Metal Packaging Market Size and Growth

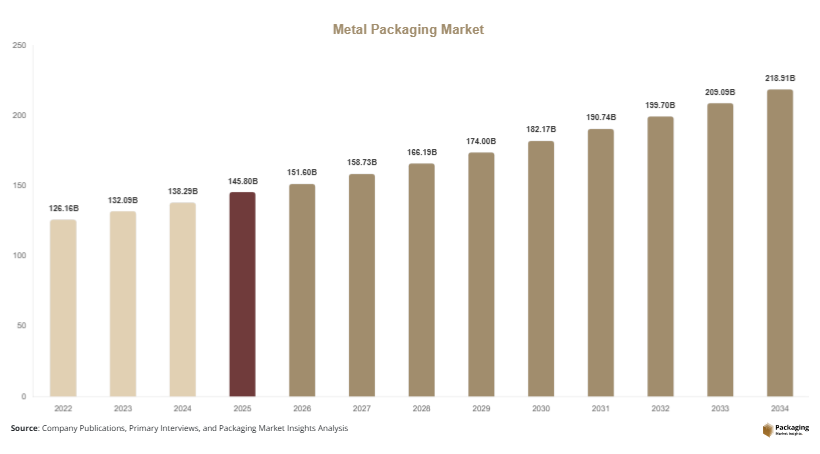

The global metal packaging market size was valued at approximately USD 145.8 billion in 2025 and is estimated to reach USD 151.6 billion in 2026. With consistent demand from beverage and processed food industries, the market is projected to reach USD 219.4 billion by 2034, expanding at a compound annual growth rate (CAGR) of 4.7% between 2025 and 2034.

The metal packaging market is experiencing steady expansion as industries seek durable, recyclable, and cost-efficient packaging solutions. Metal packaging, which includes aluminum and steel containers such as cans, barrels, caps, and closures, is widely used across food and beverages, pharmaceuticals, personal care, and industrial products. Its ability to protect products from contamination, light, and oxygen makes it a preferred option for long shelf-life packaging.

Key Highlights

- Market size estimated at USD 145.8 billion in 2025

- Expected to reach USD 219.4 billion by 2034

- CAGR projected at 4.7% from 2025–2034

- Beverage industry remains the largest consumer of metal packaging

- Sustainability initiatives are accelerating adoption of recyclable metal containers

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable and Recyclable Packaging

Sustainability has become a central trend shaping the metal packaging market. Governments and environmental organizations across the world are encouraging the reduction of single-use plastics and promoting recyclable materials. Metal packaging, particularly aluminum and steel containers, offers a significant advantage due to its ability to be recycled repeatedly without losing quality. As recycling infrastructure improves in many countries, manufacturers are increasingly adopting metal packaging to meet sustainability goals.

Consumer awareness about environmental impact is also influencing packaging preferences. Many beverage and food companies are shifting toward aluminum cans and steel containers to reduce their carbon footprint. In addition, advancements in lightweight metal packaging are helping reduce raw material usage and transportation emissions. These developments are expected to strengthen the long-term position of metal packaging within sustainable packaging strategies.

Growth of Ready-to-Drink Beverage Packaging

Another key trend influencing the metal packaging market is the rapid expansion of ready-to-drink beverage categories. Energy drinks, canned cocktails, sparkling water, and functional beverages are gaining popularity among younger consumers and urban populations. Metal cans provide a convenient format that supports portability, extended shelf life, and brand visibility.

Beverage manufacturers are also using innovative can designs and advanced printing technologies to improve branding and consumer engagement. Slim cans, resealable lids, and decorative finishes are helping brands differentiate products on retail shelves. As beverage companies launch new canned product lines, the demand for metal packaging continues to increase across both developed and emerging markets.

Market Drivers

Expansion of the Global Food and Beverage Industry

The expansion of the global food and beverage sector is one of the most important drivers of the metal packaging market. Processed foods, canned vegetables, ready meals, soups, and seafood rely heavily on metal packaging to preserve flavor and extend product shelf life. Metal containers offer superior barrier protection against moisture, light, and oxygen, making them suitable for long-term storage.

