Food and Beverage Packaging Materials Market Size and Growth

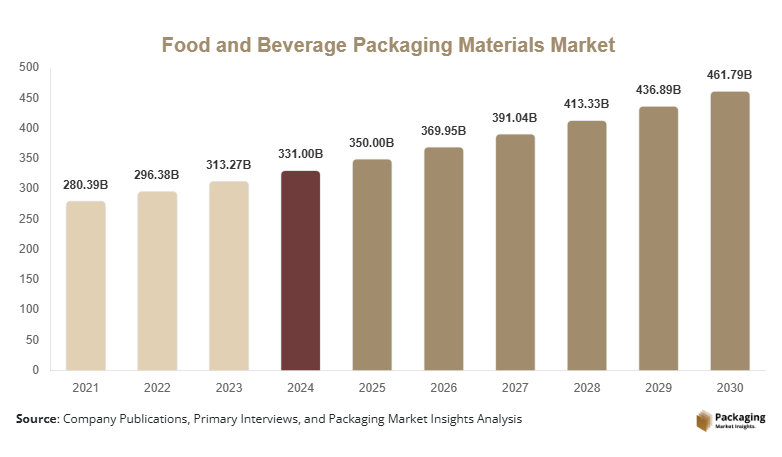

The global Food and Beverage Packaging Materials Market size was valued at USD 331 billion in 2024 and is projected to reach USD 461.78 billion by 2030, registering a compound annual growth rate (CAGR) of 5.7% during the forecast period (2025–2030). A significant global factor supporting this market growth was the increasing urbanization worldwide, which led to a surge in demand for packaged and convenience foods. This demographic shift directly fueled the need for efficient and protective packaging solutions across various food and beverage categories. The rising global population further contributed to the consistent demand for packaged food and beverages, necessitating advancements in packaging materials to ensure product safety and extended shelf life. The expansion of the e-commerce sector, particularly for groceries and ready-to-eat meals, also amplified the market’s trajectory by requiring robust and safe packaging for transit.

Key Highlights

- Asia Pacific held the dominant market share of 42% in 2024, while Latin America is projected to be the fastest-growing region with a CAGR of 6.5% during the forecast period.

- Among materials, plastics held the leading subsegment share; bioplastics is the fastest-growing subsegment with a CAGR of 9.2%. In applications, beverages was the leading subsegment; dairy products is the fastest-growing subsegment with a CAGR of 6.8%. For packaging types, rigid packaging was the dominant subsegment; flexible packaging is the fastest-growing subsegment with a CAGR of 6.3%.

- China was the dominant country, accounting for USD 75 billion in 2024, and is expected to reach USD 130 billion by 2030.

Explore more data points, trends and opportunities Download Free Sample Report

Market Trends

Sustainable Packaging Innovations: A Shifting Industry Standard

The Food and Beverage Packaging Materials Market has seen a strong trend towards sustainable packaging solutions. Consumers and regulators are increasingly prioritizing environmentally friendly options, driving manufacturers to invest in recyclable, biodegradable, and compostable materials. This includes a growing interest in bioplastics derived from renewable sources, as well as lightweight designs that reduce material usage and carbon footprint. Companies are also exploring refillable and reusable packaging models to minimize waste, reflecting a broader industry commitment to circular economy principles and enhanced brand perception.

Digitization and Smart Packaging Integration Enhancing Consumer Engagement

Another significant trend is the integration of digital technologies into food and beverage packaging. Smart packaging, incorporating features like QR codes, RFID tags, and NFC, is gaining traction for its ability to provide enhanced traceability, real-time product information, and interactive consumer experiences. These innovations enable brands to engage with customers directly, offer personalized content, and even monitor product freshness or authenticity. This trend is driven by consumer demand for transparency and convenience, as well as by brand efforts to combat counterfeiting and improve supply chain efficiency within the food and beverage packaging materials market.

Market Drivers

Rising Demand for Processed and Packaged Foods: Convenience as a Core Need

The escalating demand for processed and packaged foods, driven by busy lifestyles and increasing urbanization, is a primary driver for the Food and Beverage Packaging Materials Market. Consumers seek convenience in ready-to-eat meals, snacks, and beverages, which necessitates packaging that offers extended shelf life, portion control, and ease of use. This continuous shift in consumption patterns, particularly in emerging economies with growing middle-class populations, fuels the need for diverse packaging materials capable of meeting varying product requirements and maintaining food safety standards from production to consumption.

Technological Advancements in Packaging Materials Enhancing Performance and Safety

Innovations in packaging materials and manufacturing processes significantly propel the Food and Beverage Packaging Materials Market forward. Developments in barrier technologies, active packaging, and intelligent packaging solutions improve product preservation, extend shelf life, and enhance food safety. These advancements include new coatings that provide oxygen and moisture resistance, antimicrobial packaging that inhibits microbial growth, and lighter, more durable materials that reduce transportation costs and environmental impact. Such technological progress enables manufacturers to develop sophisticated packaging tailored to specific food and beverage products, ensuring freshness and quality for consumers.

