Labeling Machine Market Size and Growth

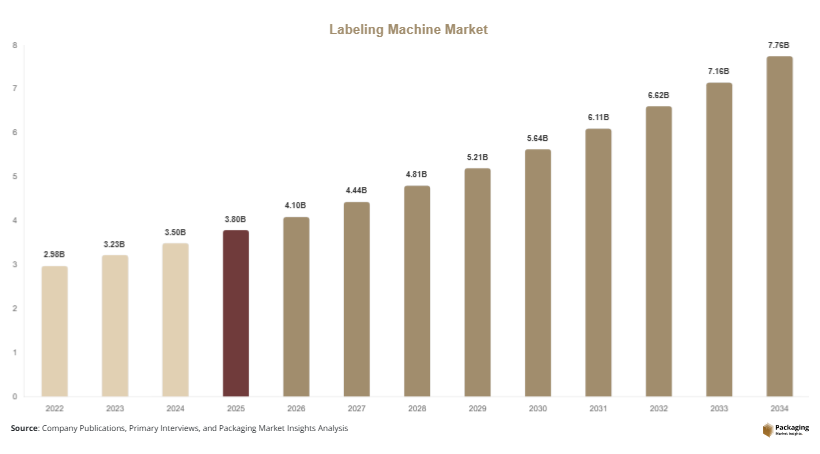

The global labeling machine market is estimated at USD 3.8 billion in 2025, and it is projected to reach USD 4.1 billion in 2026. By 2034, the market is forecasted to expand to approximately USD 7.6 billion, registering a CAGR of 8.3% (2025–2034). This steady growth reflects increasing automation in manufacturing, rising demand for packaged consumer goods, and stricter labeling regulations in pharmaceuticals and food safety sectors.

The labeling machine market has become a critical component of modern packaging automation, driven by rising demand for product traceability, branding precision, and regulatory compliance across industries such as food and beverage, pharmaceuticals, cosmetics, chemicals, and logistics. Labeling machines are no longer limited to simple sticker application systems; they now include high-speed, AI-enabled, vision-integrated, and fully automated systems capable of handling complex packaging lines with minimal human intervention.

Key Highlights:

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Pressure-sensitive labeling machines led the type segment with a 34.8% share.

- Plastic packaging dominated with a 52.1% share.

- Food & beverage applications led the segment with 41.5% share.

- The US remained the dominant country in North America with a market size of USD 1.12 billion in 2025 and USD 1.19 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Integration of Smart and Vision-Based Labeling Systems

One of the most significant trends in the labeling machine market is the integration of smart technologies such as machine vision systems, AI-based quality inspection, and IoT-enabled monitoring. Modern labeling machines are increasingly equipped with high-resolution cameras and sensors that ensure label placement accuracy, detect misalignment, and automatically reject defective packaging without halting production lines. For example, pharmaceutical manufacturers in the U.S. are deploying vision-enabled labeling systems to comply with stringent serialization requirements under DSCSA regulations. These systems improve traceability and reduce human error. In the future, predictive maintenance capabilities will further enhance efficiency by minimizing downtime and optimizing machine performance through real-time analytics.

Shift Toward Modular and Flexible Labeling Equipment

Manufacturers are increasingly adopting modular labeling machines that allow quick changeovers between different product formats, packaging materials, and label types. This trend is especially prominent in the food and beverage industry, where companies frequently introduce seasonal products and SKU variations. For instance, beverage producers in Europe are using modular labeling systems to switch between glass bottles, PET containers, and cans without extensive downtime. This flexibility reduces operational costs and improves production agility. Looking ahead, demand for compact, multi-functional labeling machines will continue to rise, especially among small and mid-sized manufacturers seeking scalable automation solutions.

Market Drivers

Rising Demand for Automated Packaging in Manufacturing Industries

The growing adoption of automation across manufacturing sectors is a key driver of the labeling machine market. Companies are increasingly replacing manual labeling processes with automated systems to improve production speed, reduce labor costs, and ensure consistency. For example, large FMCG manufacturers in India and China are investing in high-speed labeling machines integrated into automated packaging lines to meet rising domestic consumption. This shift is also supported by labor shortages in developed economies, pushing manufacturers toward robotics and automation. As production volumes increase globally, automated labeling solutions are becoming essential for maintaining efficiency and competitiveness.

