Ophthalmic Packaging Market Size and Growth

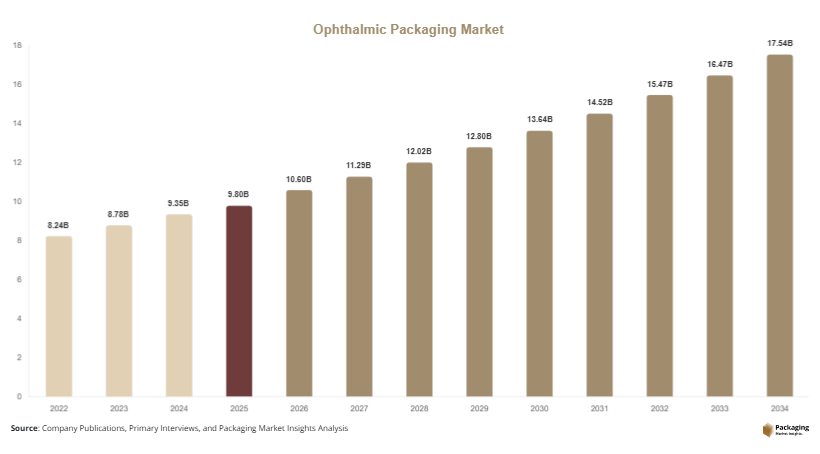

The global ophthalmic packaging market size was valued at approximately USD 9.8 billion in 2025 and is projected to reach USD 10.6 billion in 2026. With growing healthcare investments and expanding pharmaceutical production, the market is expected to reach USD 18.7 billion by 2034, registering a CAGR of 6.5% during the forecast period (2025–2034). Ophthalmic packaging plays a critical role in maintaining the stability, sterility, and efficacy of products such as eye drops, ointments, and surgical solutions. The ophthalmic packaging market is experiencing steady growth driven by the rising prevalence of eye-related disorders, increasing demand for ophthalmic drugs, and advancements in packaging technologies that ensure product safety and sterility.

Several factors are contributing to market expansion. The increasing incidence of eye conditions such as glaucoma, dry eye syndrome, and cataracts is driving demand for ophthalmic treatments, thereby boosting packaging requirements. Another key factor is the growing geriatric population, which is more susceptible to eye diseases and requires long-term treatment. Additionally, stringent regulatory requirements for pharmaceutical packaging are encouraging manufacturers to adopt high-quality and compliant packaging solutions. These regulations ensure patient safety and product integrity, further driving market growth.

Key Highlights:

Asia Pacific dominated the market with a 36.5% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.9%.

Plastic containers led the type segment with a 47.2% share, while single-dose packaging is expected to grow at a CAGR of 7.1%.

Polyethylene materials dominated with a 52.8% share, while eco-friendly materials are forecasted to grow at a CAGR of 6.8%.

Pharmaceutical applications led the segment with 62.4% share, while surgical ophthalmic products are expected to grow at a CAGR of 6.6%.

China remained the dominant country with a market size of USD 2.6 billion in 2025 and USD 2.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing adoption of preservative-free and single-dose packaging

The ophthalmic packaging market is witnessing a growing preference for preservative-free and single-dose packaging solutions. These formats are designed to reduce the risk of contamination and improve patient safety, particularly for individuals with sensitive eyes or chronic conditions. Single-dose packaging eliminates the need for preservatives, which can cause irritation or allergic reactions in some patients. Manufacturers are investing in advanced packaging technologies to produce sterile and user-friendly single-dose containers. This trend is gaining traction in developed markets where regulatory standards are stringent, and patient awareness is high. Additionally, healthcare providers are recommending preservative-free products, further supporting the adoption of these packaging solutions.

Integration of advanced materials and smart packaging technologies

Another key trend is the integration of advanced materials and smart packaging technologies in ophthalmic products. Manufacturers are using high-performance polymers that offer improved barrier properties, ensuring product stability and extended shelf life. Smart packaging solutions, such as tamper-evident features and digital tracking systems, are also being incorporated to enhance safety and traceability. These technologies help prevent counterfeit products and ensure compliance with regulatory standards. The adoption of such innovations is particularly important in the pharmaceutical industry, where product integrity is critical. As technology continues to evolve, the use of advanced materials and smart features is expected to increase significantly.

