Heavy Duty Corrugated Packaging Market Size and Growth

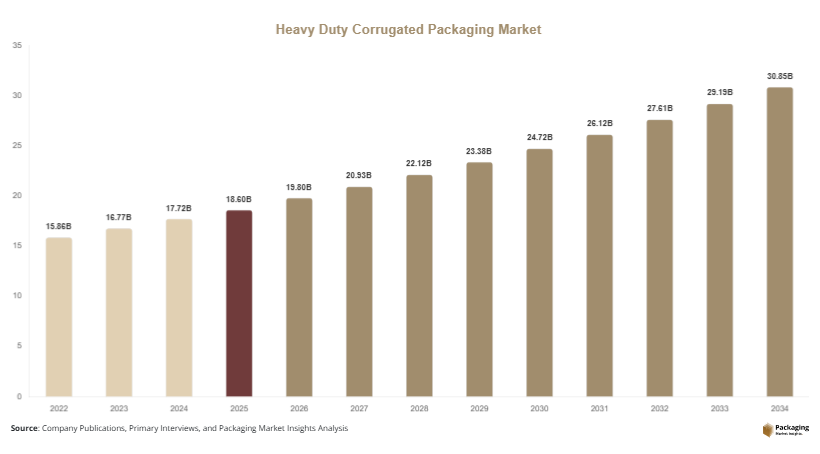

The global heavy duty corrugated packaging market size is estimated at USD 18.6 billion in 2025, which is projected to reach approximately USD 19.8 billion in 2026. Over the forecast period from 2025 to 2034, the market is expected to grow at a CAGR of 5.7%, reaching nearly USD 32.5 billion by 2034. This growth trajectory reflects rising reliance on durable, cost-efficient, and sustainable packaging solutions across heavy industries such as automotive, chemicals, and electronics. The heavy duty corrugated packaging market is witnessing steady expansion due to increasing demand from industrial logistics, e-commerce fulfillment, and bulk transportation sectors.

Heavy-duty corrugated packaging is specifically designed to handle high-load capacities, often replacing traditional wooden crates and plastic containers. The shift is driven by cost efficiency, recyclability, and ease of customization. Additionally, the rapid globalization of supply chains is increasing the need for packaging that can withstand long transit durations, variable environmental conditions, and mechanical stress.

Key Market Insights:

- Asia Pacific dominated the market with a 38.2% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 6.4%.

- Double-wall corrugated boxes led the type segment with a 34.7% share.

- Recycled paper material dominated with a 57.1% share.

- Industrial machinery applications led the segment with 41.5% share.

- China remained the dominant country with a market size of USD 4.2 billion in 2025 and USD 4.5 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable Packaging Materials

Sustainability is becoming a central trend in the heavy duty corrugated packaging market as industries aim to reduce environmental impact. Corrugated packaging, being recyclable and biodegradable, is increasingly preferred over plastic and wooden alternatives. Companies are investing in closed-loop recycling systems and sourcing certified paper materials to meet environmental regulations. For example, large manufacturing firms are shifting to recycled fiber-based packaging for exporting machinery components. This transition reduces carbon emissions and waste generation while maintaining structural integrity.

In the future, sustainability will drive innovation in lightweight yet durable packaging formats. Advanced fiber engineering and water-resistant coatings will further enhance performance. Governments in Europe and North America are also introducing stricter regulations, which will accelerate adoption. As a result, sustainable heavy-duty corrugated solutions are expected to become the industry standard.

Integration of Smart and Custom Packaging Solutions

Another significant trend is the integration of smart features and customization in heavy-duty corrugated packaging. Companies are increasingly incorporating tracking technologies such as RFID tags and QR codes into packaging to improve supply chain visibility. This is particularly useful in high-value shipments like automotive parts and industrial equipment. Additionally, manufacturers are offering tailored packaging designs to meet specific load requirements and product dimensions.

For instance, electronics exporters are using customized corrugated crates with shock-absorbing features to reduce transit damage. This trend is expected to grow as industries demand higher efficiency and reduced losses. In the long term, smart packaging will enable real-time monitoring of shipments, enhancing logistics efficiency and customer satisfaction.

Market Drivers

Expansion of Global Industrial and Manufacturing Activities

The growth of industrial production across regions is a major driver of the heavy duty corrugated packaging market. As manufacturing output increases, the need for reliable packaging to transport heavy goods also rises. Industries such as automotive, construction, and chemicals rely heavily on durable packaging solutions. Corrugated packaging provides strength, flexibility, and cost efficiency, making it suitable for bulk shipments.

For example, automotive manufacturers use heavy-duty corrugated boxes to ship engine parts and components across continents. This reduces reliance on wooden crates and lowers transportation costs. As industrialization continues in emerging markets, demand for such packaging solutions will expand further.

Growth of E-commerce and Logistics Infrastructure

The rapid expansion of e-commerce and logistics networks is another key driver. While heavy-duty packaging is traditionally associated with industrial use, it is increasingly being adopted in large-scale e-commerce operations, especially for bulky goods. Warehousing automation and the need for efficient storage are encouraging the use of standardized corrugated packaging formats.