Regulatory Compliance and Product Traceability Requirements

Strict labeling regulations across pharmaceuticals, food, and chemical industries are significantly driving market growth. Governments in regions such as North America and Europe require detailed product information, including batch numbers, expiration dates, and barcodes for traceability. Pharmaceutical companies, for instance, are adopting advanced labeling machines capable of printing and applying serialized codes to comply with anti-counterfeit regulations. In the food industry, allergen labeling and nutritional transparency requirements are further increasing demand. This regulatory environment ensures continuous investment in advanced labeling technologies, especially in high-compliance sectors.

Market Restraint

High Initial Investment and Maintenance Costs

One of the major restraints in the labeling machine market is the high initial cost associated with advanced automated systems. High-speed, AI-enabled, and fully integrated labeling machines require significant capital investment, which can be challenging for small and medium-sized enterprises. Additionally, maintenance costs, software upgrades, and skilled labor requirements add to operational expenses. For example, SMEs in Southeast Asia often rely on semi-automatic systems due to budget constraints, limiting full-scale automation adoption. This cost barrier slows market penetration in developing regions despite growing demand for packaged goods. Over time, while prices are expected to decrease due to technological advancements, upfront investment remains a key limiting factor.

Market Opportunities

Expansion of E-commerce and Logistics Packaging Automation

The rapid growth of e-commerce platforms worldwide presents a major opportunity for the labeling machine market. With increasing parcel volumes, logistics companies require high-speed labeling systems capable of handling diverse shipping labels, barcodes, and tracking information. For instance, fulfillment centers in the U.S. and China are deploying automated print-and-apply labeling systems to streamline warehouse operations. This trend is expected to grow further with the expansion of same-day and next-day delivery models. In the future, integration of labeling systems with warehouse management software will create fully automated supply chain ecosystems.

Rising Demand for Sustainable and Eco-Friendly Labeling Solutions

Sustainability is emerging as a strong growth opportunity in the labeling machine industry. Manufacturers are increasingly focusing on machines compatible with biodegradable labels, recyclable adhesives, and low-energy consumption systems. For example, European packaging companies are adopting eco-friendly labeling solutions to meet EU sustainability directives. This shift is also driven by consumer preference for environmentally responsible packaging. In the coming years, labeling machines designed for minimal material waste and energy efficiency will see higher adoption across global markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 3.8 Billion |

| Market Size in 2026 | USD 4.1 Billion |

| Market Size in 2034 | USD 7.6 Billion |

| CAGR | 8.3% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Pressure-sensitive labeling machines dominated the market with a 34.8% share in 2024, owing to their versatility, cost efficiency, and compatibility with multiple packaging formats. These machines are widely used in food, beverage, and pharmaceutical industries for high-speed labeling applications. For example, FMCG companies rely on pressure-sensitive systems for bottled products due to their reliability and low maintenance requirements.

Print-and-apply labeling systems are the fastest-growing segment, projected to grow at a CAGR of 6.9%. Growth is driven by increasing demand for logistics automation and barcode-based tracking. These systems are widely adopted in e-commerce warehouses, where real-time label generation is essential for shipping accuracy. Future growth will be supported by integration with AI-based inventory systems.

By Material

Plastic packaging labeling dominated with a 52.1% share in 2024, due to widespread use in beverages, personal care, and household products. Plastic containers require durable, moisture-resistant labels, making them a preferred choice for manufacturers.

Sustainable and paper-based labeling materials are growing at a CAGR of 6.4%, driven by environmental regulations and consumer demand for eco-friendly packaging. Companies in Europe are increasingly adopting recyclable label materials, particularly in organic food and cosmetics sectors. Future innovations will focus on biodegradable adhesives and energy-efficient printing technologies.

By End-Use

Food & beverage dominated with a 41.5% share in 2024, due to high consumption of packaged products and strong demand for branding and regulatory labeling. Beverage manufacturers extensively use high-speed labeling machines for bottles and cans.

Pharmaceuticals are the fastest-growing end-use segment with a CAGR of 6.7%, driven by serialization regulations and anti-counterfeit requirements. Hospitals and drug manufacturers increasingly rely on automated labeling systems for compliance and traceability. Future adoption will rise with global healthcare expansion.

