Industrial Labels Market Size and Growth

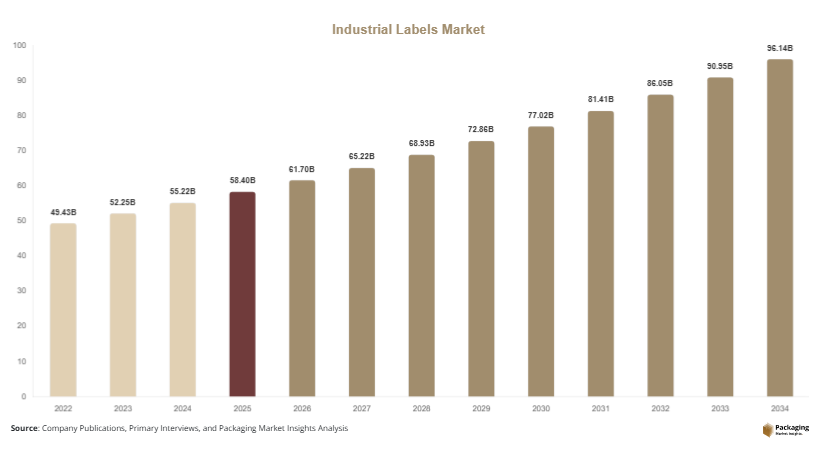

The global industrial labels market size is estimated at USD 58.4 billion in 2025 and is projected to reach USD 61.7 billion in 2026. By 2034, the market is forecast to reach USD 96.2 billion, registering a CAGR of 5.7% during 2025–2034. Growth is supported by rising industrial automation, broader adoption of RFID-enabled labels, and increasing compliance requirements across chemicals, pharmaceuticals, automotive, and electronics manufacturing. The industrial labels market is expanding steadily as manufacturers, logistics providers, and process industries increase their focus on product traceability, regulatory labeling, and durable identification solutions across harsh operating environments.

A key growth factor is the rapid digitalization of industrial supply chains. Manufacturers are increasingly deploying barcode, QR, and smart labeling systems to improve inventory accuracy, production visibility, and lifecycle tracking. Another major factor is the expansion of industrial packaging demand, especially in chemicals, lubricants, electrical equipment, and industrial consumables, where labels serve both compliance and branding purposes. The third notable growth driver is increasing demand for durable materials such as polyester, polypropylene, and metalized labels that resist heat, moisture, abrasion, and chemical exposure in industrial environments.

Key Highlights:

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.4%.

- Pressure-sensitive labels led the type segment with a 34.8% share.

- Polymer-based labels dominated with a 48.6% share.

- Manufacturing applications led end-use demand with 31.7% share.

- The US remained the dominant country with a market size of USD 9.6 billion in 2025 and USD 10.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Smart and Connected Labeling Solutions

The industrial labels market is witnessing strong movement toward connected labeling systems that combine identification with operational intelligence. RFID tags, serialized QR codes, and NFC-enabled labels are increasingly used in manufacturing plants, warehousing, and industrial logistics. For example, industrial equipment suppliers are embedding smart labels on motors, pumps, and electrical assemblies to track maintenance cycles and authenticity. These systems reduce manual scanning time and improve asset visibility across supply chains. Over the forecast period, connected labels are expected to become standard in regulated industries where traceability, anti-counterfeiting, and predictive maintenance create measurable operational value.

Sustainable Industrial Label Materials and Adhesives

Sustainability is becoming an important design factor in industrial labeling. Producers are shifting toward recyclable facestocks, biodegradable liners, solvent-free adhesives, and water-based inks that reduce environmental impact without compromising durability. Packaging manufacturers in Europe are already replacing petroleum-based label films with recycled polymer blends for drums, industrial containers, and secondary packaging. Industrial buyers increasingly assess total packaging sustainability, including labels, adhesives, and release liners. Going forward, circular packaging models and stricter environmental standards are likely to increase demand for lower-emission labeling technologies across industrial packaging, automotive parts labeling, and warehouse identification systems.