Population growth and increasing urbanization are contributing to the rising consumption of packaged foods. Consumers are seeking convenient meal options that require minimal preparation time. As a result, food manufacturers are increasing production volumes, which directly drives the demand for metal cans and containers. The growing popularity of canned beverages, including beer, soft drinks, and flavored waters, is also supporting sustained market growth.

Increasing Demand for Safe and Durable Packaging

Product safety and durability are key priorities for manufacturers and consumers. Metal packaging provides strong mechanical strength and resistance to external damage, which reduces the risk of contamination during transportation and storage. This feature makes it suitable for both food and pharmaceutical applications.

In addition, metal packaging supports advanced sealing technologies that maintain product freshness. Pharmaceutical companies are adopting metal packaging formats such as aerosol cans and specialized containers for medical sprays and topical treatments. As industries prioritize product protection and quality preservation, the demand for metal packaging continues to expand across multiple end-use sectors.

Market Restraint

Volatility in Raw Material Prices

Fluctuating raw material prices represent a significant restraint for the metal packaging market. Aluminum and steel are the primary materials used in metal packaging production, and their prices are influenced by global mining output, energy costs, geopolitical factors, and supply chain disruptions. When raw material prices rise, packaging manufacturers experience higher production costs, which can affect profit margins and pricing strategies.

These fluctuations also create uncertainty for long-term supply contracts between packaging manufacturers and consumer goods companies. For example, beverage producers that rely heavily on aluminum cans may face increased packaging expenses during periods of high aluminum prices. Such increases may lead companies to explore alternative packaging options, including plastic or composite materials.

In addition, energy-intensive metal production processes contribute to higher manufacturing costs compared with certain alternative packaging materials. Small and mid-sized packaging manufacturers may find it difficult to absorb sudden increases in raw material costs, which could limit production capacity or reduce investment in innovation.

Despite these challenges, recycling initiatives and improvements in metal recovery systems are helping reduce dependence on newly mined materials. However, raw material price volatility remains a structural constraint that manufacturers must manage through long-term procurement strategies and operational efficiency improvements.

Market Opportunities

Growth of E-commerce Packaging

The rapid expansion of e-commerce presents a growing opportunity for the metal packaging market. Online retail platforms are increasing the demand for packaging solutions that can withstand long shipping distances and handling processes. Metal containers offer durability and protection that reduce product damage during transportation.

Many premium food, beverage, and cosmetic brands are using metal packaging to maintain product quality in direct-to-consumer shipments. Decorative tins, aluminum containers, and specialty cans are becoming popular for gift packaging and premium product lines sold through online channels. As e-commerce continues to grow globally, the demand for durable and protective packaging formats is expected to increase steadily.

Technological Innovation in Lightweight Packaging

Technological advancements in lightweight metal packaging are creating new growth opportunities for manufacturers. Innovations in alloy composition, material engineering, and manufacturing techniques are enabling companies to produce thinner and lighter metal containers without compromising structural strength.

Lightweight packaging reduces transportation costs and lowers environmental impact by decreasing material usage. Beverage companies, in particular, are adopting lightweight aluminum cans to improve supply chain efficiency. In addition, improved coating technologies are helping prevent corrosion and enhance product compatibility with different food and beverage formulations. These technological improvements are expected to encourage broader adoption of metal packaging across various industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 145.8 Billion |

| Market Size in 2026 | USD 151.6 Billion |

| Market Size in 2034 | USD 219.4 Billion |

| CAGR | 4.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Aluminum dominated the metal packaging market in 2024 with an estimated share of approximately 63%. Aluminum packaging is widely used for beverage cans, aerosol containers, and food packaging due to its lightweight structure and corrosion resistance. It also provides an effective barrier against light and oxygen, which helps maintain product freshness and flavor. Beverage manufacturers prefer aluminum cans because they are easy to transport and chill quickly. In addition, aluminum packaging supports high-quality printing, allowing brands to display attractive product designs that improve shelf visibility in retail environments.

