Industrial Packaging Market Report Size and Growth

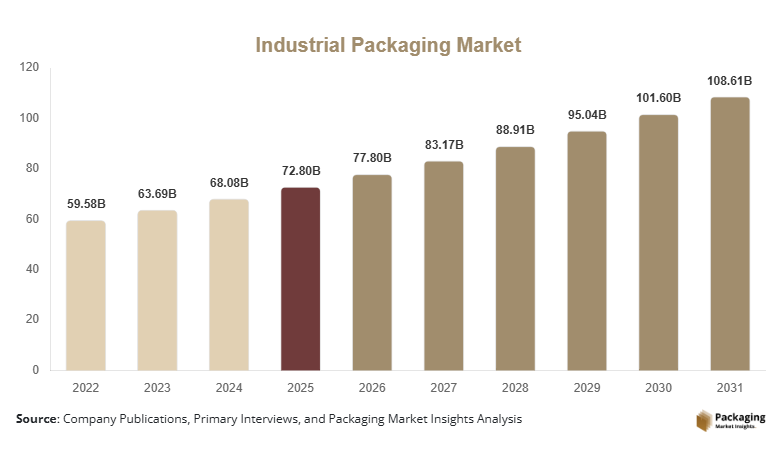

The Industrial Packaging Market was valued at USD 72.8 billion in 2025 and is projected to reach USD 108.6 billion by 2030, registering a compound annual growth rate (CAGR) of 6.9% between 2025 and 2031. Industrial packaging plays a critical role in protecting and transporting bulk goods across sectors such as chemicals, agriculture, construction, pharmaceuticals, and food processing. The market includes packaging formats designed for heavy-duty handling, long-distance transportation, and safe storage of industrial products.

A major global factor supporting the expansion of the Industrial Packaging Market is the rapid growth of global manufacturing and international trade networks. Increasing cross-border shipment of raw materials, chemicals, machinery components, and bulk agricultural commodities has amplified the demand for durable and standardized packaging solutions. Industrial packaging products such as drums, intermediate bulk containers (IBCs), pallets, sacks, and crates are widely used to maintain product integrity during handling, shipping, and storage.

In addition, improvements in supply chain logistics and warehouse automation are encouraging manufacturers to adopt high-performance packaging solutions that improve stacking efficiency, reduce damage risk, and support bulk transportation.

Key Highlights

- Asia Pacific dominated the Industrial Packaging Market in 2025 with a 38.4% share, while Middle East & Africa is projected to record the fastest growth at a 7.8% CAGR during the forecast period.

- In the Type segment, Drums accounted for the largest share in 2024, while Intermediate Bulk Containers (IBCs) are projected to grow fastest at a 7.6% CAGR.

- In the Material segment, Plastic packaging held the dominant share, while composite materials are expected to witness the fastest growth with a 7.4% CAGR.

- The United States remained the dominant country market, valued at USD 14.2 billion in 2025 and estimated to reach USD 15.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable Industrial Packaging

Sustainability has become a key trend influencing the Industrial Packaging Market. Industrial manufacturers and logistics companies are gradually shifting toward recyclable, reusable, and lightweight packaging solutions to reduce environmental impact and comply with regulatory frameworks. Governments in several regions are encouraging circular economy practices, prompting companies to redesign packaging materials to reduce plastic waste and improve recyclability.

Industrial packaging producers are increasingly investing in recycled plastic drums, fiber-based containers, and reusable pallets that support long lifecycle use. Additionally, the integration of biodegradable materials and sustainable coatings has become more common in bulk packaging applications.

Integration of Smart Packaging and Tracking Technologies

Digital transformation in logistics has accelerated the use of smart industrial packaging solutions. Many packaging manufacturers are embedding tracking technologies such as RFID tags, IoT sensors, and QR codes within industrial packaging containers.

These technologies allow companies to monitor shipment location, temperature conditions, and container utilization across supply chains. Such innovations enhance logistics transparency and inventory management efficiency. Smart industrial packaging also helps reduce product loss and enables predictive maintenance for reusable packaging assets.

As supply chains become more data-driven, the adoption of intelligent packaging solutions is expected to play a larger role in the future development of the Industrial Packaging Market.

Market Drivers

Expansion of Global Manufacturing Output

The continuous expansion of global manufacturing activities has significantly supported the growth of the Industrial Packaging Market. Manufacturing industries require robust packaging solutions for transporting raw materials, semi-finished goods, and finished products across supply chains.