Market Drivers

Rising Industrial Automation and Traceability Requirements

Industrial automation is directly increasing demand for advanced labels across production and distribution networks. Automated warehousing, robotic assembly, and digital inventory systems depend heavily on machine-readable labels for tracking components, pallets, finished goods, and spare parts. Automotive plants, for instance, now use serialized industrial labels on thousands of components to enable real-time quality tracking. The effect is greater operational visibility, fewer shipping errors, and improved recall management. As factories continue adopting Industry 4.0 systems, the requirement for durable, data-rich labels is expected to expand significantly across machinery, electronics, chemicals, and industrial packaging operations.

Regulatory Compliance Across Industrial End Markets

Regulatory labeling requirements are supporting long-term industrial labels market growth. Chemical containers require hazard communication labels, pharmaceutical packaging requires serialization, and industrial electrical products often require certification and warning labels. Compliance rules also increasingly mandate permanence, tamper evidence, and scannable coding. For example, battery manufacturers now use multilayer industrial labels showing chemical composition, recycling instructions, and safety warnings. This regulatory complexity increases label sophistication and average selling value. As compliance standards expand globally, industrial producers are expected to invest more in premium label technologies designed for durability, clarity, and long-term traceability.

Market Restraint

Volatility in Raw Material and Adhesive Costs

A major restraint in the industrial labels market is volatility in raw material pricing, particularly polymer films, specialty coatings, inks, release liners, and industrial adhesives. Since many industrial labels require chemical resistance, high-temperature tolerance, UV durability, and extended shelf life, manufacturers depend on specialized substrates whose prices are closely tied to petrochemical cycles and supply chain disruptions. Cost inflation affects both label converters and end users, especially in price-sensitive manufacturing sectors. For example, fluctuations in polypropylene and acrylic adhesive prices have increased procurement costs for heavy-duty drum labeling and warehouse labeling systems. This creates pricing pressure, narrows margins, and can delay adoption of advanced smart label technologies among small and mid-sized industrial buyers.

Market Opportunities

Expansion of RFID and Sensor-Based Industrial Labels

RFID-enabled and sensor-integrated industrial labels offer strong future scope in logistics, maintenance, and industrial asset management. These labels can store operating history, location data, and environmental exposure metrics, making them useful in equipment tracking, cold industrial supply chains, and hazardous materials handling. Industrial gas cylinder tracking is one application where smart labels improve visibility and refill efficiency. Future growth is likely to come from connected factories, where industrial labels function as digital identity layers for machinery, containers, and spare parts. As tag costs decline, adoption across mid-scale manufacturers is expected to accelerate materially.

Growth in Emerging Industrial Manufacturing Hubs

Industrial expansion in India, Vietnam, Mexico, Indonesia, and Brazil is creating substantial opportunity for label manufacturers. Rising factory output, export packaging demand, and infrastructure development are increasing need for compliance labels, logistics labels, and durable asset tags. Electronics assembly hubs in Southeast Asia, for example, require precision labels resistant to heat and solvents used in manufacturing. Future application growth is expected in electrical systems, machinery exports, industrial chemicals, and warehousing. Companies establishing regional converting facilities and localized supply chains are positioned to benefit from rising industrial production and packaging modernization in these developing markets.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 58.4 Billion |

| Market Size in 2026 | USD 61.7 Billion |

| Market Size in 2034 | USD 96.2 Billion |

| CAGR | 5.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Pressure-sensitive labels dominated the industrial labels market in 2024, accounting for 34.8% share. Their market leadership is driven by ease of application, strong adhesion performance, compatibility with multiple surfaces, and suitability for automated production lines. These labels are widely used across drums, cartons, electrical components, industrial machinery, and warehouse logistics systems. Manufacturers favor pressure-sensitive formats because they support variable data printing, barcoding, and durable coatings while reducing operational complexity. Growth is also supported by broad substrate compatibility, including plastics, metals, glass, and coated packaging surfaces used in industrial environments.

RFID labels are the fastest-growing subsegment and are projected to register a 7.3% CAGR through 2034. Growth is being driven by warehouse automation, real-time inventory systems, and industrial asset monitoring. Manufacturers increasingly use RFID labels for pallet tracking, reusable container management, and serialized equipment identification. Packaging innovation in printable antennas and lower-cost chips is improving commercial adoption. Future outlook remains strong as industrial supply chains prioritize visibility, anti-counterfeit tracking, and operational efficiency through intelligent labeling systems integrated into digital industrial infrastructure.

