Medium Density Fiberboard Market Size and Growth

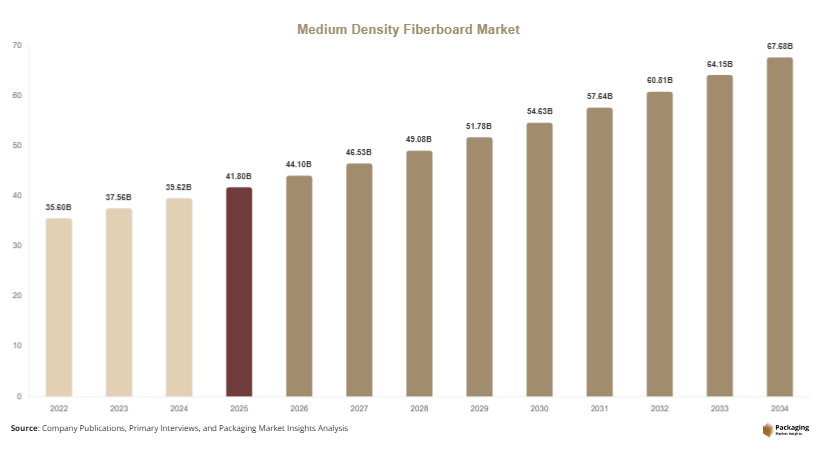

The global medium density fiberboard market was valued at USD 41.8 billion in 2025 and is projected to reach USD 44.1 billion in 2026, further expanding to USD 67.5 billion by 2034, growing at a CAGR of 5.5% during 2025–2034. The market is witnessing stable growth due to increasing construction activities, rising furniture production, and growing demand for engineered wood products across residential and commercial sectors. Medium density fiberboard, commonly known as MDF, is widely used in cabinetry, flooring systems, shelving, decorative interiors, office furniture, and modular housing applications because of its smooth surface finish, dimensional stability, and cost efficiency.

Rapid urbanization across emerging economies is significantly contributing to market expansion. Countries in Asia Pacific, Latin America, and the Middle East are witnessing increased residential construction and infrastructure modernization, creating strong demand for affordable and aesthetically appealing wood-based products. MDF continues to gain popularity over solid wood because it offers consistent quality, easier machinability, and reduced production waste. Manufacturers are also investing in moisture-resistant, fire-retardant, and low-emission MDF products to meet evolving consumer preferences and environmental standards.

Key Market Highlights

- Asia Pacific dominated the market with a 43.6% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.4%.

- Standard MDF led the type segment with a 46.9% share.

- Wood fiber-based boards dominated the material segment with a 68.3% share.

- Furniture applications led the segment with 49.7% share.

- The US remained the dominant country in North America, with a market size of USD 3.4 billion in 2025 and USD 3.6 billion in 2026

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Sustainable and Low-Emission MDF Products

The growing focus on environmentally sustainable construction materials is becoming a major trend in the medium density fiberboard market. Governments and construction companies are increasingly emphasizing low-emission engineered wood products that comply with indoor air quality regulations and green building certification standards. MDF manufacturers are responding by introducing panels made with formaldehyde-free adhesives, recycled wood fibers, and low volatile organic compound resin systems. Demand for sustainable MDF products is particularly strong in Europe and North America, where environmental compliance standards continue to tighten across residential and commercial construction sectors.

Furniture manufacturers are also integrating eco-friendly MDF panels into modular furniture production to meet consumer demand for sustainable home products. For example, several global furniture brands now market low-emission MDF kitchen cabinets and wardrobes certified under green building standards. Future market growth is expected to accelerate as recycled wood utilization and carbon-neutral manufacturing practices become more common across the engineered wood industry.