Steel represented the second major material category in the market, particularly for food cans and industrial containers. Steel packaging offers high durability and structural strength, which makes it suitable for heavy or pressure-sensitive products. It is commonly used for canned vegetables, seafood, soups, and paint containers. Although aluminum dominates beverage packaging, steel remains essential for many food preservation applications due to its strength and cost efficiency.

Steel packaging is expected to be the fastest-growing material segment with a CAGR of around 5.1% during the forecast period. One key growth factor is the increasing demand for canned food products in emerging economies. As urban populations expand and consumers seek convenient meal solutions, canned food consumption is rising steadily. Steel cans provide long shelf life and resistance to contamination, making them ideal for large-scale food distribution systems.

Another factor supporting steel packaging growth is the expansion of industrial packaging applications. Steel drums and containers are widely used for chemicals, lubricants, and industrial liquids. Manufacturers are also developing improved protective coatings that enhance corrosion resistance and extend container life. These technological improvements are expected to drive additional demand for steel-based metal packaging solutions.

By Product Type

Cans accounted for the largest share of the metal packaging market in 2024, representing approximately 58% of total revenue. Metal cans are widely used across beverage and food industries due to their durability, airtight sealing capability, and long shelf life. Beverage companies rely heavily on aluminum cans to package carbonated drinks, beer, energy drinks, and flavored water. The convenience of single-serve cans and their compatibility with automated filling systems make them highly efficient for large-scale production.

Food manufacturers also depend on metal cans for packaging vegetables, soups, seafood, and ready-to-eat meals. The ability of metal cans to withstand high-temperature sterilization processes ensures product safety and quality during long storage periods. As packaged food consumption continues to increase globally, cans are expected to maintain their leading market position.

Caps and closures are projected to be the fastest-growing product segment with a CAGR of approximately 5.3% through 2034. The rising demand for bottled beverages, pharmaceuticals, and personal care products is increasing the need for durable metal caps and closures. These components provide secure sealing that prevents leakage and contamination during storage and transportation.

Another factor driving growth in this segment is the development of advanced closure technologies. Manufacturers are introducing tamper-evident designs, improved sealing systems, and decorative finishes to enhance product safety and branding. As packaging companies continue to innovate in closure design, the adoption of metal caps and closures is expected to increase across multiple consumer product categories.

By End-Use Industry

The food and beverage industry dominated the metal packaging market in 2024 with a share of approximately 69%. Metal packaging is widely used in this sector due to its ability to preserve taste, texture, and nutritional value. Canned beverages such as soft drinks, beer, and sparkling water account for a large portion of packaging demand. In addition, canned foods such as vegetables, soups, meat, and seafood rely on metal containers for long-term preservation.

Food manufacturers prefer metal packaging because it provides strong protection against contamination and external damage. It also supports sterilization processes that extend product shelf life without requiring refrigeration. As global food consumption increases and distribution networks expand, the demand for metal packaging in the food and beverage sector remains strong.

The pharmaceutical industry is expected to be the fastest-growing end-use segment with a CAGR of approximately 5.4% during the forecast period. Pharmaceutical companies are increasingly adopting metal packaging for aerosol sprays, topical treatments, and specialized medical containers. Metal packaging ensures product stability and protects sensitive formulations from environmental exposure.

Another growth factor is the expansion of healthcare infrastructure in emerging economies. As pharmaceutical manufacturing capacity increases, the demand for safe and durable packaging materials also rises. Metal containers offer reliable sealing and contamination protection, which makes them suitable for medical products requiring strict quality standards.

Metal Packaging Market Segmentations

Material Type

- Aluminum

- Steel

Product Type

- Cans

- Barrels & Drums

- Caps & Closures

- Aerosol Containers

- Others

End-Use Industry

- Food & Beverage

- Pharmaceuticals

- Personal Care

- Industrial

- Others

Regional Analysis

North America

North America accounted for approximately 26% of the global metal packaging market share in 2025. The region is expected to register a CAGR of around 4.2% through 2034. Strong demand from the beverage sector, particularly canned beer, carbonated drinks, and energy beverages, continues to support market expansion. The presence of well-established packaging manufacturers and advanced recycling infrastructure also contributes to the region’s steady market growth.

