Nordic Pouch Packaging Market Size and Growth

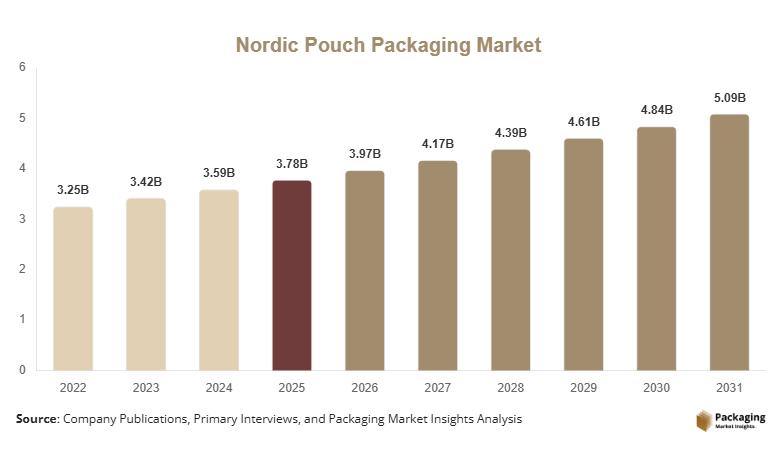

The Nordic pouch packaging market size was valued at USD 3.78 billion in 2024 and is projected to grow from USD 3.97 billion in 2025 to reach approximately USD 5.09 billion by 2030, expanding at a CAGR of 5.1% during the forecast period (2025–2030). The Nordic pouch packaging market growth is primarily driven by the rapid expansion of smokeless nicotine products, increasing adoption of sustainable and paper-based packaging solutions, and rising demand for high-barrier, hygienic, and discreet pouch formats across food, pharmaceutical, and personal care applications.

Nordic pouch packaging has evolved from a niche regional solution into a globally traded flexible packaging format. Originally developed for smokeless tobacco in Nordic countries, these pouches are now widely used in nicotine alternatives, nutraceuticals, oral care, and functional food applications. Manufacturers are increasingly focusing on lightweight materials, recyclable structures, and advanced barrier coatings to meet both regulatory and brand-owner sustainability goals. As consumption patterns shift toward discreet, on-the-go usage formats, Nordic pouch packaging is gaining strategic importance within the global flexible packaging industry.

Key Market Insights

- Nordic pouch packaging is increasingly shifting toward paper-based, bio-coated, and recyclable structures, driven by global sustainability mandates and plastic reduction regulations.

- Smokeless nicotine and tobacco-free pouch products dominate demand, accounting for over half of the total global market value.

- High-barrier Nordic pouches lead the market, supported by export-driven demand and shelf-life requirements for nicotine and pharmaceutical products.

- Europe remains the largest regional market, reflecting strong consumption in Sweden, Norway, Germany, and the UK.

- North America is the fastest-growing major market, driven by the rapid adoption of nicotine pouches in the United States and Canada.

- Asia-Pacific is emerging as a critical manufacturing and demand hub, supported by cost-efficient production, expanding exports, and rising domestic consumption.

Explore more data points, trends and opportunities Download Free Sample Report

Market Latest Trends

Sustainability-Driven Material Innovation Gaining Momentum

Sustainability has become the defining trend shaping the Nordic pouch packaging market. Manufacturers are rapidly transitioning toward paper-based and bio-derived pouch structures that reduce plastic content while maintaining functional performance. Water-based barrier coatings, compostable linings, and recyclable hybrid laminates are increasingly replacing traditional plastic-heavy materials. These innovations are particularly important for nicotine pouch brands seeking compliance with extended producer responsibility frameworks and eco-labeling requirements. Packaging suppliers that can balance sustainability with moisture and aroma protection are gaining a competitive advantage, especially in premium product categories.

Advanced Barrier Technologies

High-barrier pouches are becoming standard for export-oriented nicotine products, pharmaceuticals, and nutraceuticals, where protection from oxygen, moisture, and UV exposure is critical. At the same time, digital printing and customization capabilities are being integrated to support brand differentiation, short production runs, and regulatory labeling flexibility across multiple geographies.

