Octabin Market Size and Growth

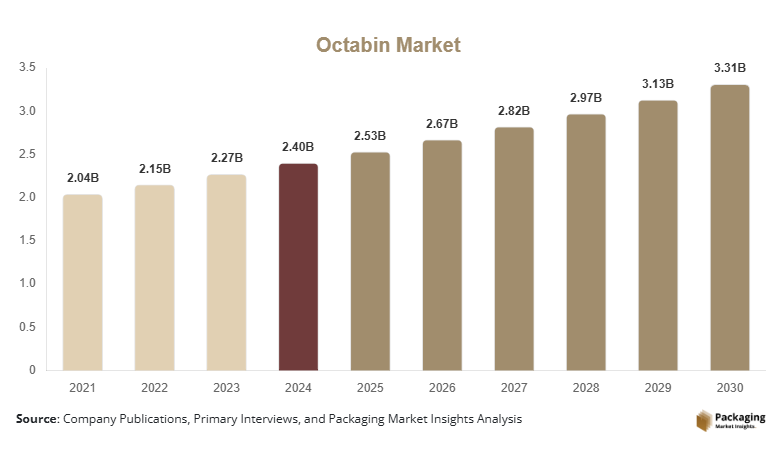

The global octabin market size was valued at USD 2.40 billion in 2024 and is projected to grow from USD 2.53 billion in 2025 to reach approximately USD 3.31 billion by 2030, expanding at a CAGR of around 5.5% during the forecast period (2025–2030).

The octabin market growth is primarily driven by rising demand for cost-efficient bulk packaging, increasing export-oriented manufacturing activities, and the growing preference for recyclable and fiber-based industrial packaging solutions across chemicals, food ingredients, agriculture, and polymer industries.

Octabins have emerged as a preferred alternative to rigid plastic bins and drums due to their superior load-bearing capacity, collapsibility, and sustainability advantages. As global supply chains increasingly prioritize logistics efficiency and environmental compliance, octabins are gaining strong traction in both developed and emerging economies.

Key Market Insights

- Sustainability-driven packaging substitution is accelerating, with octabins increasingly replacing plastic and metal bulk containers across regulated industries.

- Heavy-duty corrugated octabins dominate global demand, particularly in chemicals, plastics, and fertilizers, due to their high stacking strength and export compatibility.

- Asia-Pacific leads global consumption, supported by large-scale manufacturing, strong export volumes, and expanding industrial clusters in China and India.

- Food and beverage ingredient applications are the fastest-growing segment, driven by rising global trade of starches, sweeteners, cocoa powders, and additives.

- Customized liners and barrier coatings are becoming a key differentiation factor, enabling octabins to penetrate moisture-sensitive and high-value applications.

- Direct manufacturer-to-end-user sales dominate, reflecting the contract-based nature of industrial bulk packaging procurement.

Explore more data points, trends and opportunities Download Free Sample Report

Market Latest Trend

Sustainability-Led Bulk Packaging Adoption Gaining Momentum

The octabin market is witnessing a strong shift toward sustainability-led packaging solutions as regulatory pressure mounts against single-use plastics and non-recyclable industrial packaging. Manufacturers and exporters are increasingly adopting octabins made from recycled or mixed fiber board to meet corporate ESG goals and comply with evolving environmental standards. Light weighting innovations, FSC-certified paper usage, and improved recyclability are becoming standard requirements rather than optional features.

Market Drivers

Growth in Bulk Chemical & Polymer Trade

The global specialty chemicals and polymer industries have seen strong post-pandemic recovery, driving higher bulk exports. Octabins offer superior stacking strength and space efficiency compared to bags and drums, making them the preferred solution for international shipments.

Cost & Logistics Efficiency

Octabins reduce packaging costs by 15–30% compared to rigid containers and optimize container utilization due to collapsibility. This has significantly improved adoption among cost-sensitive exporters and contract manufacturers.

Market Restraint

Moisture Sensitivity in High-Humidity Regions

Without advanced coatings or liners, octabins can be susceptible to moisture damage, limiting adoption in certain climates and applications. Fluctuations in virgin and recycled kraft paper prices directly impact manufacturing costs, pressuring margins for small and mid-sized producers.

At the same time, buyers are demanding packaging solutions that reduce logistics costs without compromising product safety. Octabins offer superior cube efficiency in containers and warehouses, reducing freight costs and carbon emissions per shipment. As a result, the octabin market is transitioning from a commodity packaging segment to a value-engineered solution focused on sustainability, performance, and compliance.

