High Impact Corrugated Boxes Market Size and Growth

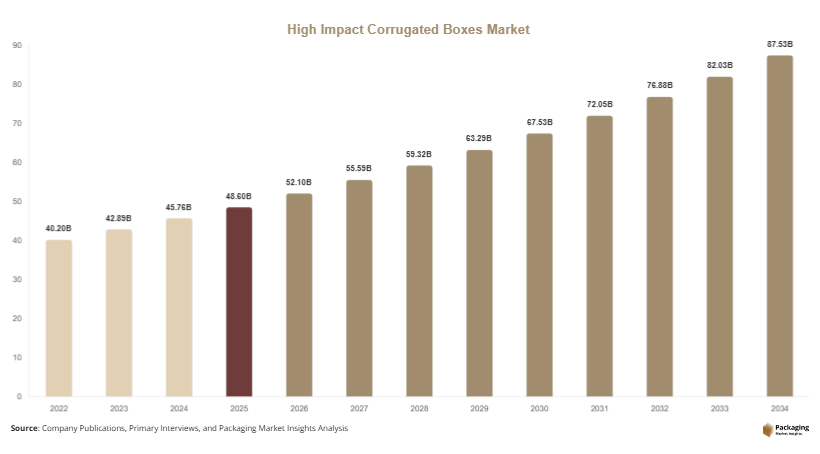

The global high impact corrugated boxes market is estimated at approximately USD 48.6 billion in 2025, increasing to around USD 52.1 billion in 2026 as demand from retail and manufacturing sectors strengthens. By 2034, the market is projected to reach nearly USD 88.4 billion, registering a CAGR of 6.7% (2025–2034). The high impact corrugated boxes market is experiencing steady expansion due to rising global demand for durable, sustainable, and cost-efficient packaging solutions across logistics, e-commerce, and industrial distribution channels. These boxes are engineered with reinforced fluting structures and high burst strength, making them suitable for transporting fragile, heavy, or high-value goods.

Growth is primarily driven by three major factors. First, the rapid expansion of e-commerce platforms has increased the need for protective secondary packaging that reduces in-transit damage. Second, sustainability regulations across Europe and Asia are encouraging the adoption of recyclable corrugated materials over plastic alternatives. Third, advancements in corrugation technology, such as double-wall and triple-wall structures, are improving load-bearing capacity and widening industrial applications.

Key Highlights

- Asia Pacific dominated the market with a 37.4% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.2%.

- Heavy-duty double-wall corrugated boxes led the type segment with a 34.2% share.

- Virgin kraft paper dominated the material segment with a 52.1% share.

- Food & beverage applications led the end-use segment with 40.9% share.

- The US remained the dominant country with a market size of USD 10.8 billion in 2025 and USD 11.6 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Shift Toward Heavy-Duty Multi-Wall Corrugated Structures

One of the most prominent trends in the high impact corrugated boxes market is the increasing adoption of multi-wall corrugated designs, particularly double-wall and triple-wall formats. These structures are engineered to provide higher stacking strength and impact resistance, making them suitable for industrial goods, automotive components, and export packaging. Manufacturers are investing in advanced flute technologies such as BC-flute combinations to enhance durability without significantly increasing weight. For example, automotive suppliers in Germany and Japan are increasingly using triple-wall corrugated boxes for engine and transmission component transport. This trend is expected to accelerate as industries prioritize damage reduction and cost-efficient logistics optimization.

Integration of Smart and Sustainable Packaging Features

Another key trend is the integration of smart packaging elements such as QR codes, RFID tracking, and moisture indicators into corrugated boxes. These enhancements improve supply chain visibility and inventory management, especially in e-commerce and pharmaceutical logistics. At the same time, sustainability is driving demand for biodegradable adhesives and water-based inks in corrugated box manufacturing. Companies in North America are increasingly adopting fully recyclable corrugated systems to meet ESG compliance goals. In the future, smart and eco-friendly corrugated packaging will become a standard requirement, particularly in cross-border trade and cold-chain applications.