Market Restraints

Fluctuations in Raw Material Prices Impacting Production Costs

The food and beverage packaging materials market faces a significant restraint due to the volatility in raw material prices. Packaging materials like plastics, paperboard, glass, and metals are derived from commodities such as crude oil, timber, silica, and borax. Geopolitical events, supply chain disruptions, and global economic shifts can cause unpredictable fluctuations in the cost of these raw materials. This instability directly impacts the production costs for packaging manufacturers, potentially leading to higher product prices, reduced profit margins, and challenges in long-term financial planning and investment in the food and beverage packaging materials market.

Market Opportunities

Growth of E-commerce and Online Food Delivery

The rapid expansion of e-commerce platforms and online food delivery services presents a significant opportunity for the food and beverage packaging materials market. As more consumers purchase groceries and prepared meals online, there is an increased need for packaging that can withstand transit, maintain product integrity, and ensure food safety during delivery. This includes specialized packaging for temperature control, tamper-evident seals, and durable yet lightweight designs that can protect items from damage, offering a new frontier for innovation and market expansion for packaging suppliers.

Emergence of Biodegradable and Compostable Packaging – Meeting Sustainability Goals

The growing global emphasis on sustainability and waste reduction is creating a substantial opportunity for biodegradable and compostable packaging solutions. With increasing consumer awareness and stricter environmental regulations, there is a rising demand for alternatives to conventional plastics that minimize ecological impact. This trend encourages research and development in bio-based polymers and plant-derived materials, allowing companies to meet corporate sustainability goals and attract environmentally conscious consumers. Investments in this sector promise not only compliance but also a strong competitive advantage in the evolving Food and Beverage Packaging Materials Market.

Report Scope

| Report Metric | Details |

|---|---|

| Market Size in 2024 | USD 331 Billion |

| Market Size in 2025 | USD 350 Billion |

| Market Size in 2030 | USD 461.78 Billion |

| CAGR | 5.7% (2025-2030) |

| Base Year for Estimation | 2024 |

| Historical Data | 2021-2023 |

| Forecast Period | 2025-2030 |

| Report Coverage | Revenue Forecast, Competitive Landscape, Supply Chain Disruption, Growth Factors, Environment & Regulatory Landscape and Trends |

| Geographies Covered | North America, Europe, APAC, Middle East and Africa, LATAM |

| Countries Covered | U.S., Canada, U.K., Germany, France, Spain, Italy, Russia, Nordic, Benelux, Rest of Europe, China, South Korea, Japan, India, Australia, Singapore, Taiwan, South East Asia, Rest of Asia-Pacific, UAE, Turky, Saudi Arabia, South Africa, Egypt, Nigeria, Rest of MEA, Brazil, Mexico, Argentina, Chile, Colombia, Rest of LATAM |

Explore more data points, trends and opportunities Download Free Sample Report

Segmental Analysis

By Material

In 2024, plastics dominated the food and beverage packaging materials market by material, accounting for a 38% share. This was attributed to its versatility, cost-effectiveness, and excellent barrier properties, making it suitable for a wide range of food and beverage products from bottles to films. Plastics offer lightweight solutions that reduce transportation costs and provide good product protection, contributing to their widespread adoption across various applications within the food and beverage sector.Bioplastics are projected to be the fastest-growing subsegment within the materials category, anticipated to achieve a CAGR of 9.2% during the forecast period. This growth will be primarily driven by increasing environmental concerns and stringent regulatory frameworks promoting sustainable packaging. As consumers and governments push for eco-friendly alternatives, manufacturers will increasingly adopt bio-based and biodegradable polymers to reduce their carbon footprint and comply with new sustainability mandates, offering significant potential for market expansion.

By Application

The Beverages application segment held the largest share of 35% in the Food and Beverage Packaging Materials Market in 2024. This was due to the immense global consumption of various beverages, including soft drinks, water, juices, and alcoholic beverages, which consistently require extensive packaging solutions. The segment's dominance is further supported by innovations in beverage packaging, such as lightweight PET bottles, aluminum cans, and aseptic cartons, all designed to ensure product safety, extend shelf life, and cater to consumer convenience. Dairy products are expected to emerge as the fastest-growing subsegment in the application category, projecting a CAGR of 6.8% during the forecast period. This growth will be fueled by the increasing global demand for packaged milk, yogurt, cheese, and other dairy derivatives, driven by growing health consciousness and rising disposable incomes. Packaging innovations, such as aseptic cartons and advanced plastic containers that extend product freshness and improve portability, will further boost this segment's expansion as consumers seek convenient and safe dairy options.

By Type

Rigid packaging held a dominant 60% share of the food and beverage packaging materials market by type in 2024. This was largely due to its superior protective qualities and ability to maintain product integrity for items like bottles, jars, cans, and rigid containers. Rigid packaging offers robust protection against physical damage and external contaminants, which is crucial for preserving the quality and safety of food and beverage products throughout the supply chain and on store shelves. Flexible packaging is projected to be the fastest-growing subsegment in the type category, anticipated to achieve a CAGR of 6.3% during the forecast period. This growth will be primarily driven by its cost-effectiveness, lightweight nature, and increasing demand for convenient, on-the-go food and beverage options. Flexible packaging, including pouches, films, and bags, offers reduced material usage and transportation costs while providing excellent barrier properties and design flexibility, making it an attractive choice for manufacturers looking to optimize their packaging solutions.