Expansion of Modular Furniture and Ready-to-Assemble Products

The rapid expansion of modular furniture manufacturing is significantly influencing the medium density fiberboard market. Urban consumers increasingly prefer ready-to-assemble furniture solutions due to affordability, space efficiency, and convenience in transportation. MDF offers smooth finishing, dimensional consistency, and compatibility with decorative laminates, making it highly suitable for modular furniture applications. Retailers and e-commerce furniture brands extensively use MDF panels for producing wardrobes, desks, cabinets, shelving systems, and entertainment units.

Countries such as India, China, Vietnam, and Indonesia are witnessing rising investment in furniture manufacturing clusters, supporting strong MDF consumption growth. The increasing penetration of online furniture sales is also encouraging manufacturers to produce lightweight and customizable MDF-based products that simplify shipping and assembly processes. Over the forecast period, digital customization technologies and smart furniture production systems are expected to strengthen the role of MDF in modern interior design and urban residential construction.

Market Drivers

Growth in Residential and Commercial Construction Activities

The expansion of residential housing projects and commercial infrastructure development is a major driver supporting the medium density fiberboard market. Rapid urbanization, rising disposable incomes, and increasing demand for affordable housing are accelerating consumption of engineered wood products globally. MDF is extensively used in wall paneling, furniture, ceilings, flooring substrates, and decorative applications because it provides cost-effective performance and design flexibility. Developing economies in Asia Pacific and the Middle East are particularly witnessing strong growth in residential apartment construction and hospitality infrastructure projects.

Commercial office renovation and retail space expansion are also contributing to higher MDF demand. Hotels, restaurants, shopping centers, and educational institutions increasingly use MDF panels for interior decoration and modular furniture installations. As governments continue investing in infrastructure modernization and urban housing programs, MDF consumption is expected to rise steadily across both residential and commercial construction sectors.

Increasing Demand for Cost-Effective Furniture Manufacturing

The growing global demand for affordable furniture products is another major factor driving the medium density fiberboard market. MDF is widely preferred in furniture manufacturing because it offers lower production costs compared to solid wood while maintaining design versatility and surface smoothness. Furniture producers increasingly rely on MDF for cabinets, wardrobes, office desks, and modular storage systems due to its machinability and compatibility with veneers and laminates.

The rise of online furniture retailing has further accelerated demand for lightweight and easy-to-assemble furniture products manufactured using MDF panels. Large-scale furniture exporters in China, Poland, Vietnam, and Malaysia are expanding production capacities to meet increasing international demand. Manufacturers are also integrating advanced CNC machining and digital printing technologies into MDF furniture production, enabling greater customization and operational efficiency. These developments are expected to sustain long-term growth across the global market.

Market Restraint

Volatility in Raw Material Availability and Environmental Regulations

Fluctuations in wood fiber availability and increasingly strict environmental regulations remain significant restraints for the medium density fiberboard market. MDF manufacturing depends heavily on timber resources, recycled wood materials, and resin chemicals, all of which are vulnerable to supply chain disruptions and pricing volatility. Deforestation concerns and restrictions on logging activities in several countries are limiting the availability of raw materials required for MDF production.

Environmental regulations regarding formaldehyde emissions and industrial waste management are also increasing compliance costs for manufacturers. Small and medium-scale MDF producers often face difficulties in upgrading production technologies to meet emission standards and sustainability certifications. For example, several regional manufacturers in developing economies have experienced operational challenges due to stricter emission monitoring requirements and higher resin costs. In addition, increasing competition from alternative engineered wood products such as plywood and particleboard may limit market expansion in price-sensitive regions. These factors could affect profitability and production scalability during the forecast period.

Market Opportunities

Expansion of Green Building and Sustainable Construction Projects

The growing adoption of green building practices presents significant opportunities for the medium density fiberboard market. Governments and private developers are increasingly prioritizing environmentally responsible construction materials to reduce carbon emissions and improve energy efficiency. MDF products manufactured using recycled wood fibers and low-emission adhesives are gaining strong acceptance in sustainable residential and commercial projects.

