Multi Layer Blown Films Market Size and Growth

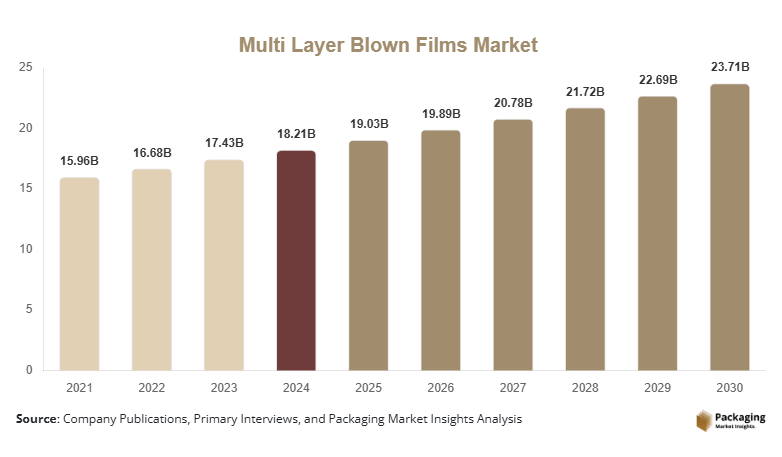

The global multi layer blown films market size was valued at USD 18.21 billion in 2024 and is projected to grow from USD 19.03 billion in 2025 to reach USD 23.71 billion by 2030, expanding at a CAGR of 4.5% during the forecast period (2025–2030). The multi layer blown films market growth is primarily driven by the increasing adoption of flexible packaging across food and beverage, pharmaceutical, and industrial applications, rising demand for high-barrier and downgauged films, and continuous advancements in co-extrusion and polymer engineering technologies.

Multi layer blown films are increasingly replacing mono-layer films due to their superior mechanical strength, enhanced oxygen and moisture barrier properties, and material efficiency. The market is also benefiting from growing global trade in packaged foods, the expansion of cold-chain logistics, and the rising emphasis on sustainable packaging structures. Emerging economies are witnessing strong demand growth supported by urbanization, modern retail expansion, and export-oriented manufacturing, while developed regions are focusing on recyclable, mono-material, and high-performance multilayer film solutions.

Key Market Insights

- Multi-layer blown films are increasingly shifting toward recyclable and mono-material structures, helping brand owners meet sustainability targets without compromising performance.

- Five-layer and seven-layer blown films dominate demand globally, offering an optimal balance between barrier performance, cost efficiency, and downgauging capability.

- Asia-Pacific dominates global consumption, supported by strong packaging demand from China, India, and Southeast Asia.

- North America remains a high-value market, driven by advanced food processing, pharmaceutical manufacturing, and technological adoption.

- Europe is the fastest-growing innovation hub, led by stringent recycling regulations and rapid adoption of circular packaging solutions.

- Technological integration, including AI-enabled extrusion control, high-output blown film lines, and advanced resin formulations, is reshaping production efficiency and product consistency.

Explore more data points, trends and opportunities Download Free Sample Report

Latest Market Trends

Shift Toward High-Barrier and Sustainable Film Structures

Manufacturers are increasingly focusing on high-barrier multi layer blown films that extend shelf life while reducing overall material usage. The use of advanced barrier layers such as EVOH, polyamide, and functionalized polyethylene is becoming more common, especially in food and pharmaceutical packaging. At the same time, the market is witnessing a strong push toward recyclable structures, with converters redesigning multilayer films to remain within polyethylene-based families. This trend is accelerating adoption among global FMCG brands seeking compliance with evolving packaging waste regulations.

Market Drivers

Rapid Expansion of the Flexible Food Packaging Industry

Rising consumption of packaged, frozen, and ready-to-eat foods has increased the need for films offering superior oxygen, moisture, and aroma barriers. Multi layer blown films outperform mono-layer alternatives by combining multiple functional properties, making them the preferred choice for food manufacturers globally.

