Home Care Packaging Market Size and Growth

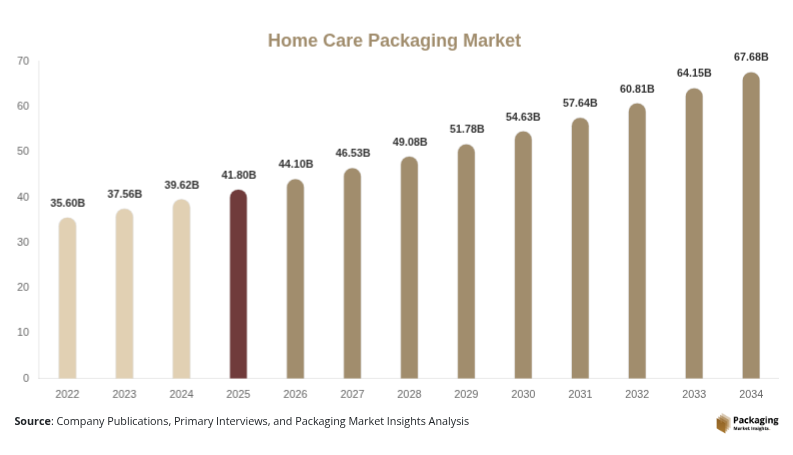

The global home care packaging market was valued at USD 41.8 billion in 2025 and is projected to reach USD 67.9 billion by 2034, expanding at a CAGR of 5.5% during the forecast period from 2025 to 2034. The market continues to grow steadily due to rising consumer demand for household cleaning products, fabric care solutions, surface disinfectants, and air fresheners. Increasing urbanization, growing awareness regarding hygiene standards, and the expansion of organized retail channels are creating sustained demand for innovative packaging solutions across developed and emerging economies.

Home care packaging includes bottles, pouches, cans, cartons, dispensers, trigger sprays, and flexible containers used for detergents, cleaners, sanitizers, and related products. Manufacturers are increasingly focusing on packaging designs that improve convenience, durability, refillability, and product safety. Demand for lightweight packaging materials and recyclable formats is also accelerating across the industry. Plastic-based containers remain dominant due to their low production cost, chemical resistance, and flexibility in design, while paper-based and mono-material packaging solutions are gaining traction because of sustainability targets.

Key Highlights

- Asia Pacific dominated the market with a 38.1% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.4%.

- Bottles & containers led the type segment with a 34.8% share.

- Plastic packaging dominated the material segment with a 57.6% share.

- Household cleaning products led the end-use segment with 45.7% share.

- The US remained the dominant country with a market size of USD 8.7 billion in 2025 and USD 9.1 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Rising Adoption of Refillable and Reusable Packaging Systems

The increasing shift toward sustainable consumption patterns is driving demand for refillable and reusable packaging systems in the home care packaging market. Consumers are becoming more aware of plastic waste generation associated with household cleaning products, leading manufacturers to introduce refill stations, reusable bottles, and concentrated cleaning formulations. Several retail chains are partnering with cleaning product brands to deploy refill kiosks in supermarkets and convenience stores. Flexible refill pouches are gaining traction because they reduce plastic consumption while lowering transportation and storage costs.

Companies are also redesigning product packaging to encourage long-term reuse. Durable trigger-spray bottles and aluminum dispensers are becoming more common in premium product categories. The future impact of this trend will be substantial as governments introduce stricter regulations regarding single-use plastics. Over the next decade, reusable packaging systems are expected to become standard across detergent, surface cleaner, and dishwashing liquid categories, particularly in North America and Europe.

Growth of Smart and Functional Packaging Solutions

The home care packaging market is witnessing increasing integration of smart packaging technologies and advanced dispensing systems. Manufacturers are introducing packaging with controlled dispensing features, anti-leak closures, child-resistant caps, and digital labels to improve user convenience and product safety. QR codes and connected packaging solutions are also being incorporated to provide usage instructions, refill information, and sustainability details.

