Medical Tubing And Catheters Market Size and Growth

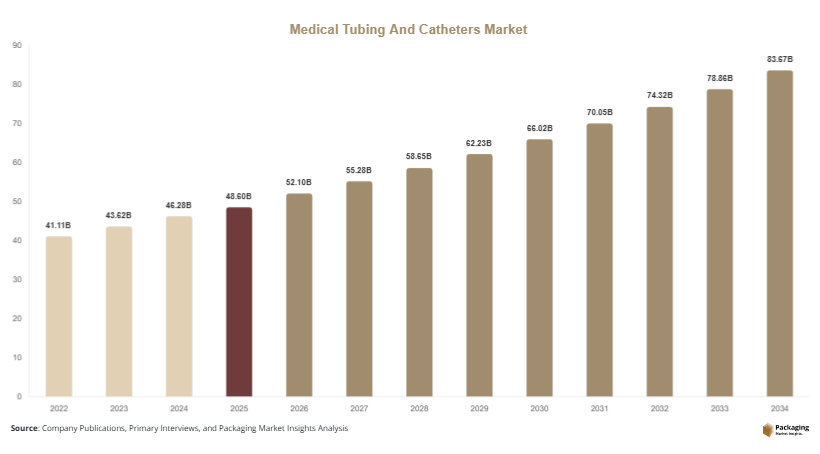

The global Medical Tubing And Catheters Market was valued at approximately USD 48.6 billion in 2025 and is estimated to reach USD 52.1 billion in 2026. Over the forecast period from 2025 to 2034, the market is projected to grow at a CAGR of 6.1%, reaching nearly USD 88.4 billion by 2034. This consistent growth reflects the essential role of tubing and catheter systems in modern healthcare delivery, ranging from diagnostics to long-term treatment. The global medical tubing and catheters market continues to expand steadily, supported by rising healthcare demand, increasing procedural volumes, and ongoing technological innovation.

A major growth factor is the increasing prevalence of chronic diseases such as cardiovascular disorders, renal diseases, and diabetes. These conditions often require repeated or continuous use of catheters and tubing systems for treatment and monitoring. The aging global population further amplifies this demand, as elderly individuals are more likely to require minimally invasive procedures and long-term care solutions. Additionally, advancements in materials such as silicone, polyurethane, and thermoplastic elastomers are improving product performance, durability, and patient comfort.

Key Highlights:

- Asia Pacific dominated the market with a 36.8% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.6%.

- Silicone-based tubing led the type segment with a 31.4% share, while antimicrobial-coated catheters are expected to grow at a CAGR of 6.8%.

- Hospitals dominated the end-use segment with a 54.2% share, while home healthcare is forecasted to grow at a CAGR of 6.9%.

- Cardiovascular applications led the segment with 39.5% share, while urological applications are expected to grow at a CAGR of 6.4%.

- The United States remained the dominant country with a market size of USD 14.3 billion in 2025 and USD 15.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising adoption of antimicrobial and sensor-enabled catheter technologies

The market is experiencing a noticeable shift toward antimicrobial and technologically advanced catheter solutions designed to improve patient safety. Healthcare providers are increasingly adopting catheters with antimicrobial coatings that reduce the risk of infections, especially in intensive care and long-term catheterization scenarios. These innovations are essential in addressing concerns related to hospital-acquired infections, which can increase treatment costs and patient recovery time.

In addition, sensor-enabled or smart catheters are gaining attention due to their ability to provide real-time data on fluid flow, pressure, and patient condition. This enhances clinical decision-making and improves procedural outcomes. Manufacturers are investing in research to integrate digital features into traditional catheter systems, aligning with the broader trend of digital healthcare transformation. These advancements are gradually reshaping product standards and influencing purchasing decisions across hospitals and healthcare facilities.

Increasing preference for minimally invasive and outpatient procedures

The growing adoption of minimally invasive procedures is significantly shaping the demand for medical tubing and catheter products. These procedures offer reduced recovery time, shorter hospital stays, and lower risks compared to traditional surgical methods. As a result, healthcare providers are increasingly relying on advanced tubing systems that provide flexibility, precision, and durability.

Outpatient and ambulatory surgical settings are also contributing to this trend, as they require efficient and cost-effective medical devices. The demand for high-performance tubing solutions that can support complex procedures is rising steadily. Additionally, advancements in imaging and surgical technologies are enabling more accurate catheter-based interventions, further supporting this shift. Manufacturers are responding by developing products that meet the specific requirements of minimally invasive applications, thereby strengthening their market position.

Market Drivers

Growing burden of chronic diseases and long-term treatment needs

The increasing prevalence of chronic diseases is a major factor driving the medical tubing and catheters market. Conditions such as cardiovascular disorders, kidney diseases, and diabetes require continuous monitoring and repeated medical interventions, often involving catheters and tubing systems. For example, dialysis patients depend on specialized tubing solutions for effective treatment, while cardiac patients frequently undergo catheter-based procedures.

