Lubricant Containers Market Size and Growth

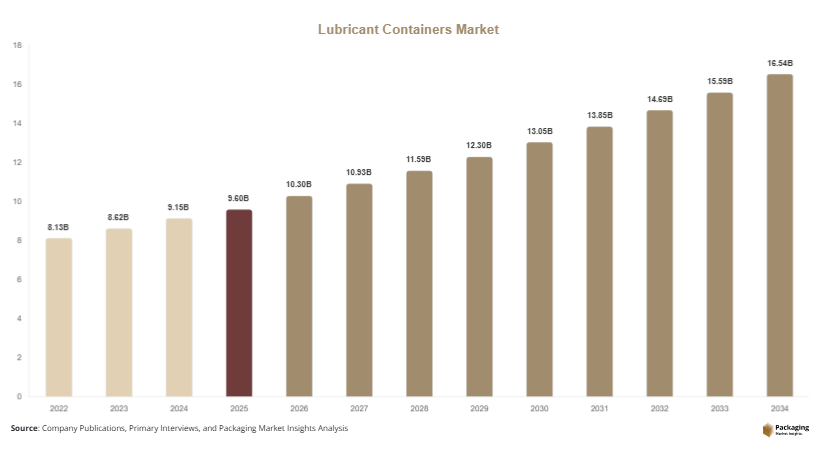

The global lubricant containers market size was valued at approximately USD 9.6 billion in 2025 and is projected to reach USD 10.3 billion in 2026. Over the forecast period from 2025 to 2034, the market is expected to grow at a compound annual growth rate (CAGR) of 6.1%, reaching nearly USD 17.4 billion by 2034. This growth reflects increasing demand for efficient storage, transportation, and dispensing solutions for lubricants across multiple industries.

One of the primary growth factors is the rising demand for automotive lubricants, driven by increasing vehicle production and ownership globally. As automotive engines and machinery require consistent lubrication, the need for durable and leak-proof containers is growing. Secondly, industrial expansion, particularly in manufacturing, construction, and energy sectors, is fueling demand for bulk lubricant storage solutions such as drums, intermediate bulk containers (IBCs), and pails. Thirdly, advancements in packaging technologies are improving container durability, safety, and ease of use, which supports wider adoption across end-use industries.

Key Market Insights

- Asia Pacific dominated the market with a 39.1% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.8%.

- Plastic containers led the type segment with a 54.6% share, while metal containers are expected to grow at a CAGR of 6.5%.

- Rigid packaging dominated with a 71.3% share, while flexible packaging is forecasted to grow at a CAGR of 6.2%.

- Automotive applications led the segment with 48.7% share, while industrial machinery is expected to grow at a CAGR of 6.4%.

- China remained the dominant country with a market size of USD 2.1 billion in 2025 and USD 2.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing adoption of sustainable and recyclable packaging solutions

The lubricant containers market is witnessing a shift toward environmentally friendly packaging solutions as sustainability becomes a key priority for manufacturers and end users. Companies are focusing on using recyclable plastics, reusable containers, and lightweight materials to reduce environmental impact. This trend is supported by regulatory initiatives aimed at reducing industrial waste and promoting circular economy practices. Manufacturers are also developing containers with improved durability to extend product life cycles. The adoption of sustainable packaging solutions not only helps companies comply with regulations but also enhances brand reputation among environmentally conscious consumers.

Integration of advanced dispensing and smart packaging technologies

Technological advancements are shaping the lubricant containers market through the integration of smart and user-friendly features. Modern containers are designed with advanced dispensing mechanisms that improve ease of use and reduce product wastage. Features such as tamper-evident seals, ergonomic handles, and precision pouring systems are becoming standard. Additionally, smart packaging technologies, including RFID tags and QR codes, are being incorporated to enable product tracking and supply chain transparency. These innovations are improving operational efficiency and enhancing user experience, making advanced containers increasingly attractive across industries.