Green-certified office complexes, hotels, and educational buildings increasingly utilize eco-friendly MDF for interior applications such as wall panels, partitions, cabinetry, and flooring systems. Manufacturers investing in FSC-certified wood sourcing and bio-based resin technologies are expected to gain competitive advantages in environmentally regulated markets. The integration of recycled content and circular economy manufacturing practices is also likely to create long-term growth opportunities across developed economies.

Rising Demand for Smart and Customized Interior Solutions

The increasing popularity of customized interior design and smart furniture systems is creating new opportunities for MDF manufacturers. Urban consumers are seeking multifunctional furniture solutions that optimize limited living spaces while maintaining modern aesthetics. MDF is highly suitable for customized furniture production because it can be easily machined, laminated, painted, and digitally printed.

Smart homes, modular apartments, and compact commercial spaces are increasingly incorporating MDF-based furniture systems integrated with lighting, storage, and automation features. Interior designers and architects are also using decorative MDF panels for premium wall finishes and acoustic solutions. The adoption of advanced CNC cutting and automated manufacturing technologies is enabling manufacturers to deliver highly customized products at competitive costs. These innovations are expected to expand the application scope of MDF across residential and commercial interiors over the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 41.8 Billion |

| Market Size in 2026 | USD 44.1 Billion |

| Market Size in 2034 | USD 67.5 Billion |

| CAGR | 5.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Standard MDF dominated the global medium density fiberboard market in 2024, accounting for approximately 46.9% of total market share. The segment maintains leadership due to widespread use across furniture manufacturing, interior decoration, shelving systems, cabinetry, and residential construction applications. Standard MDF offers smooth surface texture, uniform density, and cost-effective machinability, making it suitable for laminating, painting, veneering, and decorative finishing processes. Furniture manufacturers extensively utilize standard MDF panels for wardrobes, office desks, modular kitchen systems, and entertainment units because the material supports efficient mass production and customization. In rapidly urbanizing countries such as China, India, and Vietnam, standard MDF continues to replace traditional solid wood products due to lower costs and improved availability. Large-scale retail furniture brands are increasingly integrating standard MDF into ready-to-assemble furniture collections designed for urban residential consumers. In addition, growing adoption of automated CNC machining technologies is enabling manufacturers to improve production precision and reduce waste generation during furniture manufacturing. Rising investments in residential remodeling and commercial interior design projects are expected to sustain strong demand for standard MDF products globally.

Moisture-resistant MDF is projected to witness the fastest CAGR of 6.7% during the forecast period due to increasing demand for durable engineered wood products in kitchens, bathrooms, and humid environments. Moisture-resistant MDF panels are manufactured using specialized resin systems and wax additives that improve dimensional stability and water resistance. Demand is growing rapidly in residential construction projects, hospitality infrastructure, and modular kitchen manufacturing because consumers increasingly prioritize long-lasting interior materials with improved durability. Furniture manufacturers are adopting moisture-resistant MDF for cabinetry, bathroom vanities, laundry room storage systems, and decorative wall applications where exposure to humidity is common. The growth of compact urban housing and premium apartment developments is also supporting segment expansion, particularly in Asia Pacific and the Middle East. Manufacturers are investing in advanced resin technologies and environmentally compliant production systems to improve performance characteristics while reducing emissions. Increasing adoption of moisture-resistant MDF in commercial retail interiors, educational facilities, and healthcare buildings is expected to create long-term growth opportunities over the next decade.

By Material

Virgin wood fiber materials dominated the medium density fiberboard market in 2024 with a share of approximately 68.3%. The segment continues to lead due to consistent raw material quality, high structural integrity, and strong compatibility with engineered wood manufacturing processes. Virgin wood fibers provide smoother panel surfaces, better density control, and improved machining performance compared to lower-grade recycled alternatives. MDF manufacturers prefer virgin wood fibers for producing high-quality decorative panels, premium furniture components, and precision interior products. Countries with well-established forestry industries such as Canada, the United States, Germany, and Sweden maintain strong production capacity due to reliable access to timber resources. Furniture exporters and interior product manufacturers also favor virgin wood fiber MDF because it supports advanced finishing applications including laminates, veneers, and digital printing systems. Manufacturers are increasingly utilizing sustainably sourced timber certified under international forestry standards to meet environmental compliance requirements and strengthen export competitiveness. In addition, automated fiber refining technologies are improving production efficiency and product consistency across large-scale MDF manufacturing operations worldwide.