Market Opportunities

Sustainability-Driven Packaging Substitution

Global regulations targeting plastic reduction and carbon footprint optimization are accelerating the shift from rigid plastic bins and drums to corrugated octabins. Governments and multinational buyers are actively mandating recyclable and FSC-certified packaging, creating a strong opportunity for octabin manufacturers offering 100% recyclable, high-strength designs. Companies investing in recycled fiber optimization and lightweighting technologies stand to gain long-term contracts from export-driven industries.

Rising Export-Oriented Manufacturing in APAC

Asia-Pacific’s role as a global manufacturing and export hub particularly for chemicals, polymers, fertilizers, and food ingredients presents a substantial opportunity. Countries such as China, India, Vietnam, and Indonesia are witnessing increased demand for bulk export packaging compliant with international logistics and safety standards. Localized octabin manufacturing near ports and industrial clusters can significantly reduce logistics costs, offering a competitive advantage.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2024 | USD 2.40 Billion |

| Market Size in 2025 | USD 2.53 Billion |

| Market Size in 2030 | USD 3.31 Billion |

| CAGR | 5.5% (2025-2030) |

| Base Year for Estimation | 2024 |

| Historical Data | 2021-2023 |

| Forecast Period | 2025-2030 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Product Type

The heavy-duty corrugated octabins (double- and triple-wall) subsegment accounted for the largest share of approximately 42% of the global octabin market in 2024. This dominance is primarily attributed to their superior load-bearing capacity, structural stability, and suitability for bulk handling of high-density materials such as chemicals, resins, fertilizers, and minerals. Heavy-duty octabins are widely adopted for export-oriented applications where stacking strength, long-distance transportation resilience, and warehouse efficiency are critical requirements. Their compatibility with forklifts and palletized logistics further strengthens their position as the preferred choice among industrial users.

The laminated and coated octabins subsegment is projected to be the fastest-growing, registering a CAGR of approximately 8.6% from 2025 to 2030. This growth is driven by increasing demand for moisture-resistant, grease-resistant, and chemical-resistant packaging solutions, particularly from food ingredient exporters and specialty chemical manufacturers. Enhanced barrier performance and extended product protection are making laminated octabins increasingly attractive for high-value and sensitive bulk goods.

By Capacity Range

Octabins with a capacity of 1,000–1,500 kg held the largest market share of around 38% in 2024, making them the most widely used capacity range globally. This segment’s leadership stems from its optimal balance between high-volume storage and manageable handling efficiency. Industries such as chemicals, plastics, and agriculture prefer this capacity range due to its compatibility with standard container dimensions, forklifts, and automated warehouse systems, enabling efficient logistics and cost savings.

The above 1,500 kg capacity segment is anticipated to grow at the fastest CAGR of nearly 8.2% during the forecast period, fueled by rising demand for ultra-bulk packaging in mining additives, pigments, fertilizers, and industrial raw materials. As manufacturers aim to reduce packaging units per shipment and improve freight economics, higher-capacity octabins are gaining increased traction.

By Material Composition

The mixed fiber board subsegment, which combines virgin and recycled fibers, accounted for approximately 46% of the global market in 2024, making it the dominant material category. This leadership is driven by its ability to balance sustainability objectives with mechanical strength requirements. Mixed fiber octabins offer cost efficiency while meeting regulatory and corporate ESG standards, making them particularly attractive to large exporters and multinational buyers.

The recycled corrugated board segment is expected to experience the highest growth rate, expanding at a CAGR of around 8.9% between 2025 and 2030. This growth is supported by increasing regulatory pressure to reduce virgin material usage, rising availability of high-quality recycled fibers, and growing customer preference for circular packaging solutions.

By Liner & Closure Type

Octabins with PE liners represented the largest share of approximately 40% in 2024, driven by their widespread use in moisture-sensitive and contamination-prone applications. PE liners provide effective protection against humidity, dust, and leakage, making them essential for chemicals, food ingredients, and agricultural products. Their relatively low cost and ease of integration have contributed to their extensive adoption across industries.

The custom and functional liner segment is projected to grow at the fastest CAGR of about 9.1%, supported by increasing demand for antistatic, oxygen-barrier, food-grade, and chemical-resistant liners. High-value industries such as pharmaceuticals, specialty chemicals, and nutraceuticals are driving this trend as product safety and regulatory compliance become increasingly critical.

By End-Use Industry

The chemicals and specialty chemicals segment accounted for the largest share of nearly 34% of the global octabin market in 2024. This dominance is due to the high volume of bulk chemical exports, stringent packaging requirements, and the need for durable, stackable, and cost-efficient containers. Octabins are extensively used for pigments, additives, intermediates, and specialty formulations, making chemicals the backbone of market demand.