Market Drivers

Growth in automotive and transportation industries

The expansion of the automotive and transportation sectors is a key driver of the lubricant containers market. Increasing vehicle production and rising demand for maintenance services are driving the consumption of lubricants, which in turn increases the need for reliable containers. Automotive workshops, service centers, and retail outlets require packaging solutions that ensure safe storage and easy handling of lubricants. The growth of electric vehicles is also influencing container design, as specialized lubricants require tailored packaging solutions. As the global automotive industry continues to grow, the demand for lubricant containers is expected to increase steadily.

Rising industrialization and infrastructure development

Industrial growth and infrastructure development are significantly contributing to the expansion of the lubricant containers market. Industries such as manufacturing, construction, mining, and energy require large volumes of lubricants to maintain machinery and equipment. This drives demand for bulk packaging solutions such as drums and IBCs. The increasing complexity of industrial operations is also leading to the adoption of specialized containers that ensure product integrity and safety. As emerging economies continue to industrialize, the demand for lubricant containers is expected to rise, supporting overall market growth.

Market Restraint

Fluctuating raw material prices and environmental concerns

The lubricant containers market faces challenges related to fluctuating raw material prices and environmental concerns. Materials such as plastics and metals are subject to price volatility, which can impact production costs and profit margins. Additionally, increasing environmental regulations related to plastic usage and waste management are creating challenges for manufacturers. For example, restrictions on single-use plastics in certain regions may limit the use of conventional plastic containers. Companies must invest in alternative materials and sustainable solutions, which can increase operational costs. These factors collectively act as restraints on market growth, particularly for smaller manufacturers with limited resources.

Market Opportunities

Expansion of reusable and bulk container systems

The growing adoption of reusable and bulk container systems presents significant opportunities for the lubricant containers market. Industries are increasingly shifting toward large-capacity containers such as IBCs and returnable drums to reduce packaging waste and improve cost efficiency. These systems allow for multiple uses, reducing the need for single-use containers and supporting sustainability goals. Companies are also implementing container pooling and return programs to optimize resource utilization. As industries focus on reducing environmental impact and operational costs, the demand for reusable container solutions is expected to increase.

Growth in emerging markets and aftermarket services

Emerging markets offer substantial growth opportunities for the lubricant containers market due to rapid industrialization and increasing vehicle ownership. Countries in Asia Pacific, Latin America, and Africa are witnessing strong growth in automotive and industrial sectors, driving demand for lubricants and associated packaging solutions. Additionally, the expansion of aftermarket services, including vehicle maintenance and repair, is increasing the need for smaller and user-friendly lubricant containers. Companies are expanding their distribution networks in these regions to capture growth opportunities and strengthen market presence.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 9.6 Billion |

| Market Size in 2026 | USD 10.3 Billion |

| Market Size in 2034 | USD 17.4 Billion |

| CAGR | 6.1% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material Type

Plastic containers accounted for the largest share of approximately 54.6% in 2024. These containers are widely used due to their lightweight nature, durability, and cost-effectiveness. They are suitable for various applications, including automotive and industrial lubricants. The availability of different plastic grades allows manufacturers to design containers that meet specific requirements, further supporting their dominance in the market.

Metal containers are expected to grow at a CAGR of 6.5% during the forecast period. These containers offer superior strength and durability, making them suitable for heavy-duty applications. They are commonly used for bulk storage and transportation of lubricants in industrial settings. Increasing demand for high-capacity and reusable containers is driving growth in this segment.

By Packaging Type

Rigid packaging dominated the market in 2024, holding a share of 71.3%. This includes drums, pails, and bottles that provide strong protection and ease of handling. Rigid containers are widely used across industries due to their ability to maintain product integrity and prevent leakage.

Flexible packaging is expected to grow at a CAGR of 6.2%. These solutions offer advantages such as reduced material usage and improved storage efficiency. Flexible containers are increasingly being adopted for smaller lubricant volumes and specialized applications.

By End-Use Industry

The automotive segment dominated the market in 2024, with a share of 48.7%. The high consumption of lubricants in vehicles drives demand for containers in this segment. Automotive service centers and retail outlets require packaging solutions that ensure convenience and safety.

