Oven Bags & Pouches Market Size and Growth

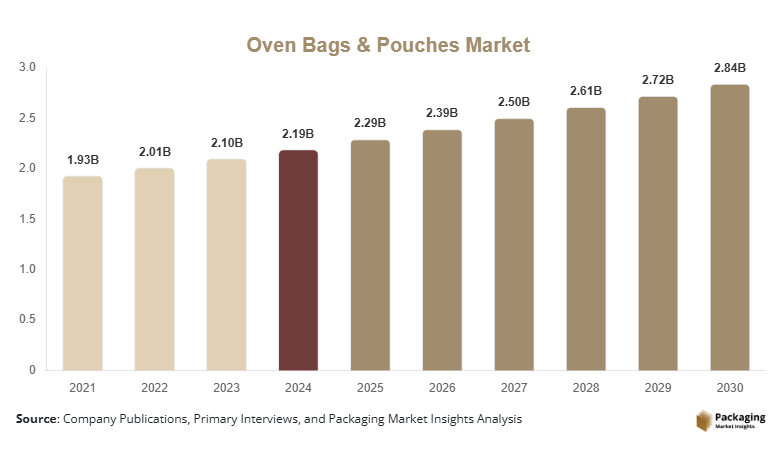

The global oven bags & pouches market size was valued at approximately USD 2.19 billion in 2024 and is projected to grow from USD 2.29 billion in 2025 to reach nearly USD 2.84 billion by 2030, expanding at a CAGR of 4.4% during the forecast period (2025–2030). The oven bags & pouches market growth is primarily driven by the rising consumption of ready-to-cook and processed food products, increasing demand for convenient and hygienic cooking solutions, and continuous advancements in high-temperature-resistant flexible packaging materials.

Oven bags and pouches are gaining widespread acceptance across household, food service, and industrial food processing applications due to their ability to retain moisture, enhance food quality, reduce cooking time, and minimize contamination risks. Growing urbanization, busy lifestyles, and the expansion of organized retail and cold-chain infrastructure are further strengthening market adoption globally.

Key Market Insights

- Oven bags and pouches are increasingly being adopted as oven-ready packaging solutions by food manufacturers to improve convenience and cooking consistency for end consumers.

- Multi-layer, high-barrier oven pouches are gaining traction due to their superior resistance to heat, grease, moisture, and oxygen.

- North America dominates the global market, driven by high consumption of packaged meats and ready meals.

- Asia-Pacific is the fastest-growing region, supported by the rapid expansion of food processing industries in China and India.

- Sustainability-focused innovations, including recyclable and downgauged ovenable films, are reshaping product development strategies.

- Direct B2B contracts with food processors remain the leading distribution channel globally.

Explore more data points, trends and opportunities Download Free Sample Report

Latest Market Trends

Rising Demand for Ready-to-Cook and Oven-Ready Packaging

Food manufacturers are increasingly shifting toward oven-ready packaging formats to cater to consumers seeking convenience without compromising food quality. Oven bags and pouches eliminate the need for additional cookware and reduce preparation steps, making them particularly attractive for packaged meats, marinated products, and frozen meals. This trend is accelerating demand for vacuum-sealed and stand-up oven pouches that offer extended shelf life and consistent cooking outcomes. Private-label brands and meal-kit companies are also contributing to volume growth by adopting customized ovenable packaging formats.

Sustainability and Material Innovation Shaping Product Development

Sustainability has emerged as a critical trend in the oven bags & pouches market. Manufacturers are investing in recyclable mono-material structures, reduced-gauge films, and alternative polymer blends to meet tightening food-contact and environmental regulations. European and North American markets, in particular, are witnessing increased adoption of recyclable PET-based and high-performance polypropylene oven bags. These innovations are helping companies maintain heat resistance while reducing overall material consumption and carbon footprint.

Market Drivers

Changing Consumer Lifestyles and Cooking Behaviors

Urbanization and busy work schedules have significantly increased reliance on convenient cooking solutions that reduce preparation time without compromising food quality. Oven bags and pouches allow users to cook food evenly while retaining moisture and flavor, making them particularly attractive for meat, poultry, and ready-meal applications. This driver has been especially prominent in North America and Europe, where household penetration of ovenable packaging has increased steadily over the past five years.

