Industrial Foam Market Size and Growth

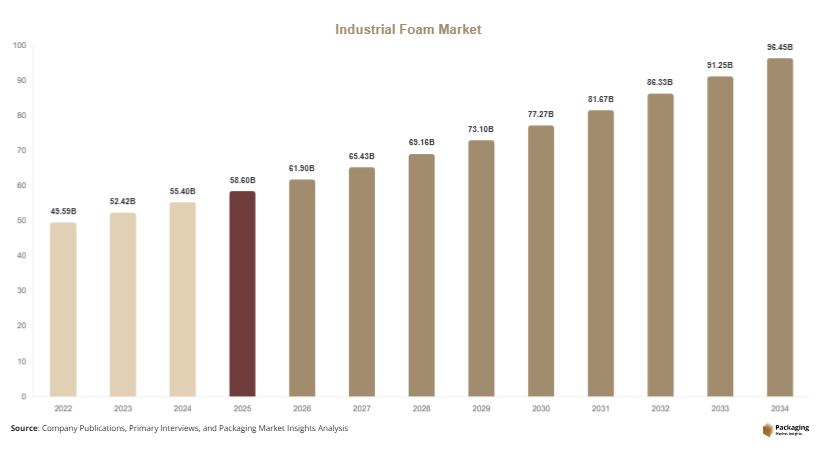

The global industrial foam market size was valued at approximately USD 58.6 billion in 2025 and is projected to reach USD 61.9 billion in 2026, with expectations to grow to USD 96.8 billion by 2034, registering a CAGR of 5.7% during the forecast period from 2025 to 2034. Industrial foam materials, including polyurethane, polystyrene, and polyethylene foams, are widely used due to their lightweight structure, insulation properties, and shock absorption capabilities. The industrial foam market is experiencing steady expansion driven by its widespread application across construction, automotive, packaging, electronics, and furniture industries.

One of the primary growth factors is the increasing demand from the construction sector, where industrial foams are used for insulation, sealing, and energy efficiency applications. As energy regulations become stricter, the need for thermal insulation materials is rising, which directly supports market growth. Another significant factor is the automotive industry’s focus on lightweight materials to improve fuel efficiency and reduce emissions. Industrial foams are extensively used in vehicle interiors, seating, and structural components, contributing to reduced overall vehicle weight.

Key Market Insights:

- Asia Pacific dominated the market with a 41.3% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.1%.

- Polyurethane foam led the type segment with a 36.7% share, while bio-based foams are expected to grow at a CAGR of 6.8%.

- Construction applications dominated with a 39.5% share, while automotive applications are forecasted to grow at a CAGR of 6.2%.

- Packaging end-use led the segment with 34.8% share, while electronics applications are expected to grow at a CAGR of 6.0%.

- China remained the dominant country with a market size of USD 13.2 billion in 2025 and USD 14.0 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Focus on Sustainable and Bio-Based Foam Materials

Sustainability is becoming a key focus area in the industrial foam market as environmental concerns and regulatory pressures continue to increase. Manufacturers are developing bio-based foams derived from renewable resources such as soy and plant oils to reduce dependence on petroleum-based materials. These sustainable alternatives offer comparable performance in terms of insulation and durability while minimizing environmental impact. Recycling technologies are also improving, enabling better recovery and reuse of foam materials. This trend is gaining traction across industries such as construction and automotive, where sustainability goals are becoming integral to product development and corporate strategies.

Rising Adoption of Advanced Foam Technologies in Electronics and Packaging

The adoption of advanced foam technologies is increasing across electronics and packaging applications. High-performance foams with enhanced properties such as flame resistance, thermal stability, and vibration damping are being developed to meet specific industry requirements. In the electronics sector, foams are used for insulation and protection of sensitive components, ensuring product reliability. In packaging, innovations in foam design are improving shock absorption and reducing material usage. The integration of smart manufacturing techniques, including precision molding and automated production, is further enhancing efficiency and product quality.

Market Drivers

Growth in Construction and Infrastructure Development

The expansion of construction and infrastructure projects is a major driver of the industrial foam market. Industrial foams are widely used for insulation, sealing, and structural support in residential, commercial, and industrial buildings. The increasing focus on energy efficiency and sustainable construction practices is driving demand for high-performance insulation materials. Government initiatives promoting green buildings and energy conservation are further supporting market growth. Additionally, rapid urbanization in developing regions is increasing the need for new construction projects, creating significant demand for industrial foam products.

