Old Corrugated Container Market Size and Growth

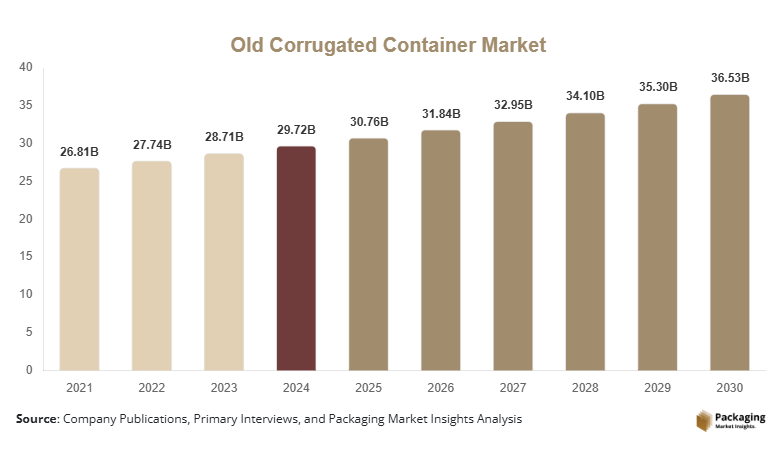

The global Old Corrugated Container (OCC) market size was valued at USD 29.72 billion in 2024 and is projected to grow from USD 30.76 billion in 2025 to reach USD 36.53 billion by 2030, expanding at a CAGR of 3.5% during the forecast period (2025–2030). The OCC market growth is primarily driven by the expanding corrugated packaging industry, rising e-commerce penetration, increasing use of recycled fiber in containerboard manufacturing, and global policy momentum toward the circular economy and landfill diversion.

OCC represents the most widely recycled paper grade globally and serves as a critical raw material for linerboard and fluting production. Demand growth is structurally supported by sustainability commitments from FMCG companies, retailers, and logistics players seeking higher recycled content in packaging. Additionally, OCC remains cost-competitive versus virgin pulp, strengthening its role as the preferred fiber source for paper mills. While short-term pricing volatility persists, long-term fundamentals remain positive due to consistent packaging demand and tightening environmental regulations.

Key Market Insights

- Commercial and retail sources remain the largest contributors to OCC supply, supported by high-volume, centralized collection from supermarkets, warehouses, and e-commerce fulfillment centers.

- Containerboard manufacturing dominates OCC consumption, accounting for more than 70% of total demand globally.

- Asia-Pacific leads global demand, driven by the rapid expansion of containerboard capacity and structural fiber deficits in key economies.

- North America remains the largest OCC exporting region, supported by high recovery rates and mature recycling infrastructure.

- Sustainability mandates, recycled content targets, and extended producer responsibility (EPR) regulations are stabilizing long-term OCC demand.

- Technological adoption in material recovery facilities, including AI-based sorting and contamination control, is improving OCC quality and price realization.

Explore more data points, trends and opportunities Download Free Sample Report

Market Latest Trends

Recycling Policy and Circular Economy Alignment Gaining Momentum

The OCC market is increasingly aligned with national and regional circular economy strategies. Governments across North America, Europe, and Asia-Pacific are strengthening recycling mandates, landfill diversion targets, and recycled content requirements for packaging materials. These policies are directly increasing OCC recovery rates while improving collection efficiency from commercial and residential sources. Large consumer goods companies are reinforcing this trend by committing to 50–100% recyclable or recycled packaging by 2030, creating structural demand stability for OCC. As a result, OCC is transitioning from a commodity-grade waste material into a strategically valued industrial feedstock.

The OCC market is also benefiting from investments in advanced sorting and processing technologies. Automated baling systems, optical scanners, and AI-enabled contamination detection are allowing recyclers to supply higher-grade OCC to paper mills, particularly for export markets. This technological shift is improving margins for processors and reducing fiber loss across the value chain.

Market Drivers

Growth in E-commerce and Corrugated Packaging

Global e-commerce volumes continue to expand at high single-digit rates, driving demand for corrugated shipping boxes. Each incremental increase in containerboard production translates directly into higher OCC consumption, reinforcing recycled fiber demand.

Cost Advantage Over Virgin Pulp

OCC-based containerboard production remains 15–30% cheaper than virgin kraft pulp alternatives, particularly during periods of pulp price inflation. This economic advantage supports sustained demand from mills globally.

Market Restraints

Price Volatility & Cyclicality

OCC prices fluctuate sharply with containerboard demand cycles, export regulations, and freight costs. Volatility creates margin uncertainty for processors and collectors.