Market Drivers

Rapid Growth of Smokeless Nicotine and Tobacco-Free Pouch Products Globally

As consumers increasingly shift away from combustible tobacco, nicotine pouches offer a discreet, odorless alternative. Nordic pouch packaging is essential to these products due to its precise portioning, moisture control, and hygienic handling. This has resulted in sustained demand growth across North America and Europe, with Asia-Pacific emerging as a high-growth region.

Accelerated Adoption of Sustainable Packaging Materials

Brand owners are under increasing pressure to meet sustainability targets, driving demand for paper-based and bio-coated Nordic pouches. Advances in water-based barrier coatings and recyclable laminates have enabled manufacturers to replace plastic-heavy structures without compromising performance, significantly expanding the addressable market size.

Market Restraints

Volatility in Raw Material Prices

Particularly, paper pulp, aluminum foil, and specialty coatings. Fluctuating input costs can compress margins, especially for manufacturers operating under long-term supply contracts. Sudden bans or classification changes can impact downstream demand, creating short-term market instability for packaging suppliers.

Market Opportunities

Regulatory-Driven Transition Toward Plastic-Free and Fiber-Based Packaging Solutions

Governments across Europe, North America, and parts of the Asia-Pacific are implementing extended producer responsibility (EPR) frameworks and single-use plastic bans. This creates a strong opening for Nordic pouch manufacturers to commercialize paper-based and bio-coated pouch structures that meet recyclability and compostability standards while retaining barrier performance. Existing players can gain pricing premiums by offering certified sustainable solutions, while new entrants can position themselves as eco-first suppliers.

Geographic Expansion of Nicotine Pouch Consumption Beyond Traditional Nordic Markets

Countries such as the United States, Canada, Japan, South Korea, and select Middle Eastern markets are witnessing double-digit growth in smokeless nicotine adoption due to reduced-risk perceptions and smoking bans. This directly fuels demand for Nordic pouch packaging, particularly in high-barrier, moisture-controlled formats. Local manufacturing partnerships and export-oriented production hubs in the Asia-Pacific present a cost-efficient route to serve these emerging demand centers.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.78 Billion |

| Market Size in 2026 | USD 3.97 Billion |

| Market Size in 2031 | USD 5.09 Billion |

| CAGR | 5.1% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | Nordic |

| Countries Covered |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

The paper–plastic hybrid Nordic pouches subsegment accounted for the largest share of the Nordic pouch packaging market, representing approximately 42% of total market value in 2024. This dominance is primarily attributed to the optimal balance these structures offer between mechanical strength, moisture and aroma barrier performance, and partial sustainability compliance. Paper–plastic hybrids are extensively used in smokeless nicotine and food applications, where full paper solutions are not yet technically viable at scale. Their compatibility with existing pouching machinery and cost efficiency has further reinforced their widespread adoption globally.

The bio-based and compostable Nordic pouches subsegment is projected to be the fastest-growing, registering an estimated CAGR of 13.2% from 2025 to 2033. This rapid growth is driven by tightening regulations on plastic usage, increasing brand commitments toward carbon neutrality, and rising consumer preference for environmentally responsible packaging. Advances in bio-coatings and compostable barrier technologies are enabling wider commercial adoption, particularly in Europe and premium product categories, positioning this subsegment for accelerated expansion.

By Barrier Performance

The high-barrier Nordic pouches subsegment held a dominant 48% share of the global market in 2024, driven by strong demand from smokeless nicotine, pharmaceutical, and nutraceutical applications. High-barrier pouches provide superior protection against oxygen, moisture, aroma loss, and UV exposure, making them essential for products with longer shelf-life requirements and export-oriented distribution. The growth of cross-border trade in nicotine pouches has further amplified demand for high-barrier packaging solutions.

The medium-barrier Nordic pouches subsegment is expected to witness the fastest growth, with a projected CAGR of 11.5% during 2025–2033. This growth is fueled by increasing use in food, functional ingredients, and personal care applications, where moderate protection is sufficient and cost optimization is a key priority. Manufacturers are increasingly developing medium-barrier solutions with improved recyclability, enhancing their attractiveness across multiple end-use industries.