Market Drivers

Expansion of Global E-Commerce and Retail Logistics

The rapid growth of e-commerce platforms is a major driver for the high impact corrugated boxes market. Online retail requires packaging that can withstand long-distance transportation, multiple handling points, and varying environmental conditions. Corrugated boxes provide cushioning, structural strength, and customization flexibility, making them ideal for this sector. For instance, large fulfillment centers in India and the United States rely heavily on corrugated packaging for daily parcel shipments. As same-day delivery and hyperlocal logistics expand, demand for high-impact corrugated solutions is expected to rise significantly.

Rising Demand from Industrial and Export-Oriented Manufacturing

Industrial manufacturing and export activities are increasingly relying on durable packaging solutions to protect heavy machinery, spare parts, and sensitive equipment. Corrugated boxes with reinforced layers help reduce damage during shipping and storage. In China and South Korea, electronics manufacturers use high-impact corrugated packaging to secure semiconductor components during global distribution. This industrial reliance on protective packaging is strengthening long-term demand and encouraging innovation in load-bearing corrugated designs.

Market Restraint

High Raw Material Price Volatility

A key restraint affecting the high impact corrugated boxes market is the fluctuation in raw material prices, particularly kraft paper and recycled fiber inputs. Since corrugated packaging is highly dependent on paper pulp availability, changes in global wood supply chains and recycling rates significantly impact production costs. For example, fluctuations in European recycled paper exports have previously caused price instability for packaging manufacturers in Asia. This volatility reduces profit margins and forces companies to adjust pricing frequently, making long-term contracts more complex for both suppliers and end users.

Market Opportunities

Growth in Circular Economy and Recycled Packaging Demand

The increasing focus on circular economy models presents a strong opportunity for corrugated box manufacturers. Governments and corporations are encouraging the use of recyclable and reusable packaging systems, particularly in Europe and North America. High-impact corrugated boxes made from recycled fibers are gaining traction in retail and logistics sectors. For example, supermarkets in the UK are transitioning toward fully recyclable packaging formats to reduce landfill waste. This shift is expected to create long-term opportunities for sustainable packaging innovation.

Expansion in Emerging Markets and Industrial Zones

Emerging economies in Southeast Asia, Africa, and Latin America offer significant growth potential due to expanding manufacturing hubs and export-oriented industries. Countries like Vietnam and Brazil are investing in industrial corridors that require strong packaging infrastructure. High-impact corrugated boxes are increasingly used for agricultural exports, electronics, and automotive components in these regions. As industrialization continues, demand for cost-effective and durable packaging solutions will increase steadily.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 48.6 Billion |

| Market Size in 2026 | USD 52.1 Billion |

| Market Size in 2034 | USD 88.4 Billion |

| CAGR | 6.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Heavy-duty double-wall corrugated boxes dominated the market in 2024 with approximately 34.2% share, driven by their widespread use in e-commerce and industrial shipping. These boxes provide a balance of strength and cost efficiency, making them suitable for electronics, FMCG, and automotive parts packaging. Companies such as global logistics providers rely heavily on double-wall formats for warehouse-to-consumer delivery systems.

The fastest-growing segment is triple-wall corrugated boxes, expected to grow at a CAGR of 6.9%. Their superior load-bearing capacity makes them ideal for heavy machinery and export goods. Increasing demand from aerospace and defense logistics is further supporting adoption, with future growth expected in high-risk shipment categories.

By Material

Virgin kraft paper dominated the material segment in 2024 with a 52.1% share, due to its high strength and consistency in fiber structure. It is widely used in premium packaging applications where durability is critical.

Recycled fiber-based materials are the fastest-growing segment, projected at a CAGR of 6.4%, driven by sustainability regulations and corporate ESG commitments. Packaging companies are increasingly investing in closed-loop recycling systems.

By End-Use

Food & beverage dominated with a 40.9% share in 2024, supported by strong demand for packaged goods and cold-chain logistics. Corrugated boxes ensure product freshness and protection during transportation.

