Industrial Electronics Packaging Market Size and Growth

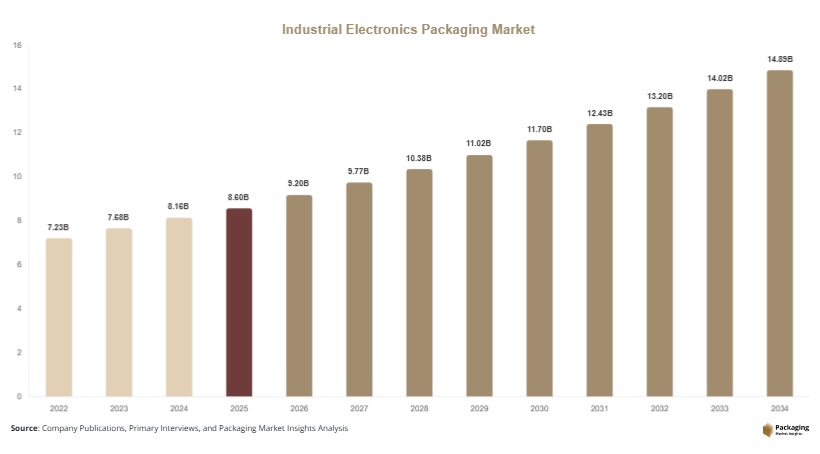

The global industrial electronics packaging market size is estimated at USD 8.6 billion in 2025 and is projected to reach USD 9.2 billion in 2026. Over the forecast period from 2025 to 2034, the market is expected to grow to USD 15.8 billion in 2034, registering a CAGR of 6.2%. The industrial electronics packaging market is expanding steadily as demand rises for durable, protective, and performance-oriented packaging solutions across sectors such as automation, semiconductors, telecommunications, and heavy machinery. Industrial electronics require packaging that ensures protection from moisture, static discharge, vibration, and temperature fluctuations.

One of the major growth factors driving the industrial electronics packaging market is the rapid expansion of industrial automation and smart manufacturing. As industries adopt advanced electronics for production efficiency, the need for specialized packaging solutions that protect sensitive components increases. Packaging plays a critical role in preventing damage during transportation and storage, especially for high-value electronic equipment.

Key Market Insights:

- Asia Pacific dominated the market with a 39.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.7%.

- Anti-static packaging led the type segment with a 32.8% share.

- Plastic materials dominated with a 55.6% share.

- Semiconductor applications led the segment with 41.2% share.

- The US remained the dominant country with a market size of USD 2.1 billion in 2025 and USD 2.3 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing adoption of anti-static and protective packaging solutions

The demand for anti-static and protective packaging is increasing as electronic components become more sensitive to environmental conditions. Industrial electronics such as semiconductors and circuit boards require packaging that prevents electrostatic discharge and physical damage. Companies are adopting advanced materials such as conductive plastics and foam inserts to enhance protection. For example, semiconductor manufacturers use anti-static bags and trays to ensure safe handling and transportation. In the future, innovations in material science are expected to improve performance and reduce costs, supporting wider adoption.

Growing focus on sustainable and reusable packaging designs

Sustainability is becoming a key trend in the industrial electronics packaging market. Manufacturers are developing packaging solutions that are recyclable, reusable, and environmentally friendly. This shift is driven by regulatory requirements and corporate sustainability goals. For instance, companies are introducing reusable packaging systems for industrial electronics to reduce waste. In the coming years, advancements in biodegradable materials and circular economy practices are expected to drive innovation and market growth.

Market Drivers

Expansion of semiconductor and electronics manufacturing

The growth of semiconductor and electronics manufacturing is a major driver of the industrial electronics packaging market. Increasing demand for electronic devices is leading to higher production of components such as chips and sensors. These components require specialized packaging to prevent damage. For example, semiconductor companies use moisture barrier packaging to protect sensitive components. As production volumes increase, the demand for packaging solutions is expected to rise.