Contamination & Quality Challenges

Rising contamination from food waste, plastics, and mixed materials reduces usable fiber yield and increases processing costs, particularly in residential streams.

Market Opportunities

Policy-Driven Recycling Expansion

Government-led recycling mandates across North America, Europe, and Asia are accelerating OCC recovery rates. Extended Producer Responsibility (EPR), landfill diversion targets, and mandatory recycled content regulations create stable, long-term demand for OCC. Markets such as India, Indonesia, and Vietnam are formalizing waste collection systems, unlocking large volumes of untapped OCC supply. Companies investing early in collection infrastructure and processing capacity can secure long-term feedstock advantages.

Rising Asia-Pacific Import Demand

Asia-Pacific remains structurally short of high-quality recovered fiber due to limited domestic collection efficiency. Despite regulatory tightening, countries such as India, Vietnam, Thailand, and Malaysia continue importing OCC for containerboard production. Export-oriented OCC processors in North America and Europe benefit from premium pricing on sorted, low-contamination OCC grades. Investment in quality control, baling, and contamination reduction directly improves export margins.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2024 | USD 29.72 Billion |

| Market Size in 2025 | USD 30.76 Billion |

| Market Size in 2030 | USD 36.53 Billion |

| CAGR | 3.5% (2025-2030) |

| Base Year for Estimation | 2024 |

| Historical Data | 2021-2023 |

| Forecast Period | 2025-2030 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Source of Generation

The Commercial & Retail OCC subsegment accounted for a dominant 38% share of the global Old Corrugated Container (OCC) market in 2024. This leadership is primarily attributed to the high and consistent generation of corrugated waste from supermarkets, hypermarkets, e-commerce fulfillment centers, warehouses, and large-format retail outlets. These sources generate clean, uniform, and high-volume OCC, making collection efficient and economically viable. The rapid growth of organized retail and last-mile logistics globally has further strengthened this segment’s contribution, particularly in North America, Europe, and Asia-Pacific.

The Residential OCC subsegment is projected to be the fastest-growing, expanding at a CAGR of approximately 6.2% from 2025 to 2030. This growth is driven by increasing urbanization, expansion of curbside recycling programs, and government initiatives aimed at improving household waste segregation. Rising e-commerce penetration at the household level has significantly increased corrugated box usage, boosting residential OCC volumes despite higher contamination challenges.

By Grade / Quality

The Standard OCC subsegment held the largest share, accounting for approximately 54% of the global OCC market in 2024. Its dominance stems from its wide availability and balanced fiber quality, making it suitable for most containerboard manufacturing applications. Standard OCC is heavily utilized by linerboard and fluting producers due to its cost-effectiveness and compatibility with existing pulping processes, especially in high-volume mills.

The Premium OCC (High Kraft Content) subsegment is expected to register the fastest growth rate at a CAGR of 5.8% during 2025–2030. Demand is being fueled by containerboard manufacturers seeking higher-strength recycled fiber to improve box performance while maintaining recycled content targets. Export markets, particularly in Asia-Pacific, increasingly prefer premium-grade OCC due to lower contamination levels and higher yield efficiency.

By Collection & Processing Type

The Baled OCC subsegment dominated the market with a 67% share in 2024, driven by its logistical advantages, ease of handling, and suitability for both domestic transportation and international export. Baled OCC reduces storage space, minimizes handling losses, and improves freight efficiency, making it the preferred format for large recycling processors and exporters.

The Sorted & Clean OCC subsegment is projected to be the fastest-growing, with a CAGR of 6.5% from 2025 to 2030. Growth is supported by increased adoption of automated sorting technologies and stricter quality requirements from containerboard mills. Clean OCC commands premium pricing, especially in export markets, incentivizing investments in advanced material recovery facilities.

By End-Use Application

The Containerboard Manufacturing subsegment accounted for a dominant 72% share of total OCC consumption in 2024. This overwhelming share is due to OCC’s role as the primary recycled fiber input for linerboard and corrugated medium production. Growth in e-commerce, food & beverage packaging, and industrial goods shipping continues to drive containerboard demand, directly supporting OCC consumption across all major regions.

The Molded Fiber & Pulp Packaging subsegment is expected to witness the fastest growth, at a CAGR of 7.0% from 2025 to 2030. This expansion is driven by increasing substitution of plastic packaging with fiber-based alternatives in foodservice, electronics, and consumer goods. OCC-based molded pulp products are gaining traction due to their recyclability, biodegradability, and alignment with sustainability goals.