Labeling Machine Market Segmentations

By Type

- Pressure-Sensitive Labeling Machines

- Print-and-Apply Labeling Systems

- Sleeve Labeling Machines

- Wet Glue Labeling Machines

By Material

- Plastic-Based Labels

- Paper-Based Labels

- Metallic Films

- Biodegradable & Eco-Friendly Labels

By End-Use

- Food & Beverage

- Pharmaceuticals

- Cosmetics & Personal Care

- Chemicals

- Logistics & E-commerce

Regional Analysis

North America

North America accounted for approximately 28.6% market share in 2025, with a projected CAGR of 7.9% through 2034. The region benefits from advanced manufacturing infrastructure, strong pharmaceutical compliance requirements, and high automation adoption. The labeling machine market is heavily influenced by food safety regulations and serialization mandates, particularly in the U.S. food and pharmaceutical sectors. The demand for high-speed and vision-based labeling systems is increasing rapidly across large-scale production facilities.

The United States dominates the region due to its strong FMCG and pharmaceutical manufacturing base. A key growth driver is the increasing adoption of smart factory technologies in industrial hubs such as Texas and California. For example, beverage manufacturers in the U.S. are integrating IoT-enabled labeling machines to improve production traceability and reduce recall risks, significantly improving supply chain transparency.

Europe

Europe held around 24.3% market share in 2025, with a CAGR of 7.5% expected. The region is characterized by strict regulatory compliance, sustainability initiatives, and high adoption of automation technologies. Demand is driven by industries such as pharmaceuticals, cosmetics, and premium food packaging.

Germany leads the European market due to its strong industrial automation ecosystem. A key driver is the country’s advanced engineering sector, where manufacturers are increasingly deploying modular labeling systems to support diversified product lines. For instance, German automotive parts suppliers use precision labeling machines for component traceability across global supply chains.

Asia Pacific

Asia Pacific dominated the global market with a 37.4% share in 2025, and is projected to grow at the highest CAGR of 9.2%. Rapid industrialization, expanding FMCG consumption, and rising pharmaceutical production are key growth factors. The region is also witnessing strong investment in packaging automation infrastructure.

China is the dominant country, supported by massive manufacturing output and export-oriented industries. A major growth driver is the expansion of domestic e-commerce platforms, which require high-volume labeling systems for logistics and warehousing operations. For example, Chinese fulfillment centers are adopting fully automated labeling lines integrated with AI-based sorting systems.

Middle East & Africa

Middle East & Africa accounted for 6.8% market share in 2025, with a CAGR of 6.5%. Growth is driven by expanding food processing industries, rising pharmaceutical imports, and infrastructure development in logistics sectors. Countries such as the UAE and Saudi Arabia are investing in modern packaging facilities.

The UAE leads the region due to its strong logistics and re-export industry. A key driver is the development of smart warehouses in Dubai, where automated labeling machines are used to manage high-volume import-export operations efficiently.

Latin America

Latin America held 3.9% market share in 2025, with the fastest regional CAGR of 6.2%. Growth is supported by rising packaged food consumption, retail expansion, and increasing pharmaceutical manufacturing.

Brazil dominates the region due to its large consumer goods industry. A key driver is the expansion of domestic beverage production, where manufacturers are adopting semi-automatic labeling machines to improve productivity and reduce operational bottlenecks in mid-sized factories.

Competitive Landscape

The labeling machine market is moderately consolidated, with key players focusing on automation, innovation, and global expansion. Major companies include Krones AG, Fuji Seal International, Herma GmbH, Barry-Wehmiller Companies, and Accraply Inc. Among these, Krones AG holds a leading position due to its extensive product portfolio and strong presence in beverage packaging automation.

Companies are investing in AI-powered labeling systems, modular machine designs, and energy-efficient technologies. Recent developments include expansion of production facilities in Asia, partnerships with packaging automation firms, and integration of digital monitoring platforms to enhance machine efficiency and predictive maintenance capabilities.

Key Players List

- Krones AG

- Fuji Seal International

- HERMA GmbH

- Barry-Wehmiller Companies

- Accraply Inc.

- Sidel Group

- Marchesini Group

- Label-Aire Inc.

- Newman Labelling Systems

- ProMach Inc.

- Bausch + Ströbel

- Pack Leader Machinery

- Quadrel Labeling Systems

- Vanguard Automation

- Revere Packaging Machinery