For instance, large online retailers are using reinforced corrugated boxes for appliances and furniture shipments. This ensures product safety while optimizing storage space. As logistics infrastructure improves globally, the demand for durable and scalable packaging solutions will continue to grow.

Market Restraint

Restraint: Fluctuations in Raw Material Prices

One of the primary challenges in the heavy duty corrugated packaging market is the volatility in raw material prices, particularly paper pulp. The cost of recycled and virgin paper is influenced by supply chain disruptions, environmental regulations, and energy costs. These fluctuations directly impact manufacturing expenses and profit margins for packaging companies.

For example, during periods of high demand for paper products, the cost of raw materials increases significantly, forcing manufacturers to raise prices. This can lead to reduced adoption among cost-sensitive industries. Additionally, supply shortages can disrupt production schedules, affecting overall market growth. Addressing this challenge requires improved supply chain management and investment in alternative materials.

Market Opportunities

Growth in Renewable Energy Sector

The renewable energy sector presents significant opportunities for the heavy duty corrugated packaging market. Equipment such as solar panels, wind turbine components, and batteries require robust packaging solutions for safe transportation. Corrugated packaging offers a lightweight yet strong alternative to traditional materials, making it ideal for this sector.

As investments in renewable energy projects increase globally, the demand for heavy-duty packaging will rise. Companies can develop specialized packaging solutions tailored to these applications, creating new revenue streams.

Expansion in Emerging Markets

Emerging economies offer substantial growth opportunities due to rapid industrialization and infrastructure development. Countries in Asia, Africa, and Latin America are witnessing increased manufacturing activities, leading to higher demand for packaging solutions.

For instance, the expansion of automotive and electronics manufacturing in Southeast Asia is driving the need for durable packaging. Companies entering these markets can benefit from lower production costs and growing demand. In the future, localized manufacturing and supply chains will further boost market growth.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 18.6 Billion |

| Market Size in 2026 | USD 19.8 Billion |

| Market Size in 2034 | USD 32.5 Billion |

| CAGR | 5.7% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Double-wall corrugated boxes dominated the market in 2024 with a 34.7% share. Their widespread adoption is attributed to their balance between strength and cost efficiency. These boxes are commonly used in industries such as automotive and electronics, where moderate to heavy loads need to be transported safely. For example, automotive suppliers use double-wall boxes to ship engine components and spare parts. The structural integrity of these boxes ensures protection against mechanical stress during transit. Additionally, their compatibility with automated packaging systems enhances operational efficiency.

Triple-wall corrugated packaging is the fastest-growing segment, with a projected CAGR of 6.2%. This growth is driven by increasing demand for high-strength packaging solutions capable of replacing wooden crates. Industries such as heavy machinery and construction are adopting triple-wall packaging for transporting large equipment. Future developments in material engineering are expected to further enhance the load-bearing capacity of these boxes, making them suitable for a wider range of applications.

By Material

Recycled paper dominated the market with a 57.1% share in 2024, driven by sustainability trends and cost advantages. Companies are increasingly using recycled materials to reduce environmental impact and comply with regulations. For instance, manufacturers in Europe are adopting recycled fiber-based packaging to meet circular economy goals. The availability of recycling infrastructure also supports the widespread use of this material. Additionally, recycled paper offers sufficient strength for most industrial applications, making it a preferred choice.

Virgin kraft paper is the fastest-growing material segment, with a CAGR of 5.8%. This growth is driven by the need for higher strength and durability in demanding applications. Industries such as chemicals and heavy machinery require packaging that can withstand extreme conditions. Virgin kraft paper provides superior performance, making it suitable for these applications. In the future, innovations in sustainable sourcing and production processes are expected to enhance its adoption.

By End-Use

Industrial machinery accounted for the largest share of 41.5% in 2024, driven by the need for durable packaging solutions for heavy equipment. This segment includes packaging for construction machinery, industrial tools, and large components. For example, manufacturers use heavy-duty corrugated boxes to transport machinery parts across long distances. The ability to customize packaging designs to fit specific products further supports its dominance.

Electronics is the fastest-growing end-use segment, with a CAGR of 6.6%. The increasing production and export of electronic devices are driving demand for protective packaging solutions. Corrugated packaging provides cushioning and structural support, reducing the risk of damage during transit. As the electronics industry continues to expand, the demand for advanced packaging solutions is expected to grow significantly.