Growth of industrial automation and smart manufacturing

The adoption of industrial automation is driving demand for packaging solutions that protect advanced electronic systems. Smart manufacturing relies on interconnected devices that require reliable packaging to ensure performance. For instance, automation equipment manufacturers use durable packaging to protect components during transportation. This trend is expected to continue as industries invest in advanced technologies.

Market Restraint

High cost of advanced packaging materials and solutions

One of the key challenges in the industrial electronics packaging market is the high cost of advanced materials and packaging solutions. Anti-static and moisture barrier materials are more expensive than conventional packaging, which can increase overall costs. For example, small manufacturers may find it difficult to adopt these solutions due to budget constraints. Additionally, customization and specialized designs add to production costs. These factors can limit market growth, particularly in price-sensitive regions.

Market Opportunities

Development of smart packaging technologies

The integration of smart technologies into packaging presents a significant opportunity. Smart packaging solutions can monitor environmental conditions and provide real-time data on product status. For example, sensors embedded in packaging can track temperature and humidity. This helps ensure the safety of industrial electronics during transportation. In the future, the adoption of smart packaging is expected to increase, creating new growth opportunities.

Increasing demand in emerging industrial markets

Emerging markets offer substantial opportunities for the industrial electronics packaging market. Rapid industrialization and infrastructure development are driving demand for industrial electronics. Countries in Asia Pacific and Latin America are investing in manufacturing and automation, which increases the need for packaging solutions. For instance, growing electronics production in India is creating demand for protective packaging. This trend is expected to support market expansion.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 8.6 Billion |

| Market Size in 2026 | USD 9.2 Billion |

| Market Size in 2034 | USD 15.8 Billion |

| CAGR | 6.2% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Anti-static packaging dominated the market in 2024 with a 32.8% share, driven by its ability to protect electronic components from electrostatic discharge. This type of packaging is widely used in semiconductor and electronics manufacturing industries. For example, anti-static bags and trays are used to transport sensitive components safely. The increasing demand for advanced electronics is supporting the growth of this segment.

Moisture barrier packaging is the fastest-growing segment, with a CAGR of 6.5%. This growth is driven by the need to protect components from humidity and environmental conditions. Industries such as semiconductor manufacturing are adopting these solutions. Future innovations in materials are expected to enhance performance and expand applications.

By Material

Plastic materials dominated the market with a 55.6% share in 2024, driven by their durability and versatility. These materials are widely used in industrial electronics packaging due to their cost efficiency and protective properties. For instance, polyethylene and polypropylene are commonly used materials.

Biodegradable materials are the fastest-growing segment, with a CAGR of 6.4%. The growth is driven by increasing demand for sustainable packaging solutions. Companies are investing in eco-friendly materials to meet regulatory requirements. Future advancements are expected to improve performance and adoption.

By End-Use

Semiconductor applications accounted for the largest share of 41.2% in 2024, driven by the need for protective packaging solutions. Microchips and electronic components require packaging that prevents damage during transportation. For example, semiconductor companies use specialized packaging to ensure product safety.

Industrial automation is the fastest-growing segment, with a CAGR of 6.6%. The increasing adoption of automation technologies is driving demand for packaging solutions. As industries invest in advanced systems, the need for reliable packaging will continue to grow.

Industrial Electronics Packaging Market Segmentations

By Packaging Type

- Protective Packaging

- Anti-Static Packaging

- Moisture Barrier Packaging

- Thermal Insulated Packaging

- Custom Industrial Packaging

By Material

- Plastics

- Metals

- Paper & Paperboard

- Advanced Composite Materials

By End-Use Industry

- Automotive Electronics

- Consumer Electronics

- Industrial Machinery

- Aerospace & Defense

- Energy & Power Equipment

Regional Analysis

North America

North America accounted for approximately 24.3% of the global market share in 2025 and is projected to grow at a CAGR of 5.9% through 2034. The region benefits from a strong presence of semiconductor and electronics manufacturers, as well as advanced logistics infrastructure. The demand for high-performance packaging solutions is driven by the need to protect sensitive components during transportation and storage. Sustainability initiatives and regulatory requirements are encouraging the adoption of eco-friendly materials. Additionally, the growth of industrial automation and smart manufacturing is supporting market expansion.