For example, premium laundry care brands are using smart dosing caps that minimize detergent wastage and improve product efficiency. Aerosol packaging with enhanced spray precision is also becoming popular in disinfectant and air care products. Future growth in this area will be supported by rising consumer demand for convenience and hygiene-focused packaging. Smart packaging technologies are expected to create stronger brand differentiation and improve customer engagement across retail and online distribution channels.

Market Drivers

Increasing Demand for Household Hygiene Products

Growing consumer awareness regarding hygiene and cleanliness is one of the major factors driving the home care packaging market. Demand for surface disinfectants, floor cleaners, fabric care products, and air sanitizers has increased significantly across residential and commercial sectors. Urban consumers are purchasing a wider range of specialized cleaning products, leading to greater demand for customized packaging formats.

This trend directly increases packaging consumption because each product category requires specific container designs and dispensing systems. Trigger sprays, refill pouches, aerosol cans, and squeeze bottles are increasingly used for convenience and product differentiation. For instance, multinational cleaning brands are expanding their packaging portfolios to cater to antibacterial and eco-friendly cleaning products. Rising hygiene awareness across emerging economies is expected to sustain strong packaging demand during the forecast period.

Expansion of E-Commerce and Organized Retail

Rapid expansion of online retail and supermarket chains is accelerating growth in the home care packaging market. E-commerce platforms require durable and leak-resistant packaging solutions capable of protecting products during long-distance transportation. Packaging manufacturers are developing stronger lightweight containers and flexible packaging formats that reduce shipping costs while maintaining product integrity.

The growth of subscription-based home care product delivery services is also supporting packaging innovation. Concentrated refill packs and compact packaging formats are increasingly used to optimize logistics efficiency. Large retail chains are demanding visually attractive packaging that improves shelf visibility and enhances consumer engagement. This driver is expected to remain important as online grocery sales continue expanding across Asia Pacific, North America, and Latin America.

Market Restraint

Fluctuating Raw Material Prices and Environmental Regulations

Fluctuating prices of plastic resins, aluminum, paperboard, and specialty chemicals remain a significant restraint for the home care packaging market. Packaging manufacturers are highly dependent on petroleum-based raw materials, making production costs vulnerable to global crude oil price volatility. Sudden increases in raw material prices directly affect profit margins and create pricing challenges for packaging suppliers.

In addition, strict environmental regulations regarding plastic waste management are creating operational challenges for manufacturers using conventional plastic packaging. Several countries have introduced regulations targeting single-use plastics and non-recyclable materials, forcing companies to redesign packaging systems and invest in sustainable alternatives. Smaller packaging manufacturers often struggle to absorb these additional compliance costs.

For example, detergent and disinfectant packaging producers in Europe are facing pressure to incorporate recycled content while maintaining packaging durability and chemical resistance. Sustainable materials often carry higher production costs and limited availability, which can slow adoption. Regulatory uncertainty and changing recycling standards may continue to impact investment decisions and supply chain planning across the industry.

Market Opportunities

Development of Sustainable Packaging Materials

Growing environmental concerns are creating significant opportunities for sustainable packaging materials in the home care packaging market. Manufacturers are increasingly investing in biodegradable plastics, recycled polymers, paper-based containers, and compostable flexible packaging formats. Consumer preference for eco-friendly products is encouraging brands to reduce virgin plastic usage and improve recyclability.

The adoption of post-consumer recycled plastics in detergent bottles and refill pouches is expected to increase substantially over the forecast period. Companies are also exploring bio-based materials derived from agricultural waste and renewable resources. Sustainable packaging innovations will create opportunities across premium and mass-market home care product categories. Packaging suppliers capable of balancing sustainability, durability, and cost efficiency are likely to gain competitive advantages in the coming years.

