Meat Packaging Films Market Size and Growth

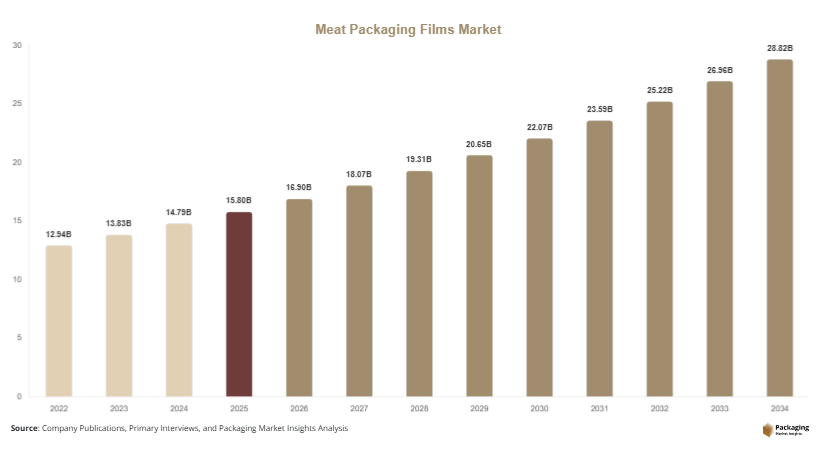

The global meat packaging films market size was valued at approximately USD 15.8 billion in 2025 and is projected to reach USD 16.9 billion in 2026. By 2034, the market is forecasted to achieve nearly USD 30.7 billion, registering a CAGR of 6.9% during 2025–2034. Growth is being supported by increasing consumption of packaged meat products across retail supermarkets, convenience stores, and online grocery channels. Consumers are increasingly preferring pre-packaged meat due to hygiene concerns, convenience, and improved shelf stability.

The meat packaging films market is experiencing consistent expansion due to rising global meat consumption, increasing demand for hygienic food packaging, and advancements in high-barrier film technologies. Meat packaging films are widely used to preserve freshness, extend shelf life, prevent contamination, and improve transportation efficiency for processed and fresh meat products. These films include vacuum packaging films, shrink films, thermoforming films, and modified atmosphere packaging solutions that help maintain product quality throughout distribution channels.

Key Highlights

- Asia Pacific dominated the market with a 36.8% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 7.1%.

- Vacuum packaging films led the type segment with a 34.6% share.

- Polyethylene-based materials dominated the market with a 41.9% share.

- Poultry packaging applications led the segment with 38.7% share.

- The United States remained the dominant country with a market size of USD 3.8 billion in 2025 and USD 4.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable and Recyclable Meat Packaging Films

One of the major trends in the meat packaging films market is the transition toward sustainable and recyclable flexible packaging materials. Food manufacturers and retailers are reducing the use of difficult-to-recycle multilayer plastics and adopting mono-material polyethylene films that support recycling initiatives. Packaging companies are developing thinner high-barrier films that reduce raw material consumption while maintaining oxygen and moisture protection. For example, meat processors in Europe are increasingly adopting recyclable vacuum packaging films for poultry and processed meat products to comply with environmental regulations. This trend is expected to accelerate as governments implement stricter plastic waste reduction policies and consumers demand environmentally responsible packaging solutions.

Rising Demand for Vacuum Skin Packaging Technologies

Another important trend is the growing use of vacuum skin packaging for premium fresh meat products. Vacuum skin packaging tightly seals the film around meat products, improving product visibility, extending shelf life, and reducing leakage. Supermarkets and food retailers are increasingly adopting this technology because it enhances product presentation and minimizes spoilage during transportation. For example, beef producers in the United States and Australia are introducing premium vacuum skin packaged cuts for retail distribution and export markets. The trend is expected to create opportunities for advanced high-barrier films with improved puncture resistance and transparency over the forecast period.

Market Drivers

Growth in Global Meat Consumption and Processed Food Demand

The increasing consumption of meat products worldwide is a key driver for the meat packaging films market. Rising urbanization, changing dietary preferences, and growing disposable income are increasing demand for packaged poultry, beef, pork, and seafood products. Consumers are increasingly purchasing pre-packaged meat due to convenience and hygiene concerns. Packaging films help extend shelf life, reduce contamination, and maintain freshness during storage and transportation. For example, poultry processors in China and India are expanding packaged meat distribution networks to meet rising demand from urban supermarkets and online grocery platforms. As meat consumption continues to rise globally, demand for advanced packaging films is expected to increase steadily.