Material Efficiency and Downgauging Trends

Brand owners and converters are increasingly focused on reducing material usage without compromising performance. Multi layer blown films enable downgauging by distributing mechanical strength across layers, reducing overall resin consumption and lowering transportation costs. This aligns with both cost-reduction strategies and sustainability objectives.

Market Restraint

Volatile raw material prices

Particularly, polyethylene and specialty resins such as EVOH and polyamide. Fluctuations in crude oil prices directly impact production costs and profit margins for manufacturers. Another restraint is regulatory pressure on plastic usage, especially in Europe and parts of North America. While multilayer films offer performance advantages, recycling complexity remains a concern. Companies must invest heavily in R&D to ensure compliance, which may slow adoption in price-sensitive markets.

Market Opportunities

Transition toward Recyclable and Mono-Material Multilayer Structures

Governments across Europe, North America, and parts of Asia-Pacific are tightening regulations on non-recyclable plastic packaging. This has created strong demand for innovative blown film structures that maintain barrier and mechanical performance while using compatible polymer families. Companies that invest in recyclable PE-based multilayer films or EVOH-replacement technologies are well-positioned to capture premium contracts from global food and FMCG brands.

Rising demand from export-oriented Food and Pharmaceutical Manufacturing Hubs

Particularly in Asia-Pacific and Latin America. Countries such as India, Vietnam, Thailand, Brazil, and Mexico are expanding food processing and pharmaceutical exports, requiring high-barrier, contamination-resistant packaging. Multi layer blown films are increasingly preferred due to their ability to extend shelf life and withstand long-distance transportation. New entrants establishing localized manufacturing or technical partnerships in these regions can benefit from lower production costs and rising domestic consumption.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2024 | USD 18.21 Billion |

| Market Size in 2025 | USD 19.03 Billion |

| Market Size in 2030 | USD 23.71 Billion |

| CAGR | 4.5% (2025-2030) |

| Base Year for Estimation | 2024 |

| Historical Data | 2021-2023 |

| Forecast Period | 2025-2030 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Resin Type

The Polyethylene (PE) subsegment accounted for a dominant approximately 62% share of the global multi layer blown films market in 2024. This leadership is primarily attributed to polyethylene’s versatility, cost-effectiveness, and compatibility with multi-layer co-extrusion processes. PE resins, particularly LLDPE and LDPE, offer excellent flexibility, puncture resistance, and sealability, making them the preferred choice for food packaging, industrial liners, and consumer goods applications. Additionally, the growing focus on recyclable mono-material packaging has further strengthened the adoption of PE-based multilayer films, as they align well with existing recycling streams and regulatory requirements.

The Ethylene Vinyl Alcohol (EVOH) subsegment is projected to be the fastest-growing resin category, registering an estimated CAGR of 8.6% from 2025 to 2030. This growth is driven by increasing demand for high-barrier packaging in food, pharmaceutical, and medical applications, where oxygen sensitivity is critical. EVOH’s superior oxygen barrier properties significantly extend product shelf life, particularly in meat, dairy, and ready-to-eat food packaging. As global food exports and pharmaceutical production expand, EVOH-containing multilayer films are gaining traction despite their higher cost, positioning this subsegment for accelerated growth.

By Application

The Packaging application segment held the largest share, accounting for nearly 55% of the global multi layer blown films market in 2024. This dominance is driven by widespread use in food and beverage packaging, pharmaceutical packaging, and consumer goods protection. Multi layer blown films are extensively adopted in pouches, bags, liners, and lamination structures due to their ability to combine barrier performance, mechanical strength, and downgauging benefits. Rising consumption of packaged foods, growth of e-commerce, and increasing demand for shelf-stable packaging continue to reinforce the packaging segment’s leading position globally.

The Medical and Healthcare application segment is expected to witness the fastest growth, expanding at an estimated CAGR of 9.1% from 2025 to 2030. This rapid growth is fueled by rising healthcare expenditure, increased pharmaceutical manufacturing, and heightened focus on hygiene and contamination prevention. Multi layer blown films are widely used in medical device packaging, pharmaceutical pouches, and protective medical covers due to their excellent moisture and microbial barrier properties. The expansion of global healthcare infrastructure and growing demand for sterile, high-performance packaging solutions are key factors accelerating growth in this segment.