Rising Demand for Premium and Customized Packaging

The increasing premiumization of home care products is creating opportunities for advanced and customized packaging solutions. Consumers are seeking aesthetically appealing packaging with improved functionality and convenience features. Premium detergents, fragrance-based cleaners, and specialty disinfectants are increasingly using customized dispensing systems and attractive packaging designs to differentiate products.

Brands are investing in digital printing, ergonomic bottle designs, and smart dispensing technologies to enhance consumer experience. Customized packaging also supports stronger brand identity and improved shelf visibility in competitive retail environments. Future opportunities are expected to emerge in refillable luxury packaging and smart connected packaging systems. Growing disposable income in emerging economies is likely to accelerate demand for premium home care packaging formats during the forecast period.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 41.8 Billion |

| Market Size in 2026 | USD 44.1 Billion |

| Market Size in 2034 | USD 67.9 Billion |

| CAGR | 5.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Bottles & containers dominated the type segment with a 34.8% market share in 2024. These packaging formats remain widely used across detergents, disinfectants, floor cleaners, and liquid soaps because they provide durability, chemical resistance, and convenient dispensing functionality. Plastic bottles are particularly preferred due to their lightweight structure and compatibility with trigger sprays and pump dispensers. Manufacturers continue to introduce ergonomic bottle designs that improve handling and reduce product wastage. Large cleaning product brands are also adopting transparent packaging to improve product visibility and enhance consumer trust. Bottles & containers remain essential in retail environments because they support attractive branding and labeling. Demand for high-density polyethylene and polyethylene terephthalate containers continues to rise across both premium and mass-market product categories.

Refill pouches are projected to register the fastest CAGR of 6.8% during the forecast period. The growing popularity of sustainable packaging and concentrated cleaning products is strongly supporting demand for refill pouch solutions. Consumers increasingly prefer refill systems because they reduce packaging waste and offer lower product costs. Flexible refill packaging also improves logistics efficiency by reducing transportation weight and storage requirements. Several multinational cleaning product companies are introducing refill-based business models for detergents and liquid cleaners. Future demand is expected to increase further as retailers expand refill stations and governments promote waste reduction initiatives. Packaging manufacturers are developing recyclable mono-material pouches and high-barrier flexible packaging to improve sustainability performance and product shelf life.

By Material

Plastic dominated the material segment with a 57.6% market share in 2024. Plastic packaging remains widely used in the home care industry because it offers strong chemical resistance, lightweight properties, and cost-effective manufacturing. Materials such as HDPE, PET, and polypropylene are extensively utilized in bottles, pouches, caps, and dispensers. Plastic packaging also supports flexible design customization and compatibility with various dispensing systems. Household cleaning product manufacturers prefer plastic because it maintains durability during transportation and storage. In addition, plastic packaging provides effective moisture and contamination protection for liquid and powder-based home care products. The widespread availability of plastic processing infrastructure continues to support its market dominance across developed and emerging economies.

Paper-based packaging is anticipated to witness the fastest CAGR of 6.2% over the forecast period. Increasing environmental concerns and regulatory pressure to reduce plastic waste are accelerating the shift toward paper-based alternatives. Manufacturers are introducing paper bottles, fiber-based cartons, and recyclable paper pouches for selected home care applications. Sustainable branding strategies are encouraging companies to adopt renewable packaging materials with lower environmental impact. Paper-based packaging is also gaining consumer acceptance due to improved recyclability and biodegradable characteristics. Technological advancements in barrier coatings and moisture-resistant paper structures are expected to expand application scope across liquid and powdered cleaning products. Demand for eco-friendly packaging formats is likely to remain strong as sustainability becomes a central purchasing factor.

By End-Use

Household cleaning products accounted for the largest end-use segment with a 45.7% share in 2024. Rising global consumption of laundry detergents, dishwashing liquids, surface cleaners, and floor cleaning solutions is driving demand for diverse packaging formats. Bottles, refill pouches, aerosol cans, and trigger spray containers are extensively used across this category. Packaging plays an important role in product differentiation, ease of use, and transportation safety. Cleaning product brands are increasingly investing in customized packaging designs to strengthen retail visibility and improve customer convenience. Growth in urban households and rising hygiene awareness continue to support consumption of packaged home cleaning products. Demand from institutional and commercial cleaning sectors is also contributing to sustained packaging requirements worldwide.

