial intelligence, robotics, blockchain, and advanced automation systems into packaging operations.

One of the key growth factors is the increasing adoption of smart manufacturing across the packaging industry. Companies are integrating sensors, automation lines, and AI-based monitoring systems to improve production efficiency and reduce operational costs. Another important driver is the rising demand for supply chain transparency. Packaging 4.0 enables real-time tracking, traceability, and authentication of products using technologies such as RFID tags and blockchain integration. This is especially important in pharmaceuticals, food & beverage, and high-value consumer goods sectors.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Smart labeling systems led the technology segment with a 30.4% share.

- Plastic packaging integration dominated with a 52.3% share.

- Food & beverage applications led the segment with 43.1% share.

- The US remained the dominant country with a market size of USD 3.6 billion in 2025 and USD 4.0 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Integration of AI and Predictive Analytics in Packaging Operations

A major trend in the packaging 4.0 market is the integration of artificial intelligence and predictive analytics into packaging production systems. Manufacturers are increasingly using AI-driven systems to optimize production workflows, detect defects in real time, and forecast maintenance requirements. For example, large FMCG companies are deploying AI-enabled packaging lines that automatically adjust machine settings based on product type and demand fluctuations. This reduces downtime and improves production accuracy. In the future, AI is expected to play a central role in fully autonomous packaging ecosystems, where minimal human intervention is required.

Blockchain-Based Supply Chain Transparency in Packaging

Another important trend is the use of blockchain technology for supply chain transparency and product authentication. Packaging 4.0 solutions now integrate blockchain-based QR codes and RFID systems to track products from manufacturing to end-users. For example, pharmaceutical companies use blockchain-enabled packaging to verify drug authenticity and prevent counterfeiting. This improves consumer trust and regulatory compliance. In the coming years, blockchain adoption is expected to expand across food safety, luxury goods, and electronics packaging sectors, ensuring secure and transparent supply chains.

Market Drivers

Rising Adoption of Smart Manufacturing and Industry 4.0

The increasing adoption of Industry 4.0 technologies is a major driver of the packaging 4.0 market. Manufacturers are shifting toward fully automated and digitally connected production systems. Packaging lines are now equipped with IoT sensors, robotics, and cloud-based monitoring systems. For example, automotive and electronics manufacturers use smart packaging systems to synchronize production with real-time demand. This integration improves efficiency, reduces errors, and lowers operational costs, driving widespread adoption of Packaging 4.0 solutions.

Growth of E-commerce and Demand for Intelligent Packaging

The rapid expansion of e-commerce is another key driver. Online retail requires dynamic packaging systems capable of handling high order volumes and customized packaging requirements. Packaging 4.0 technologies enable automated sorting, real-time tracking, and adaptive labeling systems. For instance, global e-commerce companies use smart packaging solutions to optimize last-mile delivery and reduce packaging waste. This increasing reliance on digital logistics infrastructure is significantly boosting market growth.

Market Restraint

High Implementation Costs and Infrastructure Complexity

One of the major restraints in the packaging 4.0 market is the high cost of implementation and technological integration. Advanced systems such as AI-driven automation, IoT-enabled packaging lines, and blockchain infrastructure require significant capital investment. Small and medium-sized enterprises often struggle to adopt these technologies due to financial limitations. Additionally, integrating Packaging 4.0 systems into existing traditional manufacturing setups requires complex infrastructure upgrades and skilled workforce training. For example, many mid-sized food packaging companies in emerging economies face challenges in upgrading legacy systems, slowing down adoption rates. Cybersecurity risks associated with connected packaging systems also add to operational concerns.

Market Opportunities

Expansion of Smart Healthcare Packaging

The healthcare sector presents a significant opportunity for Packaging 4.0 solutions. Smart packaging systems can monitor temperature-sensitive pharmaceuticals, track medication usage, and prevent counterfeiting. For example, IoT-enabled blister packs are being used to track patient adherence to medication schedules. This improves healthcare outcomes and reduces waste. As the pharmaceutical industry continues to expand globally, demand for intelligent packaging solutions is expected to rise significantly.

Growth of Fully Automated Smart Factories

The development of fully automated smart factories offers another major opportunity. Packaging 4.0 systems can be fully integrated into robotic production lines, enabling end-to-end automation. For example, consumer goods manufacturers are deploying smart factories where packaging, labeling, and logistics are managed through centralized digital systems. This reduces labor dependency and increases efficiency. In the future, smart factories are expected to become the standard in high-volume manufacturing industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 12.8 Billion |

| Market Size in 2026 | USD 14.2 Billion |

| Market Size in 2034 | USD 31.5 Billion |

| CAGR | 10.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Technology

Smart labeling systems dominated the Packaging 4.0 market in 2024 with a 32.5% share, due to their widespread use in product tracking, branding, and consumer engagement. These systems are widely adopted in FMCG, retail, and pharmaceutical industries because they provide real-time information exchange between manufacturers, distributors, and consumers. For example, beverage companies use smart labels to provide nutritional information, traceability data, and promotional engagement features. Smart labeling systems also enhance inventory management and reduce supply chain inefficiencies by enabling automated scanning and tracking.