Industries such as chemicals, automotive components, electronics, and construction materials rely heavily on industrial packaging products including drums, pallets, crates, and bulk containers. These packaging solutions ensure safe storage and transportation of heavy and hazardous materials. As manufacturing output increases globally, the demand for durable packaging formats continues to grow.

Growth of Bulk Chemical and Petrochemical Trade

Another key driver of the Industrial Packaging Market is the increasing trade of bulk chemicals and petrochemical products. Chemicals are often transported in large quantities using industrial containers such as steel drums, intermediate bulk containers, and flexible bulk bags.

The expansion of petrochemical production in several regions has increased the need for specialized packaging capable of handling hazardous and high-volume liquids. Industrial packaging products are designed to meet strict safety standards, making them essential in chemical supply chains.

As global chemical production and exports continue to expand, demand for high-strength industrial packaging solutions is expected to remain strong.

Market Restraint

Restraint: Volatility in Raw Material Prices

Fluctuations in raw material prices remain a significant challenge for the Industrial Packaging Market. Industrial packaging products are manufactured using materials such as plastic resins, steel, aluminum, and fiberboard. The prices of these materials are highly sensitive to global supply chain disruptions, energy costs, and geopolitical conditions.

Price volatility directly affects production costs for packaging manufacturers. When raw material costs increase sharply, companies may face reduced profit margins or may need to pass the additional costs to end users. This can create pricing pressure in competitive industrial markets.

Furthermore, industries that rely heavily on industrial packaging often seek cost optimization in their logistics operations. As a result, sudden increases in packaging prices can influence purchasing decisions and reduce short-term demand.

Supply chain disruptions affecting steel or polymer availability can also delay production and impact packaging supply. Managing raw material price fluctuations therefore remains a critical challenge for manufacturers operating in the Industrial Packaging Market.

Market Opportunities

Growth of Reusable Industrial Packaging Systems

The growing adoption of reusable packaging systems presents an important opportunity for companies operating in the Industrial Packaging Market. Reusable containers, pallets, and bulk bins are increasingly used in closed-loop supply chains.

These systems allow companies to reduce packaging waste, improve operational efficiency, and lower long-term logistics costs. Industries such as automotive manufacturing, electronics, and food processing are actively implementing returnable packaging solutions for repeated transport cycles.

As sustainability initiatives become more widespread, reusable industrial packaging solutions are expected to gain wider acceptance.

Rising Demand from Emerging Economies

Emerging economies are experiencing rapid industrialization and infrastructure development, which creates strong opportunities for the Industrial Packaging Market. Countries across Asia, Latin America, and Africa are expanding their manufacturing capabilities and export-oriented industries.

Growing industrial output in these regions increases the need for packaging solutions designed for bulk transport and storage. Industrial packaging providers are increasingly establishing production facilities and distribution networks in emerging markets to support local demand.

The continued development of industrial clusters and export-oriented manufacturing zones is expected to generate new growth avenues for packaging manufacturers over the coming years.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 72.8 Billion |

| Market Size in 2026 | USD 77.8 Billion |

| Market Size in 2031 | USD 108.8 Billion |

| CAGR | 6.9% (2026-2031) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2031 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

The Drums segment dominated the Industrial Packaging Market in 2024 and accounted for approximately 32.6% of the market share. Drums are widely used in industrial applications for transporting liquids, chemicals, and hazardous materials. Steel and plastic drums are commonly used due to their durability and ability to withstand harsh transportation conditions.

Their standardized sizes and compatibility with industrial handling equipment made them a preferred choice across chemical, pharmaceutical, and oil industries.

The Intermediate Bulk Containers (IBCs) segment will record the fastest growth with a projected CAGR of 7.6% during the forecast period. IBCs provide higher storage capacity and improved logistics efficiency compared to traditional drums. These containers will gain popularity due to their stackability and compatibility with automated warehouse systems.

By Material

The Plastic segment accounted for the largest share of the Industrial Packaging Market in 2024, representing 41.8% of total market revenue. Plastic packaging materials such as high-density polyethylene are widely used in industrial packaging due to their lightweight structure and chemical resistance.

Plastic drums, containers, and pallets are widely adopted in industries requiring corrosion-resistant packaging.

The Composite Materials segment will witness the fastest growth at a 7.4% CAGR during the forecast period. Composite packaging solutions combine the strength of multiple materials to enhance durability and performance. These materials will gain popularity in applications requiring enhanced load-bearing capacity.

