Oxygen Barrier Nutraceutical Packaging Market Size and Growth

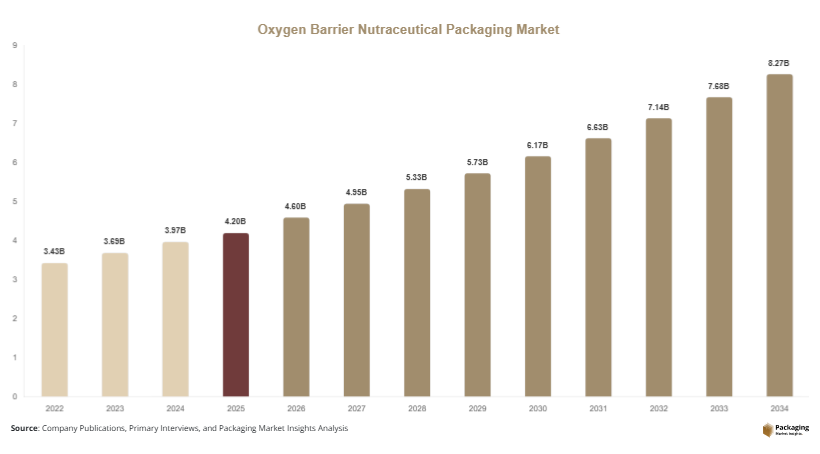

The market size was valued at approximately USD 4.2 billion in 2025 and is expected to reach around USD 4.6 billion in 2026. Over the forecast period from 2025 to 2034, the market is projected to grow to nearly USD 8.9 billion, registering a compound annual growth rate (CAGR) of 7.6%. The oxygen barrier nutraceutical packaging market is gaining steady traction as the global nutraceutical industry expands and product stability becomes a priority.

The primary purpose of oxygen barrier packaging is to protect nutraceutical products such as dietary supplements, functional foods, probiotics, and herbal formulations from oxidation. Exposure to oxygen can degrade active ingredients, reduce shelf life, and affect product efficacy. As a result, manufacturers are increasingly adopting advanced packaging solutions that offer superior barrier properties.

Key Highlights:

- The market size reached USD 4.2 billion in 2025, reflecting steady growth driven by rising demand for protective packaging solutions. This expansion is supported by increasing consumption of nutraceutical products worldwide.

- The market is expected to grow to USD 8.9 billion by 2034, indicating strong long-term growth potential. Expansion of global supply chains and product innovation are contributing to this upward trend.

- The market is projected to register a CAGR of 7.6% during the forecast period from 2025 to 2034. Consistent demand across developed and emerging markets is supporting this stable growth rate.

- Increasing demand for nutraceutical products globally is a key growth driver. Consumers are focusing more on preventive healthcare, boosting the need for effective packaging solutions.

- Advancements in high-barrier packaging technologies are enhancing product protection and shelf life. Innovations in multi-layer films and coatings are improving oxygen resistance and overall packaging performance.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

One significant trend in the oxygen barrier nutraceutical packaging market is the increasing adoption of multi-layer and high-barrier films. These films combine different materials such as polyethylene, polyethylene terephthalate, and aluminum layers to create strong oxygen resistance. Manufacturers are investing in these advanced materials to improve product shelf life and maintain the stability of sensitive ingredients. The trend is particularly evident in packaging for probiotics and omega-based supplements, where oxidation can quickly degrade product quality. As consumer expectations for product efficacy rise, companies are focusing on packaging solutions that offer consistent protection and performance.

Another key trend is the growing shift toward sustainable and recyclable oxygen barrier packaging solutions. Environmental concerns are encouraging companies to reduce reliance on traditional plastic materials and adopt eco-friendly alternatives. Manufacturers are developing recyclable high-barrier films and bio-based materials that maintain oxygen resistance while minimizing environmental impact. This trend is gaining momentum in developed regions where regulatory frameworks and consumer awareness are driving sustainability initiatives. As a result, companies are balancing performance and environmental responsibility in their packaging strategies.