The fastest-growing subsegment is AI-driven packaging automation, projected to grow at a CAGR of 11.2%. Growth is driven by increasing demand for predictive analytics, automated decision-making, and operational efficiency. AI systems analyze production data in real time and optimize packaging speed, material usage, and quality control. For example, FMCG companies are integrating AI vision systems to detect packaging defects instantly and adjust production lines automatically. Future adoption will expand across all manufacturing sectors, including automotive, healthcare, and electronics, as companies move toward fully autonomous packaging ecosystems.

By Material

Plastic-based smart packaging held the dominant position with 51.8% share in 2024, primarily due to its flexibility, durability, and cost-effectiveness. It is widely used for integrating sensors, RFID tags, and smart labeling systems in packaging applications. Plastic materials allow easy embedding of electronic components required for Packaging 4.0 systems. For example, consumer electronics manufacturers use plastic-based packaging for smart tracking and logistics optimization.

The fastest-growing subsegment is hybrid materials, expected to grow at a CAGR of 9.4%. Growth is driven by sustainability requirements and the need to combine durability with eco-friendly properties. Hybrid packaging materials integrate biodegradable components with smart electronic systems, enabling environmentally responsible yet technologically advanced packaging solutions. Future development will focus on reducing environmental impact while maintaining high-performance packaging capabilities.

By End-Use

Food & beverage dominated the market in 2024 with a 43.1% share, due to strong demand for supply chain traceability, freshness monitoring, and automated packaging systems. This sector relies heavily on Packaging 4.0 technologies to ensure product safety, reduce waste, and improve logistics efficiency. For example, global beverage companies use smart packaging systems for inventory tracking and distribution optimization.

Healthcare is the fastest-growing segment, projected at a CAGR of 10.1%, driven by demand for drug safety, anti-counterfeiting, and patient compliance tracking. Smart pharmaceutical packaging systems enable real-time monitoring of medication usage and temperature conditions. For example, IoT-enabled blister packs are used in chronic disease management to ensure proper dosage tracking. Future adoption will expand significantly as healthcare systems become more digitalized and regulatory compliance requirements increase.

Packaging 4.0 Market Segmentations

By Technology

- Smart Labeling Systems

- RFID-Enabled Packaging

- AI-Driven Packaging Automation

- Blockchain-Integrated Packaging

By Material

- Plastic-Based Smart Packaging

- Paper-Based Packaging

- Hybrid Materials

- Biodegradable Smart Packaging

By End-Use

- Food & Beverage

- Healthcare

- Consumer Electronics

- Industrial Manufacturing

Regional Analysis

North America

North America accounted for 31.2% of the global Packaging 4.0 market in 2025, with a projected CAGR of 9.8% during 2025–2034. The region is one of the earliest adopters of digital manufacturing ecosystems, driven by strong industrial automation infrastructure, high penetration of AI technologies, and advanced logistics networks. The United States and Canada collectively form a mature industrial base where packaging automation is already integrated into FMCG, pharmaceuticals, electronics, and e-commerce sectors. The demand for Packaging 4.0 solutions is significantly influenced by the need for supply chain transparency, efficiency optimization, and real-time operational monitoring.

A key growth factor in North America is the rapid adoption of smart warehouses and AI-driven fulfillment centers. Companies such as major retail and logistics operators are deploying automated packaging lines integrated with robotics and IoT sensors to handle high-volume e-commerce demand. For example, distribution centers in the United States use AI-powered packaging systems that automatically adjust packaging size based on product dimensions, reducing material waste and shipping costs. Another major factor is pharmaceutical compliance requirements, where Packaging 4.0 technologies enable serialization, traceability, and anti-counterfeiting measures.

The United States remains the dominant country due to large-scale investment in Industry 4.0 infrastructure. A major unique driver is the expansion of cloud-connected manufacturing ecosystems, where packaging systems are integrated with ERP and supply chain platforms. This allows real-time production adjustments based on demand fluctuations. For instance, FMCG giants in the US use predictive analytics to adjust packaging output in response to retail demand signals. Additionally, the presence of leading technology firms accelerates innovation in AI-based packaging automation and robotics integration. The growing shift toward sustainable packaging also pushes manufacturers to adopt digital optimization tools that reduce material usage and improve lifecycle efficiency.

Europe

Europe accounted for 27.4% market share in 2025, with a projected CAGR of 10.1% during 2025–2034. The region is characterized by strong regulatory frameworks, sustainability-driven manufacturing practices, and high adoption of industrial automation technologies. Countries such as Germany, France, Italy, and the United Kingdom are leading in integrating smart packaging technologies into automotive, industrial, and food processing sectors. European industries are increasingly focused on reducing carbon emissions, improving supply chain transparency, and enhancing production efficiency through Packaging 4.0 solutions.

A key growth factor in Europe is strict regulatory enforcement around sustainability and digital traceability. The European Union has implemented strong policies encouraging circular economy practices, which is driving adoption of smart packaging systems that optimize material usage and enable recycling traceability. Another major factor is industrial automation in automotive manufacturing, where Packaging 4.0 systems are used for precision component packaging, logistics tracking, and production synchronization. For example, automotive suppliers in Germany use RFID-enabled packaging systems to track parts across multi-tier supply chains.