By Trade Flow

The Domestic Consumption subsegment represented approximately 61% of global OCC demand in 2024, supported by strong internal recycling ecosystems in North America, Europe, and China. Domestic utilization reduces transportation costs and supply chain risks while supporting national circular economy objectives.

The Export-Oriented OCC subsegment is projected to grow at the fastest CAGR of 5.9% from 2025 to 2030, driven by persistent fiber deficits in Asia-Pacific, particularly in India and Southeast Asia. Export demand for high-quality OCC remains strong despite regulatory fluctuations, as emerging economies continue to expand containerboard capacity faster than domestic fiber recovery systems.

Old Corrugated Container Market Segmentations

By Source of Generation

- Commercial & Retail OCC

- Industrial & Manufacturing OCC

- Residential OCC

- Institutional OCC

By Grade / Quality

- Premium OCC (High Kraft Content)

- Standard OCC

- Low-Grade / Contaminated OCC

- By Collection & Processing Type

Baled OCC

- Loose / Unbaled OCC

- Sorted & Clean OCC

- Mixed Paper Streams (OCC-Dominant)

By End-Use Application

- Containerboard Manufacturing

- Paperboard & Cartonboard

- Molded Fiber & Pulp Packaging

- Other Recycled Paper Products

By Trade Flow

- Domestic Consumption

- Export-Oriented OCC

Regional Analysis

North America

North America remains one of the most influential regions in the OCC market, accounting for approximately 28% of global demand in 2024. The United States dominates regional activity due to high per-capita packaging consumption, advanced recycling infrastructure, and strong domestic containerboard production. U.S.-generated OCC also supports global supply through exports to the Asia-Pacific, particularly India and Southeast Asia. Canada contributes steadily through industrial and commercial OCC streams, supported by strong sustainability regulations. Regional demand is further reinforced by large-scale e-commerce activity and food & beverage packaging growth.

Europe

Europe represents around 21% of global OCC demand, driven by strict recycling targets, landfill bans, and extended producer responsibility frameworks. Countries such as Germany, the United Kingdom, France, Italy, and Spain lead OCC consumption and recovery. European paper mills increasingly rely on domestically recovered OCC, reducing export volumes but strengthening internal supply chains. Demand growth is supported by sustainable packaging adoption, retail logistics expansion, and investments in circular material systems. Eastern Europe is emerging as a growth zone due to improving waste collection infrastructure and rising industrial output.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing region in the OCC market, accounting for nearly 42% of global demand in 2024. China, despite tightening import controls, remains a major consumer through domestic recovery and alternative fiber sourcing. India is the fastest-growing OCC market globally, supported by rapid containerboard capacity expansion, urbanization, and e-commerce growth. Southeast Asian countries such as Vietnam, Indonesia, Thailand, and Malaysia are increasing OCC imports due to limited domestic recovery rates. Japan and South Korea represent mature but stable markets with high-quality recycling systems. Structural fiber deficits across the region continue to drive long-term OCC demand growth.

Latin America

Latin America accounts for approximately 6% of global OCC demand, with Brazil and Mexico leading regional consumption. Growth is supported by rising packaging demand from the food, beverage, and consumer goods industries. Recycling infrastructure remains uneven across the region, but government-led initiatives and private investments are gradually improving OCC recovery rates. Export opportunities are emerging as quality standards improve, particularly for baled and sorted OCC.

Middle East & Africa

The Middle East & Africa region represents around 3% of global demand, with growth concentrated in the UAE, Saudi Arabia, South Africa, and Egypt. Packaging demand driven by food imports, retail expansion, and industrial development is supporting OCC consumption. Several countries are investing in waste management and recycling capacity to reduce landfill dependency, creating long-term growth opportunities. Africa’s recycling market remains underpenetrated, offering future upside as urbanization and formal collection systems expand.

Competitive Landscape

The OCC market is moderately fragmented, with the top five companies accounting for approximately 24% of global market share. Large integrated paper and packaging companies dominate due to their captive supply chains, recycling infrastructure, and scale advantages. Regional recyclers and processors play a significant role in local markets, particularly in collection and baling activities. Competition is primarily driven by pricing efficiency, quality consistency, logistics reach, and long-term supply contracts with containerboard mills.

Key Players in the Old Corrugated Container Market

- Smurfit Westrock

- International Paper

- DS Smith

- Pratt Industries

- Nine Dragons Paper

- Oji Holdings

- Lee & Man Paper

- Mondi Group

- UPM

- Cascades

- Stora Enso

- WestRock Recycling

- Sappi

- Georgia-Pacific

- Rengo Co., Ltd.