Liquid Packaging Market Size and Growth

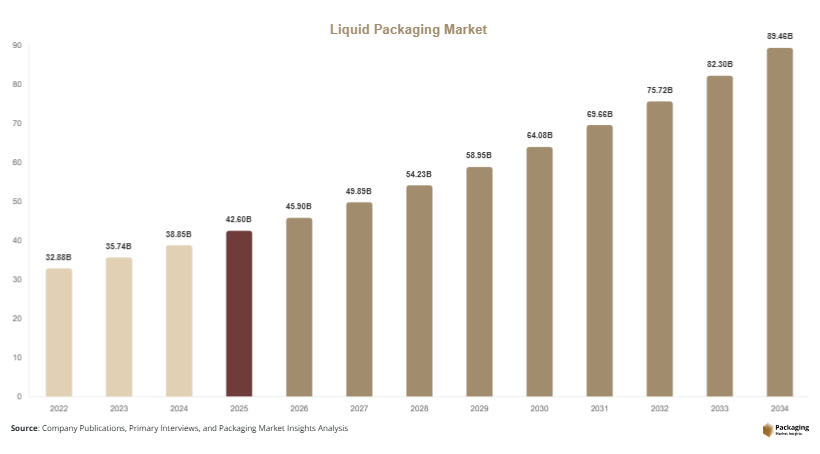

The global liquid packaging market Size is estimated at USD 42.6 billion, and it is projected to reach USD 45.9 billion in 2026. By 2034, the market is expected to reach approximately USD 89.4 billion, expanding at a CAGR of 8.7% (2025–2034). This growth is primarily driven by rising urban consumption patterns, increasing demand for packaged beverages, and technological advancements in packaging materials and machinery.

The liquid packaging market Size is witnessing steady expansion as global demand for safe, efficient, and sustainable packaging solutions for liquid products continues to grow across industries such as food and beverage, pharmaceuticals, personal care, chemicals, and household products. Liquid packaging plays a critical role in preserving product integrity, extending shelf life, and enabling efficient transportation across complex global supply chains. The increasing consumption of bottled beverages, dairy products, liquid medicines, and industrial chemicals has significantly strengthened the demand for advanced liquid packaging solutions, including pouches, cartons, bottles, drums, and flexible packaging formats.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Flexible liquid packaging solutions led the type segment with a 34.1% share.

- Plastic-based packaging dominated with a 53.2% share.

- Food & beverage applications led the segment with 44.6% share.

- The US remained the dominant country with a market size of USD 13.8 billion in 2025 and USD 14.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Sustainable and Lightweight Liquid Packaging

A major trend in the liquid packaging market Size is the increasing shift toward sustainable and lightweight packaging formats. Manufacturers are actively reducing plastic usage and transitioning toward recyclable and bio-based materials such as paper-based cartons, plant-based plastics, and hybrid packaging structures. For example, beverage companies in Europe are increasingly adopting carton-based liquid packaging for milk and juices to reduce carbon emissions and meet regulatory sustainability targets. Similarly, personal care brands in North America are introducing refillable liquid packaging systems to minimize waste generation. This trend is expected to reshape supply chains as companies invest in eco-design packaging technologies and circular economy models, reducing environmental impact while maintaining product safety.

Growth of Smart and Tamper-Evident Liquid Packaging Systems

Another important trend is the adoption of smart and tamper-evident liquid packaging solutions. These systems integrate technologies such as QR codes, NFC tags, temperature sensors, and leak detection indicators to improve product safety and traceability. For instance, pharmaceutical companies are increasingly using tamper-evident liquid packaging for syrups and injectable drugs to ensure regulatory compliance and prevent counterfeiting. In the food industry, smart packaging is being used for dairy and beverage products to monitor freshness and storage conditions. This trend is expected to accelerate with advancements in IoT and digital supply chain systems, enabling real-time tracking and enhanced consumer engagement through connected packaging solutions.