Expansion of Cold-Chain and Food Distribution Infrastructure

The rapid expansion of cold-chain logistics and refrigerated transportation systems is another major growth driver. Modern meat supply chains require high-performance packaging films that maintain product integrity across long-distance transportation and storage conditions. Vacuum and modified atmosphere packaging technologies help reduce spoilage and preserve product quality during international trade. In Brazil and the United States, meat exporters increasingly rely on multilayer barrier films to improve export efficiency and comply with international food safety standards. Investments in cold storage warehouses and temperature-controlled transportation are expected to support long-term demand for meat packaging films.

Market Restraint

Environmental Concerns Related to Plastic Waste Generation

One of the key restraints affecting the meat packaging films market is increasing environmental concern regarding plastic packaging waste. Most meat packaging films are manufactured using multilayer plastic structures that are difficult to recycle through conventional waste management systems. Governments across Europe and North America are implementing regulations aimed at reducing single-use plastic packaging, which is creating compliance challenges for packaging manufacturers and meat processors. For example, retailers in several European countries are reducing conventional plastic tray and film packaging in response to sustainability targets. In addition, fluctuations in resin prices and recycling infrastructure limitations can increase operational costs for manufacturers. Although recyclable and bio-based packaging solutions are emerging, higher production costs and limited commercial-scale adoption remain major barriers for widespread implementation. These environmental and regulatory challenges may slow market growth in regions with strict sustainability requirements.

Market Opportunities

Expansion of Smart Packaging and Traceability Solutions

The integration of smart packaging technologies presents a significant opportunity for the meat packaging films market. Meat producers and retailers are increasingly adopting QR codes, RFID labels, and freshness indicators to improve traceability and food safety monitoring. Smart packaging solutions help track temperature exposure, expiration dates, and supply chain movement, reducing the risk of contamination and spoilage. For example, premium meat brands in Japan and Germany are integrating digital tracking systems into flexible meat packaging to improve consumer confidence and regulatory compliance. As food safety standards continue to strengthen globally, demand for intelligent packaging films is expected to rise substantially.

Rising Demand for High-Barrier Bio-Based Packaging Films

The development of bio-based and compostable barrier films offers strong future growth opportunities. Packaging companies are investing in renewable polymer technologies and biodegradable coatings to reduce environmental impact while maintaining oxygen and moisture barrier performance. Food manufacturers are increasingly exploring plant-based packaging materials to align with sustainability goals and improve brand positioning. Countries such as Canada and Sweden are supporting investments in sustainable flexible packaging research. As recycling infrastructure and bio-based material availability improve, demand for environmentally friendly meat packaging films is expected to increase across global food processing industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 15.8 Billion |

| Market Size in 2026 | USD 16.9 Billion |

| Market Size in 2034 | USD 30.7 Billion |

| CAGR | 6.9% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Vacuum packaging films dominated the market in 2024 with approximately 34.6% share due to their ability to extend shelf life and reduce oxidation in fresh and processed meat products. These films are widely used across beef, poultry, pork, and seafood packaging applications because they minimize air exposure and prevent bacterial contamination. Supermarkets and food processors increasingly prefer vacuum packaging for premium meat products because it improves product appearance and reduces leakage during transportation. Meat exporters in the United States, Australia, and Brazil rely heavily on high-barrier vacuum films to preserve freshness during international shipments. In addition, advancements in multilayer co-extrusion technologies are improving puncture resistance and transparency, making vacuum packaging films highly suitable for retail meat display applications.

Thermoforming films are projected to be the fastest-growing type segment, registering a CAGR of 7.4% during the forecast period. These films are increasingly used in automated packaging systems due to their flexibility, durability, and cost efficiency. Thermoforming films provide strong sealing performance and are compatible with vacuum and modified atmosphere packaging technologies. Meat processors are investing in thermoforming equipment to improve production speed and reduce packaging waste. In Europe and Asia Pacific, food manufacturers are increasingly adopting recyclable thermoforming film structures to meet sustainability targets. The growth of ready-to-cook packaged meat products and convenience meal kits is expected to create long-term demand for advanced thermoforming packaging solutions.

By Material

Polyethylene-based materials dominated the market in 2024 with a market share of approximately 41.9%. Polyethylene films are widely preferred due to their flexibility, moisture resistance, sealing performance, and cost-effectiveness. These materials are commonly used in vacuum packaging, shrink films, and thermoforming structures for meat packaging applications. Food processors favor polyethylene because it provides strong barrier performance while supporting high-speed packaging operations. In addition, polyethylene films are compatible with multilayer packaging systems that enhance oxygen resistance and shelf stability. The growing global demand for packaged poultry and processed meat products continues to support segment dominance across retail and export-oriented meat industries.