Rapid Expansion of the Processed and Packaged Food Industry

Food manufacturers are increasingly adopting ovenable pouches to improve shelf life, reduce contamination risks, and enhance consumer convenience. Ready-to-cook meats, frozen meals, and pre-marinated products increasingly rely on oven-safe packaging formats, creating consistent bulk demand from industrial food processors. This trend has been reinforced by growth in organized retail and cold chain logistics worldwide.

Market Restraints

Volatility in Raw Material Prices

Particularly for petrochemical-based polymers such as nylon, PET, and PP. Fluctuating oil prices directly impact production costs, squeezing profit margins for manufacturers and limiting pricing flexibility.

Regulatory Scrutiny Related to Food Contact Safety and Environmental Impact

Compliance with varying regional standards increases certification costs and slows product approvals, particularly for smaller manufacturers. Overcoming these barriers requires continuous R D investment and regulatory alignment, which may slow market expansion in price-sensitive regions.

Market Opportunities

Expansion of Ready-to-Cook and Meal-Kit Ecosystems

As consumers increasingly seek convenient yet high-quality home-cooked meals, food brands are investing in oven-ready packaging formats that eliminate additional cookware and preparation steps. This trend creates strong demand for customized oven pouches with enhanced barrier properties, branding space, and portion control features. Existing packaging manufacturers can leverage this shift by developing co-branded solutions with food producers, while new entrants can target private-label meal kit companies.

Integration of Sustainable and Recyclable Materials

Regulatory pressure on single-use plastics, particularly in Europe and parts of Asia, is pushing packaging producers toward mono-material, recyclable, and biodegradable ovenable solutions. Companies that successfully balance heat resistance with environmental compliance stand to gain early-mover advantages. Innovations such as recyclable PET-based oven bags and reduced-gauge high-barrier films present strong growth potential, especially among premium food brands and environmentally conscious consumers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2024 | USD 2.19 Billion |

| Market Size in 2025 | USD 2.29 Billion |

| Market Size in 2030 | USD 2.84 Billion |

| CAGR | 4.4% (2025-2030) |

| Base Year for Estimation | 2024 |

| Historical Data | 2021-2023 |

| Forecast Period | 2025-2030 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

The nylon (PA-based oven bags) subsegment accounted for the largest share of the global oven bags & pouches market, contributing approximately 34% of total market revenue in 2024. This dominance is primarily attributed to nylon’s superior heat resistance, high tensile strength, and excellent puncture resistance, making it ideal for high-temperature cooking applications such as roasting meat and poultry. Nylon-based materials are widely adopted by food processors and household consumers due to their ability to withstand temperatures above 200°C while maintaining food safety and structural integrity.

The multi-layer high-barrier films subsegment is projected to be the fastest-growing during the forecast period, registering a CAGR of around 7.8% from 2025 to 2030. Growth in this segment is driven by increasing demand for advanced barrier properties, including combined resistance to oxygen, moisture, and grease. These films are extensively used in ready-to-cook meals and vacuum-sealed products, where extended shelf life and consistent cooking performance are critical, positioning multi-layer structures for rapid expansion.

By Product Type

The oven cooking bags subsegment held a dominant share of approximately 38% of the global market in 2024. Their widespread use in household cooking, affordability, and compatibility with conventional ovens have driven strong adoption across both developed and developing regions. Oven cooking bags are particularly popular for roasting applications, where moisture retention and ease of cleanup are key consumer benefits.

The stand-up oven pouches subsegment is anticipated to witness the fastest growth, with a projected CAGR of nearly 8.2% from 2025 to 2030. This growth is supported by increasing adoption in ready-to-cook and premium packaged food categories, where enhanced shelf appeal, branding space, and convenience play a critical role. Food manufacturers increasingly favor stand-up formats due to their ability to combine cooking functionality with retail presentation.

By Temperature Resistance

The 180°C–220°C temperature resistance subsegment accounted for the largest share, representing around 41% of total market demand in 2024. This temperature range aligns with most conventional oven settings used in residential and commercial kitchens, making it the most versatile and commercially viable category. Packaging solutions in this range balance material cost, safety, and performance, driving widespread adoption.

The above 220°C temperature resistance subsegment is expected to grow at the fastest pace, recording a CAGR of approximately 7.5% during the forecast period. This growth is fueled by increasing demand from commercial kitchens and premium food processing applications that require higher temperature tolerance for specialized cooking and roasting processes.