Multi Layer Blown Films Market Segmentations

By Resin Type

- Polyethylene (PE)

- Polypropylene (PP)

- Ethylene Vinyl Alcohol (EVOH)

- Polyamide (Nylon)

- Polybutylene Terephthalate (PBT)

By Application

- Packaging

- Agriculture

- Medical and Healthcare

- Automotive

- Construction

Regional Analysis

North America

North America holds about 23% share, with the U.S. dominating due to advanced packaging technologies and strong food processing industries. Europe accounts for roughly 21%, led by Germany, France, and Italy, with strong emphasis on sustainable packaging. The multi layer blown films market in North America remains one of the most technologically advanced, with strong demand from food, healthcare, and industrial packaging sectors. The U.S. accounts for the majority of regional consumption, supported by high packaged food penetration, stringent quality standards, and continuous investment in high-speed extrusion lines. Demand is increasingly shifting toward downgauged, high-performance films that reduce logistics costs while maintaining durability. Pharmaceutical and medical packaging applications are also expanding rapidly, reinforcing long-term demand stability in the region.

Europe

Europe represents a critical growth and innovation region for the multi layer blown films market, led by Germany, France, Italy, and the U.K. The region is highly driven by sustainability mandates, recycling targets, and circular economy initiatives. European converters are early adopters of mono-material multilayer designs and advanced barrier alternatives. Growth is also supported by strong demand from premium food packaging, dairy products, meat processing, and pharmaceutical exports. Eastern Europe is emerging as a manufacturing hub due to lower production costs and increasing foreign investments in packaging infrastructure.

Asia-Pacific

Asia-Pacific is the largest and fastest-expanding regional market for multi layer blown films, accounting for the highest share of global demand. China leads regional consumption due to its massive food processing, consumer goods, and export packaging industries. India is witnessing rapid growth driven by packaged food expansion, pharmaceutical manufacturing, and government initiatives such as Make in India. Southeast Asian countries including Vietnam, Thailand, and Indonesia are becoming important production and consumption hubs, supported by rising urban populations and increasing export-oriented manufacturing. Japan and South Korea remain technology-driven markets with strong demand for specialty and high-precision films.

Latin America

The multi layer blown films market in Latin America is growing steadily, led by Brazil and Mexico. Demand is primarily driven by food packaging, agriculture films, and industrial applications. Brazil benefits from a strong domestic food processing industry, while Mexico’s proximity to North American supply chains supports export-driven demand. Although the region remains price-sensitive, adoption of multilayer films is increasing as manufacturers seek improved shelf life and reduced packaging waste.

Middle East & Africa

The Middle East & Africa region is witnessing moderate but steady growth in the multi layer blown films market. The Middle East, led by Saudi Arabia, the UAE, and Egypt, is investing heavily in food security, packaging localization, and industrial diversification, boosting demand for advanced blown films. Africa’s growth is supported by expanding packaged food consumption, agricultural films, and intra-regional trade. South Africa remains the most mature market in the region, with growing adoption of multilayer packaging for food exports.

Competitive Landscape

The multi layer blown films market is moderately fragmented, with global and regional manufacturers competing on technology, pricing, and customer relationships. The top five players collectively account for approximately 34–36% of the global market, indicating a balanced competitive environment. Large multinational players dominate high-value and technologically advanced segments, while regional manufacturers maintain strong positions in cost-competitive and localized markets.

Key Players in the Multi Layer Blown Films Market

- Amcor

- Berry Global

- Mondi Group

- Sealed Air

- Coveris

- UFlex

- Constantia Flexibles

- Winpak

- Toray Plastics

- Oben Group

- Sigma Plastics Group

- Inteplast Group

- Clondalkin Group

- Polibak

- Jindal Poly Films