By Material

Polymer-based labels held the leading 48.6% market share in 2024, supported by durability, flexibility, and chemical resistance. Polypropylene, polyester, and polyethylene labels are commonly used where exposure to moisture, oils, solvents, abrasion, or extreme temperatures is expected. Industrial packaging, machinery identification, and long-life compliance labeling rely heavily on polymer-based solutions. For example, lubricant drums and electrical enclosures often use polyester labels with specialty coatings for long-term readability. Their printable surface quality and compatibility with thermal transfer and digital printing also strengthen dominance in high-performance industrial labeling applications.

Eco-friendly paper composites are forecast to grow at a 6.6% CAGR, making them the fastest-growing material category. Growth is supported by sustainability initiatives, liner recycling programs, and low-emission adhesive development. These materials increasingly serve secondary industrial packaging, warehouse labels, and lighter-duty compliance labeling where full polymer durability is unnecessary. Future demand will benefit from innovations in moisture-resistant coatings and reinforced paper composites that improve performance while maintaining recyclability. As industrial buyers incorporate sustainability metrics into packaging procurement, eco-designed label materials are expected to gain broader acceptance across multiple sectors.

By End-Use

Manufacturing was the dominant end-use segment in 2024 with 31.7% market share, driven by labeling needs across equipment, components, packaging, spare parts, and process tracking systems. Modern factories rely on labels for quality control, inventory flow, warning communication, and serialized identification. Automotive plants, electronics manufacturers, and heavy equipment producers all require specialized labels resistant to oils, friction, and heat exposure. The increasing use of automated assembly lines has expanded demand for machine-readable industrial labels with consistent print quality, durability, and traceability performance throughout production and aftermarket servicing.

Pharmaceutical industrial packaging is projected to be the fastest-growing end-use segment, recording a 6.9% CAGR through 2034. Growth is fueled by serialization requirements, anti-counterfeit packaging, temperature-sensitive logistics labeling, and compliance documentation. Pharmaceutical manufacturing also demands highly precise print quality and adhesive stability. Future scope includes smart labels embedded with authentication and tracking features for supply chain security. Sustainability trends in pharmaceutical packaging materials will further encourage innovation in specialty industrial labels designed for compliance, digital verification, and improved lifecycle traceability.

Industrial Labels Market Segmentations

By Type

- Pressure-Sensitive Labels

- Shrink Sleeve Labels

- RFID Labels

- Glue-Applied Labels

- In-Mold Labels

By Material

- Polymer-Based Labels

- Paper-Based Labels

- Metalized Labels

- Composite Eco Materials

By End-User

- Manufacturing

- Chemicals

- Pharmaceuticals

- Automotive

- Electronics

- Logistics & Warehousing

Regional Analysis

North America

North America accounted for 24.6% of the industrial labels market share in 2025 and is projected to grow at a CAGR of 5.1% through 2034. Growth is supported by industrial automation, strong warehousing demand, and regulatory labeling requirements across chemicals, pharmaceuticals, and industrial machinery. The region also benefits from widespread adoption of RFID systems in logistics and manufacturing operations. Industrial e-commerce packaging and serialized product tracking are further expanding label consumption across both primary and secondary industrial packaging formats.

The United States dominates the regional market due to its broad manufacturing base and advanced supply chain digitization. A unique growth driver is high adoption of predictive maintenance systems, where labeled components are digitally linked to service histories and operating data. Industrial equipment manufacturers increasingly use connected labels on pumps, motors, and control systems to improve maintenance scheduling, supporting higher demand for smart industrial labeling solutions.

Europe

Europe held 21.8% market share in 2025 and is forecast to grow at a CAGR of 4.9% during the forecast period. Demand is supported by industrial packaging regulations, advanced printing technologies, and increasing sustainability standards for label materials. Manufacturers across chemicals, automotive components, and industrial goods increasingly prefer recyclable label substrates and low-emission adhesive systems. The region’s export-oriented manufacturing base also supports consistent demand for multilingual compliance labels and durable shipping identification systems.