By Product Format

The stand-up Nordic pouches subsegment accounted for approximately 37% of the Nordic pouch packaging market in 2024, making it the leading product format. This strong position is driven by superior shelf visibility, ease of handling, and enhanced branding space, which are particularly important in retail-oriented nicotine and consumer goods segments. Stand-up pouches also support resealability and ergonomic designs, further increasing their appeal to brand owners.

The resealable Nordic pouches subsegment is projected to grow at the fastest pace, achieving a CAGR of 12.4% from 2025 to 2033. Rising consumer preference for portion control, freshness retention, and repeated usage is accelerating demand for resealable formats. This trend is especially prominent in premium nicotine products and nutraceutical applications, where convenience and product integrity are critical purchasing factors.

By Capacity Range

The 100–250 grams capacity range dominated the market, accounting for nearly 40% of global demand in 2024. This segment aligns closely with typical consumer usage cycles for nicotine pouches and small-format food and nutraceutical products. Regulatory packaging norms and ease of transportation further support the widespread adoption of this capacity range across global markets.

The below 100 grams subsegment is anticipated to be the fastest-growing, with an estimated CAGR of 12.8% during the forecast period. Growth in this segment is driven by increasing demand for single-use, trial-size, and on-the-go consumption formats, particularly among first-time users and premium product launches. Brand owners are increasingly leveraging smaller pack sizes to enhance affordability and market penetration.

By End-Use Industry

The smokeless tobacco and nicotine products subsegment represented the largest share of the Nordic pouch packaging market, accounting for approximately 55% of total market value in 2024. This dominance reflects the core application of Nordic pouches, driven by rapid global adoption of nicotine pouches as a smoke-free alternative. Continuous product innovation, expanding regulatory acceptance, and aggressive market expansion by nicotine brands are sustaining strong packaging demand.

The pharmaceuticals and nutraceuticals subsegment is projected to be the fastest-growing end-use category, registering a CAGR of 12.0% from 2025 to 2033. This growth is supported by rising demand for hygienic, unit-dose packaging formats, increasing consumption of dietary supplements, and the need for precise dosing and contamination protection. As healthcare and wellness trends continue to strengthen globally, this segment is expected to play an increasingly important role in shaping future Nordic pouch packaging demand.

Nordic Pouch Packaging Market Segmentations

By Material Type

- Paper-Based Nordic Pouches

- Paper–Plastic Hybrid Nordic Pouches

- Bio-Based & Compostable Nordic Pouches

- Aluminum-Lined Nordic Pouches

By Barrier Performance

- Low-Barrier Nordic Pouches

- Medium-Barrier Nordic Pouches

- High-Barrier Nordic Pouches

By Product Format

- Flat Nordic Pouches

- Stand-Up Nordic Pouches

- Shaped / Ergonomic Nordic Pouches

- Resealable Nordic Pouches

By Capacity Range

- Below 100 grams

- 100–250 grams

- 250–500 grams

- Above 500 grams

By End-Use Industry

- Smokeless Tobacco & Nicotine Products

- Food & Beverage

- Pharmaceuticals & Nutraceuticals

- Cosmetics & Personal Care

- Industrial & Specialty Applications

Competitive Landscape

The Nordic pouch packaging market share is moderately consolidated, with the top five players accounting for approximately 45–50% of total market value. Large multinational packaging companies dominate high-volume and export-oriented segments due to their advanced material capabilities, global manufacturing footprints, and long-term contracts with nicotine and consumer goods brands. Smaller and regional players remain competitive in niche applications and localized markets, particularly where customization and flexibility are critical.

Key Players in the Nordic Pouch Packaging Market

- Amcor

- Mondi Group

- Huhtamaki

- Berry Global

- Smurfit Kappa

- DS Smith

- Constantia Flexibles

- UPM Specialty Papers

- WestRock

- Stora Enso

- Sealed Air

- ProAmpac

- Glenroy

- Coveris

- Klöckner Pentaplast