Recycled wood fiber materials are expected to record the fastest CAGR of 6.5% through 2034 due to rising sustainability initiatives and growing pressure to reduce industrial waste generation. MDF manufacturers are increasingly integrating recycled wood particles, post-consumer wood waste, and industrial wood residues into production processes to support circular economy goals and reduce raw material costs. Demand for recycled fiber MDF is especially increasing in Europe and North America, where green building certifications and environmental regulations encourage the use of recycled-content construction materials. Commercial office developers and institutional construction projects are adopting recycled MDF panels to improve sustainability performance and comply with environmentally responsible procurement standards. Manufacturers are also investing in advanced cleaning, refining, and sorting technologies that improve recycled fiber quality and production consistency. The increasing popularity of eco-friendly furniture products and sustainable home interiors is expected to further accelerate segment growth. As environmental awareness continues expanding globally, recycled wood fiber MDF is likely to become a major focus area for future product innovation and manufacturing investment.

By End-Use

Furniture manufacturing dominated the end-use segment in 2024, accounting for approximately 49.7% of the global medium density fiberboard market share. MDF has become one of the most widely used materials in furniture production because of its affordability, dimensional stability, and ease of customization. Manufacturers extensively utilize MDF in wardrobes, modular kitchens, office desks, bookshelves, entertainment units, and storage cabinets. The material’s smooth surface enables efficient application of laminates, veneers, paints, and decorative coatings, making it suitable for modern furniture aesthetics. Growth in urban apartment construction and rising consumer preference for affordable ready-to-assemble furniture are major factors supporting segment expansion. Large-scale furniture exporters in Asia Pacific and Eastern Europe continue increasing MDF consumption to meet growing international demand for modular furniture products. E-commerce furniture retailing is also accelerating the use of MDF panels due to lightweight design requirements and cost-effective logistics advantages. Additionally, advancements in digital manufacturing technologies are enabling customized MDF furniture production with improved operational efficiency and reduced material waste.

Commercial construction applications are anticipated to register the fastest CAGR of 6.1% during the forecast period. Increasing investments in office complexes, retail stores, educational institutions, hotels, and healthcare infrastructure are creating strong demand for MDF products across interior construction applications. Commercial buildings increasingly use MDF for wall paneling, ceiling systems, partitions, cabinetry, and decorative architectural elements because the material combines cost efficiency with aesthetic versatility. The expansion of coworking spaces, hospitality projects, and mixed-use commercial developments is further supporting market growth. In emerging economies, rapid urbanization and retail modernization are driving higher demand for modular interior systems manufactured using MDF panels. Manufacturers are also developing fire-retardant and moisture-resistant MDF products specifically designed for commercial construction environments with strict safety requirements. Increasing adoption of green building certification programs is encouraging architects and developers to integrate low-emission MDF materials into sustainable commercial projects, creating additional long-term growth opportunities across the segment.

Medium Density Fiberboard Market Segmentations

By Type

- Standard MDF

- Moisture-Resistant MDF

- Fire-Resistant MDF

- Ultra-Light MDF

By Material

- Wood Fiber-Based MDF

- Recycled Wood Fiber MDF

- Agricultural Fiber-Based MDF

- Hybrid Fiber MDF

By End-User

- Furniture Manufacturing

- Construction & Interior Decoration

- Flooring Applications

- Retail Fixtures & Displays

Regional Analysis

North America

North America accounted for approximately 21.4% of the global medium density fiberboard market share in 2025 and is projected to expand at a CAGR of 4.9% during the forecast period. The region continues to witness stable demand due to strong residential renovation activities, increasing modular furniture adoption, and rising investments in commercial interior construction. MDF products are widely utilized across cabinetry, flooring underlayment, office furniture, and decorative wall panel applications because they offer cost efficiency and design flexibility. Growing demand for sustainable engineered wood products is also encouraging manufacturers to introduce low-emission and recycled-content MDF solutions. In the United States and Canada, rising urban housing upgrades and remodeling expenditures are further supporting long-term market growth across residential construction sectors.