Increasing Demand from Automotive Industry

The automotive industry is another key driver of the industrial foam market, as manufacturers seek lightweight materials to improve fuel efficiency and reduce emissions. Industrial foams are used in vehicle interiors, seating, and structural components, providing comfort and safety while reducing weight. The shift toward electric vehicles is also contributing to market growth, as foams are used for thermal insulation and battery protection. Advancements in foam technology are enabling the development of materials with improved performance characteristics, further supporting their adoption in automotive applications.

Market Restraint

Environmental Concerns and Recycling Challenges

Environmental concerns related to the disposal and recycling of industrial foam materials present a significant challenge for the market. Many foam products are derived from non-biodegradable materials, which contribute to waste accumulation and environmental pollution. Regulatory restrictions on the use of certain chemicals and materials are also impacting production processes. For example, limitations on the use of specific blowing agents in foam manufacturing are increasing compliance costs for manufacturers. Additionally, the lack of efficient recycling infrastructure in some regions further complicates waste management. These factors are encouraging companies to invest in sustainable alternatives, but the transition can be costly and time-consuming.

Market Opportunities

Development of Recyclable and High-Performance Foam Solutions

The development of recyclable and high-performance foam materials presents significant opportunities for market growth. Manufacturers are investing in research and development to create foams that can be easily recycled without compromising performance. Innovations in material science are enabling the production of foams with enhanced durability, thermal resistance, and lightweight properties. These advancements are particularly beneficial for industries such as construction and automotive, where performance requirements are high. Companies that focus on developing sustainable and high-performance solutions are likely to gain a competitive advantage.

Expansion of Emerging Markets and Industrialization

Emerging markets are providing substantial growth opportunities for the industrial foam industry. Rapid industrialization, urbanization, and economic development in regions such as Asia Pacific, Latin America, and Africa are driving demand for foam products. The expansion of manufacturing and construction activities is increasing the need for insulation and protective materials. Additionally, the growth of the middle-class population is driving demand for consumer goods, further supporting market expansion. Companies that establish a strong presence in these regions can benefit from increasing demand and favorable economic conditions.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 58.6 Billion |

| Market Size in 2026 | USD 61.9 Billion |

| Market Size in 2034 | USD 96.8 Billion |

| CAGR | 5.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Polyurethane foam dominated the market in 2024, accounting for approximately 36.7% of the total share. This type of foam is widely used due to its versatility, durability, and excellent insulation properties. It is commonly applied in construction, automotive, and furniture industries, where thermal and acoustic insulation are essential. Polyurethane foam also offers flexibility and resistance to wear, making it suitable for a wide range of applications. Its ability to be customized for different densities and performance requirements further supports its widespread adoption.

Bio-based foams are expected to grow at the fastest CAGR of 6.8% during the forecast period. These foams are derived from renewable resources and are gaining popularity due to increasing environmental concerns. Manufacturers are focusing on developing sustainable alternatives to traditional petroleum-based foams, which is driving innovation in this segment. The demand for eco-friendly materials is expected to continue rising, supporting the growth of bio-based foams.

By Application

The construction segment dominated the market in 2024, holding a share of 39.5%. Industrial foam is widely used in building insulation, sealing, and structural applications. The increasing focus on energy efficiency and sustainable construction practices is driving demand in this segment. Additionally, government regulations promoting green building standards are supporting the adoption of high-performance insulation materials.

The automotive segment is expected to grow at a CAGR of 6.2%, driven by the need for lightweight materials and improved vehicle performance. Industrial foam is used in seating, interiors, and structural components, providing comfort and safety. The shift toward electric vehicles is also contributing to growth, as foams are used for battery insulation and protection.

By End-Use

The packaging segment accounted for the largest share of 34.8% in 2024. Industrial foam is widely used for protective packaging, providing cushioning and shock absorption during transportation. The growth of e-commerce and global trade is driving demand for efficient packaging solutions. Additionally, the need to protect fragile goods is supporting the adoption of foam packaging.

