Food Cans Market Size and Growth

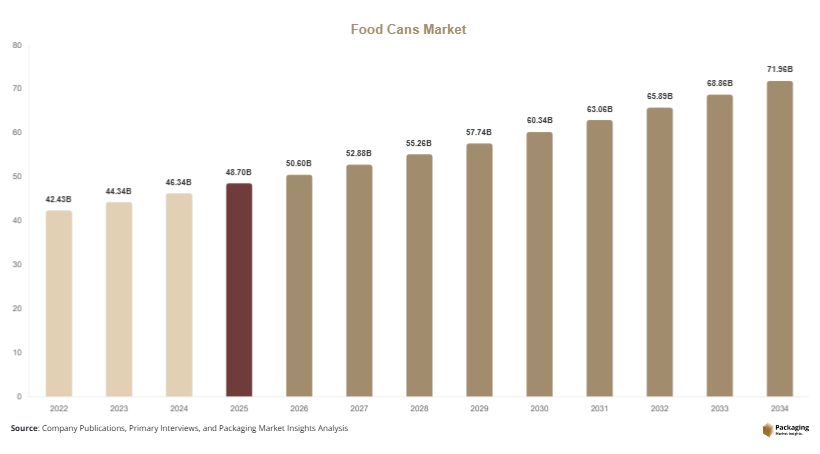

The global food cans market was valued at USD 48.7 billion in 2025 and is projected to reach USD 72.4 billion by 2034, expanding at a CAGR of 4.5% during the forecast period from 2025 to 2034. The market reached an estimated value of USD 50.6 billion in 2026, supported by increasing demand for shelf-stable food products, rising urbanization, and expanding retail distribution networks worldwide. Food cans remain one of the most widely used packaging formats across processed vegetables, seafood, pet food, ready meals, soups, sauces, fruits, and meat products due to their long shelf life, durability, and strong barrier protection against moisture, oxygen, and contaminants.

The growing consumption of convenience foods is one of the major growth factors supporting market expansion. Changing consumer lifestyles, rising working populations, and increasing preference for ready-to-eat products are driving demand for canned food packaging globally. Manufacturers are focusing on lightweight can structures, BPA-free coatings, and easy-open lid technologies to improve product appeal and operational efficiency. Food can packaging also provides excellent transportation stability, making it highly suitable for global food trade and long-distance logistics operations.

Key Market Highlights

- Asia Pacific dominated the market with a 36.9% share in 2025.

- Latin America is projected to grow at the fastest CAGR of 5.8%.

- Aluminum food cans led the type segment with a 33.7% share.

- Metal packaging dominated the material segment with a 71.2% share.

- Processed food applications led the end-use segment with 44.8% share.

- The US remained the dominant country with a market size of USD 9.4 billion in 2025 and USD 9.8 billion in 2026.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Increasing Adoption of Sustainable Metal Packaging

Sustainability initiatives are significantly influencing the food cans market as manufacturers increase the use of recyclable aluminum and steel packaging materials. Food brands are focusing on reducing packaging waste and improving recycled material usage to meet environmental goals and regulatory standards. Metal food cans provide long shelf life and can be recycled multiple times without major quality loss, making them attractive for sustainable packaging strategies. Several global food companies are increasing recycled aluminum content in canned vegetables, soups, and beverage products to strengthen sustainability performance.

This trend is expected to accelerate further as governments expand recycling regulations and consumers demand environmentally responsible packaging. Investments in lightweight can manufacturing and energy-efficient recycling systems are helping reduce operational costs and carbon emissions. Advanced coating technologies are also improving food safety and corrosion resistance while supporting recyclability. Over the forecast period, sustainable packaging innovation is expected to remain a major competitive factor within the global food cans market.

Growth of Smart and Convenient Packaging Features

The market is witnessing growing adoption of easy-open lids, resealable packaging systems, QR-enabled labels, and digital printing technologies. Consumers increasingly prefer packaging formats that improve convenience, portability, and product accessibility. Food manufacturers are integrating pull-tab lids and microwave-compatible cans to support demand for ready-to-eat and on-the-go meal products. Smart labeling solutions are also helping brands improve consumer engagement, product traceability, and inventory management capabilities.