Market Drivers

Rising prevalence of eye disorders and aging population

The increasing prevalence of eye disorders is a major factor driving the ophthalmic packaging market. Conditions such as glaucoma, cataracts, and dry eye syndrome are becoming more common due to aging populations and lifestyle changes. The growing geriatric population is particularly susceptible to these conditions, leading to higher demand for ophthalmic medications. This, in turn, increases the need for reliable and safe packaging solutions that maintain product efficacy. Healthcare providers are also emphasizing early diagnosis and treatment, further boosting demand for ophthalmic products and packaging.

Stringent regulatory requirements for pharmaceutical packaging

Regulatory requirements play a crucial role in driving the adoption of high-quality ophthalmic packaging solutions. Governments and regulatory bodies have established strict guidelines to ensure the safety, sterility, and efficacy of pharmaceutical products. Compliance with these regulations requires the use of advanced packaging materials and technologies. Manufacturers are investing in research and development to meet these standards and avoid penalties. The need for tamper-evident and child-resistant packaging is also increasing, particularly for over-the-counter ophthalmic products. These regulatory factors are driving continuous innovation and growth in the market.

Market Restraint

High cost of advanced packaging solutions

The high cost associated with advanced ophthalmic packaging solutions is a significant restraint for market growth. Technologies such as single-dose packaging and preservative-free systems require specialized materials and manufacturing processes, leading to increased production costs. Small and medium-sized pharmaceutical companies may find it challenging to invest in such technologies, limiting their adoption. Additionally, the cost of compliance with regulatory requirements can be substantial, particularly for companies operating in multiple regions. These factors can impact profit margins and slow down market expansion. For example, transitioning from multi-dose to single-dose packaging requires significant investment in new equipment and production lines, which can be a barrier for some manufacturers.

Market Opportunities

Development of sustainable and recyclable packaging materials

The growing focus on sustainability presents significant opportunities for the ophthalmic packaging market. Manufacturers are exploring the use of recyclable and biodegradable materials to reduce environmental impact. Innovations in material science are enabling the development of eco-friendly packaging solutions that maintain product safety and performance. These sustainable solutions are gaining acceptance among consumers and regulatory bodies, creating new growth opportunities. Companies that invest in sustainable packaging technologies are likely to gain a competitive advantage in the market.

Expansion of pharmaceutical manufacturing in emerging markets

Emerging markets offer substantial growth opportunities due to increasing healthcare investments and expanding pharmaceutical manufacturing capabilities. Countries in Asia Pacific, Latin America, and Africa are witnessing significant growth in the healthcare sector, driven by rising population and improving access to medical services. This expansion is increasing demand for ophthalmic products and packaging solutions. Governments are also supporting local manufacturing through favorable policies and incentives. As a result, companies are investing in these regions to capitalize on growth opportunities and strengthen their market presence.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.8 Billion |

| Market Size in 2026 | USD 10.6 Billion |

| Market Size in 2034 | USD 18.7 Billion |

| CAGR | 6.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Plastic containers dominated the market with a 47.2% share in 2024. These containers are widely used for ophthalmic products due to their durability, lightweight nature, and cost-effectiveness. They provide excellent protection against contamination and are compatible with various formulations. Manufacturers are focusing on improving container design to enhance usability and patient convenience.

Single-dose packaging is expected to grow at the fastest CAGR of 7.1% during the forecast period. This segment is gaining popularity due to its ability to eliminate contamination risks and improve patient safety. The increasing demand for preservative-free formulations is driving the adoption of single-dose packaging. Technological advancements are further enhancing the efficiency and affordability of these solutions.

By Material

Polyethylene materials accounted for the largest share of 52.8% in 2024 due to their flexibility, durability, and chemical resistance. These materials are widely used in ophthalmic packaging applications. Their ability to maintain product integrity under various conditions is driving their adoption.

Eco-friendly materials are projected to grow at a CAGR of 6.8% due to increasing demand for sustainable packaging solutions. Manufacturers are developing biodegradable and recyclable materials to reduce environmental impact. This trend is supported by regulatory requirements and consumer preferences.

