Highly Visible Packaging Sizing Market Size and Growth

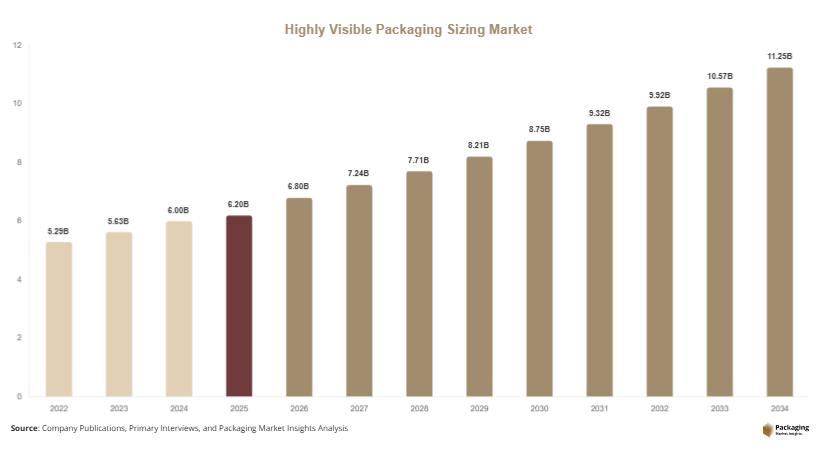

In 2025, the global highly visible packaging sizing market size is estimated at USD 6.2 billion and is projected to reach USD 6.8 billion in 2026. Over the forecast period from 2025 to 2034, the market is expected to grow at a CAGR of 6.5%, reaching approximately USD 11.9 billion by 2034. The highly visible packaging sizing market is gaining traction as brands focus on improving product visibility, shelf impact, and consumer engagement in competitive retail environments.

Highly visible packaging sizing refers to packaging formats, dimensions, and structural designs optimized to enhance product visibility and recognition on shelves or digital platforms. This includes larger front-facing areas, ergonomic designs, and strategic size variations that improve brand communication. One of the primary growth factors is the rapid expansion of organized retail and supermarkets, where shelf competition is intense. Brands are increasingly investing in packaging sizing strategies that improve visibility and differentiate products.

Key Highlights

- Asia Pacific dominated the market with a 38.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 7.2%.

- Flexible visible packaging formats led the type segment with a 33.8% share, while modular packaging sizing is expected to grow at a CAGR of 7.0%.

- Plastic-based materials dominated with a 49.6% share, while paper-based materials are forecasted to grow at a CAGR of 6.8%.

- Food & beverage applications led the segment with 42.9% share, while personal care packaging is expected to grow at a CAGR of 6.9%.

- China remained the dominant country with a market size of USD 1.4 billion in 2025 and USD 1.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing focus on shelf-ready and display-optimized packaging sizes

Retailers and manufacturers are increasingly prioritizing packaging sizing that enhances shelf readiness and visibility. Shelf-ready packaging solutions are designed to be easily placed on retail shelves without additional handling, improving operational efficiency while maximizing product exposure. These packaging sizes often include perforated boxes, stackable formats, and front-facing designs that ensure brand logos and product information remain visible. For example, beverage companies are adopting display-ready cartons that can be directly placed on supermarket shelves, reducing labor costs and improving merchandising. This trend is expected to drive further innovation in packaging design, including customizable sizing formats that align with retailer requirements and consumer preferences.

Integration of right-sized packaging in e-commerce and logistics

The rise of e-commerce has led to increased emphasis on right-sized packaging that balances visibility and efficiency. Packaging that is too large can increase shipping costs, while undersized packaging may compromise product protection and brand visibility. Companies are adopting data-driven approaches to determine optimal packaging sizes for different products. For instance, electronics brands are using compact yet visually appealing packaging that enhances unboxing experiences while reducing material usage. This trend is expected to continue as logistics providers and retailers focus on sustainability and cost efficiency. Future developments may include automated packaging systems that adjust size dynamically based on product dimensions.

Market Drivers

Expansion of organized retail and visual merchandising strategies

The growth of organized retail, including supermarkets, hypermarkets, and convenience stores, is a major driver for the highly visible packaging sizing market. Retail environments are becoming increasingly competitive, with brands competing for consumer attention within limited shelf space. Packaging sizing plays a critical role in visual merchandising, influencing purchasing decisions. Larger front panels, unique shapes, and optimized dimensions help products stand out. For example, snack manufacturers are using vertically extended packaging to increase shelf visibility. This cause-and-effect relationship between retail competition and packaging innovation is driving demand for highly visible packaging sizing solutions.

Rising demand for brand differentiation and consumer engagement

Brands are increasingly using packaging as a tool for differentiation and consumer engagement. Highly visible packaging sizing allows companies to communicate product features, branding, and value propositions effectively. In industries such as personal care and food, packaging size and design significantly influence consumer perception. For example, premium products often use larger or uniquely shaped packaging to convey quality and value. This growing emphasis on branding is encouraging manufacturers to invest in innovative packaging sizing solutions. As competition intensifies, companies that adopt effective packaging strategies are likely to gain a competitive advantage.