The future impact of this trend is expected to be substantial as retail digitization and e-commerce grocery sales continue expanding globally. Smart packaging technologies can improve supply chain transparency and reduce food waste through better tracking systems. Companies investing in digital printing and connected packaging are likely to strengthen brand visibility and customer interaction. Demand for premium canned food packaging with enhanced convenience features is expected to increase steadily across both developed and emerging markets.

Market Drivers

Rising Demand for Processed and Ready-to-Eat Foods

The increasing global consumption of processed and ready-to-eat food products is one of the primary drivers supporting growth in the food cans market. Urban lifestyles, longer working hours, and rising dual-income households are encouraging consumers to purchase convenient packaged meals with extended shelf life. Food cans provide excellent product protection, preserve nutritional value, and support large-scale food storage and transportation. Manufacturers of soups, seafood, meat products, fruits, and vegetables continue expanding canned food production to meet rising consumer demand.

Retail expansion and online grocery platforms are also contributing to higher packaged food sales. For example, canned pet food and ready meal categories are witnessing strong demand growth across North America and Asia Pacific. Food can manufacturers are increasing production capacity and introducing lightweight designs to improve supply chain efficiency. The growing popularity of emergency food storage products and shelf-stable packaged foods is expected to further support long-term market expansion.

Expansion of Global Food Export and Retail Industries

The growth of international food trade and organized retail networks is driving demand for durable and transport-efficient food packaging solutions. Food cans offer strong resistance to contamination, leakage, and product spoilage during long-distance transportation, making them highly suitable for export operations. Emerging economies are witnessing rapid supermarket expansion and increased packaged food consumption, creating higher demand for canned products across urban markets.

Several food processing companies are investing in advanced canning technologies and automated filling systems to improve production output and packaging quality. The expansion of modern retail chains in countries such as India, Brazil, Indonesia, and Mexico is strengthening packaged food distribution networks. Rising demand for packaged seafood, fruits, and canned vegetables in export markets is expected to support continued growth in food can packaging production during the forecast period.

Market Restraint

Fluctuating Metal Raw Material Prices

Fluctuating prices of aluminum and steel remain a major restraint for the food cans market. Metal packaging production depends heavily on raw material availability and global commodity pricing trends. Rising energy costs, mining disruptions, trade restrictions, and supply chain volatility can significantly affect manufacturing expenses and profit margins for food can producers. Small and medium-sized manufacturers are particularly vulnerable to raw material price instability, which can reduce competitiveness.

In addition, alternative packaging solutions such as flexible pouches and rigid plastic containers are creating pricing pressure in some product categories. Certain food brands are shifting toward lightweight flexible packaging formats to reduce packaging and logistics costs. For example, ready meal manufacturers in several regions are increasing adoption of microwaveable trays and flexible pouches for convenience-oriented products. These competitive pressures may limit market expansion in low-margin food segments. However, ongoing investments in recycled metal sourcing and lightweight can production technologies are expected to partially offset raw material cost challenges.

Market Opportunities

Growth in Pet Food Packaging Applications

The expanding global pet food industry presents a significant opportunity for food can manufacturers. Pet owners increasingly prefer premium wet pet food products packaged in metal cans due to freshness preservation and product safety benefits. Rising pet ownership rates and increasing spending on pet nutrition are driving demand for canned pet food packaging across North America, Europe, and Asia Pacific. Manufacturers are introducing smaller portion cans, easy-open lids, and premium printed packaging designs to improve product appeal.

Future growth opportunities are expected to emerge from premium and organic pet food categories. E-commerce pet food sales are also increasing demand for durable and transport-resistant packaging formats. Companies investing in sustainable metal packaging solutions for pet food products are likely to gain competitive advantages. The expansion of premium pet nutrition brands in emerging economies is expected to create additional long-term opportunities for the food cans market.

Rising Demand for BPA-Free and Smart Food Cans

The growing consumer preference for safer and technologically advanced packaging solutions is creating opportunities for BPA-free coatings and smart food cans. Food manufacturers are increasingly adopting non-toxic internal coatings to address health concerns and regulatory requirements. BPA-free can technologies improve food safety while maintaining corrosion resistance and product shelf stability. Several companies are also integrating QR codes and digital tracking features into food cans to improve supply chain transparency.

