Food Packaging Films Market Size and Growth

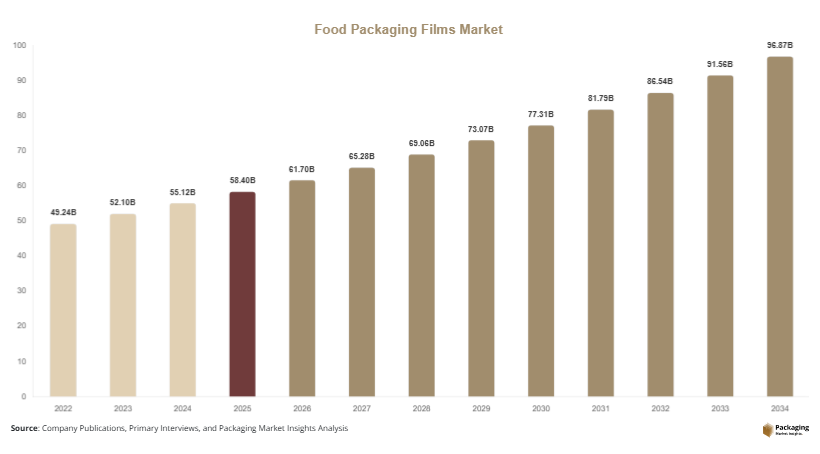

The global food packaging films market size was valued at approximately USD 58.4 billion in 2025 and is projected to reach USD 61.7 billion in 2026. Over the forecast period from 2025 to 2034, the market is expected to grow at a CAGR of 5.8%, reaching an estimated USD 102.6 billion by 2034. This growth reflects the increasing reliance on flexible packaging solutions that offer convenience, durability, and extended shelf life. The food packaging films market is experiencing steady expansion due to rising demand for packaged food products, evolving consumer preferences, and advancements in packaging technologies.

One of the primary growth factors is the rising consumption of ready-to-eat and convenience foods, particularly in urban areas where busy lifestyles drive demand for packaged products. In addition, the expansion of e-commerce and food delivery services is increasing the need for durable and lightweight packaging films that ensure product safety during transportation. Another key factor is the growing focus on food safety and hygiene, which is encouraging manufacturers to adopt advanced packaging materials that protect against contamination and spoilage.

Key Highlights:

- Asia Pacific dominated the market with a 38.2% share in 2025, while Latin America is projected to grow at the fastest CAGR of 6.3%.

- Polyethylene films led the type segment with a 34.5% share, while biodegradable films are expected to grow at a CAGR of 6.7%.

- Flexible plastic packaging dominated with a 55.8% share, while paper-based films are forecasted to grow at a CAGR of 5.9%.

- Food applications led the segment with 72.4% share, while dairy packaging is expected to grow at a CAGR of 6.1%.

- China remained the dominant country with a market size of USD 13.1 billion in 2025 and USD 13.9 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing adoption of sustainable and biodegradable packaging films

The market is witnessing a shift toward sustainable packaging solutions as environmental concerns and regulatory requirements continue to rise. Consumers are becoming more aware of the environmental impact of plastic waste, leading to increased demand for biodegradable and recyclable packaging films. Manufacturers are responding by developing innovative materials derived from renewable resources, such as plant-based polymers and compostable films.

This trend is further supported by government regulations aimed at reducing single-use plastics and promoting sustainable practices. Companies are investing in research to improve the performance of biodegradable films, ensuring they meet the durability and barrier requirements of food packaging. Retailers and food brands are also adopting eco-friendly packaging to enhance their brand image and meet consumer expectations. As sustainability becomes a key purchasing factor, the adoption of environmentally friendly packaging films is expected to accelerate.

Growing demand for high-barrier and multi-layer film technologies

The demand for high-barrier and multi-layer films is increasing due to the need for extended shelf life and improved food protection. These films are designed to prevent moisture, oxygen, and light from affecting the quality of food products, making them essential for packaging perishable items. Multi-layer films combine different materials to achieve enhanced performance, offering flexibility, strength, and barrier properties.

This trend is particularly significant in the packaging of processed and ready-to-eat foods, where maintaining freshness and quality is critical. Advances in film technology are enabling manufacturers to create thinner yet more effective packaging solutions, reducing material usage while maintaining performance. The adoption of high-barrier films is also supported by the growth of global food trade, which requires packaging solutions that can withstand long transportation times and varying environmental conditions.