Market Restraint

Challenges related to material usage optimization and sustainability

One of the key restraints in the highly visible packaging sizing market is the challenge of balancing visibility with sustainability. Larger or more elaborate packaging sizes can increase material usage, leading to higher costs and environmental concerns. Regulatory pressure to reduce packaging waste is forcing companies to reconsider their sizing strategies. For example, excessive packaging in consumer goods has been criticized for contributing to waste, prompting brands to adopt minimalistic designs. This creates a trade-off between visibility and sustainability. Companies must invest in innovative materials and design techniques to address this challenge, but such investments can increase operational complexity and costs. As a result, sustainability considerations may limit the adoption of certain visible packaging formats.

Market Opportunities

Adoption of smart packaging and digital printing technologies

The integration of smart packaging and digital printing technologies presents significant opportunities for the highly visible packaging sizing market. Digital printing allows for high-quality graphics and customization, enabling brands to create visually appealing packaging without increasing size excessively. Smart packaging features, such as QR codes and augmented reality elements, enhance consumer interaction while maintaining compact packaging sizes. For instance, brands are incorporating scannable codes on packaging to provide additional product information and promotional content. These innovations are expected to drive demand for optimized packaging sizes that balance visibility and functionality.

Growth in emerging markets with expanding retail infrastructure

Emerging markets are offering substantial growth opportunities due to the rapid expansion of retail infrastructure. Countries in Asia, Africa, and Latin America are witnessing the growth of supermarkets and organized retail, which increases the need for effective packaging solutions. For example, retail chains in India and Brazil are adopting standardized shelf layouts, encouraging brands to optimize packaging sizes for visibility. Additionally, increasing disposable incomes and urbanization are driving consumer demand for packaged goods. This trend is expected to create new opportunities for packaging manufacturers to develop region-specific sizing solutions that cater to local market dynamics.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 6.2 Billion |

| Market Size in 2026 | USD 6.8 Billion |

| Market Size in 2034 | USD 11.9 Billion |

| CAGR | 6.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Flexible visible packaging formats dominated the market with a 33.8% share in 2024. These formats include pouches, wraps, and flexible containers that offer enhanced visibility and adaptability. The dominance of this segment is attributed to its cost-effectiveness and ability to accommodate various product sizes. Flexible packaging is widely used in food and beverage and personal care industries due to its lightweight nature and high printability. For example, snack manufacturers are using transparent pouches with large front panels to improve product visibility. The segment is expected to maintain its dominance due to ongoing innovations in flexible packaging materials and design.

Modular packaging sizing is the fastest-growing subsegment, with a CAGR of 7.0%. This approach involves designing packaging components that can be adjusted or combined to create different sizes. The growth is driven by the need for customizable and efficient packaging solutions. For instance, electronics companies are using modular packaging to accommodate products of different sizes while maintaining consistent branding. Future developments are expected to focus on automation and standardization, enabling efficient production and distribution.

By Material

Plastic-based materials dominated the segment with a 49.6% share in 2024. These materials are widely used due to their durability, flexibility, and cost-effectiveness. Plastic packaging allows for innovative shapes and sizes, making it suitable for highly visible packaging applications. For example, beverage bottles and personal care containers often use plastic materials to achieve distinctive designs. Despite sustainability concerns, the segment continues to dominate due to its versatility and established supply chain.

Paper-based materials are the fastest-growing segment, with a CAGR of 6.8%. The growth is driven by increasing demand for sustainable packaging solutions. Paper-based packaging offers recyclability and biodegradability, making it an attractive alternative to plastic. For instance, brands are adopting paper-based cartons and boxes with optimized sizes to reduce environmental impact. Future advancements in paper technology are expected to improve strength and durability, further supporting growth.

By End-Use

The food and beverage segment accounted for the largest share of 42.9% in 2024. The dominance of this segment is driven by the need for attractive and functional packaging that enhances product visibility. Packaging sizing plays a crucial role in influencing consumer purchasing decisions in this industry. For example, beverage companies use uniquely shaped bottles and larger labels to attract attention. The growth of convenience foods and ready-to-eat products is further supporting demand.

Personal care packaging is the fastest-growing segment, with a CAGR of 6.9%. The growth is driven by increasing consumer demand for premium and aesthetically appealing products. Packaging sizing in this segment is designed to enhance brand perception and usability. For instance, cosmetic brands are using compact yet visually striking packaging to appeal to consumers. Future growth is expected to be supported by innovation and increasing demand for personalized products.