Germany dominates the European market due to its strong engineering and industrial automation base. A unique growth driver is the integration of cyber-physical systems into packaging operations. German manufacturers are deploying fully connected production lines where packaging machines communicate with production planning systems in real time. This enables dynamic adjustment of packaging workflows based on demand fluctuations. Additionally, the rise of smart pharmaceutical packaging in Europe is contributing to growth, as companies adopt blockchain-enabled traceability systems to meet regulatory requirements and ensure drug authenticity.

Asia Pacific

Asia Pacific dominated the market with 37.4% share in 2025, and is projected to grow at the highest CAGR of 11.3% during 2025–2034. The region is the global manufacturing hub for electronics, automotive, FMCG, and e-commerce industries, making it a critical driver for Packaging 4.0 adoption. China, Japan, South Korea, and India are key contributors, with strong government support for digital transformation initiatives and smart factory development.

A major growth factor in Asia Pacific is large-scale industrial production and export-oriented manufacturing. Countries like China and India are heavily investing in automated packaging systems to support high-volume production. For example, Chinese electronics manufacturers use AI-driven packaging lines to manage export shipments efficiently while maintaining quality control. Another important driver is the rapid expansion of e-commerce platforms, which require intelligent packaging systems capable of handling massive order volumes and customized packaging requirements.

China dominates the region due to its massive industrial base and government-led digital transformation programs. A unique driver is the integration of AI-driven smart manufacturing zones, where packaging systems are fully automated and connected to centralized production ecosystems. These systems enable predictive maintenance, real-time optimization, and autonomous packaging adjustments. Additionally, Japan and South Korea are contributing through advanced robotics integration in packaging systems, particularly in electronics and semiconductor industries. The growing adoption of sustainable packaging technologies in Asia Pacific is also accelerating, driven by regulatory pressure and consumer awareness regarding environmental impact.

Middle East & Africa

The Middle East & Africa accounted for 3.8% of the market in 2025, with a projected CAGR of 9.2% during 2025–2034. Although still in the early stages of adoption, the region is witnessing steady growth due to increasing investments in logistics infrastructure, smart cities, and digital transformation initiatives. The UAE, Saudi Arabia, and South Africa are leading adopters of Packaging 4.0 technologies.

A key growth factor is the development of smart logistics hubs and trade corridors. Countries in the Gulf region are investing heavily in automated port systems and logistics infrastructure that integrate smart packaging technologies for tracking and efficiency. Another driver is the expansion of retail and FMCG sectors, which are increasingly adopting automated packaging systems to improve supply chain performance. For example, large distribution centers in the UAE use RFID-based packaging systems for inventory tracking and logistics optimization.

The UAE dominates the region due to its smart city initiatives and advanced logistics infrastructure. A unique growth driver is the integration of AI and IoT technologies in logistics hubs such as airports and ports. These systems enable real-time tracking of packaged goods across international supply chains. Additionally, the region is investing in digital healthcare infrastructure, which is driving demand for smart pharmaceutical packaging solutions with traceability features.

Latin America

Latin America held 5.2% share in 2025, and is expected to grow at the fastest regional CAGR of 11.0% during 2025–2034. The region is experiencing rapid growth in e-commerce, retail modernization, and industrial digitalization. Brazil, Mexico, and Argentina are the key markets driving adoption of Packaging 4.0 solutions.

A key growth factor is the expansion of e-commerce and digital retail platforms. Online shopping growth is driving demand for automated packaging systems capable of handling high-volume order fulfillment. Another important driver is industrial modernization in food and beverage exports, where packaging automation is used to ensure efficiency and compliance with international standards. For example, Brazilian agricultural exporters use automated packaging systems for large-scale shipment processing.

Brazil dominates the region due to its strong manufacturing and export base. A unique driver is the adoption of smart packaging systems in agro-export industries, where packaging technologies are used to maintain product quality during long-distance transportation. Additionally, increasing investment in industrial automation and logistics infrastructure is accelerating adoption of Packaging 4.0 systems across manufacturing hubs.

Competitive Landscape

The packaging 4.0 market is highly competitive, driven by digital transformation strategies and automation investments. Sealed Air Corporation is a leading player due to its strong focus on smart packaging solutions and automation integration. The company continues to invest in AI-driven packaging technologies and digital supply chain solutions.

Other major players include Amcor plc, Tetra Pak, Smurfit Kappa, and WestRock. These companies are focusing on integrating IoT, robotics, and sustainable materials into their packaging systems. Strategic collaborations with technology providers are also shaping the competitive landscape.

Key Players List

- Sealed Air Corporation

- Amcor plc

- Tetra Pak International S.A.

- Smurfit Kappa Group

- WestRock Company

- DS Smith Plc

- Mondi Group

- International Paper Company

- Sonoco Products Company

- Avery Dennison Corporation

- BASF SE

- SAP SE

- Rockwell Automation

- Siemens AG

- Schneider Electric SE