The future scope of smart packaging applications is expected to expand significantly with the growth of connected retail systems and digital consumer engagement strategies. Smart labels can help manufacturers provide nutritional information, traceability data, and promotional content directly to consumers. Investments in intelligent packaging technologies are likely to strengthen premium canned food categories and improve operational efficiency across global food supply chains.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2025 | USD 48.7 Billion |

| Market Size in 2026 | USD 50.6 Billion |

| Market Size in 2034 | USD 72.4 Billion |

| CAGR | 4.5% (2026-2034) |

| Base Year for Estimation | 2025 |

| Historical Data | 2022-2024 |

| Forecast Period | 2026-2034 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Type

The two-piece food cans segment dominated the global food cans market in 2024 and accounted for approximately 46.8% of total market share. Two-piece cans are widely preferred across beverage-compatible canned foods, soups, fruits, ready meals, and seafood applications due to their lightweight structure, reduced material consumption, and cost-efficient production capabilities. Manufacturers increasingly favor two-piece steel and aluminum cans because they support high-speed filling operations and improve transportation efficiency compared to traditional three-piece alternatives. Large food processing companies across the United States, Germany, China, and Japan continue to invest in automated can manufacturing technologies to increase production capacity and reduce operational costs. Demand for durable shelf-stable food products also supports segment dominance, particularly in urban retail markets where convenience foods continue to gain traction. Additionally, the expansion of organized retail chains and private-label packaged food brands has accelerated adoption of standardized two-piece can formats across global food distribution systems.

Easy-open cans are projected to emerge as the fastest-growing type segment during the forecast period and are expected to expand at a CAGR of 6.7% from 2025 to 2034. Rising consumer demand for convenience-oriented food packaging continues to support rapid adoption of pull-tab and easy-open lid technologies across canned vegetables, pet food, seafood, dairy products, and ready-to-eat meals. Food brands are increasingly focusing on user-friendly packaging solutions that improve accessibility for elderly consumers and support on-the-go food consumption trends. Easy-open can technologies also reduce the need for external tools, improving consumer safety and product usability. In Asia Pacific and Latin America, growing urbanization and expansion of convenience retail stores are increasing demand for portable packaged food products that utilize advanced closure systems. Packaging manufacturers are also introducing lightweight easy-open aluminum can designs to reduce material usage while improving recyclability. Future growth of this segment is expected to benefit from innovations in resealable lids, ergonomic opening mechanisms, and digital printing integration for enhanced product branding.

By Material

Steel cans held the largest share in the food cans market in 2024 and represented nearly 58.3% of global revenue. Steel remains the dominant packaging material due to its superior strength, durability, corrosion resistance, and compatibility with thermal sterilization processes used in canned food manufacturing. Steel cans are extensively utilized for packaging vegetables, soups, sauces, meat products, seafood, and pet food because they provide long shelf life and strong protection against contamination. Food manufacturers continue to rely on steel packaging for bulk transportation and export-oriented food distribution due to its ability to withstand harsh storage and shipping conditions. In Europe and North America, steel recycling infrastructure remains well developed, supporting circular economy initiatives and sustainable packaging targets. Major packaging producers are also introducing thinner steel can structures that reduce raw material consumption while maintaining performance standards. The growing demand for affordable shelf-stable food products across emerging economies further contributes to the continued dominance of steel food cans globally.

Aluminum cans are expected to register the fastest CAGR of 6.4% during the forecast period due to increasing demand for lightweight, recyclable, and premium-looking food packaging solutions. Aluminum offers advantages such as lower transportation costs, high recyclability rates, improved printing quality, and better resistance to moisture and oxidation. Food companies are increasingly utilizing aluminum cans for premium packaged foods, nutritional beverages, baby food products, and ready-to-eat meal packaging. In regions such as Asia Pacific and Latin America, rapid growth in modern retail infrastructure and convenience food consumption is supporting demand for lightweight aluminum packaging formats. Sustainability regulations encouraging reduced carbon emissions are also motivating manufacturers to shift toward aluminum packaging because recycled aluminum requires significantly lower energy during production compared to virgin material processing. Future developments in high-barrier aluminum coating technologies and smart labeling integration are expected to further strengthen growth opportunities within this segment over the next decade.