Highly Visible Packaging Sizing Market Segmentations

By Type

- Flexible Visible Packaging

- Rigid Packaging Formats

- Modular Packaging Sizing

- Others

By Material

- Plastic-Based

- Paper-Based

- Metal-Based

- Others

By End-Use

- Food & Beverage

- Personal Care

- Healthcare

- Electronics

- Others

Regional Analysis

North America

North America accounted for approximately 25.1% of the highly visible packaging sizing market share in 2025 and is expected to grow at a CAGR of 6.1% during the forecast period. The region benefits from a well-established retail sector and high adoption of advanced packaging technologies. Companies are focusing on optimizing packaging sizes to improve shelf visibility and reduce logistics costs. The growth of e-commerce and direct-to-consumer channels is further driving demand for right-sized packaging solutions. Additionally, sustainability initiatives are encouraging the use of recyclable materials and efficient packaging designs.

The United States dominates the North American market due to its large consumer base and strong retail infrastructure. A unique growth driver in this region is the adoption of data-driven packaging optimization. Companies are using analytics to determine the most effective packaging sizes for different products and retail environments. For example, major retailers are collaborating with packaging suppliers to develop standardized packaging formats that enhance shelf efficiency. This trend is expected to drive innovation and improve overall market performance.

Europe

Europe held a market share of 27.4% in 2025 and is projected to grow at a CAGR of 6.3%. The region is characterized by stringent regulations related to packaging waste and sustainability. Companies are focusing on optimizing packaging sizes to reduce material usage while maintaining visibility. The presence of advanced manufacturing capabilities and strong consumer awareness supports the adoption of innovative packaging solutions. Additionally, the growth of private label products is increasing demand for distinctive packaging designs.

Germany is the leading country in the European market, driven by its strong industrial base and focus on sustainability. A key growth driver in this region is the implementation of packaging waste directives, which require companies to minimize packaging materials. For example, retailers are encouraging suppliers to adopt compact and efficient packaging sizes. This trend is expected to drive innovation in packaging design and support market growth.

Asia Pacific

Asia Pacific dominated the market with a 38.2% share in 2025 and is expected to grow at a CAGR of 6.9%. Rapid urbanization, population growth, and expanding retail infrastructure are key factors driving the market in this region. The increasing demand for packaged goods and the growth of e-commerce are contributing to the adoption of highly visible packaging sizing solutions. Additionally, rising consumer awareness and changing lifestyles are influencing packaging preferences.

China is the dominant country in the Asia Pacific region due to its large manufacturing base and growing retail sector. A unique growth driver is the rapid expansion of online retail platforms, which require optimized packaging sizes for efficient logistics. For example, e-commerce companies are adopting standardized packaging formats to reduce shipping costs and improve efficiency. This trend is expected to drive market growth in the region.

Middle East & Africa

The Middle East & Africa region accounted for 5.9% of the market share in 2025 and is expected to grow at a CAGR of 6.0%. The region is experiencing growth in retail and hospitality sectors, which is driving demand for effective packaging solutions. Companies are focusing on improving product visibility to attract consumers in competitive markets. Additionally, increasing investments in infrastructure and urban development are supporting market growth.

The United Arab Emirates is the dominant country in this region, driven by its strong retail and tourism sectors. A key growth driver is the expansion of premium retail outlets, which require visually appealing packaging. For example, luxury products often use larger and uniquely designed packaging to enhance brand image. This trend is expected to support market growth in the region.

Latin America

Latin America held a market share of 4.9% in 2025 and is projected to grow at the fastest CAGR of 7.2%. The region is witnessing increasing demand for packaged goods due to rising urbanization and changing consumer lifestyles. The expansion of retail and e-commerce sectors is driving the adoption of optimized packaging sizes. Additionally, the availability of raw materials supports packaging production.

Brazil is the dominant country in the Latin American market, supported by its large consumer base and growing retail sector. A unique growth driver is the development of local packaging industries, which are focusing on cost-effective and efficient solutions. For example, manufacturers are adopting flexible packaging formats to improve visibility and reduce costs. This trend is expected to drive market growth in the region.

Competitive Landscape

The highly visible packaging sizing market is moderately competitive, with several global players focusing on innovation and design capabilities. A leading company in this market has established a strong presence through continuous investment in research and development, enabling the creation of advanced packaging solutions. Companies are adopting strategies such as product innovation, strategic partnerships, and expansion into emerging markets to strengthen their position.

Manufacturers are increasingly focusing on sustainability and efficiency to meet regulatory requirements and consumer expectations. Recent developments include the introduction of new packaging designs that optimize size and visibility while reducing material usage. Collaborations between packaging companies and retailers are also driving innovation. Additionally, the adoption of digital technologies is enabling companies to improve design and production processes, enhancing competitiveness.

Key Players List

- Amcor Plc

- Berry Global Inc.

- Sealed Air Corporation

- Sonoco Products Company

- Smurfit Kappa Group

- DS Smith Plc

- WestRock Company

- Huhtamaki Oyj

- Mondi Group

- International Paper Company

- UFP Technologies

- Constantia Flexibles

- Coveris Holdings

- Graphic Packaging International

- Ball Corporation