Food and Beverage Packaging Materials Market Segmentations

By Material

- Plastics

- Paper & Paperboard

- Glass

- Metal

- Bioplastics

By Application

- Beverages

- Dairy Products

- Bakery & Confectionery

- Fruits & Vegetables

- Meat, Poultry & Seafood

- Ready-to-Eat Meals

- Others

By Type

- Rigid Packaging

- Flexible Packaging

Regional Analysis

North America

North America held a 28% share of the Food and Beverage Packaging Materials Market in 2024 and is projected to exhibit a CAGR of 5.2% during the forecast period (2025–2030). The region is characterized by high consumer spending and a mature processed food industry. The United States was the dominant country in North America. Its growth was significantly influenced by the strong consumer demand for convenience foods and premium packaged products. The fast-paced lifestyles of American consumers drove the need for easy-to-use, single-serve, and shelf-stable packaging formats across a wide range of food and beverage items. This demand led to continuous innovation in packaging designs and materials to meet evolving preferences for freshness, portability, and aesthetic appeal.

Europe

Europe accounted for a 25% share of the Food and Beverage Packaging Materials Market in 2024 and is anticipated to grow at a CAGR of 5.0% from 2025 to 2030. The European market is highly regulated and strongly driven by sustainability initiatives. Germany was the dominant country in the European food and beverage packaging materials market. Its expansion was primarily propelled by robust environmental policies and a strong consumer inclination towards eco-friendly packaging solutions. Germany's leadership in circular economy principles and advanced recycling infrastructure encouraged manufacturers to adopt recyclable and reusable packaging materials, driving innovation in sustainable alternatives and reducing the reliance on virgin plastics.

Asia Pacific

The Asia Pacific Food and Beverage Packaging Materials Market held the largest share, at 42%, in 2024 and is expected to register a CAGR of 6.2% during the forecast period (2025–2030). The region is a powerhouse of economic growth and expanding populations. China was the dominant country in the Asia Pacific market. Its significant growth stemmed from rapid urbanization and increasing disposable incomes, which fueled a massive demand for packaged food and beverages. As millions moved to urban centers, convenience foods became a staple, leading to extensive adoption of modern packaging solutions for products ranging from dairy and confectionery to ready-to-eat meals, thereby expanding the Food and Beverage Packaging Materials Market.

Middle East & Africa

The Middle East & Africa Food and Beverage Packaging Materials Market held a 3% share in 2024 and is projected to achieve a CAGR of 5.9% during the forecast period (2025–2030). The region is experiencing economic diversification and a rise in tourism. The United Arab Emirates (UAE) was the dominant country in the Middle East & Africa. Its market growth was considerably boosted by its thriving tourism sector and an expanding food service industry. The influx of international visitors and the establishment of numerous hotels and restaurants created a high demand for packaged food and beverage products, requiring sophisticated and hygienic packaging solutions to cater to diverse culinary preferences and maintain product quality in a demanding hospitality environment.

Latin America

Latin America accounted for a 2% share of the Food and Beverage Packaging Materials Market in 2024 and is projected to be the fastest-growing region, with a CAGR of 6.5% during the forecast period (2025–2030). This growth is attributed to improving economic conditions and changing consumer habits. Brazil was the dominant country in the Latin American market. Its expansion was primarily driven by an expanding middle class and the increasing consumption of processed and convenience foods. As more Brazilians entered the middle-income bracket, their purchasing power increased, leading to higher demand for packaged snacks, beverages, and ready-to-cook meals, which in turn stimulated the need for efficient and attractive packaging materials.

Competitive Landscape

The food and beverage packaging materials market is characterized by the presence of a few prominent players and a large number of regional participants. Strategic initiatives like mergers, acquisitions, and new product launches are common. Amcor Plc is a key market leader, recently focusing on sustainable packaging solutions.

- For instance, in 2024, Amcor announced an expansion of its product line with new recyclable high-barrier flexible packaging films, aiming to meet growing demand for eco-friendly options. Other important players are concentrating on technological advancements and expanding their global footprint to gain a competitive edge in the food and beverage packaging materials market.

Key Food and Beverage Packaging Materials Market Companies

- Amcor Plc

- Ball Corporation

- Tetra Pak Group

- Crown Holdings Inc.

- Ardagh Group S.A.

- O-I Glass, Inc.

- Smurfit Kappa Group plc

- DS Smith Plc

- WestRock Company

- AptarGroup, Inc.

- Berry Global Group, Inc.

- Huhtamaki Oyj

- Constantia Flexibles Group GmbH

- Sealed Air Corporation

- Mondi Group

- Winpak Ltd.

- Silgan Holdings Inc.