This growing patient population is creating sustained demand for reliable and high-quality medical devices. In addition, advancements in healthcare diagnostics are enabling early detection of diseases, leading to more frequent use of catheter-based treatments. The need for long-term care solutions further strengthens demand, as patients require safe and comfortable devices for extended use. This trend is expected to remain a key driver of market growth over the forecast period.

Expansion of healthcare infrastructure and access in emerging economies

The expansion of healthcare infrastructure in emerging markets is playing a critical role in market growth. Governments and private organizations are investing heavily in building hospitals, clinics, and diagnostic centers to improve healthcare access. This expansion is increasing the demand for essential medical devices, including tubing and catheter systems.

Rising disposable incomes and improving healthcare awareness are encouraging patients to seek better medical treatment, further supporting demand. Additionally, favorable government initiatives and policies are promoting the adoption of advanced medical technologies. Manufacturers are increasingly focusing on these regions to tap into high-growth opportunities, often establishing local production facilities to reduce costs and improve supply chain efficiency. This ongoing development is expected to significantly contribute to global market expansion.

Market Restraint

Concerns related to infection risks and stringent regulatory requirements

Despite technological advancements, infection risks associated with catheter use remain a significant challenge for the market. Catheter-associated infections can lead to severe complications, prolonged hospital stays, and increased healthcare costs. These risks are particularly high in cases involving long-term catheterization, where maintaining hygiene and device integrity becomes more complex.

Regulatory authorities have implemented strict guidelines to ensure product safety and efficacy, which can increase the time and cost required for product approval. Manufacturers must conduct extensive testing and clinical trials, which can delay product launches and limit innovation. Additionally, product recalls due to safety concerns can impact company reputation and financial performance. These factors collectively create barriers for new entrants and pose challenges for existing players aiming to expand their product portfolios.

Market Opportunities

Rising demand for home healthcare and portable medical solutions

The increasing shift toward home healthcare is creating new opportunities for the medical tubing and catheters market. Patients are increasingly opting for treatment at home to reduce hospital visits and associated costs. This trend is driving the demand for portable and easy-to-use medical tubing systems that can be managed by patients or caregivers.

Manufacturers are developing innovative solutions tailored for home use, including simplified catheter kits and compact tubing systems. The integration of telemedicine and remote monitoring technologies is further supporting this trend, enabling healthcare providers to monitor patient conditions without requiring frequent hospital visits. This shift is expected to create significant growth opportunities, particularly in developed markets with advanced healthcare systems.

Advancements in material science and product engineering

Technological advancements in materials and product design are opening new avenues for market growth. The development of bio-compatible materials such as silicone and thermoplastic elastomers is improving the performance and safety of medical tubing and catheters. These materials offer enhanced flexibility, durability, and resistance to chemical reactions, making them suitable for a wide range of applications.

Innovations in product design, including kink-resistant tubing and ergonomic catheter structures, are improving usability and patient comfort. These advancements are particularly important in complex medical procedures that require precision and reliability. Manufacturers are investing in research and development to create differentiated products that meet evolving clinical needs. This focus on innovation is expected to drive market growth and create competitive advantages for key players.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 48.6 Billion |

| Market Size in 2026 | USD 52.1 Billion |

| Market Size in 2034 | USD 88.4 Billion |

| CAGR | 6.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Silicone tubing emerged as the dominant subsegment in 2024, accounting for approximately 31.4% of the total market share. Its widespread adoption is attributed to its superior flexibility, biocompatibility, and durability, making it suitable for a wide range of medical applications. Silicone tubing is widely used in cardiovascular, respiratory, and gastrointestinal procedures due to its ability to withstand extreme conditions and maintain structural integrity. Additionally, its resistance to chemical reactions and ease of sterilization enhance its suitability for long-term use.

Antimicrobial-coated catheters are expected to witness the fastest growth, with a projected CAGR of 6.8% during the forecast period. The increasing focus on infection prevention is driving demand for these advanced products. Healthcare providers are adopting antimicrobial solutions to reduce the risk of complications associated with catheter use. Continuous innovation in coating technologies is further enhancing product effectiveness, supporting the growth of this segment.

By Application

Cardiovascular applications dominated the market in 2024, holding a share of approximately 39.5%. The high prevalence of cardiovascular diseases and the increasing number of catheter-based procedures are key factors driving this segment. Medical tubing and catheters are essential in procedures such as angioplasty and cardiac catheterization, where precision and reliability are critical.