The United States remained the dominant country in North America due to strong furniture manufacturing and large-scale home improvement spending. One major growth driver in the country is the increasing adoption of ready-to-assemble furniture sold through e-commerce and retail furniture chains. Manufacturers are investing in digitally finished MDF panels and lightweight engineered wood solutions to meet evolving consumer preferences for customizable interiors. The growth of green commercial buildings is also encouraging higher use of FSC-certified MDF materials in office and hospitality projects. Rising renovation activity across aging residential infrastructure and increasing demand for affordable interior materials continue to strengthen the position of MDF products across the U.S. construction and furniture industries.

Europe

Europe represented nearly 24.8% of the global medium density fiberboard market in 2025 and is expected to register a CAGR of 5.1% through 2034. The market is supported by stringent sustainability regulations, growing demand for engineered wood products, and strong furniture manufacturing industries across Germany, Italy, and Poland. MDF panels are extensively used in kitchen furniture, office interiors, retail displays, and decorative architectural applications because of their smooth finish and versatility. European manufacturers are increasingly focusing on formaldehyde-free resin systems and recycled wood integration to comply with environmental standards. Rising investments in energy-efficient residential buildings and eco-friendly renovation projects are also contributing to increasing demand for certified MDF products throughout the region.

Germany dominated the European market due to its advanced furniture manufacturing ecosystem and strong engineered wood processing industry. A unique growth driver in the country is the expansion of automated furniture production technologies integrated with precision CNC machining systems. German manufacturers are increasingly producing customized MDF furniture and decorative panels for export markets across Europe and North America. The rise of compact urban housing is also increasing demand for multifunctional MDF furniture systems that optimize interior space efficiency. In addition, sustainability-focused retailers continue expanding the use of low-emission MDF products within premium residential and commercial interior applications, supporting long-term market development across the country.

Asia Pacific

Asia Pacific dominated the medium density fiberboard market with a 43.6% share in 2025 and is anticipated to expand at a CAGR of 6.3% during the forecast period. Rapid urbanization, rising residential construction activity, and large-scale furniture manufacturing are major growth factors supporting the region’s leadership position. Countries such as China, India, Vietnam, Indonesia, and Malaysia continue to experience rising consumption of engineered wood products due to increasing middle-class spending and expanding infrastructure development. MDF products are widely used in modular furniture, office interiors, retail fixtures, and low-cost housing projects across the region. Strong export-oriented furniture manufacturing industries and growing investment in automated wood panel production technologies are also accelerating market growth across Asia Pacific.

China remained the dominant country in the region with substantial production and consumption capacity for MDF products. One important growth driver is the rapid expansion of the country’s modular furniture export industry. Chinese manufacturers are heavily investing in automated panel processing technologies and sustainable production systems to improve international competitiveness. The country also benefits from strong domestic demand for affordable housing and commercial interior development. Rising investments in smart city projects and modern office infrastructure continue to increase the use of MDF panels for decorative and structural interior applications. In addition, China’s rapidly expanding e-commerce furniture sector is creating consistent long-term demand for lightweight and customizable MDF-based furniture products.

Middle East & Africa

The Middle East & Africa medium density fiberboard market accounted for approximately 5.9% of global revenue in 2025 and is projected to grow at a CAGR of 5.4% through 2034. Increasing investments in commercial construction, hospitality infrastructure, and urban residential development are supporting regional demand for MDF products. Countries across the Gulf Cooperation Council are witnessing rising adoption of engineered wood materials for interior decoration and modular furniture applications. MDF is gaining popularity in shopping malls, hotels, educational institutions, and luxury residential projects due to its affordability and design flexibility. Government-backed infrastructure diversification initiatives and tourism development programs are also encouraging growth in the regional furniture and interior construction industries.