By End-Use

Processed food applications dominated the food cans market in 2024 and accounted for around 49.2% of total market revenue. Processed food manufacturers heavily rely on canned packaging solutions to preserve food quality, extend shelf life, and ensure safe transportation across domestic and international supply chains. Canned vegetables, beans, soups, pasta products, meat items, seafood, and ready meals continue to witness strong demand due to changing dietary habits and increasing urban lifestyles. The expansion of e-commerce grocery platforms and supermarket retail chains has further accelerated demand for packaged shelf-stable foods globally. In countries such as the United States, China, India, and Brazil, rising middle-class populations and busy working schedules continue to increase consumption of packaged convenience foods. Manufacturers are also focusing on BPA-free coatings, improved labeling technologies, and lightweight can structures to meet evolving regulatory and consumer expectations. The ability of canned packaging to reduce food waste and maintain nutritional stability continues to support segment dominance worldwide.

Pet food applications are anticipated to emerge as the fastest-growing end-use segment and are projected to expand at a CAGR of 6.9% during the forecast period. Rising pet ownership rates, increasing expenditure on premium pet nutrition products, and growing awareness regarding pet health are major factors driving demand for canned pet food packaging. Metal food cans are widely preferred for pet food because they provide excellent product protection, prevent spoilage, and maintain nutritional integrity over extended periods. Premium wet pet food brands increasingly utilize aluminum and steel can packaging to improve product shelf life and strengthen brand positioning in competitive retail environments. In North America and Europe, the premiumization trend within the pet care industry continues to encourage innovation in easy-open cans, recyclable packaging, and digitally printed labeling solutions. Emerging economies across Asia Pacific and Latin America are also witnessing increasing adoption of commercial pet food products, creating substantial long-term growth opportunities for food can manufacturers operating within the pet care sector.

Food Cans Market Segmentations

By Type

- Two-Piece Cans

- Three-Piece Cans

- Easy-Open Cans

- Retort Cans

By Material

- Steel

- Aluminum

- Tinplate

- Others

By End-User

- Processed Foods

- Seafood

- Pet Food

- Ready-to-Eat Meals

- Fruits & Vegetables

- Dairy Products

Regional Analysis

North America

North America accounted for 27.3% of the global food cans market share in 2025 and is projected to grow at a CAGR of 4.2% during the forecast period. The region benefits from strong demand for packaged foods, advanced food processing infrastructure, and widespread consumption of canned vegetables, soups, seafood, and pet food products. Rising preference for recyclable metal packaging and increasing consumer awareness regarding food safety are supporting market expansion. Food manufacturers are also investing in lightweight aluminum can technologies and BPA-free coatings to improve sustainability performance. The growth of online grocery platforms and convenience food consumption is further strengthening regional demand.

The United States remained the dominant country within North America due to its large processed food industry and established retail distribution networks. The country is witnessing increasing demand for canned ready meals, protein-rich seafood products, and premium pet food packaging. Several food companies are modernizing packaging operations through automation and smart labeling systems. Rising exports of canned food products and growing investment in recyclable metal packaging infrastructure are expected to support continued market growth across the United States during the forecast period.

Europe

Europe held 29.1% of the global food cans market share in 2025 and is expected to expand at a CAGR of 4.4% through 2034. The region has a mature food packaging industry supported by strong recycling infrastructure and strict sustainability regulations. Demand for canned vegetables, seafood, fruits, and organic packaged foods remains stable across European markets. Governments and packaging companies are increasingly promoting recyclable aluminum and steel packaging solutions to reduce environmental impact. Investments in lightweight can manufacturing and energy-efficient production systems are contributing to market growth.

Germany dominated the European market due to its strong packaged food manufacturing sector and advanced recycling ecosystem. German consumers continue to show high demand for convenient and shelf-stable food products, supporting strong consumption of food cans. Manufacturers are investing in digital printing technologies and sustainable coatings to improve product differentiation and regulatory compliance. Rising exports of processed foods and growth in premium canned pet food products are expected to strengthen market opportunities in Germany over the forecast period.