Market Drivers

A major driver of the oxygen barrier nutraceutical packaging market is the increasing consumption of dietary supplements and functional foods. The global shift toward preventive healthcare is encouraging consumers to incorporate nutraceutical products into their daily routines. This growing demand requires packaging solutions that preserve the potency and effectiveness of active ingredients. Oxygen barrier packaging plays a crucial role in maintaining product quality, especially for sensitive compounds such as vitamins, enzymes, and probiotics. As consumption continues to rise, the demand for reliable packaging solutions is expected to increase significantly.

Another important driver is the expansion of the global nutraceutical supply chain. Manufacturers are distributing products across multiple regions, which involves longer transit times and exposure to varying environmental conditions. Oxygen barrier packaging helps protect products during transportation and storage, ensuring that they reach consumers in optimal condition. This is particularly important for companies operating in international markets where regulatory standards and quality expectations are stringent. The need for consistent product quality across geographies is driving the adoption of advanced packaging solutions.

Market Restraint

One of the key restraints in the oxygen barrier nutraceutical packaging market is the high cost associated with advanced barrier materials and technologies. Multi-layer films, specialized coatings, and high-performance packaging solutions often involve complex manufacturing processes and expensive raw materials. This can increase overall packaging costs for nutraceutical companies, particularly small and medium-sized enterprises with limited budgets.

The impact of this restraint is evident in price-sensitive markets where cost considerations play a significant role in purchasing decisions. For example, smaller nutraceutical brands may opt for conventional packaging solutions to reduce expenses, even if it compromises product shelf life. This can limit the adoption of oxygen barrier packaging in certain segments of the market. Additionally, the cost factor can influence pricing strategies, potentially affecting product competitiveness in the market.

Market Opportunities

One promising opportunity in the oxygen barrier nutraceutical packaging market is the rapid growth of personalized nutrition. Consumers are increasingly seeking customized nutraceutical solutions tailored to their specific health needs. This trend is creating demand for specialized packaging that can preserve the quality of individualized formulations. Oxygen barrier packaging is well-suited for this purpose, as it ensures the stability of diverse ingredients in personalized products. As the personalized nutrition market expands, packaging providers have the opportunity to develop innovative solutions that cater to this niche segment.

Another significant opportunity lies in the expansion of emerging markets. Regions such as Asia Pacific and Latin America are experiencing rising disposable incomes and growing awareness of health and wellness products. This is driving demand for nutraceuticals and, consequently, for advanced packaging solutions. As local manufacturers upgrade their production capabilities and adopt global standards, the demand for oxygen barrier packaging is expected to increase. Companies that establish a strong presence in these markets can benefit from long-term growth opportunities.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 4.2 Billion |

| Market Size in 2026 | USD 4.6 Billion |

| Market Size in 2034 | USD 8.9 Billion |

| CAGR | 7.6% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Plastic-based oxygen barrier packaging dominated the market in 2024, accounting for approximately 64% of the total share. These materials are widely used due to their flexibility, cost-effectiveness, and ability to provide strong barrier properties. Multi-layer plastic films are particularly popular as they combine different materials to enhance oxygen resistance. These packaging solutions are commonly used for capsules, powders, and liquid supplements. Their lightweight nature and ease of customization make them suitable for a wide range of applications.

Bio-based and sustainable materials are the fastest-growing segment, expected to register a CAGR of 8.4% during the forecast period. The increasing focus on environmental sustainability is driving demand for eco-friendly packaging solutions. Manufacturers are developing bio-based films and recyclable materials that offer comparable barrier properties to traditional plastics. This segment is gaining traction among companies seeking to align with sustainability goals and regulatory requirements.

By Packaging Type

Flexible packaging held the largest market share in 2024, accounting for nearly 58% of total demand. Flexible formats such as pouches, sachets, and films are widely used due to their convenience, lightweight nature, and cost efficiency. These packaging solutions are ideal for single-use and multi-dose nutraceutical products. Their ability to incorporate high-barrier layers makes them suitable for protecting sensitive ingredients from oxygen exposure.

Rigid packaging is the fastest-growing segment, with a projected CAGR of 7.9%. Bottles, jars, and containers made from high-barrier materials are increasingly used for premium nutraceutical products. These packaging formats offer enhanced protection and are preferred for products that require extended shelf life. The growing demand for premium and high-value nutraceuticals is driving growth in this segment.