Saudi Arabia emerged as the leading market within the region due to strong investment in urban infrastructure and tourism-related development projects. A key growth driver is the expansion of large-scale mixed-use construction projects under national economic diversification strategies. Hotels, entertainment complexes, and commercial office spaces increasingly utilize MDF products for decorative interiors, cabinetry, and acoustic wall systems. The growing popularity of modular kitchens and customized residential furniture is also accelerating MDF consumption across urban housing projects. Additionally, increasing imports of engineered wood products and partnerships with international furniture brands are contributing to steady long-term market growth in Saudi Arabia and neighboring Gulf economies.

Latin America

Latin America accounted for approximately 4.3% of the global medium density fiberboard market in 2025 and is expected to register the fastest CAGR of 6.4% during the forecast period. The region is witnessing rising demand for affordable furniture products, residential housing expansion, and modernization of retail infrastructure. MDF panels are increasingly used in low-cost modular furniture production because they offer cost advantages and compatibility with decorative laminates. Countries such as Brazil, Mexico, Chile, and Colombia are experiencing growth in organized furniture retail and home improvement industries, supporting long-term MDF demand. Increasing urbanization and rising middle-income consumer spending are also contributing to greater adoption of engineered wood products throughout the region.

Brazil remained the dominant country in Latin America due to its strong furniture manufacturing industry and expanding residential construction activities. One unique growth driver is the growing export of MDF-based furniture products to North America and Europe. Brazilian manufacturers continue investing in plantation forestry resources and advanced wood processing facilities to strengthen production efficiency and raw material availability. Domestic demand for affordable modular furniture is also increasing as urban apartment living becomes more common in major metropolitan areas. Additionally, the expansion of home renovation retail chains and interior decoration services is contributing to rising MDF panel consumption across residential and commercial construction applications.

Competitive Landscape

The medium density fiberboard market is moderately consolidated, with a mix of global manufacturers, regional producers, and vertically integrated wood product companies. Competition is primarily driven by production capacity, raw material access, sustainability certifications, and distribution networks across furniture and construction industries. Leading companies are focusing on expanding low-emission MDF production, improving moisture resistance grades, and increasing the share of recycled wood fiber usage to meet environmental standards.

Key players such as Kronospan, EGGER Group, Arauco, Sonae Arauco, and Greenply Industries dominate the global supply landscape. Among these, Kronospan is considered a leading market player due to its extensive manufacturing footprint across Europe, North America, and Asia, along with its strong vertical integration from raw material sourcing to finished board production.

Strategically, companies are investing in capacity expansion, particularly in Asia Pacific and Latin America, where demand from furniture manufacturing and construction sectors is rising rapidly. For example, producers are setting up new MDF plants near timber-rich regions to reduce logistics costs and ensure stable raw material supply. Sustainability remains a key competitive factor, with firms launching formaldehyde-free and low-VOC MDF boards aligned with green building certifications.

Recent developments also show increased partnerships between MDF manufacturers and furniture brands to ensure customized board specifications for modular furniture lines. Digital supply chain management and automated production lines are further improving efficiency and reducing operational costs.

Key Players List

- Kronospan

- EGGER Group

- Arauco

- Sonae Arauco

- Greenply Industries Ltd.

- Century Plyboards (India) Ltd.

- Georgia-Pacific LLC

- West Fraser Timber Co. Ltd.

- Weyerhaeuser Company

- Daiken Corporation

- Norbord Inc.

- Kastamonu Entegre

- Swiss Krono Group

- UPM-Kymmene Corporation

- Boise Cascade Company

- Finsa (Financiera Maderera S.A.)

- Masisa S.A.