The electronics segment is projected to grow at a CAGR of 6.0%. Industrial foam is used for insulation and protection of electronic components, ensuring product reliability. The increasing demand for consumer electronics and technological advancements are driving growth in this segment. Manufacturers are focusing on developing advanced foam materials to meet the specific requirements of the electronics industry.

Industrial Foam Market Segmentations

By Type

- Polyurethane Foam

- Polystyrene Foam

- Polyethylene Foam

- Bio-based Foam

By Application

- Construction

- Automotive

- Packaging

- Electronics

By End-Use

- Packaging Industry

- Construction Industry

- Automotive Industry

- Electronics Industry

Regional Analysis

North America

North America accounted for approximately 23.7% of the global industrial foam market share in 2025 and is expected to grow at a CAGR of 5.3% during the forecast period. The region’s growth is driven by strong demand from construction, automotive, and packaging industries. The presence of established manufacturers and advanced production technologies supports market development. Increasing focus on energy efficiency and sustainable building practices is also contributing to demand for insulation materials.

The United States is the dominant country in North America, supported by its large construction and automotive sectors. A unique growth factor in this region is the adoption of advanced insulation technologies in green building projects. Government regulations promoting energy efficiency are encouraging the use of industrial foam materials, which is driving market growth.

Europe

Europe held a market share of approximately 21.5% in 2025 and is projected to grow at a CAGR of 5.2%. The region is characterized by strict environmental regulations and a strong focus on sustainability. Demand for industrial foam is driven by construction and automotive applications, where energy efficiency and lightweight materials are essential. Technological advancements in foam production are also contributing to market growth.

Germany leads the European market due to its strong industrial base and focus on innovation. A unique growth factor is the increasing adoption of eco-friendly foam materials in manufacturing processes. Companies are investing in sustainable solutions to comply with regulatory requirements, which is driving market expansion.

Asia Pacific

Asia Pacific dominated the industrial foam market in 2025 with a share of 41.3% and is expected to grow at a CAGR of 6.0%. Rapid industrialization, urbanization, and increasing demand for consumer goods are driving market growth. The expansion of construction and automotive industries in countries such as China and India is a major contributor to demand.

China is the dominant country in the Asia Pacific region, supported by its large manufacturing sector and growing infrastructure development. A key growth factor is the increasing investment in construction projects, which require efficient insulation materials. Rising disposable incomes and urbanization are further supporting market expansion.

Middle East & Africa

The Middle East & Africa region accounted for approximately 6.4% of the global market share in 2025 and is projected to grow at a CAGR of 5.6%. The market is driven by increasing construction activities and the expansion of industrial sectors. Demand for insulation materials is rising due to extreme climatic conditions in the region.

The United Arab Emirates is a leading market in this region, supported by strong infrastructure development and high construction activity. A unique growth factor is the increasing use of insulation materials in commercial and residential buildings to improve energy efficiency, which is driving demand for industrial foam.

Latin America

Latin America held a market share of approximately 7.1% in 2025 and is expected to grow at the fastest CAGR of 6.1%. The region’s growth is driven by rising industrialization and increasing demand for construction materials. The expansion of manufacturing and packaging industries is also supporting market growth.

Brazil is the dominant country in Latin America, driven by its large industrial base and growing construction sector. A key growth factor is the increasing investment in infrastructure development, which is creating demand for insulation and protective materials. This is driving the adoption of industrial foam products across various applications.

Competitive Landscape

The industrial foam market is moderately competitive, with several global and regional players focusing on innovation and sustainability. Companies are investing in research and development to create advanced foam materials with improved performance and reduced environmental impact. Strategic partnerships and expansions are common strategies used to strengthen market presence.

BASF SE is recognized as a leading player in the market, known for its extensive product portfolio and strong global presence. The company recently introduced sustainable foam solutions aimed at reducing environmental impact. Other key players are also focusing on developing innovative products and expanding their production capacities to meet growing demand.

Key Players List

- BASF SE

- Dow Inc.

- Huntsman Corporation

- Recticel NV

- Covestro AG

- Armacell International S.A.

- Zotefoams Plc

- Sekisui Chemical Co., Ltd.

- UFP Technologies Inc.

- Rogers Corporation

- INOAC Corporation

- FoamPartner Group

- Future Foam Inc.

- FXI Holdings Inc.

- Trelleborg AB