Market Drivers

Rising Consumption of Packaged Beverages and Liquid Foods

The growing consumption of packaged beverages and liquid food products is a major driver of the liquid packaging market Size. Urbanization, busy lifestyles, and increasing health awareness have led to higher demand for bottled water, juices, dairy drinks, and ready-to-drink beverages. For example, large beverage manufacturers in India and China are expanding production capacities to meet rising domestic demand. This has resulted in increased adoption of high-speed liquid filling and packaging systems across manufacturing facilities. Additionally, the expansion of quick-service restaurants and convenience stores has further strengthened demand for efficient liquid packaging solutions.

Expansion of Pharmaceutical and Healthcare Liquid Packaging Demand

Another key driver is the increasing demand for liquid packaging in the pharmaceutical and healthcare sectors. Liquid medicines, syrups, vaccines, and nutritional supplements require highly secure, sterile, and contamination-free packaging solutions. For instance, global vaccination programs have significantly increased demand for specialized liquid vials and ampoules with tamper-proof sealing. Pharmaceutical companies are also investing in advanced packaging technologies that ensure dosage accuracy and extend shelf life. This growing focus on patient safety and regulatory compliance is expected to sustain strong demand for high-quality liquid packaging solutions globally.

Market Restraint

Volatility in Raw Material Prices and Supply Chain Disruptions

One of the key restraints in the liquid packaging market Size is the volatility in raw material prices, particularly plastics, aluminum, and paper-based materials. Fluctuations in crude oil prices directly impact plastic packaging costs, creating uncertainty for manufacturers. Additionally, supply chain disruptions caused by geopolitical tensions, transportation delays, and raw material shortages affect production efficiency. For example, during global logistics disruptions, beverage companies faced delays in obtaining packaging materials, leading to production bottlenecks. These challenges increase operational costs and limit profitability for packaging manufacturers, especially in price-sensitive markets.

Market Opportunities

Growth of E-commerce and Direct-to-Consumer Liquid Product Delivery

The rapid expansion of e-commerce platforms presents a significant opportunity for the liquid packaging market Size. Online grocery delivery services and direct-to-consumer beverage brands require durable, leak-proof, and lightweight liquid packaging solutions to ensure safe transportation. For instance, online dairy and juice delivery companies in urban regions are adopting advanced pouch-based packaging systems to reduce spillage and improve logistics efficiency. This trend is expected to grow further as digital retail platforms expand globally, increasing demand for innovative liquid packaging formats optimized for last-mile delivery.

Advancements in Bio-Based and Edible Liquid Packaging Materials

The development of bio-based and edible liquid packaging materials offers a strong future opportunity. Companies are investing in research to develop packaging derived from seaweed, starch, and biodegradable polymers that reduce environmental impact. For example, pilot projects in Europe are testing edible water capsules for sports events and eco-friendly beverage packaging alternatives. These innovations are expected to gain traction as governments enforce stricter environmental regulations and consumers shift toward sustainable consumption practices. Over time, bio-based liquid packaging could transform traditional packaging systems across multiple industries.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 42.6 Billion |

| Market Size in 2026 | USD 45.9 Billion |

| Market Size in 2034 | USD 89.4 Billion |

| CAGR | 8.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Flexible liquid packaging dominated with a 34.1% share in 2024, driven by its cost efficiency, lightweight nature, and suitability for beverages, dairy, and personal care products. For example, pouch-based packaging is widely used in emerging markets for juices and flavored drinks due to affordability and convenience.

Rigid eco-friendly packaging is the fastest-growing segment with a CAGR of 6.8%, driven by sustainability initiatives and demand for premium packaging formats. Companies are increasingly adopting recyclable cartons and reusable bottles, particularly in Europe and North America. Future growth will be supported by eco-design innovations and regulatory support.

By Material

Plastic-based packaging dominated with a 53.2% share in 2024, due to durability, flexibility, and low production cost. It is widely used in bottled water, soft drinks, and industrial liquids.

Biodegradable and paper-based packaging is the fastest-growing segment with a CAGR of 6.1%, driven by environmental concerns and regulatory pressure. Companies are shifting toward compostable and recyclable packaging materials, especially in food and beverage sectors.

By End-Use

Food & beverage dominated with a 44.6% share in 2024, driven by high consumption of bottled drinks, dairy products, and juices. Packaging plays a critical role in shelf life extension and brand differentiation.