Germany remains the dominant country in Europe, driven by its strong automotive and machinery sectors. A unique regional growth factor is advanced engineering product labeling, where high-performance labels must withstand oils, heat, vibration, and long operating cycles. Industrial robotics and precision equipment producers increasingly specify engineered polyester and metalized labels, creating higher-value demand segments beyond standard industrial identification applications.

Asia Pacific

Asia Pacific led the market with 39.1% share in 2025 and is projected to expand at a CAGR of 6.3% through 2034. Regional growth is supported by manufacturing expansion, industrial exports, and increasing adoption of automated packaging and labeling systems. Growth in electronics, automotive assembly, industrial chemicals, and electrical equipment production is driving large-volume label demand. Expanding warehouse automation in regional logistics hubs also contributes significantly to barcode and RFID label consumption.

China dominates the Asia Pacific industrial labels market due to large-scale manufacturing output and industrial packaging demand. One unique growth driver is electronics export labeling, where precise, heat-resistant, and anti-static labels are required for components, circuit boards, and industrial devices. As China expands advanced manufacturing and automation infrastructure, demand for intelligent, durable, and compliance-oriented industrial labeling solutions continues to strengthen across multiple verticals.

Middle East & Africa

The Middle East & Africa represented 6.2% share in 2025 and is expected to grow at a CAGR of 5.8% during the forecast period. Industrial diversification, logistics expansion, and packaging modernization are supporting market development. Growth is visible in chemicals, oilfield services, food processing equipment, and industrial exports. Warehousing expansion in regional trade corridors is increasing demand for pallet labels, shipping identification, and heavy-duty adhesive labeling systems designed for high-temperature and dusty operating environments.

The United Arab Emirates leads the region, supported by logistics infrastructure and industrial trade activity. A unique driver is industrial free-zone manufacturing, where exported machinery, industrial packaging, and chemical products require multilingual compliance labeling for international markets. This export-focused labeling requirement is encouraging adoption of durable, weather-resistant industrial labels across packaging, warehousing, and containerized industrial transport operations.

Latin America

Latin America accounted for 8.3% of global market share in 2025 and is projected to record the fastest CAGR of 6.4% through 2034. Rising industrial output, modernization of packaging lines, and stronger regional trade are contributing to growth. Expansion in food processing machinery, agricultural chemicals, industrial lubricants, and warehouse distribution is increasing demand for resilient industrial labels. Local converting capacity is also improving availability of custom industrial label solutions tailored to regional climate and logistics conditions.

Brazil dominates the regional market due to its broad industrial manufacturing and packaging sector. A unique growth factor is agro-industrial chemical labeling demand, where labels must resist moisture, UV exposure, and chemical abrasion during transport and storage. This specialized requirement is creating stronger demand for multilayer laminated labels and advanced adhesive systems, supporting premium product adoption across industrial packaging applications.

Competitive Landscape

The industrial labels market is moderately fragmented, with leading participants competing through material innovation, smart labeling integration, regional expansion, and sustainability-focused product development. CCL Industries remains the market leader due to its broad converting network, diversified industrial label portfolio, and strong capabilities in pressure-sensitive, RFID, and specialty durable labeling products. The company recently expanded advanced RFID industrial label production to address warehouse automation and industrial asset tracking demand.

Other leading companies include Avery Dennison Corporation, 3M Company, UPM Raflatac, and Brady Corporation. Avery Dennison focuses on intelligent labeling platforms and sustainable material innovation. 3M maintains strength in engineered adhesive systems and harsh-environment industrial labeling. UPM Raflatac continues expanding recyclable facestock solutions for industrial packaging. Brady Corporation remains a strong provider in safety, compliance, and industrial identification systems. Strategic partnerships, material science investments, and localized manufacturing are expected to remain central competitive strategies over the forecast period.

Key Players List

- CCL Industries

- Avery Dennison Corporation

- 3M Company

- UPM Raflatac

- Brady Corporation

- Multi-Color Corporation

- Sato Holdings

- Fuji Seal International

- Lintec Corporation

- Henkel AG

- Zebra Technologies

- Flexcon Company

- Resource Label Group

- Schreiner Group

- Coveris Labels