Metal Cosmetic Packaging Market Size and Growth

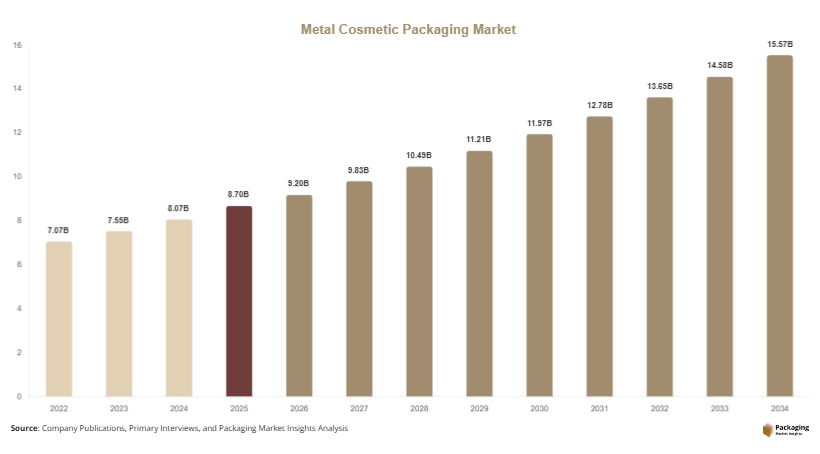

The global metal cosmetic packaging market size was valued at approximately USD 8.7 billion in 2025 and is projected to reach USD 9.2 billion in 2026. The market is expected to reach around USD 15.6 billion by 2034, registering a CAGR of 6.8% during the forecast period (2025–2034). Growth is being supported by increasing demand for recyclable packaging materials, expansion of premium beauty brands, and rising consumption of personal care products across emerging economies.

The metal cosmetic packaging market is experiencing steady growth as cosmetic and personal care brands increasingly adopt premium, durable, and sustainable packaging solutions. Metal packaging, including aluminum and tin-based containers, offers superior barrier protection, recyclability, aesthetic appeal, and product durability, making it a preferred choice across skincare, fragrance, haircare, and color cosmetics applications. As consumers place greater emphasis on sustainability and premium product presentation, manufacturers are expanding investments in innovative metal packaging formats.

Key Market Highlights

- Asia Pacific dominated the market with a 38.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.4%.

- Aluminum packaging led the type segment with a 48.9% share.

- Aluminum material dominated the market with a 61.5% share.

- Skincare applications led the end-use segment with 36.8% share.

- The US remained the dominant country with a market size of USD 1.34 billion in 2025 and USD 1.42 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Refillable Metal Cosmetic Packaging

Refillable packaging solutions are becoming a major trend within the metal cosmetic packaging market as cosmetic brands seek to reduce packaging waste and improve sustainability performance. Consumers are increasingly purchasing refill packs instead of replacing entire product containers, particularly in skincare, fragrances, and luxury cosmetics. Metal packaging offers durability and repeated usability, making it ideal for refill systems. For example, several premium skincare brands have introduced refillable aluminum jars and metal compact cases that allow consumers to replace product inserts while retaining the original package. This trend is expected to expand significantly as regulatory authorities promote waste reduction initiatives and brands strengthen circular packaging strategies. Future developments may include smart refill systems and customizable packaging designs.

Growth of Premium Decorative Metal Packaging

Premium aesthetics are becoming increasingly important in the cosmetics industry, driving demand for decorative metal packaging solutions. Manufacturers are investing in embossing, laser engraving, digital printing, and anodized finishing technologies to create visually distinctive packaging. For instance, luxury fragrance brands are using customized aluminum containers and decorative metal caps to enhance shelf appeal and reinforce premium brand positioning. This trend is expected to continue as beauty companies compete through packaging innovation. Future growth will likely be supported by advances in digital decoration technologies that enable short production runs, personalization, and enhanced branding opportunities while maintaining sustainable packaging credentials.

Market Drivers

Rising Demand for Sustainable Packaging Solutions

Growing environmental awareness among consumers is significantly driving demand for metal cosmetic packaging. Brands are under increasing pressure to reduce plastic consumption and adopt recyclable packaging materials. Metal packaging, particularly aluminum, offers high recyclability rates and can be repeatedly reused without substantial loss of quality. This creates a direct cause-and-effect relationship where sustainability concerns drive packaging material shifts. For example, major global cosmetic brands have announced commitments to increase recyclable packaging content and reduce virgin plastic use. As these sustainability goals become more widespread, demand for metal cosmetic packaging solutions is expected to increase steadily across both premium and mass-market product categories.