Recyclable mono-material films are expected to emerge as the fastest-growing material segment with a projected CAGR of 7.3% during the forecast period. Sustainability regulations and retailer commitments to reduce plastic waste are encouraging the transition toward recyclable packaging structures. Packaging manufacturers are developing mono-material polyethylene films that maintain barrier performance while improving recyclability. Food retailers in Germany, France, and Canada are increasingly adopting recyclable flexible packaging solutions for fresh meat applications. Companies are also investing in lightweight film technologies that reduce resin consumption without compromising product protection. As circular economy initiatives expand globally, demand for recyclable meat packaging films is expected to increase steadily.

By End-Use

Poultry packaging dominated the global market in 2024 with approximately 38.7% share due to rising worldwide consumption of chicken products and increasing demand for affordable protein sources. Poultry products require protective packaging films that prevent contamination, retain freshness, and maintain product appearance throughout storage and distribution. Supermarkets and food retailers increasingly use transparent vacuum and modified atmosphere packaging films for fresh poultry products to improve shelf presentation and consumer confidence. Countries including the United States, China, and Brazil continue to witness high packaged poultry consumption driven by urbanization and changing dietary habits. In addition, rapid growth in frozen poultry exports is supporting demand for durable high-barrier packaging films.

Processed meat packaging is projected to be the fastest-growing end-use segment, registering a CAGR of 7.2% through 2034. Rising demand for ready-to-eat meat products, sausages, deli meats, and frozen processed foods is supporting segment growth. Consumers increasingly prefer convenient packaged meal solutions due to busy lifestyles and urban work patterns. Packaging companies are developing advanced flexible films with resealable features, antimicrobial coatings, and enhanced oxygen barriers to improve shelf life and product quality. Food manufacturers are also adopting attractive printed packaging designs to improve branding and retail visibility. Growth in convenience food consumption and expanding retail distribution channels are expected to support future demand for processed meat packaging films.

Meat Packaging Films Market Segmentations

By Type

- Vacuum Packaging Films

- Thermoforming Films

- Shrink Films

- Modified Atmosphere Packaging Films

By Material

- Polyethylene

- Polypropylene

- Polyamide

- Recyclable Mono-Material Films

By End-User

- Poultry Packaging

- Beef Packaging

- Pork Packaging

- Seafood Packaging

- Processed Meat Packaging

Regional Analysis

North America

North America accounted for approximately 25.3% of the global market share in 2025 and is projected to grow at a CAGR of 6.2% during the forecast period. The region benefits from high packaged meat consumption, advanced cold-chain logistics, and strong supermarket retail penetration. Consumers in the United States and Canada increasingly prefer packaged fresh meat due to convenience and food safety concerns. Demand for vacuum packaging films and modified atmosphere packaging solutions continues to increase across poultry, beef, and seafood industries. In addition, food safety regulations related to contamination prevention and shelf-life management are encouraging meat processors to adopt advanced high-barrier film technologies. Investments in recyclable packaging innovations are further supporting market growth across the region.

The United States dominates the North American market due to its large meat processing industry and strong retail distribution infrastructure. A unique growth driver in the country is the increasing demand for premium packaged meat products and ready-to-cook meal kits. Supermarkets and online grocery platforms are expanding packaged meat offerings with transparent high-barrier films and resealable packaging formats. Meat exporters are also adopting advanced thermoforming films to improve product protection during international shipments. Rising demand for protein-rich diets and convenience foods is expected to support continued market expansion in the United States.

Europe

Europe represented nearly 23.1% market share in 2025 and is expected to expand at a CAGR of 5.9% through 2034. The region is characterized by strict food safety standards, advanced meat processing industries, and increasing demand for sustainable packaging materials. European meat producers are adopting recyclable flexible packaging and lightweight film structures to reduce environmental impact and comply with regulatory requirements. Demand for vacuum skin packaging is increasing across premium meat categories due to improved product visibility and shelf-life extension. Countries including Germany, France, and the United Kingdom are witnessing rising consumption of packaged poultry and processed meat products through supermarket chains and convenience retail channels.

Germany remains the dominant country in the European market because of its strong processed meat industry and export-oriented food sector. A unique growth factor in Germany is the increasing use of recyclable mono-material packaging films for premium meat packaging applications. Retailers and food brands are introducing sustainable packaging initiatives aimed at reducing plastic waste and improving recycling rates. In addition, meat processors are investing in automated packaging lines and digital traceability technologies to improve efficiency and regulatory compliance. The country’s focus on sustainable food packaging is expected to support long-term market growth.