Asia Pacific

Asia Pacific dominated the food cans market with a 36.9% share in 2025 and is projected to grow at a CAGR of 5.1% through 2034. Rapid urbanization, increasing disposable incomes, and expanding organized retail sectors are driving packaged food consumption across the region. Countries such as China, India, Japan, and Indonesia are witnessing higher demand for canned vegetables, seafood, fruits, and ready-to-eat meals. Food processing companies are expanding manufacturing capacity to meet growing domestic and export demand. Rising investment in modern packaging technologies is also supporting regional market growth.

China remained the largest country-level market in Asia Pacific due to its large food processing industry and strong canned seafood production capabilities. The country continues to increase exports of canned fruits, vegetables, and ready meal products to international markets. Food packaging manufacturers are investing in lightweight can technologies and automated production systems to improve efficiency. Rising middle-class consumption and expanding e-commerce grocery sales are expected to support long-term growth in the Chinese food cans market.

Middle East & Africa

The Middle East & Africa accounted for 8.4% of the global food cans market revenue in 2025 and is projected to grow at a CAGR of 4.8% during the forecast period. Increasing urbanization, rising packaged food imports, and expanding supermarket networks are supporting demand for canned food products across the region. Governments are investing in food security initiatives and local food processing industries to reduce import dependence. Demand for long shelf-life packaged foods is particularly strong in regions with challenging climate conditions and growing tourism industries.

Saudi Arabia emerged as the dominant country within the region due to rising demand for imported packaged foods and processed meat products. The country is witnessing growth in modern retail chains and convenience food consumption, supporting higher food can packaging demand. Food manufacturers are increasingly adopting recyclable packaging materials to align with sustainability goals. Investments in domestic food manufacturing facilities and cold chain infrastructure are expected to create additional growth opportunities for the regional market.

Latin America

Latin America is projected to register the fastest CAGR of 5.8% during the forecast period due to rising processed food consumption and expanding retail distribution systems. The region is experiencing growing demand for canned seafood, vegetables, beans, fruits, and meat products. Increasing urbanization and changing consumer lifestyles are encouraging higher adoption of convenient packaged foods. Investments in food processing industries and metal packaging facilities are also contributing to market expansion across several Latin American countries.

Brazil dominated the Latin American food cans market due to its large agricultural sector and growing packaged food exports. The country continues to expand production of canned fruits, vegetables, and meat products for domestic and international markets. Rising supermarket penetration and increasing demand for shelf-stable packaged foods are supporting market growth. Manufacturers are also investing in sustainable aluminum can production and modern food processing technologies to improve competitiveness and operational efficiency.

Competitive Landscape

The global food cans market remains moderately consolidated, with leading companies focusing on production expansion, lightweight metal technologies, sustainable packaging innovations, and strategic partnerships with food processing companies. Major manufacturers continue investing in advanced can manufacturing equipment, digital printing technologies, and recyclable packaging solutions to strengthen their competitive positioning in both developed and emerging markets.

Ball Corporation remains one of the leading players in the market due to its extensive global manufacturing presence, strong aluminum packaging portfolio, and continuous investments in sustainable metal packaging technologies. The company has focused on lightweight can production and enhanced recycling capabilities to support growing environmental regulations and circular economy initiatives. Crown Holdings, Inc. and Silgan Holdings Inc. are also expanding their food packaging operations through automation upgrades and regional capacity expansions.

Companies such as Ardagh Group and CANPACK continue to strengthen market presence through innovation in easy-open can designs, improved barrier coatings, and premium food packaging solutions. Manufacturers are increasingly collaborating with food brands to develop customized packaging formats that improve shelf appeal and operational efficiency. Strategic acquisitions, regional production expansion, and investment in low-carbon manufacturing processes are expected to remain key competitive strategies across the global food cans industry during the forecast period.

Key Players List

- Ball Corporation

- Crown Holdings, Inc.

- Silgan Holdings Inc.

- Ardagh Group S.A.

- CANPACK Group

- CPMC Holdings Limited

- Kian Joo Can Factory Berhad

- Toyo Seikan Group Holdings Ltd.

- Massilly Holding SAS

- Trivium Packaging

- HUBER Packaging Group GmbH

- Colep Packaging

- Independent Can Company

- Orora Packaging Australia Pty Ltd.

- BWAY Corporation