Expansion of the Global Premium Beauty Industry

The rapid growth of premium beauty and personal care products is another important driver of market expansion. Consumers increasingly associate metal packaging with quality, durability, and luxury. As premium skincare, fragrance, and cosmetics categories expand, manufacturers are adopting metal containers to strengthen brand perception and improve product presentation. For example, luxury fragrance brands frequently utilize decorative aluminum bottles and metal caps to enhance product differentiation. The continued growth of prestige beauty retail channels and online premium beauty sales is expected to support sustained demand for metal packaging solutions during the forecast period.

Market Restraint

Higher Production Costs Compared with Plastic Packaging

One of the key restraints affecting the metal cosmetic packaging market is the relatively higher production cost associated with metal packaging materials and manufacturing processes. Aluminum and tin packaging generally require more complex fabrication, decoration, and transportation processes than conventional plastic packaging. This cost differential can create challenges for budget-focused cosmetic brands and emerging companies with limited packaging budgets.

The impact is particularly noticeable in mass-market product categories where price competitiveness remains important. For example, smaller cosmetic manufacturers may continue using plastic containers despite sustainability advantages offered by metal packaging. Additionally, fluctuations in aluminum and metal commodity prices can increase manufacturing expenses and affect profit margins. While technological improvements and increased recycling rates are helping reduce costs over time, pricing remains a significant consideration for widespread adoption. Consequently, some market participants may face challenges balancing sustainability objectives with affordability requirements.

Market Opportunities

Expansion of Recycled Metal Packaging Solutions

The increasing availability of recycled aluminum and other recycled metal materials presents significant growth opportunities for packaging manufacturers. Beauty brands are actively seeking packaging solutions with lower carbon footprints while maintaining product quality and aesthetics. Recycled metal packaging allows companies to meet sustainability targets without compromising functionality. For example, several skincare and fragrance brands have launched packaging made from high percentages of post-consumer recycled aluminum. Future opportunities are expected to emerge as recycling infrastructure improves globally and consumers increasingly prioritize environmentally responsible beauty products. This trend is likely to support innovation in lightweight recycled packaging designs and sustainable sourcing strategies.

Growth of Cosmetic Markets in Emerging Economies

Emerging economies across Asia Pacific, Latin America, and the Middle East offer substantial growth potential for metal cosmetic packaging suppliers. Rising disposable incomes, urbanization, and increasing beauty product consumption are creating strong demand for premium packaging formats. Countries such as India, Indonesia, Brazil, and the United Arab Emirates are witnessing rapid expansion in skincare and cosmetics spending. Packaging manufacturers can capitalize on this trend by offering localized production capabilities and customized metal packaging solutions. Future opportunities are expected to arise from expanding retail networks, increasing online beauty sales, and growing consumer awareness of sustainable packaging alternatives.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.7 Billion |

| Market Size in 2026 | USD 9.2 Billion |

| Market Size in 2034 | USD 15.6 Billion |

| CAGR | 6.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Aluminum packaging dominated the market in 2024, accounting for approximately 48.9% of total market share. This segment leads due to its lightweight nature, corrosion resistance, high recyclability, and compatibility with a wide range of cosmetic products. Aluminum containers are extensively used in deodorants, fragrances, skincare products, and haircare packaging because they provide excellent barrier protection against moisture, light, and contamination. Major beauty brands continue to prefer aluminum packaging for both sustainability and premium aesthetics. For example, numerous skincare companies utilize aluminum jars and bottles to reinforce eco-friendly brand positioning. Additionally, advancements in decorative finishing technologies have improved aluminum packaging appeal, further strengthening segment dominance. Increasing consumer preference for recyclable packaging is expected to maintain strong demand for aluminum-based solutions.

Refillable metal packaging is projected to be the fastest-growing subsegment, registering a CAGR of 8.1% through 2034. Growth is being driven by increasing sustainability initiatives and rising consumer interest in waste reduction. Cosmetic brands are launching refillable packaging systems to encourage repeat purchases while minimizing packaging disposal. Future opportunities are expected to emerge through innovative refill mechanisms, premium reusable designs, and subscription-based beauty product models. As refillable packaging becomes more accessible across product categories, demand for durable metal packaging formats is expected to accelerate significantly.