Market Drivers

Rising consumption of packaged and convenience foods

The increasing demand for packaged and convenience foods is a major factor driving the food packaging films market. Urbanization and changing lifestyles have led to a shift in consumer behavior, with a growing preference for ready-to-eat and easy-to-prepare food products. Packaging films play a crucial role in preserving the quality and safety of these products, making them an essential component of the food supply chain.

Food manufacturers are expanding their product portfolios to cater to diverse consumer preferences, which is increasing the demand for flexible packaging solutions. The growth of supermarkets, hypermarkets, and online grocery platforms is further supporting this trend. Additionally, advancements in packaging design are enhancing product appeal, encouraging consumers to choose packaged foods. This growing demand is expected to drive continuous market expansion.

Expansion of e-commerce and food delivery services

The rapid growth of e-commerce and food delivery services is significantly influencing the demand for food packaging films. These platforms require packaging solutions that can protect food products during transportation while maintaining freshness and quality. Flexible packaging films are widely used due to their lightweight nature, durability, and cost-effectiveness.

The increasing use of digital platforms for food ordering is creating new opportunities for packaging manufacturers. Companies are developing innovative packaging solutions that meet the specific requirements of online delivery, such as leak-proof and temperature-resistant films. The rise of cloud kitchens and quick-service restaurants is also contributing to demand. This trend is expected to continue as consumers increasingly rely on convenient food delivery options.

Market Restraint

Environmental concerns and regulatory pressure on plastic usage

Environmental concerns related to plastic waste are a significant restraint for the food packaging films market. Traditional plastic films are often non-biodegradable, contributing to environmental pollution and waste management challenges. Governments and regulatory bodies are implementing strict regulations to limit the use of single-use plastics, which is impacting market growth.

Manufacturers are required to invest in sustainable alternatives, which can increase production costs and affect profit margins. For example, transitioning to biodegradable materials often involves higher raw material costs and complex manufacturing processes. Additionally, recycling infrastructure for flexible packaging films is still underdeveloped in many regions, limiting the effectiveness of sustainability initiatives. These challenges are creating barriers for market expansion and requiring companies to adapt their strategies to meet regulatory requirements.

Market Opportunities

Innovation in recyclable and mono-material packaging solutions

The development of recyclable and mono-material packaging films presents significant growth opportunities for the market. Mono-material films are designed to be easily recyclable, addressing one of the key challenges associated with multi-layer packaging. These solutions are gaining popularity as they align with sustainability goals and regulatory requirements.

Manufacturers are investing in research to develop materials that offer the same performance as traditional multi-layer films while being fully recyclable. This innovation is expected to attract food manufacturers seeking sustainable packaging options. The adoption of recyclable films is also supported by increasing consumer awareness and demand for environmentally responsible products. This trend is likely to drive long-term growth in the market.

Growth in emerging markets and changing consumption patterns

Emerging markets offer substantial opportunities for the food packaging films market due to rising incomes and changing consumption patterns. As urbanization increases, consumers in these regions are adopting modern lifestyles, leading to higher demand for packaged food products. The expansion of retail infrastructure, including supermarkets and convenience stores, is further supporting market growth.

Local manufacturers are expanding their production capacities to meet rising demand, while global players are entering these markets to capitalize on growth opportunities. Additionally, government initiatives to improve food safety and packaging standards are encouraging the adoption of advanced packaging solutions. This combination of factors is expected to create favorable conditions for market expansion in emerging economies.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 58.4 Billion |

| Market Size in 2026 | USD 61.7 Billion |

| Market Size in 2034 | USD 102.6 Billion |

| CAGR | 5.8% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

Polyethylene films dominated the market in 2024, accounting for approximately 34.5% of the total share. These films are widely used due to their flexibility, durability, and cost-effectiveness. Polyethylene films provide excellent moisture resistance, making them suitable for packaging a wide range of food products. Their ease of processing and compatibility with various packaging formats further support their widespread adoption.

Biodegradable films are expected to grow at the fastest CAGR of 6.7% during the forecast period. The increasing focus on sustainability is driving demand for these eco-friendly alternatives. Manufacturers are developing biodegradable films that offer similar performance to traditional plastics, enabling their use in various applications. This trend is expected to gain momentum as regulatory pressure increases.

By Application

Food applications dominated the market in 2024, holding a share of approximately 72.4%. Packaging films are widely used in the food industry to preserve freshness and extend shelf life. The growing demand for packaged food products is driving the adoption of advanced packaging solutions.