The United States dominates the regional market due to its advanced industrial base and high demand for electronics. A unique growth driver is the increasing adoption of electric vehicles, which require complex electronic systems. For example, EV manufacturers use specialized packaging for battery management systems. This trend is expected to drive demand for industrial electronics packaging in the region.

Europe

Europe held a 22.1% market share in 2025 and is expected to grow at a CAGR of 5.7% during the forecast period. The region’s focus on sustainability and strict environmental regulations is shaping the market. Countries such as Germany, France, and the UK are leading the adoption of recyclable packaging materials. The demand for high-quality packaging solutions is driven by the automotive and industrial sectors.

Germany is the dominant country in the region, supported by its strong manufacturing industry. A unique growth driver is the emphasis on precision engineering, which requires reliable packaging for sensitive components. For instance, industrial equipment manufacturers use customized packaging solutions to protect electronics. This trend is expected to support market growth.

Asia Pacific

Asia Pacific emerged as the largest regional market with a 39.1% share in 2025 and is projected to grow at a CAGR of 6.6%. Rapid industrialization, expanding electronics manufacturing, and increasing investments in infrastructure are driving market growth. Countries such as China, India, and Japan are major contributors. The demand for industrial electronics is increasing, which boosts the need for packaging solutions.

China dominates the region due to its large manufacturing base. A key growth driver is the expansion of the semiconductor industry. For example, electronics manufacturers use advanced packaging to protect components during export. Government support for industrial growth is also contributing to market expansion.

Middle East & Africa

The Middle East & Africa region accounted for 6.8% of the market share in 2025 and is expected to grow at a CAGR of 6.1%. The region is experiencing growth due to increasing investments in industrial sectors and infrastructure development. Countries such as the UAE and South Africa are expanding their manufacturing capabilities, which drives demand for packaging solutions.

The UAE is a key market, supported by its growing industrial base. A unique growth driver is the expansion of logistics and trade hubs. For example, companies are adopting durable packaging to protect electronics during transit. This trend is expected to support market growth.

Latin America

Latin America held a 10.7% market share in 2025 and is projected to grow at the fastest CAGR of 6.7%. The region is experiencing growth due to expanding industrial and manufacturing sectors. Countries such as Brazil and Mexico are key contributors. The rising demand for electronics is driving the need for packaging solutions.

Brazil dominates the regional market due to its large industrial base. A unique growth driver is the growth of renewable energy projects, which require industrial electronics. For instance, packaging solutions are used to protect components in solar and wind energy systems. This trend is expected to support market growth.

Competitive Landscape

The industrial electronics packaging market is moderately fragmented, with several global and regional players competing on innovation, material quality, and sustainability. Companies are focusing on developing advanced packaging solutions that meet the evolving needs of the electronics industry.

Amcor Plc is identified as a market leader due to its strong product portfolio and focus on sustainable packaging solutions. The company invests in research and development to improve material performance and reduce environmental impact. Other key players are adopting strategies such as mergers, acquisitions, and partnerships to strengthen their market position.

Recent developments include the introduction of smart packaging solutions, advancements in biodegradable materials, and expansion into emerging markets. Companies are also focusing on automation to improve production efficiency and reduce costs.

Key Players

- Amcor Plc

- Sealed Air Corporation

- Berry Global Inc.

- Mondi Group

- Sonoco Products Company

- Smurfit Kappa Group

- DS Smith Plc

- International Paper Company

- WestRock Company

- Huhtamaki Oyj

- UFP Technologies

- Pregis LLC

- Storopack Hans Reichenecker GmbH

- Polyplus Packaging

- Protective Packaging Corporation