By Application

Dietary supplements dominated the market in 2024, accounting for approximately 60% of the total share. This segment includes vitamins, minerals, and herbal supplements that require protection from oxidation. The widespread use of these products across various age groups is driving demand for reliable packaging solutions. Oxygen barrier packaging ensures that active ingredients remain stable and effective throughout the product lifecycle.

Functional foods and beverages are the fastest-growing application segment, expected to register a CAGR of 8.6%. The increasing popularity of fortified foods and drinks is driving demand for packaging solutions that can preserve product quality. Oxygen barrier packaging plays a critical role in maintaining the freshness and nutritional value of these products, supporting their growth in the market.

Oxygen Barrier Nutraceutical Packaging Market Segmentations

By Material Type

- Plastic-Based Materials

- Bio-Based Materials

By Packaging Type

- Flexible Packaging

- Rigid Packaging

By Application

- Dietary Supplements

- Functional Foods & Beverages

- Probiotics & Herbal Products

Regional Analysis

North America

North America accounted for approximately 32% of the global oxygen barrier nutraceutical packaging market share in 2025 and is expected to grow at a CAGR of 6.8% during the forecast period. The region benefits from a well-established nutraceutical industry and high consumer awareness regarding product quality and safety.

The United States dominates the regional market due to its large consumer base and strong presence of nutraceutical manufacturers. A unique growth factor in this region is the increasing demand for clean-label products, which is driving the adoption of high-quality oxygen barrier packaging solutions.

Europe

Europe held around 25% of the market share in 2025 and is projected to grow at a CAGR of 6.5% through 2034. The region is characterized by stringent regulatory standards that emphasize product safety and packaging quality.

Germany is a leading market in Europe, supported by its advanced manufacturing capabilities and strong pharmaceutical and nutraceutical sectors. A unique growth factor is the increasing focus on sustainable packaging solutions, which is encouraging the development of recyclable oxygen barrier materials.

Asia Pacific

Asia Pacific accounted for approximately 28% of the market share in 2025 and is expected to grow at a CAGR of 8.3%. Rapid urbanization and increasing health awareness are driving demand for nutraceutical products in the region.

China leads the regional market due to its large population and expanding healthcare industry. A unique growth factor is the rapid growth of e-commerce platforms, which is increasing demand for durable and protective packaging solutions.

Middle East & Africa

The Middle East & Africa region held about 8% of the market share in 2025 and is projected to grow at a CAGR of 7.1%. The market is supported by rising healthcare investments and increasing awareness of preventive health measures.

The United Arab Emirates is a key market in the region, driven by a growing expatriate population and rising demand for premium nutraceutical products. A unique growth factor is the increasing adoption of imported nutraceuticals, which require high-quality packaging for long-distance transportation.

Latin America

Latin America accounted for approximately 7% of the market share in 2025 and is expected to grow at a CAGR of 6.9%. The region is experiencing steady growth in the nutraceutical sector, supported by increasing consumer awareness.

Brazil dominates the regional market due to its large population and growing health-conscious consumer base. A unique growth factor is the rising demand for functional foods and supplements, which is driving the need for advanced packaging solutions.

Competitive Landscape

The oxygen barrier nutraceutical packaging market is characterized by a mix of global and regional players competing on the basis of product innovation, quality, and pricing. Companies are focusing on developing advanced barrier materials and sustainable packaging solutions to meet evolving consumer and regulatory requirements.

Amcor plc is a leading player in the market, known for its extensive product portfolio and global presence. The company has recently introduced recyclable high-barrier packaging solutions designed specifically for nutraceutical applications, reflecting the growing emphasis on sustainability.

Other major players are investing in research and development to enhance product performance and expand their market reach. Strategic partnerships, mergers, and acquisitions are also common as companies seek to strengthen their competitive position and access new markets.

Key Players List

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Constantia Flexibles

- Mondi Group

- Huhtamaki Oyj

- Uflex Ltd

- Winpak Ltd

- Glenroy Inc.

- ProAmpac LLC

- Clondalkin Group

- AptarGroup Inc.

- Gerresheimer AG

- Coveris Holdings S.A.