Heavy Duty Corrugated Packaging Market Segmentations

By Type

- Single Wall Corrugated Packaging

- Double Wall Corrugated Packaging

- Triple Wall Corrugated Packaging

By Material

- Recycled Paper

- Virgin Kraft Paper

By End-User

- Industrial Machinery

- Automotive

- Electronics

- Chemicals

Regional Analysis

North America

North America accounted for approximately 24.6% of the global market share in 2025 and is projected to grow at a CAGR of 5.1% through 2034. The region benefits from a well-established industrial base and advanced logistics infrastructure. The presence of large-scale manufacturing industries, particularly in the United States, supports consistent demand for heavy-duty corrugated packaging. Additionally, the adoption of automation in warehousing and distribution centers is increasing the need for standardized and durable packaging formats. Sustainability initiatives and recycling programs are also contributing to market growth, as companies aim to reduce environmental impact.

The United States dominates the regional market due to its strong manufacturing output and export activities. A key growth driver in the country is the increasing demand for packaging solutions in the aerospace and defense sectors. For example, the transportation of aircraft components requires high-strength packaging that can withstand long transit durations. The shift toward sustainable packaging materials is also gaining momentum, with companies investing in recycled fiber-based solutions. This trend is expected to drive steady growth in the region.

Europe

Europe held a 21.3% market share in 2025 and is expected to grow at a CAGR of 4.9% during the forecast period. The region’s focus on environmental sustainability and stringent regulations on packaging waste are key factors influencing market dynamics. Countries such as Germany, France, and the United Kingdom are leading the adoption of eco-friendly packaging solutions. The automotive and industrial machinery sectors are major consumers of heavy-duty corrugated packaging in Europe.

Germany is the dominant country in the region, driven by its strong manufacturing and export-oriented economy. A unique growth driver is the emphasis on circular economy practices, which encourage the use of recyclable materials. For example, German manufacturers are increasingly replacing wooden crates with corrugated packaging to meet sustainability targets. The region also benefits from advanced recycling infrastructure, which supports the widespread adoption of corrugated materials.

Asia Pacific

Asia Pacific emerged as the largest regional market with a 38.2% share in 2025 and is projected to grow at a CAGR of 6.1%. Rapid industrialization, expanding manufacturing sectors, and increasing exports are key factors driving growth in the region. Countries such as China, India, and Japan are major contributors to market expansion. The growing demand for consumer electronics and automotive components is also boosting the need for heavy-duty packaging solutions.

China dominates the Asia Pacific market due to its large manufacturing base and export activities. A significant growth driver is the expansion of e-commerce logistics and cross-border trade. For instance, Chinese manufacturers are using reinforced corrugated packaging for exporting heavy machinery and electronics. Government initiatives to promote sustainable packaging are also supporting market growth. The region is expected to remain the largest market throughout the forecast period.

Middle East & Africa

The Middle East & Africa region accounted for 8.7% of the market share in 2025 and is expected to grow at a CAGR of 5.5%. The region’s growth is driven by increasing industrial activities and infrastructure development. Countries such as the UAE and South Africa are investing in logistics and manufacturing sectors, which is boosting demand for packaging solutions. The oil and gas industry also contributes to market growth by requiring durable packaging for equipment transportation.

Saudi Arabia is a key market in the region, supported by its industrial diversification initiatives. A unique growth driver is the development of large-scale infrastructure projects, which require the transportation of heavy machinery. For example, construction companies are adopting corrugated packaging for equipment components to reduce costs and improve handling efficiency. The region is expected to witness steady growth due to ongoing industrialization.

Latin America

Latin America held a 7.2% market share in 2025 and is projected to grow at the fastest CAGR of 6.4%. The region is experiencing growth due to expanding manufacturing activities and increasing trade. Countries such as Brazil and Mexico are key contributors to market expansion. The rising demand for packaging in the automotive and food processing industries is also driving growth.

Brazil dominates the regional market, supported by its large industrial base. A key growth driver is the expansion of export-oriented industries, which require durable packaging solutions. For instance, Brazilian manufacturers are using heavy-duty corrugated packaging for exporting agricultural machinery. The region’s growing focus on sustainability is also encouraging the adoption of recyclable materials, which will support long-term market growth.

Competitive Landscape

The heavy duty corrugated packaging market is moderately fragmented, with several global and regional players competing on innovation, pricing, and sustainability. Leading companies are focusing on product development, strategic partnerships, and capacity expansion to strengthen their market position.

International Paper Company is identified as the market leader due to its extensive product portfolio and global presence. The company has been investing in sustainable packaging solutions and expanding its manufacturing capabilities. Other key players are also adopting similar strategies, including mergers and acquisitions to enhance their market reach.

Companies are increasingly investing in research and development to create high-performance packaging solutions. For example, advancements in multi-layer corrugated structures are improving strength while reducing material usage. Additionally, digital printing technologies are enabling customization and branding opportunities. These strategies are expected to intensify competition in the market.

Key Players

- International Paper Company

- WestRock Company

- Smurfit Kappa Group

- DS Smith Plc

- Packaging Corporation of America

- Mondi Group

- Stora Enso

- Georgia-Pacific LLC

- Oji Holdings Corporation

- Nine Dragons Paper Holdings

- Rengo Co., Ltd.

- Cascades Inc.

- Klabin S.A.

- SCG Packaging

- Pratt Industries