Disinfectant packaging is projected to grow at the fastest CAGR of 6.6% through 2034. Increasing consumer awareness regarding sanitation and germ protection is driving strong demand for disinfectant sprays, wipes, and liquid sanitizers. Packaging manufacturers are developing specialized leak-proof and tamper-resistant containers to improve product safety and shelf stability. Aerosol cans and precision dispensing systems are increasingly used for household disinfectant applications. Sustainable packaging innovations are also emerging in this segment, including recyclable bottles and refillable spray containers. Future growth is expected to be supported by healthcare-inspired hygiene practices adopted in residential settings. Expanding institutional cleaning activities and commercial sanitation programs will further accelerate demand for disinfectant packaging solutions globally.

Home Care Packaging Market Segmentations

By Type

- Bottles & Containers

- Pouches & Sachets

- Caps & Closures

- Flexible Packaging

- Cartons & Boxes

By Material

- Plastic

- Paper & Paperboard

- Metal

- Glass

- Biodegradable Materials

By End-User

- Laundry Care

- Dishwashing Products

- Surface Cleaners

- Air Care Products

- Toilet Care Products

Regional Analysis

North America

North America accounted for 24.6% of the global home care packaging market share in 2025 and is projected to grow at a CAGR of 5.1% through 2034. The region benefits from high consumer spending on cleaning and hygiene products, along with strong demand for premium packaging solutions. Rising adoption of sustainable packaging materials and refillable packaging systems is supporting market growth. E-commerce expansion across the United States and Canada is also increasing demand for durable leak-proof packaging. Manufacturers are investing in lightweight bottles and recyclable flexible packaging to meet regulatory requirements and consumer sustainability preferences.

The United States dominates the regional market due to high consumption of laundry detergents, disinfectants, and surface cleaners. One unique growth driver in the country is the rapid adoption of concentrated cleaning products packaged in compact refill pouches. Several retailers are promoting refill stations and reusable containers to reduce plastic waste. Home care brands are increasingly introducing post-consumer recycled plastic packaging for household cleaners. Growth in private-label cleaning products and online grocery platforms is expected to further support packaging demand across the country.

Europe

Europe held 22.8% of the global home care packaging market in 2025 and is expected to expand at a CAGR of 4.9% during the forecast period. Strict environmental regulations regarding plastic usage and recycling are strongly influencing packaging innovation in the region. Consumers are increasingly demanding recyclable and reusable packaging solutions for home cleaning products. Demand for paper-based containers and mono-material flexible packaging is growing steadily. The region also benefits from high penetration of automated packaging technologies and strong adoption of sustainable manufacturing practices.

Germany remains the dominant country in the European market because of its advanced packaging industry and strict waste management policies. A major growth driver in Germany is the expansion of refill-based retail models for household cleaners and detergents. Several supermarket chains have introduced refill stations for liquid cleaning products, encouraging reusable packaging adoption. Packaging companies are also investing in recyclable trigger spray systems and biodegradable pouches. Increasing consumer preference for environmentally responsible products continues to reshape packaging strategies across the country.

Asia Pacific

Asia Pacific dominated the global home care packaging market with a 38.1% share in 2025 and is projected to register a CAGR of 6.1% through 2034. Rapid urbanization, rising disposable incomes, and growing household awareness regarding hygiene are fueling strong demand for home care products and related packaging solutions. Expanding middle-class populations in China, India, Indonesia, and Vietnam are contributing to increased consumption of detergents, disinfectants, and surface cleaners. The region also benefits from cost-effective manufacturing capabilities and rising investments in flexible packaging production facilities.