By Application

Pharmaceutical applications dominated the market with a 62.4% share in 2024. Ophthalmic drugs require high-quality packaging to ensure safety and efficacy. The increasing prevalence of eye disorders is driving demand for pharmaceutical packaging solutions.

Surgical ophthalmic products are expected to grow at a CAGR of 6.6% due to rising demand for eye surgeries. Packaging plays a critical role in maintaining sterility and ensuring product safety. Technological advancements are improving packaging performance and supporting segment growth.

Ophthalmic Packaging Market Segmentations

By Product Type

- Plastic Containers

- Glass Containers

- Single-Dose Packaging

- Multi-Dose Packaging

By Application

- Pharmaceutical

- Surgical Ophthalmic Products

- Diagnostic Products

- Contact Lens Solutions

By Distribution Channel

- Direct Sales

- Pharmaceutical Distributors

- Hospital Supply Chains

- Online Medical Suppliers

Regional Analysis

North America

North America accounted for approximately 25.1% of the ophthalmic packaging market share in 2025 and is projected to grow at a CAGR of 6.0% during the forecast period. The region benefits from advanced healthcare infrastructure and high demand for ophthalmic products. The presence of major pharmaceutical companies and increasing adoption of advanced packaging technologies are driving market growth.

The United States dominates the regional market due to its large patient population and strong healthcare system. A key growth factor is the increasing use of preservative-free packaging solutions, which improve patient safety and compliance. Continuous innovation in packaging technologies is supporting market expansion.

Europe

Europe held a market share of around 22.7% in 2025 and is expected to grow at a CAGR of 5.8%. The region’s growth is driven by strict regulatory requirements and high awareness of eye health. Manufacturers are focusing on developing compliant and sustainable packaging solutions.

Germany is the leading country in the European market due to its strong pharmaceutical industry. A major growth factor is the emphasis on quality and safety standards, which is encouraging the adoption of advanced packaging technologies.

Asia Pacific

Asia Pacific dominated the market with a 36.5% share in 2025 and is projected to grow at a CAGR of 7.0%. Rapid urbanization, increasing healthcare expenditure, and growing prevalence of eye disorders are driving growth in this region. The expansion of pharmaceutical manufacturing is also contributing significantly.

China is the dominant country in the region, supported by large-scale production capabilities and government initiatives. A unique growth factor is the increasing investment in healthcare infrastructure, which is boosting demand for ophthalmic packaging solutions.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7.2% of the market share in 2025 and is expected to grow at a CAGR of 6.2%. The market is gradually expanding due to improving healthcare infrastructure and increasing awareness of eye health.

The United Arab Emirates is a key contributor to regional growth due to its focus on healthcare development. A significant growth factor is the adoption of advanced packaging technologies, which enhance product safety and compliance.

Latin America

Latin America held a market share of around 8.5% in 2025 and is projected to grow at the fastest CAGR of 6.9%. Increasing healthcare investments and rising prevalence of eye disorders are driving market growth. The expansion of pharmaceutical manufacturing is also contributing to demand.

Brazil dominates the regional market due to its growing healthcare sector. A unique growth factor is the increasing availability of affordable ophthalmic treatments, which is boosting demand for packaging solutions.

Competitive Landscape

The ophthalmic packaging market is moderately competitive, with several global and regional players focusing on innovation and compliance. Companies are investing in research and development to enhance packaging performance and meet regulatory requirements. Strategic partnerships and acquisitions are also common, enabling companies to expand their market presence.

Gerresheimer AG is a leading player in the market, known for its high-quality pharmaceutical packaging solutions. The company recently introduced advanced ophthalmic packaging systems designed to improve product safety and usability. Other major players are also focusing on sustainability and technological advancements to remain competitive.

Key Players List

- Gerresheimer AG

- Amcor plc

- West Pharmaceutical Services, Inc.

- Schott AG

- Berry Global Inc.

- AptarGroup, Inc.

- SGD Pharma

- Tekni-Plex, Inc.

- Nipro Corporation

- BD (Becton, Dickinson and Company)

- Nemera Development S.A.

- UFP Technologies, Inc.

- Silgan Holdings Inc.

- WestRock Company

- Sealed Air Corporation