By Material

Aluminum material accounted for approximately 61.5% of market share in 2024, making it the dominant material segment. Aluminum offers an optimal combination of lightweight performance, recyclability, durability, and visual appeal. It is widely used in cosmetic packaging because it protects products from external contamination while supporting premium branding initiatives. Numerous fragrance, deodorant, and skincare brands rely on aluminum packaging to meet both sustainability objectives and aesthetic requirements. Investments in aluminum recycling infrastructure are improving supply chain sustainability and supporting continued material adoption. Furthermore, manufacturers continue introducing lightweight aluminum packaging designs that reduce material consumption while maintaining structural integrity.

Recycled metal materials are expected to be the fastest-growing segment, expanding at a CAGR of 8.4% during the forecast period. The growth is linked to increasing corporate sustainability commitments and growing consumer awareness regarding environmental responsibility. Packaging manufacturers are sourcing higher levels of recycled aluminum to reduce carbon emissions and improve resource efficiency. Future demand is expected to strengthen as governments introduce stricter sustainability regulations and cosmetic companies prioritize low-carbon packaging solutions.

By End-Use

Skincare products dominated the end-use segment in 2024, accounting for approximately 36.8% of total market share. The segment benefits from strong demand for premium packaging solutions that preserve product quality and enhance brand image. Metal jars, tins, bottles, and refillable containers are increasingly used for creams, serums, and moisturizers due to their durability and premium appearance. The rapid growth of anti-aging, wellness, and premium skincare categories has further supported segment expansion. Cosmetic manufacturers continue investing in aesthetically appealing packaging to attract consumers and differentiate products within competitive retail environments.

Premium cosmetics are expected to be the fastest-growing end-use segment, registering a CAGR of 8.0% through 2034. Growth is being driven by rising consumer spending on luxury beauty products and increasing demand for distinctive packaging designs. Brands are utilizing metal packaging to create premium experiences and strengthen customer engagement. Future growth is expected to be supported by limited-edition product launches, personalized packaging concepts, and increasing adoption of sustainable luxury packaging strategies.

Metal Cosmetic Packaging Market Segmentations

By Type

- Aluminum Packaging

- Tin Packaging

- Aerosol Metal Packaging

- Refillable Metal Packaging

By Material

- Aluminum

- Tinplate

- Stainless Steel

- Recycled Metal Materials

By End-User

- Skincare

- Haircare

- Fragrances

- Color Cosmetics

- Premium Cosmetics

Regional Analysis

North America

North America accounted for approximately 27.9% of the global metal cosmetic packaging market share in 2025 and is projected to grow at a CAGR of 6.1% through 2034. The region benefits from strong demand for premium beauty products, advanced packaging technologies, and increasing sustainability initiatives among major cosmetic brands. Consumers increasingly prefer recyclable and refillable packaging formats, encouraging manufacturers to invest in innovative metal packaging solutions. Growth is further supported by expanding e-commerce beauty sales and rising adoption of luxury skincare products. The presence of established packaging suppliers and beauty companies continues to strengthen regional market development.

The United States dominates the North American market. A unique growth driver is the increasing popularity of refillable beauty products within prestige cosmetics channels. Several luxury beauty brands operating in the country have launched reusable metal containers designed to reduce packaging waste and improve customer retention. Retailers are dedicating more shelf space to sustainable beauty products, creating additional demand for metal cosmetic packaging solutions. This trend is expected to support long-term market growth throughout the forecast period.

Europe

Europe represented approximately 25.8% of the global market share in 2025 and is forecast to grow at a CAGR of 6.3% through 2034. The region benefits from strong environmental regulations and widespread adoption of sustainable packaging practices. Cosmetic manufacturers across Europe are increasingly transitioning from plastic packaging to recyclable metal alternatives to comply with regulatory requirements and consumer expectations. The region's mature beauty industry and strong luxury cosmetics sector further support demand for premium metal packaging solutions. Investments in circular economy initiatives are also contributing to market expansion.