China leads the Asia Pacific market due to large-scale production and consumption of home cleaning products. One unique growth driver in the country is the rapid expansion of e-commerce-based household product sales. Online retailers require durable and compact packaging capable of supporting long transportation cycles. Domestic packaging manufacturers are increasing production of lightweight bottles and flexible refill packs to meet growing demand. Government initiatives promoting recyclable plastics and sustainable packaging materials are also supporting long-term market growth across the country.

Middle East & Africa

The Middle East & Africa accounted for 7.9% of the global home care packaging market in 2025 and is forecast to grow at a CAGR of 5.6% during the study period. Rising urban population growth and increasing awareness regarding household hygiene are supporting demand for cleaning and sanitization products. Expanding retail infrastructure and supermarket penetration are also creating opportunities for packaging manufacturers. Flexible packaging formats are gaining popularity because of their affordability and convenience. Growth in hospitality and commercial cleaning sectors further contributes to rising packaging demand across the region.

Saudi Arabia dominates the regional market due to increasing household consumption and expanding retail distribution channels. One unique growth driver in the country is the rising demand for premium fragranced home care products packaged in aesthetically appealing containers. Local and international brands are introducing customized packaging designs targeting high-income urban consumers. Investments in sustainable packaging production and recycling infrastructure are gradually increasing. The expansion of organized retail and e-commerce platforms is expected to strengthen long-term packaging demand across the country.

Latin America

Latin America represented 6.6% of the global home care packaging market in 2025 and is expected to grow at the fastest CAGR of 6.4% during the forecast period. Rising demand for affordable household cleaning products and expanding urban populations are key factors supporting market growth. Flexible packaging formats are increasingly used due to their low cost and reduced transportation expenses. Growth in supermarket chains and convenience stores is creating opportunities for visually attractive and lightweight packaging solutions. Increasing awareness regarding sanitation and household hygiene also supports product consumption across the region.

Brazil remains the leading market in Latin America due to strong domestic demand for laundry detergents and surface cleaners. One unique growth driver in the country is the rapid growth of economy-sized packaging formats designed for value-conscious consumers. Packaging manufacturers are producing large-volume refill pouches and lightweight plastic containers to address affordability concerns. Domestic brands are also investing in colorful packaging designs to improve retail shelf appeal. Rising e-commerce activity and improvements in regional logistics infrastructure are expected to support future market expansion.

Competitive Landscape

The home care packaging market is moderately consolidated, with major players focusing on sustainable material development, packaging innovation, and strategic partnerships. Amcor plc remains a leading company due to its extensive product portfolio, global manufacturing network, and investments in recyclable packaging technologies. The company continues expanding its flexible packaging solutions designed for refillable and concentrated home care products.

Berry Global Inc., Sonoco Products Company, AptarGroup Inc., and Silgan Holdings Inc. are also key participants in the market. These companies are investing in lightweight packaging solutions, smart dispensing systems, and post-consumer recycled materials to strengthen their competitive positions. Several manufacturers are partnering with consumer goods brands to develop customized eco-friendly packaging formats.

Recent industry developments include investments in mono-material flexible packaging, recyclable trigger spray systems, and refillable dispensing technologies. Packaging suppliers are also adopting digital printing technologies to improve branding flexibility and reduce production lead times. Sustainability initiatives remain central to competitive strategies, with companies focusing on circular economy goals and carbon footprint reduction. Increasing demand for e-commerce-compatible packaging and premium packaging aesthetics is expected to intensify competition during the forecast period.

Key Players List

- Amcor plc

- Berry Global Inc.

- Sonoco Products Company

- AptarGroup Inc.

- Silgan Holdings Inc.

- Gerresheimer AG

- ALPLA Group

- DS Smith plc

- Mondi Group

- Huhtamaki Oyj

- Sealed Air Corporation

- RPC Group plc

- Reynolds Consumer Products

- Graham Packaging Company

- WestRock Company