Industrial machinery is expected to grow at a CAGR of 6.4%. The increasing use of lubricants in manufacturing and heavy industries is driving demand for durable and high-capacity containers. The growth of industrial activities further supports this segment.

Lubricant Containers Market Segmentations

By Material Type

- Plastic Containers

- Metal Containers

- Others

By Packaging Type

- Rigid Packaging

- Flexible Packaging

By End-Use Industry

- Automotive

- Industrial Machinery

- Marine

- Aviation

Regional Analysis

North America

North America accounted for approximately 23.4% of the lubricant containers market share in 2025 and is projected to grow at a CAGR of 5.6% during the forecast period. The region benefits from a well-established automotive and industrial base, which drives consistent demand for lubricants and packaging solutions. Increasing focus on sustainability and advanced packaging technologies is also influencing market growth.

The United States dominates the regional market due to its large automotive industry and strong presence of manufacturing sectors. A key growth factor is the increasing demand for high-performance lubricants in industrial applications, which requires specialized containers designed for safety and efficiency.

Europe

Europe held a market share of 25.1% in 2025 and is expected to grow at a CAGR of 5.8%. The region is characterized by stringent environmental regulations and a strong emphasis on sustainable packaging solutions. Companies are adopting recyclable materials and reusable containers to comply with regulatory requirements.

Germany leads the European market, supported by its robust industrial base and advanced manufacturing capabilities. A unique growth factor is the increasing adoption of eco-friendly packaging solutions, which is driving innovation in container design and materials.

Asia Pacific

Asia Pacific dominated the market with a 39.1% share in 2025 and is projected to grow at a CAGR of 6.8%. Rapid industrialization, urbanization, and increasing vehicle ownership are key factors driving market growth in this region. The expanding manufacturing sector further supports demand for lubricant containers.

China is the dominant country, driven by its large industrial base and strong automotive production. A unique growth factor is the rapid expansion of infrastructure projects, which increases demand for lubricants and associated packaging solutions.

Middle East & Africa

The Middle East & Africa region accounted for 6.3% of the market share in 2025 and is expected to grow at a CAGR of 5.7%. The market is gradually expanding due to increasing industrial activities and infrastructure development.

Saudi Arabia is a key market in the region, supported by its oil and gas industry. A unique growth factor is the high demand for industrial lubricants, which drives the need for durable and high-capacity containers.

Latin America

Latin America accounted for 6.1% of the market share in 2025 and is projected to grow at the fastest CAGR of 6.8%. The region is experiencing growth in automotive and industrial sectors, driving demand for lubricant containers.

Brazil dominates the regional market, supported by its large automotive industry. A unique growth factor is the increasing demand for aftermarket automotive services, which boosts the use of small and medium-sized lubricant containers.

Competitive Landscape

The lubricant containers market is moderately competitive, with key players focusing on product innovation, sustainability, and capacity expansion. Companies are investing in advanced manufacturing technologies and developing eco-friendly packaging solutions to meet evolving industry requirements. Strategic partnerships and acquisitions are also common strategies used to strengthen market presence.

Mauser Packaging Solutions is recognized as a leading player in the market, known for its extensive product portfolio and focus on sustainability. The company recently introduced reusable container systems designed to reduce environmental impact. Other key players, including Greif Inc., Berry Global Inc., Schutz GmbH, and Time Technoplast Ltd., are also investing in research and development to enhance product offerings and maintain competitiveness.

Key Players List

- Mauser Packaging Solutions

- Greif Inc.

- Berry Global Inc.

- Schutz GmbH

- Time Technoplast Ltd.

- Balmer Lawrie & Co. Ltd.

- CurTec Holdings B.V.

- Den Hartogh Logistics

- Hoover Ferguson Group

- IPACKCHEM Group

- Jokey Group

- RPC Group Plc

- Plastipak Holdings Inc.

- Alpla Group

- Grief Packaging LLC