Urological applications are expected to grow at the fastest CAGR of 6.4% during the forecast period. The rising incidence of urinary disorders and the aging population are contributing to this growth. Advanced catheter designs that improve patient comfort and reduce complications are supporting adoption. The increasing availability of specialized urological devices is further driving segment expansion.

By End-Use

Hospitals accounted for the largest share of the market in 2024, representing approximately 54.2% of total revenue. The high volume of surgical procedures and patient admissions in hospitals drives demand for medical tubing and catheter products. Hospitals are also early adopters of advanced technologies, further supporting this segment’s dominance.

Home healthcare is projected to grow at the fastest CAGR of 6.9% during the forecast period. The increasing preference for home-based care and rising healthcare costs are key factors driving this segment. Patients with chronic conditions are increasingly relying on home healthcare solutions, which require reliable and easy-to-use medical devices. This trend is encouraging manufacturers to develop products tailored for home use.

Medical Tubing And Catheters Market Segmentations

By Type

- Silicone Tubing

- PVC Tubing

- Polyurethane Tubing

- Antimicrobial Catheters

By Application

- Cardiovascular

- Urology

- Gastrointestinal

- Respiratory

By End-Use

- Hospitals

- Ambulatory Surgical Centers

- Home Healthcare

Regional Analysis

North America

North America held a significant share of the medical tubing and catheters market in 2025, accounting for approximately 34.2% of global revenue. The region is projected to grow at a CAGR of 5.8% during the forecast period, supported by advanced healthcare infrastructure and high healthcare spending. The presence of leading market players and continuous technological innovation further strengthens the region’s position.

The United States dominates the regional market due to its strong healthcare system and high adoption of advanced medical devices. A notable growth factor is the emphasis on research and development, which drives continuous product innovation. Additionally, favorable reimbursement policies encourage the adoption of advanced catheter technologies, supporting sustained market growth.

Europe

Europe accounted for around 26.5% of the global market share in 2025 and is expected to grow at a CAGR of 5.6% over the forecast period. The region benefits from a well-established healthcare system and increasing demand for minimally invasive procedures. Government initiatives aimed at improving healthcare quality are also contributing to market growth.

Germany leads the European market, supported by its strong manufacturing base and technological expertise. A key growth factor in the region is the increasing focus on sustainability and the adoption of eco-friendly materials in medical devices. This trend is encouraging innovation and aligning with stringent environmental regulations.

Asia Pacific

Asia Pacific dominated the market with a share of 36.8% in 2025 and is expected to register the fastest CAGR of 6.7% during the forecast period. Rapid urbanization, increasing healthcare expenditure, and expanding healthcare infrastructure are driving market growth in the region.

China is the leading country in Asia Pacific, supported by its large population and growing healthcare sector. A unique growth factor is the increasing investment in domestic manufacturing, which enhances product availability and reduces reliance on imports. This development is strengthening the region’s competitiveness and supporting market expansion.

Middle East & Africa

The Middle East & Africa region accounted for approximately 6.3% of the market in 2025 and is expected to grow at a CAGR of 5.9% during the forecast period. The region is witnessing gradual improvements in healthcare infrastructure and increasing awareness of advanced medical treatments.

Saudi Arabia is a key market within the region, driven by significant investments in healthcare development. A notable growth factor is the government’s focus on expanding healthcare access through infrastructure projects. These initiatives are increasing demand for medical devices, including tubing and catheter systems.

Latin America

Latin America held a market share of around 6.2% in 2025 and is projected to grow at a CAGR of 6.6% over the forecast period. The region is experiencing growth due to rising healthcare investments and improving access to medical services.

Brazil dominates the regional market, supported by its expanding healthcare system. A unique growth factor is the growth of the private healthcare sector, which is investing in advanced medical technologies to improve service quality. This trend is driving demand for high-performance medical tubing and catheter products.

Competitive Landscape

The medical tubing and catheters market is moderately consolidated, with several global and regional players competing on the basis of product innovation, quality, and pricing. Companies are focusing on expanding their product portfolios and strengthening their global presence through strategic partnerships and acquisitions. Continuous investment in research and development is enabling manufacturers to introduce advanced products with improved safety and performance.

Medtronic is a leading player in the market, recognized for its extensive range of catheter-based products. The company has recently introduced antimicrobial-coated solutions aimed at reducing infection risks. Other major companies are also focusing on technological advancements and capacity expansion to meet growing demand. Competitive strategies include product launches, mergers, and collaborations to enhance market position and address evolving healthcare needs.

Key Players List

- Medtronic plc

- Becton, Dickinson and Company

- Boston Scientific Corporation

- Teleflex Incorporated

- Smiths Medical

- Cardinal Health

- Cook Medical

- ConvaTec Group

- Coloplast A/S

- Terumo Corporation

- Nipro Corporation

- Freudenberg Medical

- Zeus Industrial Products

- Raumedic AG

- Nordson Corporation