Pharmaceutical liquid packaging is the fastest-growing segment with a CAGR of 6.9%, driven by increasing demand for syrups, vaccines, and liquid medicines. Growth is supported by strict regulatory compliance and rising healthcare expenditure.

Liquid Packaging Market Segmentations

By Type

- Flexible Liquid Packaging

- Rigid Liquid Packaging

- Aseptic Liquid Packaging

- Eco-Friendly Liquid Packaging

- Smart & Connected Liquid Packaging

By Material

- Plastic

- Paper & Paperboard

- Glass

- Metal

- Biodegradable Materials

By End-User

- Food & Beverage

- Pharmaceuticals

- Personal Care & Cosmetics

- Chemicals

- Household Products

Regional Analysis

North America

North America accounted for 29.2% market share in 2025, with a CAGR of 8.1%. The region benefits from advanced packaging technologies, high beverage consumption, and strong pharmaceutical demand. Liquid packaging innovation is strongly supported by automation in manufacturing and high consumer preference for convenience products.

The United States dominates the region due to its large food and beverage industry. A key growth driver is the widespread adoption of smart packaging systems in beverage production facilities. For example, major dairy brands in the U.S. use automated filling and sealing systems integrated with digital tracking technologies to ensure product safety and quality control.

Europe

Europe held 24.5% market share in 2025, with a CAGR of 7.8%. The region is driven by sustainability regulations, strong recycling infrastructure, and high demand for eco-friendly packaging. The liquid packaging market is increasingly focused on reducing plastic usage.

Germany leads the region due to its advanced packaging engineering sector. A key driver is the adoption of recyclable carton-based liquid packaging in dairy and juice industries. For instance, German beverage companies have transitioned to lightweight cartons to meet EU environmental targets and reduce packaging waste.

Asia Pacific

Asia Pacific dominated with 37.4% market share in 2025, and is projected to grow at a CAGR of 9.3%. Rapid urbanization, rising disposable incomes, and expansion of retail and food industries are key growth factors. The region also benefits from large-scale manufacturing capabilities.

China remains the dominant country due to its massive beverage production industry. A key driver is the expansion of bottled water and ready-to-drink beverage consumption. For example, Chinese beverage manufacturers are investing in high-speed liquid filling lines to meet rising domestic and export demand.

Middle East & Africa

The region accounted for 5.8% market share in 2025, with a CAGR of 6.7%. Growth is driven by expanding food import dependency, tourism-driven beverage consumption, and improving retail infrastructure.

The UAE dominates the region due to its strong logistics and hospitality sectors. A key driver is the demand for premium bottled water and beverage packaging in hotels and airlines, supporting growth in high-quality liquid packaging solutions.

Latin America

Latin America held 3.1% market share in 2025, with a CAGR of 6.2%. Growth is driven by expanding food processing industries, rising beverage exports, and increasing retail penetration.

Brazil leads the region due to its strong agricultural and beverage production base. A key driver is the growing export of juices and dairy beverages, requiring durable and transport-friendly liquid packaging solutions.

Competitive Landscape

The liquid packaging market Size is highly competitive, with major players focusing on sustainability, automation, and material innovation. Key companies include Amcor plc, Tetra Pak International S.A., SIG Group, Sealed Air Corporation, and Berry Global Inc. Among these, Tetra Pak International S.A. leads due to its strong global presence and dominance in carton-based liquid packaging solutions.

Companies are investing in recyclable materials, bio-based packaging technologies, and smart packaging integration. Recent strategies include expanding production facilities in Asia, partnerships with beverage manufacturers, and development of low-carbon packaging solutions aligned with global sustainability goals.

Key Players List

- Amcor plc

- Tetra Pak International S.A.

- SIG Group

- Sealed Air Corporation

- Berry Global Inc.

- Huhtamaki Oyj

- Smurfit Kappa Group

- DS Smith Plc

- Mondi Group

- WestRock Company

- Ball Corporation

- Sonoco Products Company

- Elopak ASA

- Evergreen Packaging

- Coveris Holdings S.A.