The food and beverage ingredients segment is expected to be the fastest-growing end-use, with a projected CAGR of approximately 8.7% from 2025 to 2030. Growth is driven by rising global trade in starches, cocoa powders, sugar substitutes, and nutritional ingredients, along with increasing demand for hygienic, food-grade, and export-compliant bulk packaging solutions.

By Distribution Channel

Direct sales from manufacturers to end users accounted for the largest share of around 48% in 2024, reflecting the contract-based nature of industrial bulk packaging procurement. Large chemical, food, and agricultural companies prefer direct sourcing to ensure consistent quality, customization, and long-term supply reliability.

The industrial export packaging contracts segment is anticipated to grow at the highest CAGR of approximately 8.4%, supported by increasing cross-border trade, third-party logistics partnerships, and turnkey export packaging solutions. As exporters seek integrated packaging and logistics support, this channel is gaining strategic importance within the global octabin market.

Octabin Market Segmentations

By Product Type

- Standard Corrugated Octabins (Single-Wall)

- Heavy-Duty Corrugated Octabins (Double/Triple-Wall)

- Laminated / Coated Octabins

- Hybrid Octabins (Corrugated + Reinforcement)

By Capacity Range

- Below 500 kg

- 500–1,000 kg

- 1,000–1,500 kg

- Above 1,500 kg

By Material Composition

- Virgin Kraft Paperboard

- Recycled Corrugated Board

- Mixed Fiber Board

By Liner & Closure Type

- Without Liner

- With PE Liner

- With Aluminum Foil / Barrier Liner

- Custom & Functional Liners

By End-Use Industry

- Chemicals & Specialty Chemicals

- Food & Beverage Ingredients

- Agriculture & Fertilizers

- Pharmaceuticals & Nutraceuticals

- Plastics & Resins

- Minerals, Pigments & Additives

By Distribution Channel

- Direct Sales (Manufacturer to End User)

- Packaging Solution Integrators

- Industrial Export Packaging Contracts

Regional Analysis

North America

North America remains one of the largest consumers of octabins, driven primarily by the United States and Canada. The region accounts for roughly 24% of global demand in 2024, supported by strong chemical, agricultural input, and polymer industries. High awareness of sustainable packaging, coupled with strict regulatory compliance requirements, has accelerated the adoption of corrugated bulk containers. Demand in North America is largely export-driven, with octabins used extensively for shipping chemicals, resins, and food ingredients to Europe and Asia.

Europe

Europe represents approximately 21% of the global octabin market, with Germany, France, the Netherlands, and the U.K. leading regional demand. European buyers are highly receptive to recyclable and low-carbon packaging solutions, making octabins an attractive alternative to rigid bulk containers. The region is also one of the fastest adopters of laminated and coated octabins, particularly for specialty chemicals and food-grade applications. Sustainability mandates and circular economy policies continue to reinforce long-term demand.

Asia-Pacific

Asia-Pacific is the largest and fastest-growing regional market, accounting for nearly 45% of global demand in 2024. China alone contributes around 22%, followed by India at approximately 11%. Rapid industrialization, expanding chemical and fertilizer exports, and rising food ingredient trade are key growth drivers. India is the fastest-growing national market, supported by government initiatives such as “Make in India,” increased manufacturing investments, and rising export packaging requirements.

Latin America

Latin America accounts for about 6% of global demand, with Brazil and Mexico as key markets. Growth is driven by fertilizer exports, agri-commodities, and food ingredients. While adoption remains lower than in Asia or Europe, increasing export activity and infrastructure development are gradually expanding octabin usage across the region.

Middle East & Africa

The Middle East & Africa region holds around 4% of the global market, with demand concentrated in the GCC countries and South Africa. Chemical exports, mining, and specialty materials are the primary end uses. Intra-regional trade and export-focused packaging demand are expected to support steady growth.

Competitive Landscape

The octabin market is moderately fragmented, with the top five players collectively accounting for approximately 38% of global market share. Large multinational paper and packaging companies dominate high-volume contracts and export-oriented customers, while regional players serve localized demand. Competitive intensity remains high, with pricing closely linked to kraft paper costs and customization capabilities. Companies offering heavy-duty, liner-integrated, and sustainable octabin solutions are consistently outperforming commodity-focused manufacturers.

Key Players in the Global Octabin Market

- Smurfit Westrock

- International Paper

- Mondi Group

- DS Smith

- Packaging Corporation of America

- Stora Enso

- Pratt Industries

- Nine Dragons Paper

- Oji Holdings

- Rengo Co.

- Lee & Man Paper

- Georgia-Pacific

- Klabin

- SCG Packaging

- Nippon Paper Industries