Asia Pacific

Asia Pacific dominated the global meat packaging films market with a 36.8% share in 2025 and is projected to register a CAGR of 7.3% during the forecast period. Rapid urbanization, rising meat consumption, and expanding organized retail infrastructure are driving regional demand for meat packaging films. Countries such as China, India, Japan, and Thailand are witnessing increasing consumption of packaged poultry, seafood, and processed meat products. Growing middle-class populations and changing dietary habits are supporting higher demand for hygienic and convenient packaged food products. Investments in modern food processing facilities and refrigerated transportation systems are further strengthening the regional market.

China is the leading country in Asia Pacific due to its large meat processing industry and rapidly expanding supermarket retail sector. A unique growth driver in China is the increasing demand for packaged poultry and frozen meat products distributed through e-commerce grocery platforms. Meat processors are adopting advanced vacuum packaging technologies to improve product shelf life and reduce food waste. In addition, government investments in food safety monitoring and cold-chain infrastructure are encouraging the use of high-performance packaging films. Increasing meat exports and urban food consumption are expected to continue supporting regional market growth.

Middle East & Africa

The Middle East & Africa region accounted for approximately 7.4% market share in 2025 and is projected to expand at a CAGR of 6.6% through 2034. Rising urban population, increasing supermarket penetration, and growing demand for halal packaged meat products are supporting market expansion across the region. Countries within the Gulf Cooperation Council are investing in food processing and refrigerated distribution systems to improve food security and reduce import dependence. Demand for leak-resistant and durable meat packaging films is increasing due to high temperatures and long transportation distances. Packaging companies are also introducing multilayer barrier films to improve product freshness and shelf stability.

Saudi Arabia dominates the regional market due to high consumption of packaged poultry and imported meat products. A major growth driver in the country is the expansion of modern retail chains and food distribution infrastructure. Supermarkets are increasingly offering vacuum-packed and modified atmosphere packaged meat products to improve hygiene and convenience for consumers. Meat importers are also investing in advanced packaging technologies to improve transportation efficiency and minimize spoilage during storage. Continued growth in packaged food retail and food service industries is expected to support market demand across the country.

Latin America

Latin America held around 7.4% market share in 2025 and is forecasted to expand at a CAGR of 7.1%, making it one of the fastest-growing regional markets. Increasing meat exports, improving cold-chain logistics, and expanding processed food industries are driving demand for meat packaging films across the region. Consumers are increasingly purchasing packaged poultry and beef products from supermarkets and hypermarkets due to convenience and hygiene considerations. Packaging manufacturers are expanding regional production facilities to meet rising demand for high-barrier flexible films. Government initiatives supporting food export quality standards are further contributing to market growth.

Brazil remains the dominant country in Latin America because of its large poultry and beef export industries. A unique growth factor in Brazil is the rising use of multilayer export packaging films designed for frozen meat transportation. Meat exporters are increasingly adopting advanced vacuum packaging solutions to maintain freshness during long-distance international shipments. The country is also witnessing increased investment in sustainable flexible packaging technologies and food processing infrastructure. Growing global demand for Brazilian meat exports is expected to continue supporting market growth during the forecast period.

Competitive Landscape

The global meat packaging films market is moderately competitive, with major companies focusing on sustainable packaging technologies, advanced barrier materials, and strategic partnerships with food processors. Manufacturers are investing heavily in recyclable mono-material films, multilayer barrier structures, and smart packaging technologies to strengthen their market presence. Companies are also expanding production capacities and automated film manufacturing facilities to meet increasing global demand.

Amcor plc remains one of the leading companies in the market due to its broad flexible packaging portfolio, global manufacturing network, and strong investments in sustainable packaging innovation. Sealed Air Corporation, Berry Global, Winpak Ltd., and Coveris Holdings are also significant market participants focusing on high-barrier vacuum packaging and thermoforming film technologies. Strategic acquisitions, product innovation, and partnerships with meat processing companies continue to shape competitive dynamics across the industry.

Key Players List

- Amcor plc

- Sealed Air Corporation

- Berry Global Inc.

- Winpak Ltd.

- Coveris Holdings S.A.

- Mondi Group

- Constantia Flexibles

- Sonoco Products Company

- Smurfit Kappa Group

- LINPAC Packaging

- Bemis Manufacturing Company

- Kureha Corporation

- Toray Plastics

- Flexopack S.A.

- Clifton Packaging Group Limited