By End-Use Industry

The meat, poultry, and seafood subsegment dominated the global oven bags & pouches market, accounting for nearly 42% of total revenue in 2024. Rising global protein consumption, increasing sales of pre-marinated and oven-ready meat products, and strong demand from food processors have significantly contributed to this segment’s leadership. Ovenable packaging ensures consistent cooking results, improved food safety, and extended shelf life, making it essential for protein-based products.

The ready-to-eat and ready-to-cook meals subsegment is projected to be the fastest-growing, with an estimated CAGR of 7.9% from 2025 to 2030. Growth is driven by urban lifestyles, expanding meal-kit services, and rising consumer preference for convenient cooking solutions that reduce preparation time without sacrificing quality.

By Distribution Channel

The direct sales (B2B contracts) subsegment held the largest share of the global market, contributing approximately 45% of total revenue in 2024. This dominance is driven by long-term supply agreements between packaging manufacturers and large food processors, meat producers, and foodservice operators. Direct sales ensure consistent product quality, customized specifications, and stable volume demand, making this channel critical for large-scale market participants.

The private label and retail packaging subsegment is expected to register the fastest growth, expanding at a CAGR of around 8.0% during the forecast period. The rapid growth of private-label food brands, especially in supermarkets and online grocery platforms, is driving demand for cost-effective yet high-performance oven bags and pouches, supporting strong expansion in this channel.

Oven Bags & Pouches Market Segmentations

By Material Type

- Nylon (PA-Based Oven Bags)

- Polyethylene (Heat-Resistant PE)

- Polypropylene (High-Temperature PP)

- Aluminum Foil-Laminated Structures

- Multi-Layer High-Barrier Films

By Product Type

- Oven Cooking Bags

- Stand-Up Oven Pouches

- Flat Oven Pouches

- Vacuum Oven Pouches

- Resealable Oven Pouches

By Temperature Resistance

- Up to 180°C

- 180°C–220°C

- Above 220°C

By End-Use Industry

- Meat, Poultry Seafood

- Ready-to-Eat Ready-to-Cook Meals

- Bakery Confectionery

- Foodservice Catering

- Household / Retail Consumers

By Distribution Channel

- Direct Sales (B2B Contracts)

- Packaging Distributors

- Private Label Retail Packaging

Regional Analytic

North America

North America remains the largest regional market for oven bags and pouches, accounting for approximately 32% of the global market share in 2024. The United States leads regional demand, driven by strong consumption of packaged meats, poultry, and ready meals, along with high penetration of modern retail and private-label food products. Food processors in the region increasingly rely on ovenable packaging to enhance product differentiation and meet consumer expectations for convenience. Canada also contributes steadily, supported by similar consumption patterns and regulatory alignment with the U.S.

Europe

Europe represents the second-largest market, holding nearly 28% of global demand, with Germany, the United Kingdom, and France as major contributors. European consumers show a strong preference for safe, sustainable, and high-quality food packaging solutions. Strict food safety regulations and sustainability mandates are driving innovation in recyclable and high-barrier oven pouches. Growth in this region is also supported by the increasing adoption of ready-to-cook meals and bakery products.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing regional market, expanding at a CAGR exceeding 8%. China accounts for the largest share in the region due to its rapidly expanding food processing sector and rising consumption of packaged foods. India is witnessing strong growth driven by urbanization, increasing disposable incomes, and government initiatives supporting food manufacturing. Japan and South Korea represent mature but stable markets with consistent demand from premium and convenience food segments.

Latin America

Latin America holds a smaller but steadily growing share, led by Brazil and Mexico. Growth in this region is supported by rising packaged food consumption and improving cold-chain infrastructure. The Middle East Africa market is also expanding, driven by urbanization, growth in foodservice establishments, and increasing reliance on imported packaged food products.

Competitive Landscape

The oven bags & pouches market is moderately consolidated, with the top five manufacturers accounting for approximately 48% of the global market share. Large multinational packaging companies dominate due to their advanced material technologies, global manufacturing footprints, and strong relationships with food processors. While premium and high-barrier segments are controlled by major players, regional manufacturers remain competitive in cost-sensitive and private-label segments.

Key Players in the Oven bags & pouches Market

- Amcor

- Berry Global

- Mondi Group

- Sealed Air

- Huhtamaki

- Winpak

- Coveris

- Constantia Flexibles

- ProAmpac

- Clondalkin Group

- UFlex

- Wipak Group

- Sigma Plastics

- Flexopack

- TC Transcontinental