E-commerce logistics is the fastest-growing segment at a CAGR of 7.1%, driven by rising online shopping and same-day delivery models. Packaging customization is also increasing in this segment.

High Impact Corrugated Boxes Market Segmentations

By Type

- Single-Wall Corrugated Boxes

- Double-Wall Corrugated Boxes

- Triple-Wall Corrugated Boxes

- Heavy-Duty Reinforced Corrugated Boxes

By Material

- Virgin Kraft Paper

- Recycled Fiber-Based Paper

- Bleached Corrugated Board

- Coated Corrugated Materials

By End-User

- Food & Beverage

- E-commerce & Logistics

- Electronics & Electricals

- Automotive & Industrial Goods

- Healthcare & Pharmaceuticals

Regional Analysis

North America

North America accounted for approximately 23.5% market share in 2025, with steady growth projected at a CAGR of 5.9% (2025–2034). The region benefits from a well-established logistics network, advanced retail infrastructure, and strong demand from e-commerce giants. Increasing emphasis on sustainable packaging and regulatory pressure to reduce plastic waste is further driving corrugated box adoption across the United States and Canada.

The United States is the dominant country in this region, driven by large-scale distribution centers and high parcel shipment volumes. A key growth driver is the rapid expansion of subscription-based retail models and direct-to-consumer shipping. For example, major fulfillment centers in Texas and California increasingly rely on reinforced corrugated boxes to reduce damage during automated sorting processes.

Europe

Europe held around 21.8% market share in 2025, growing at a CAGR of 5.7% due to strict environmental regulations and strong recycling infrastructure. The region’s packaging industry is highly influenced by sustainability mandates and circular economy policies.

Germany leads the European market, driven by its strong manufacturing base and automotive exports. A unique growth driver is the adoption of eco-design packaging standards across industrial supply chains. Automotive exporters increasingly use multi-layer corrugated boxes for engine components shipped across EU borders.

Asia Pacific

Asia Pacific dominated the market with a 37.4% share in 2025, expanding at a CAGR of 7.4%, making it the fastest-growing regional segment. Rapid industrialization, booming e-commerce, and export-led manufacturing are key contributors.

China remains the dominant country, supported by large-scale electronics and consumer goods exports. A major growth driver is the expansion of cross-border e-commerce platforms such as regional logistics hubs in Shenzhen and Shanghai, where corrugated packaging demand is rising sharply.

Middle East & Africa

The region accounted for 8.6% market share in 2025, with a CAGR of 6.1% driven by growing retail infrastructure and logistics diversification. Increasing trade activities in Gulf countries are expanding packaging demand.

Saudi Arabia leads the region, supported by its industrial diversification strategy under Vision 2030. A key driver is rising demand for packaged food imports and construction material logistics requiring durable corrugated solutions.

Latin America

Latin America held 8.7% market share in 2025, with the fastest projected growth at a CAGR of 6.2%. Expansion of agribusiness exports and retail modernization is fueling demand.

Brazil is the dominant country, driven by large agricultural export volumes. A unique driver is the use of high-impact corrugated boxes for fruit and meat exports to Europe and Asia, ensuring durability during long-distance transport.

Competitive Landscape

The market is moderately consolidated with key players focusing on capacity expansion, sustainability, and digital printing technologies. Leading companies include International Paper, WestRock, Smurfit Kappa, DS Smith, Mondi Group, and Packaging Corporation of America. Among these, Smurfit Kappa holds a leading position due to its integrated recycling and packaging ecosystem. Companies are investing in lightweight high-strength materials, automation in box manufacturing, and eco-friendly coatings to enhance competitiveness.

Key Players List

- International Paper

- WestRock

- Smurfit Kappa

- DS Smith

- Mondi Group

- Packaging Corporation of America

- Georgia-Pacific

- Oji Holdings

- Nine Dragons Paper

- WestRock India Packaging

- Rengo Co. Ltd.

- Sappi Limited

- Cascades Inc.

- Visy Industries

- Pratt Industries