Dairy packaging is expected to grow at the fastest CAGR of 6.1% during the forecast period. The increasing consumption of dairy products and the need for effective packaging solutions are key factors driving this segment. Advanced films that provide barrier protection are supporting the growth of dairy packaging applications.

By End-Use

Food processing companies accounted for the largest share of the market in 2024, representing approximately 49.7% of total revenue. These companies rely heavily on packaging films to ensure product safety and quality. The expansion of the food processing industry is driving demand for packaging solutions.

Retail and e-commerce are expected to grow at the fastest CAGR of 6.4% during the forecast period. The increasing use of online platforms for food purchasing is driving demand for packaging films that can withstand transportation and handling. This trend is expected to continue as e-commerce expands.

Food Packaging Films Market Segmentations

By Type

- Polyethylene Films

- Polypropylene Films

- Polyester Films

- Biodegradable Films

By Application

- Food Packaging

- Dairy Products

- Meat & Poultry

- Bakery & Confectionery

By End-User

- Food Processing Companies

- Retail

- E-commerce

Regional Analysis

North America

North America accounted for approximately 27.6% of the global food packaging films market share in 2025 and is projected to grow at a CAGR of 5.4% during the forecast period. The region benefits from a well-established food processing industry and high consumer demand for packaged products. Advanced packaging technologies and strong distribution networks further support market growth.

The United States dominates the regional market due to its large food industry and high consumption of convenience foods. A unique growth factor is the increasing adoption of sustainable packaging solutions driven by consumer awareness and regulatory initiatives. Companies in the region are focusing on developing recyclable and biodegradable films to meet environmental standards.

Europe

Europe held a market share of around 24.3% in 2025 and is expected to grow at a CAGR of 5.2% over the forecast period. The region is characterized by strict environmental regulations and a strong focus on sustainability. The demand for eco-friendly packaging solutions is driving innovation in the market.

Germany leads the European market due to its advanced manufacturing capabilities and strong food processing sector. A key growth factor is the increasing adoption of circular economy practices, which encourage recycling and reuse of packaging materials. This trend is influencing product development and market dynamics.

Asia Pacific

Asia Pacific dominated the market with a share of 38.2% in 2025 and is expected to grow at a CAGR of 6.2% during the forecast period. Rapid urbanization, increasing disposable incomes, and changing dietary habits are driving demand for packaged food products in the region.

China is the dominant country in Asia Pacific, supported by its large population and expanding retail sector. A unique growth factor is the rapid growth of e-commerce platforms, which is increasing demand for durable and efficient packaging solutions. This trend is supporting the adoption of advanced packaging films.

Middle East & Africa

The Middle East & Africa region accounted for approximately 5.1% of the market share in 2025 and is expected to grow at a CAGR of 5.6% during the forecast period. The region is experiencing gradual growth due to improving economic conditions and increasing demand for packaged food products.

Saudi Arabia is a key market in the region, driven by its growing food processing industry. A notable growth factor is the expansion of retail infrastructure, including supermarkets and hypermarkets, which is increasing the demand for packaged food products and related packaging solutions.

Latin America

Latin America held a market share of around 4.8% in 2025 and is projected to grow at the fastest CAGR of 6.3% during the forecast period. The region is benefiting from increasing urbanization and rising consumer demand for convenience foods.

Brazil dominates the regional market due to its large population and expanding food industry. A unique growth factor is the increasing investment in food processing and packaging technologies, which is enhancing product quality and supporting market growth.

Competitive Landscape

The food packaging films market is moderately competitive, with several global and regional players focusing on innovation and sustainability. Companies are investing in research and development to create advanced packaging solutions that meet evolving consumer and regulatory requirements. Strategic partnerships and mergers are common as companies seek to expand their market presence.

Amcor plc is a leading player in the market, known for its extensive portfolio of packaging solutions. The company recently introduced recyclable packaging films aimed at reducing environmental impact. Other major players are also focusing on developing sustainable products and expanding their production capacities to meet growing demand.

Key Players List

- Amcor plc

- Berry Global Inc.

- Sealed Air Corporation

- Mondi Group

- Huhtamaki Oyj

- Coveris Holdings S.A.

- Constantia Flexibles

- Uflex Ltd.

- Toray Industries Inc.

- Mitsubishi Chemical Group

- DuPont de Nemours Inc.

- Winpak Ltd.

- Bemis Company Inc.

- Clondalkin Group

- Cosmo Films Ltd.