By Application

The Chemical & Petrochemical segment dominated the Industrial Packaging Market in 2024 and held 36.9% of the market share. Industrial packaging plays an essential role in transporting chemicals safely across supply chains.

Steel drums, intermediate bulk containers, and specialized containers are widely used for handling hazardous liquids and chemicals.

The Construction Materials segment will grow at the fastest pace with a projected CAGR of 7.1% during the forecast period. The growth will be supported by rising infrastructure development and increased demand for packaging used in transporting cement additives, coatings, and industrial adhesives.

Industrial Packaging Market Segmentations

By Type

- Drums

- Intermediate Bulk Containers (IBCs)

- Sacks & Bags

- Crates

- Pallets

- Bulk Boxes

By Material

- Plastic

- Metal

- Paper & Paperboard

- Composite Materials

- Wood

By Application

- Chemical & Petrochemical

- Agriculture

- Construction Materials

- Pharmaceuticals

- Food Processing

Regional Analysis

North America

North America accounted for 26.7% of the Industrial Packaging Market share in 2025. The region benefited from a well-established industrial manufacturing ecosystem and strong logistics infrastructure. The market will expand at a CAGR of 5.8% between 2025 and 2033, supported by stable demand from manufacturing and construction sectors.

The United States represented the dominant country within the region. The country's large-scale chemical manufacturing industry created significant demand for bulk industrial containers such as steel drums and intermediate bulk containers. In addition, advanced logistics networks supported the widespread use of palletized industrial packaging solutions across supply chains.

Europe

Europe represented 22.5% of the Industrial Packaging Market share in 2025. The regional market benefited from strong regulatory frameworks governing industrial safety and packaging standards. The market will grow at a CAGR of 5.9% during the forecast period.

Germany emerged as the leading country within the region. The country's strong industrial base, particularly in automotive manufacturing and industrial machinery production, supported consistent demand for heavy-duty packaging systems. Industrial packaging products are widely used for transporting machinery components and industrial chemicals across European supply chains.

Asia Pacific

Asia Pacific held the largest share of the Industrial Packaging Market at 38.4% in 2025. The region benefited from rapid industrialization and expanding manufacturing output across several countries. The regional market will grow at a CAGR of 7.2% during the forecast period.

China dominated the Asia Pacific market. The country’s large manufacturing sector generated significant demand for industrial packaging products used in exporting goods globally. Industrial packaging solutions such as pallets, containers, and flexible bulk bags played an essential role in supporting China's large-scale manufacturing supply chains.

Middle East & Africa

The Middle East & Africa accounted for 7.1% of the Industrial Packaging Market share in 2025. Industrial expansion and increasing petrochemical production supported demand for specialized packaging solutions. The region will grow at a CAGR of 7.8% through the forecast period.

Saudi Arabia represented the dominant country market within the region. The country’s petrochemical and oil refining industries require specialized packaging solutions for transporting chemicals and industrial liquids. Industrial packaging products such as steel drums and bulk containers are widely used in petrochemical logistics.

Latin America

Latin America held 5.3% of the Industrial Packaging Market share in 2025. The regional market benefited from growing agricultural exports and expanding manufacturing sectors. The Industrial Packaging Market in the region will grow at a CAGR of 6.2% during the forecast period.

Brazil emerged as the leading country market in Latin America. The country's strong agricultural export industry generated demand for industrial sacks and bulk containers used in transporting grains, fertilizers, and other commodities. Industrial packaging solutions support the efficient handling and export of agricultural products.

Competitive Landscape

The Industrial Packaging Market is characterized by the presence of global packaging manufacturers and regional suppliers specializing in heavy-duty packaging products. Companies compete based on product durability, material innovation, and global distribution capabilities.

Greif Inc. represents a major market leader with a strong portfolio of industrial containers including steel drums, plastic drums, and intermediate bulk containers. The company continues to expand its global manufacturing footprint and invest in sustainable packaging innovations.

Other key players are also focusing on developing recyclable packaging materials and reusable container systems to meet evolving industrial requirements. Strategic acquisitions and expansion into emerging markets remain common growth strategies among leading companies.

Key Players in the Industrial Packaging Market

- Greif Inc.

- Mauser Packaging Solutions

- Schutz GmbH & Co. KGaA

- International Paper Company

- Mondi Group

- Smurfit Kappa Group

- Berry Global Inc.

- DS Smith Plc

- Sealed Air Corporation

- Nefab Group

- BWAY Corporation

- Hoover Ferguson Group

- Myers Industries Inc.

- Brambles Limited

- Time Technoplast Ltd.