The United States remains the dominant country within the North American market. One unique growth factor driving demand is the rapid expansion of canned alcoholic beverages, including hard seltzers and canned cocktails. Beverage companies prefer aluminum cans due to their portability and ability to preserve flavor. As new beverage brands enter the market, packaging suppliers are expanding production capacity to meet growing demand.

Europe

Europe held nearly 23% of the global metal packaging market share in 2025 and is projected to grow at a CAGR of approximately 4.1% during the forecast period. Strict environmental regulations and sustainability initiatives are encouraging companies to adopt recyclable packaging materials. The region has one of the highest recycling rates for aluminum beverage cans, which supports long-term market stability.

Germany is the leading market within Europe due to its strong manufacturing base and well-developed recycling systems. A unique growth factor in the country is the implementation of deposit return systems that encourage consumers to return used metal containers for recycling. This infrastructure strengthens the circular economy model and increases the adoption of metal packaging among food and beverage companies.

Asia Pacific

Asia Pacific represented the largest share of the metal packaging market at around 34% in 2025 and is forecast to expand at a CAGR of nearly 5.8% through 2034. Rapid urbanization, population growth, and rising disposable income are increasing the demand for packaged foods and beverages across the region. Countries such as China, India, and Japan are experiencing strong growth in canned food consumption.

China dominates the Asia Pacific market due to its large manufacturing sector and growing beverage industry. A unique growth factor driving demand is the expansion of domestic beverage brands targeting younger consumers. These brands frequently launch canned energy drinks and flavored beverages, which significantly increases demand for aluminum cans and related packaging solutions.

Middle East & Africa

The Middle East & Africa region accounted for approximately 8% of the global metal packaging market share in 2025. The market is expected to grow at a CAGR of about 4.9% during the forecast period. Rising urban populations and increasing demand for packaged food products are contributing to the expansion of metal packaging applications in the region.

Saudi Arabia is a key market within the region due to its expanding food processing industry. A unique growth factor supporting demand is the increasing investment in local food manufacturing facilities. As domestic production of canned food and beverages rises, the need for metal packaging solutions is also increasing across the country.

Latin America

Latin America accounted for nearly 9% of the global metal packaging market share in 2025 and is projected to grow at a CAGR of around 4.6% through 2034. The growth of the beverage sector, particularly canned soft drinks and beer, is a major contributor to the region’s market development. In addition, increasing urbanization is encouraging the adoption of packaged food products.

Brazil leads the Latin American market due to its strong beverage manufacturing industry. One unique growth factor driving demand is the popularity of canned beer in retail and hospitality sectors. Beverage companies are investing in modern canning facilities and packaging technologies, which is strengthening the regional metal packaging supply chain.

Competitive Landscape

The metal packaging market is moderately consolidated, with several global companies operating extensive manufacturing networks and investing in technological innovation. Leading packaging manufacturers are focusing on lightweight materials, sustainable production methods, and advanced printing technologies to strengthen their competitive positions.

One of the leading companies in the market is Ball Corporation, which maintains a strong presence in aluminum beverage can manufacturing. The company continues to expand production capacity to meet growing demand from beverage brands worldwide. Its investments in sustainable packaging solutions and recycling initiatives support long-term growth.

Other major players include Crown Holdings, Ardagh Group, Silgan Holdings, and Can-Pack. These companies compete by expanding manufacturing facilities, forming partnerships with beverage and food companies, and investing in advanced packaging technologies.

Recent strategic initiatives include capacity expansions in emerging markets, development of lightweight metal containers, and adoption of digital printing techniques for improved branding. Competitive strategies increasingly focus on sustainability and cost efficiency as companies respond to evolving environmental regulations and changing consumer preferences.

Key Players List

- Ball Corporation

- Crown Holdings Inc.

- Ardagh Group

- Silgan Holdings Inc.

- CAN-PACK S.A.

- Amcor Plc

- Sonoco Products Company

- Mauser Packaging Solutions

- Tata Steel Packaging

- Kian Joo Can Factory Berhad

- Toyo Seikan Group Holdings

- CPMC Holdings Limited

- Envases Group

- Colep Packaging

- Trivium Packaging