France is the dominant country in the European market. A unique growth driver is the strong presence of luxury fragrance and skincare brands that utilize decorative metal packaging to reinforce premium positioning. Companies are increasingly investing in customized aluminum packaging and refillable fragrance containers. The trend toward luxury sustainability is accelerating demand for recyclable metal packaging across French beauty brands, creating opportunities for packaging manufacturers and suppliers.

Asia Pacific

Asia Pacific dominated the market with a 38.6% share in 2025 and is projected to expand at a CAGR of 7.5% during the forecast period. Rising beauty product consumption, increasing disposable incomes, and rapid urbanization are driving strong demand for cosmetic packaging solutions across the region. Growth in premium skincare and personal care products is particularly significant in countries such as China, Japan, South Korea, and India. Additionally, increasing investments in local packaging manufacturing capabilities are supporting market expansion. The growing influence of beauty-focused social media marketing is also contributing to product premiumization and packaging innovation.

China remains the dominant country in Asia Pacific. A unique growth driver is the rapid expansion of domestic beauty brands targeting premium consumer segments. Chinese cosmetic companies are increasingly adopting high-quality metal packaging to compete with international brands and strengthen product differentiation. Growth in online beauty retail channels and live-stream commerce platforms is creating additional demand for visually appealing and durable packaging formats.

Middle East & Africa

The Middle East & Africa accounted for approximately 4.7% of market share in 2025 and is expected to register a CAGR of 6.7% through 2034. Growth is being supported by increasing beauty product consumption, expansion of luxury retail channels, and rising disposable incomes among urban consumers. International cosmetic brands continue expanding their regional presence, creating demand for premium packaging solutions. Additionally, growing awareness of sustainable packaging concepts is gradually influencing purchasing decisions. Investments in modern retail infrastructure and duty-free shopping channels are further supporting market development.

The United Arab Emirates leads the regional market. A unique growth driver is the strong demand for premium fragrances and luxury personal care products. High consumer spending on prestige beauty products has encouraged brands to utilize decorative metal packaging to enhance product presentation. The expansion of luxury shopping destinations and tourism-related retail activities continues to create favorable conditions for metal cosmetic packaging adoption.

Latin America

Latin America held approximately 3.0% of the global market share in 2025 and is projected to grow at the fastest CAGR of 7.4% through 2034. The region is benefiting from increasing cosmetic consumption, expanding middle-class populations, and growing demand for premium personal care products. Beauty brands are increasingly investing in sustainable packaging solutions to attract environmentally conscious consumers. The development of local manufacturing capabilities is also supporting market growth. Rising demand for skincare and haircare products continues to create opportunities for packaging suppliers.

Brazil dominates the Latin American market. A unique growth driver is the country's strong personal care and beauty industry, which is among the largest globally. Domestic cosmetic companies are increasingly adopting metal packaging formats for premium skincare, deodorants, and fragrance products. The growing popularity of sustainable beauty products is expected to further support demand for recyclable metal packaging solutions across the country.

Competitive Landscape

The metal cosmetic packaging market is moderately consolidated, with global packaging manufacturers competing through sustainability initiatives, product innovation, and strategic collaborations. Ball Corporation is recognized as a leading company due to its extensive aluminum packaging portfolio, strong manufacturing capabilities, and focus on recyclable packaging solutions.

Other major participants include Trivium Packaging, Crown Holdings, AptarGroup, and Berlin Packaging. These companies continue investing in lightweight metal packaging technologies, decorative finishing capabilities, and sustainable material sourcing programs. Strategic partnerships with cosmetic brands are helping manufacturers develop customized packaging solutions tailored to evolving consumer preferences.

Recent competitive strategies include acquisitions, production expansions, and investments in recycled aluminum packaging. Companies are increasingly focusing on refillable systems, premium packaging aesthetics, and circular economy initiatives to strengthen market position. The growing emphasis on sustainability and premiumization is expected to shape future competition within the industry.

Key Players List

- Ball Corporation

- Trivium Packaging

- Crown Holdings Inc.

- AptarGroup Inc.

- Berlin Packaging

- Ardagh Group

- Silgan Holdings Inc.

- Envases Group

- Tubex Holding GmbH

- Montebello Packaging

- Alltub Group

- Albéa Group

- Sonoco Products Company

- CCL Container

- Jamestrong Packaging

- Massilly Holding SAS